FFIN - First Financial Bankshares: At Fair Value Finally

2023-10-04 22:40:50 ET

Summary

- First Financial Bancshares is a well-run Texan bank with a strong presence in smaller communities.

- FFIN's stock price has dropped 40% this year, trading at a 10-year low earnings multiple.

- The current price is close to the fair value, but uncertainty in the sector might soon make it attractive.

Intro

First Financial Bankshares ( FFIN ) is a very profitable Texan bank with a strong presence in several smaller communities around West Central Texas. The bank was written up several times on Seeking Alpha and most of the analysts do agree that it is an exceptionally well-run bank, though the valuation was the sticking point.

This year the stock price of FFIN has gone down about 40% and is trading at a 10-year low earnings multiple. At a PE of 16X is still not a steal but we believe that at these valuation levels, FFIN should be placed on investor radars as economic uncertainty might soon turn it into a good bargain.

In this article, we will first talk about what makes FFIN unique and then estimate the value of the bank to determine if the stock price is finally attractive.

Why is it so much better than the rest?

FFIN currently trades at a PE multiple of 16X when industry majors such as Bank of America or Wells Fargo go for 8 -10X and the KBW Regional Banking Index has a PE of 8.4X. Part of the reason for this premium is the bank's exposure to the growing economy of Texas. On the other hand, FFIN is even more pricey than its Texan peers. Assuming that markets are somewhat efficient, there must be a reason for it.

Just by looking at some straightforward operating metrics, we can see that the quality of FFIN stands out:

- It does have one of the highest Return on Equity ((ROE)).

- It does have the lowest cost of funds.

- It does have one of the lowest expense ratios.

| Texas Banks |

| PE LTM |

| P/B tangible |

| RoE LTM |

| Cost of Funds q2 |

| Expense Ratio LTM |

| Loans/Assets % |

| Non-interest revenue |

| First Financial |

| 15.5x |

| 3.2x |

| 16% |

| 1.1% |

| 46% |

| 52% |

| 23% |

| Cullen/Frost Bankers |

| 8.2x |

| 2.2x |

| 21% |

| 1.4% |

| 58% |

| 35% |

| 22% |

| Prosperity Bancshares |

| 10x |

| 1.4x |

| 7% |

| 1.5% |

| 45% |

| 52% |

| 13% |

| Guaranty Bancshares |

| 10x |

| 1.2x |

| 13% |

| 1.9% |

| 64% |

| 72% |

| 18% |

| Veritex Holdings |

| 6x |

| 0.9x |

| 11% |

| 3% |

| 52% |

| 76% |

| 12% |

SEC filling and our estimates

First Financial, just like most of its community bank peers, usually engages in deposit-gathering activities from local residents and businesses and uses these to originate loans to the said customers and invest in securities. The yields generated on the financial instruments are usually determined by the market as the services provided by different banks are not all that differentiated and lending is more or less a commodity business. Since the lending revenue line is pretty much out of the control of individual banks, the main focus of management traditionally has been on the cost side. The cost side is where FFIN excels.

Banks with lower funding costs are able to generate higher risk-adjusted profit margins per given asset portfolio, thus generating higher return on equity. A stronger equity base, assuming that not all profits are paid out, allows the most profitable banks to grow their loan books at a faster pace, and thus higher RoE results in greater EPS growth. FFIN, if it can maintain its high level of profitability, will be able to grow faster than its peers and therefore it commands this premium in valuation.

The size of a justifiable valuation premium is the main topic of discussion when it comes to FFIN. In essence, it comes down to the future expected RoE and the risk profile of the business. The higher the expected RoE and the more secure the returns are, the higher the earnings multiple that investors should be paying for a bank.

To assess the earnings multiple we would be willing to pay, we will look at factors driving the performance of FFIN individually and asses the sustainability and risk factors behind them.

Lowest cost of funds

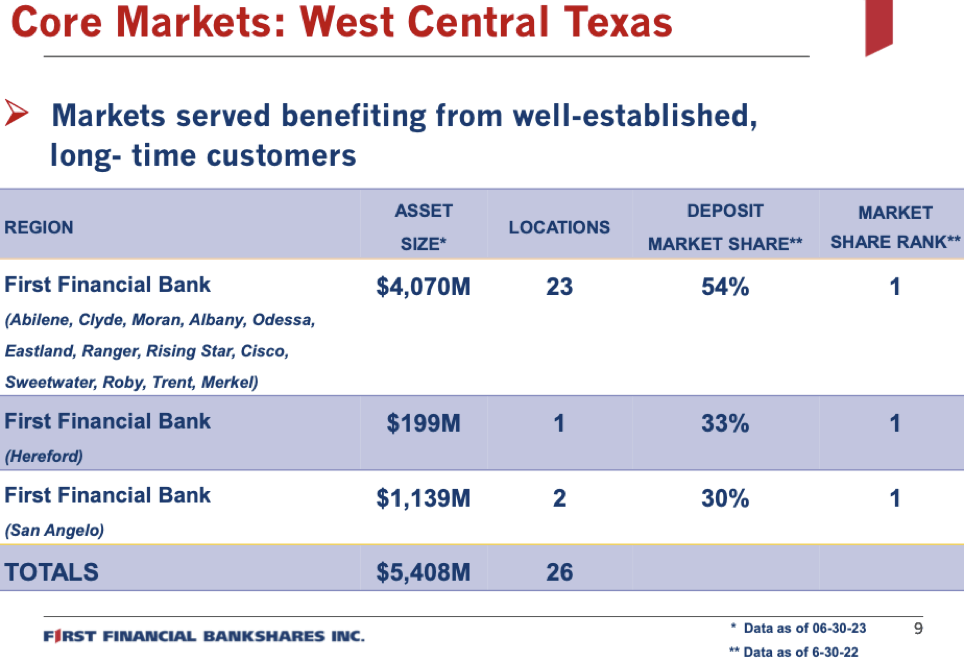

FFIN operates a retail focused branch network with 80 locations predominantly in smaller and not as competitive markets. FFIN is often the largest bank in its target markets and is able to offer a suite of services to its customers. The increased number of products and services provided by a single bank creates loyalty to that bank even if it does not pay the highest rate of interest on the checking/saving accounts. This is essentially the universal banking model of Bank of America and the likes applied to a much smaller local community.

{kind=link}

The strong local brand and customer loyalty enable FFIN to fund itself by offering customers lower rates on their savings accounts. Customers using the FFIN as their default checking account provide the bank with interest-free funds. Only the largest banks in the market are used as the default checking account providers.

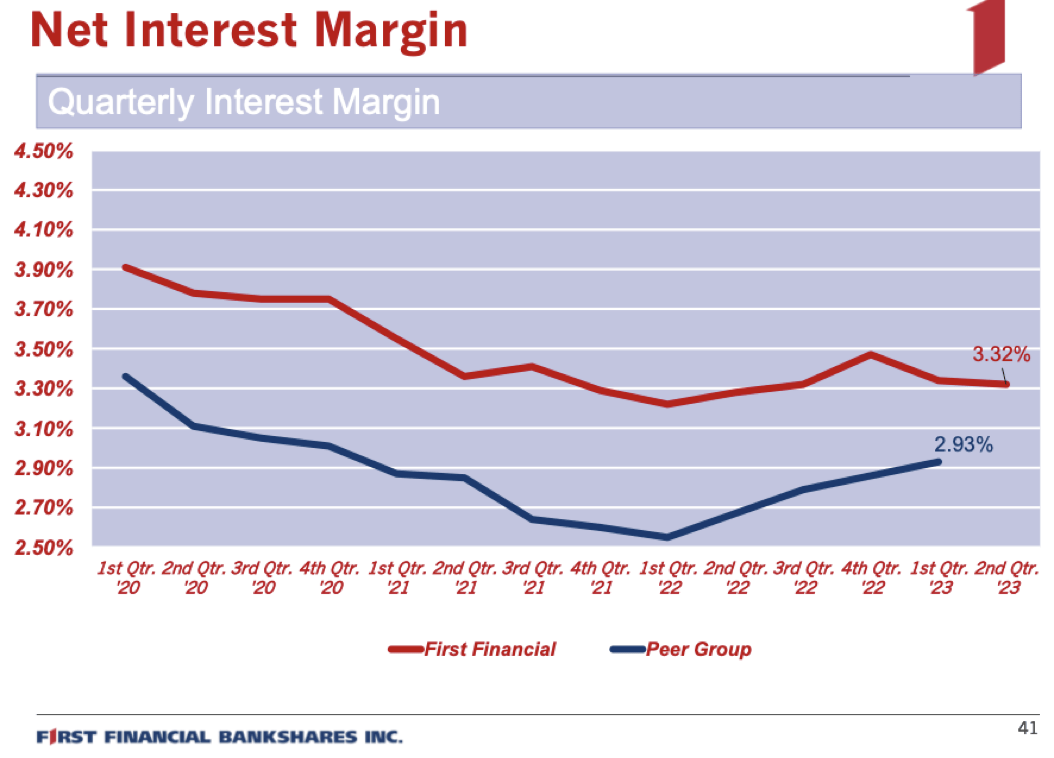

The low funding cost that FFIN has translates into leading net interest margins. As long as FFIN can source most of its deposits from markets where it has the leading position, it will likely continue having a low funding cost and a leading net interest margin. We believe that this is a sustainable advantage of FFIN.

{kind=link}

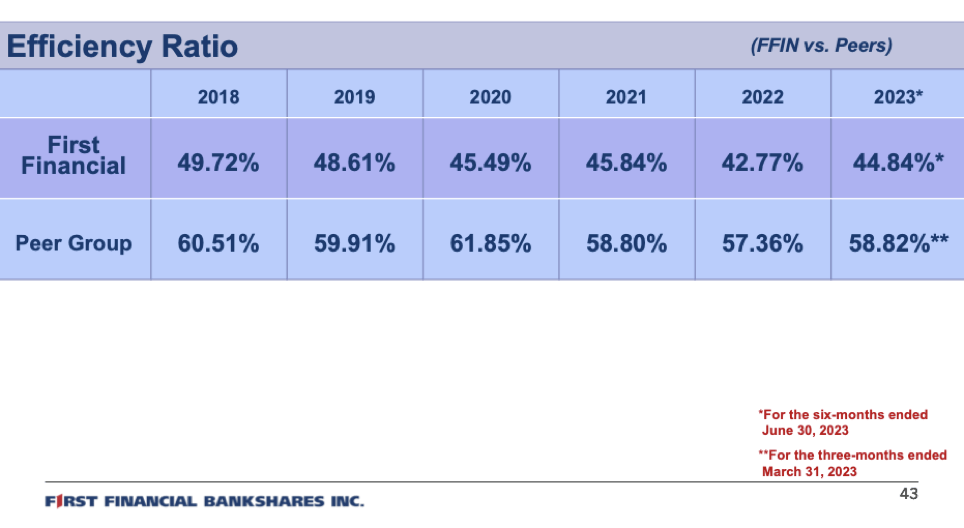

Lowest expense ratios

FFIN also happens to be a really efficient operator. Its expense ratio of 46% is quite impressive for a bank focused on retail deposit gathering.

FFIN has around $11 billion of total deposits spread across 334K accounts. The average deposit size is only $34K and only 35% of deposits do not meet the FDIC insurance threshold. This is by all means a secure deposit base and the fact that it is generated with such a low expense ratio is impressive.

A higher rate of efficiency enables the bank to generate a higher profit margin per given net interest spread. FFIN has been as profitable as it is in large part due to its better efficiency than its peers.

{kind=link}

The exact reasons for higher efficiency are not always easy to pin down as it is often a result of many incremental savings which is a direct result of cost-conscious corporate culture and good management.

FFIN has been leading in efficiency for a number of years and it has been managed by the same team for a number of years also. Scott Dueser, the CFO and Chairman of the bank has been leading the business since 2001. Before that, he was one of the regional managers. Mr. Dueser is also a significant shareholder with FFIN shares worth $50 million.

Most of the executive as well as regional managers of FFIN have been with the business for a number of years. It is reasonable to expect the bank to perform well as long as the same management team stays in charge. Mr. Dueser is 69 though we would imagine that most of the long-serving managers would be willing to step in and continue maintaining the same culture.

Part of the reason for efficient operations is the centralisation of the back-of-the-office operations of the group. These operations have a fixed cost basis and therefore can be scaled more efficiently across a larger group.

From the FY2022 10K of FFIN:

Although we consolidated our bank charters into one charter in 2012, we continue to regionally manage our operations with local advisory boards of directors, local regional presidents and local decision-making processes. We have consolidated substantially all of the non-customer facing operations, such as investment securities, accounting, check processing, credit administration, risk management, treasury management, marketing, customer contact center, technology, training and human resources, which improved our efficiency and allows the regions to concentrate on serving the banking needs of their local communities.

We expect the bank to maintain this operational set-up and continue operating efficiently.

The valuation framework

After establishing that the competitive advantages of FFIN are sustainable we need to get asses for the value of the business to decide what earning multiple would be reasonable for this superior business. We will apply a rather intuitive valuation methodology to this bank.

We express the operating earnings of the bank as a percentage of interest-earning assets. At H1 2023 this ratio has been 2.4%. The interest-earning assets of FFIN are primarily funded with deposits and retained earnings (equity). We will also assume that going forward only these two funding methods will be used and future asset growth will be proportional to the deposit and retained earnings growth.

| Funding Cost and Income |

| H1 2023 |

| First Financial |

| Funding cost |

| 3.0% |

| Deposits and interest-bearing liabilities |

| 11,458,204 |

| Interest Cost |

| 58,361 |

| Non-Interest Expense |

| 114,869 |

| Non-interest income |

| 57,954 |

| Net operating expenses |

| 56,915 |

| Net net funding cost |

| 2.0% |

| Loans as a share of assets, % |

| 51% |

| Yield on total assets |

| 4.4% |

| Operating income spread |

| 2.4% |

| Earning assets |

| 12,047,485 |

SEC filings and our estimates

There are 2 main factors driving the valuation, the interest-earning asset growth and net operating income spread.

Assuming that deposits will grow at a rate of 7%, as was the case during the 5 years before the COVID deposit boom of 2020. Earning assets will grow at above this rate as retained earnings will also be added. The asset-to-tangible equity ratio of the bank is 12.2X, above longer-term averages due to recent security value impairments. Assuming that the bank is in deleveraging mode and applies only a 7x multiple, the $140 million of retained earnings of FY2022 would be turned into $1.0 billion of earning assets. The current earning assets are $12 billion, so the equity base would support an asset growth of 8%. We note that we deem the current level of leverage somewhat excessive, and assume that over the next few years, the growth of the business might be constrained.

Assuming the 8% interesting earning asset growth rate, FFIN would have $17.6 billion of earning assets in 5 years. With the operating income spread of 2.4% FFIN would be likely to deliver $420 million of operating income and $320 million of earnings.

The net operating spread of the business is likely to increase as the old low-yielding securities mature and as new deposits are invested at a currently prevailing higher rate. We believe that the deposit cost will continue to be low. An operating spread increase to say 2.7% would raise the 5-year forward profit expectation to $380 million.

Assuming that the bank would be able to continue performing well due to the sustainable competitive advantages, we would apply a 5-year forward earnings multiple of 15x. In this case, the future value of the bank would be $5.7 billion. Given the current market price of $3.5 billion and the dividend yield of 2.2%, the expected annual return over the next 5 years would be about 12% from an investment in FFIN at the current share price.

This return is probably in line with the risk profile of the business, given the competitive and cyclical nature of the banking industry.

The key risks

As the bank expands and gradually grows out of the smaller markets it might be forced to increasingly focus deposit-gathering activities on the more competitive urban markets of Dallas and Houston. In the larger markets, FFIN will not have a strong competitive position and thus will have to offer depositors significantly higher rates. We will continue monitoring the developments to assess the profitability of new FFIN branches and if needed will re-assess our valuation.

Depending on the economic climate and prevailing interest rates, the bank's investment securities might have to be impaired further, weakening the bank's equity position, and constraining its future asset growth or forcing it to invest in low-yielding short-term cash-like instruments. Future loan impairments due to unforeseen circumstances would have a similar effect.

Conclusions

First Financial is a premium-quality bank capable of outgrowing its industry peers and delivering better returns to shareholders. It is also selling at a premium valuation multiple which would reduce the intrinsic returns to long-term holders of the stock. Our base case valuation estimates indicate the expected returns on investment in FFIN at the current price are neither poor nor exceedingly attractive and we would consider them to be fair. First Financial is a good quality bank and we intend to continue following the development of this business. On the other hand, we do not see much margin of safety at the current price.

For further details see:

First Financial Bankshares: At Fair Value Finally