TD - First Horizon: A Great Risk-To-Reward Prospect Amidst TD Bank Uncertainty

2023-04-14 06:24:45 ET

Summary

- There are fears that the deal that involves TD Bank acquiring First Horizon will fall through because of regulatory concerns and changing economics.

- These fears are not wholly unreasonable and investors may need to brace themselves for a haircut on the deal.

- Even with a haircut, though, there does seem to be an upside from here so long as the deal is completed.

Mergers and acquisitions activities can be particularly complicated. But at the same time, they can also result in attractive returns for investors. Normally, you would expect a deal that has been struck to be completed at the terms initially agreed upon. But this is not always the case. Between regulatory issues, economic issues, and company-specific issues, there is always some risk that the picture could change and necessitate a reassessment of the picture. In the market's eyes, there is a rather significant risk that shareholders of First Horizon Corporation ( FHN ) will be subjected to such an adjustment as it works to complete its transaction with TD Bank ( TD ) that would see TD Bank acquire it entirely. Although there is some risk that the deal could fall apart, or that a downward revision in deal terms could come about, I would make the case that, on a risk-adjusted basis, the picture for shareholders of First Horizon is incredibly appealing at this time.

A look at concerns

In a typical merger or acquisition, you would expect the shares of the company that's being purchased or absorbed to trade awfully close to the buyout price that was agreed upon between it and its acquirer. Such was the case for shares of First Horizon, with the stock trading just pennies shy of the $25 purchase price initially agreed upon between it and TD Bank. But this relationship broke down rather significantly at the tail end of February. At one point, shares of First Horizon even fell below $15.

This decline seems to have been driven by two primary factors. The first, like clockwork, involves the fact that the acquisition of First Horizon was expected to close no later than February 27th of this year. That would mark one day shy of the one-year anniversary of the announcement that it would be taken over by TD Bank. According to the original terms of the agreement, if the deal had not been completed by then, then it could be canceled by the parties. The cause of this failure falls on the regulatory side, with First Horizon even acknowledging that the new extended deadline of May 27th that was agreed upon by both sides may not be long enough for regulators to approve a transaction. The second reason behind the pain likely involves concerns over the health of the company since, in early March, the banking sector began seeing a great deal of turmoil that started with the collapse of Silicon Valley Bank's parent, SVB Financial Group ( SIVBQ ). A banking crisis has the potential to significantly change the health of any of the companies affected. And, when coupled with continued interest rate increases, a deal in general becomes less attractive than it otherwise would be.

I am not qualified to speak on regulatory matters. It is unclear whether regulators will approve or deny the transaction. Certainly, to have an extension, and then announce that the extended date might not be long enough, is not exactly confidence-inspiring. On the financial side of things, however, there is some cause for concern. To see what I mean, we need only look at recent financial performance reported by management.

{kind=link}

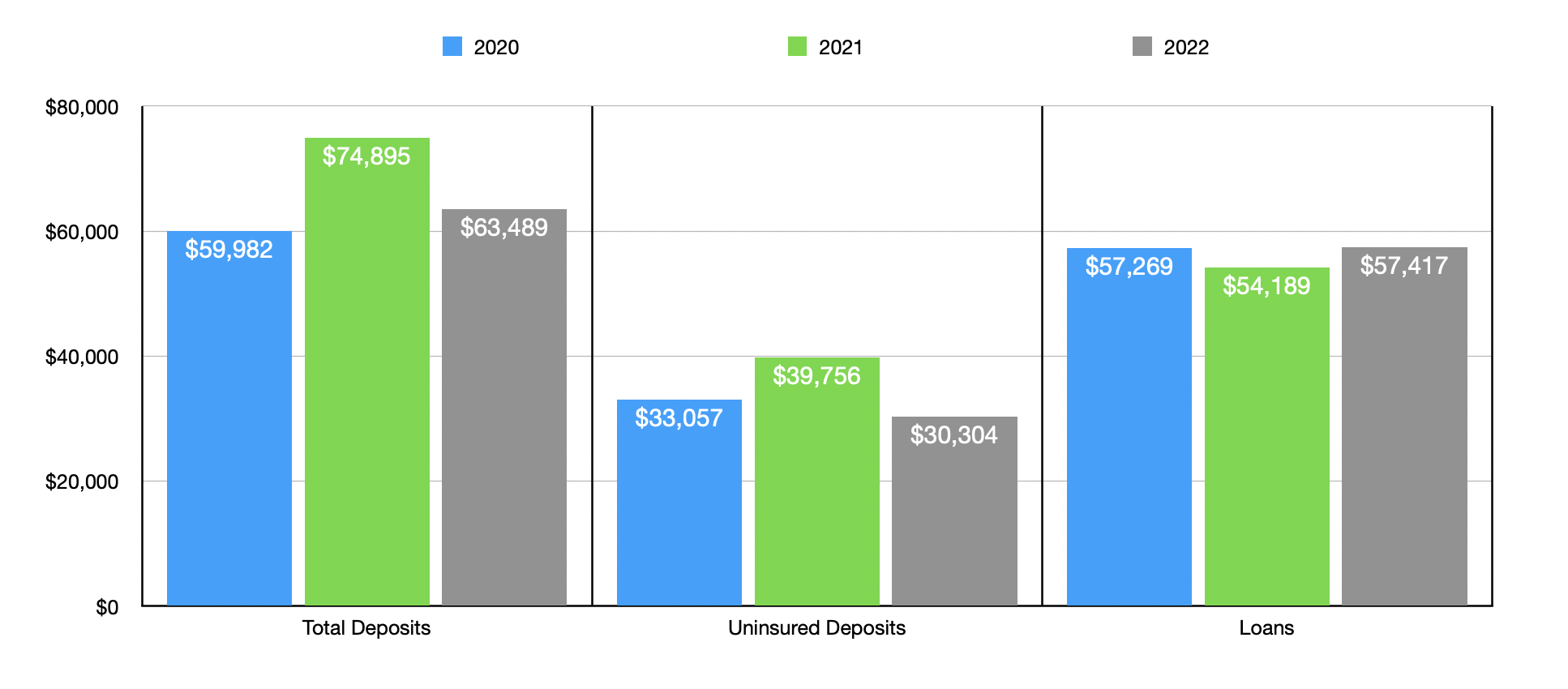

For starters, keep in mind that the original deal between First Horizon and TD Bank was struck in late February of 2022. So the financial results that would be most relevant in the decision-making process between both parties would be for the 2021 fiscal year. In many respects, that marked a great time for First Horizon. Deposits, for instance, came in at $74.90 billion that year. Loans, meanwhile, totaled $54.19 billion. Unfortunately, the company would show some weakness following that point. In 2022 , for instance, total deposits dropped 15.2% to $63.49 billion. Loans, meanwhile, did increase some, hitting $57.42 billion. This is great, but the decline in deposits is particularly worrisome.

According to management, such a decline should have been anticipated. In their 2022 annual report, they made the case that, even though interest rates were low at the time, federal assistance and stimulus programs in 2020 and 2021 caused deposits to grow materially. This does have some ring of truth to it. In 2020, for instance, deposits were $69.98 billion. And the year before that, they were a paltry $32.43 billion. Though not mentioned by management in the annual report, you could also argue that rising interest rates would cause market participants to withdraw some of their deposits and look for stronger yield elsewhere.

{kind=link}

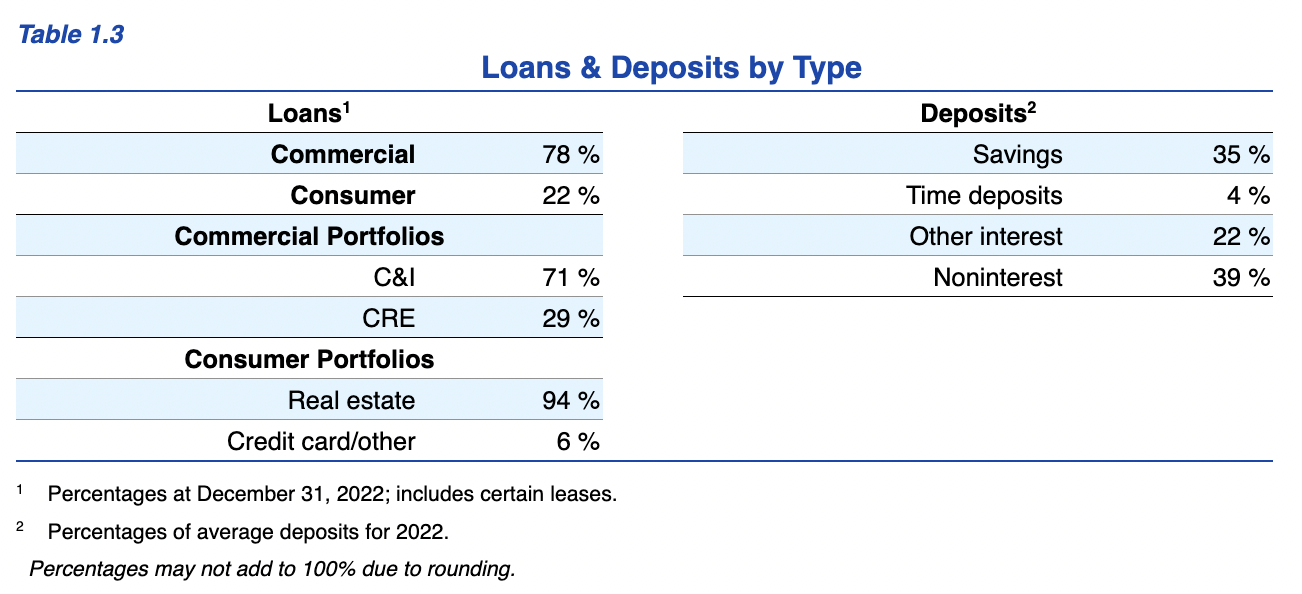

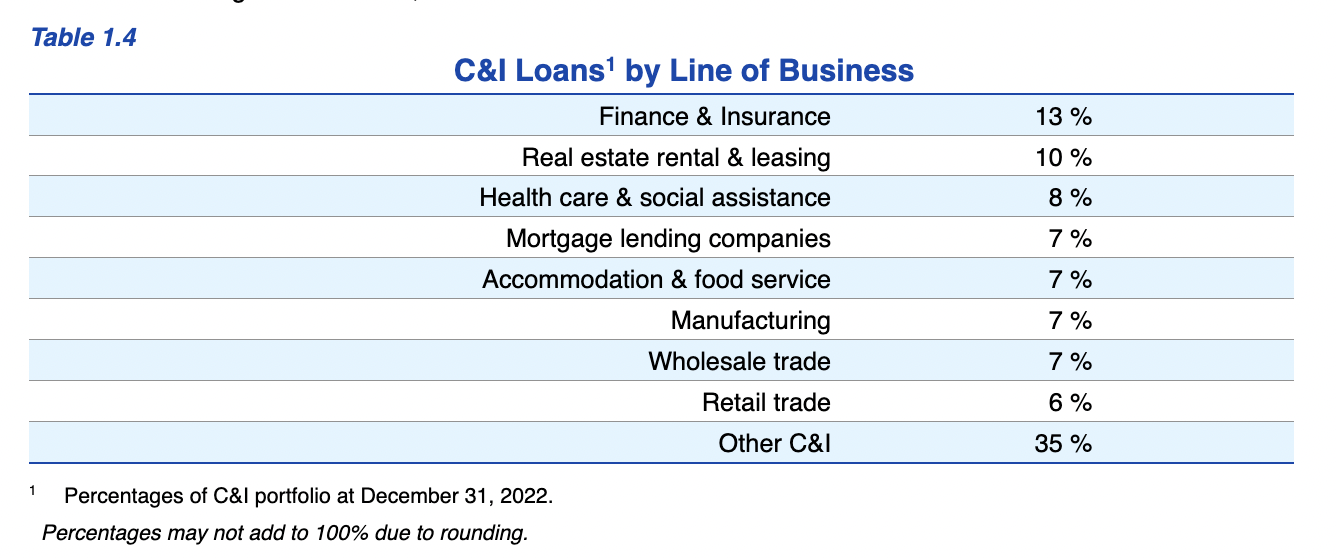

Keep in mind that none of this factors in what happened earlier this year. With the collapse of Silicon Valley Bank, as well as other financial institutions, any company that is similar in nature to the firms that fell would naturally become suspect. To be fair to First Horizon, the company has not revealed any data that would suggest that its deposits are related to early-stage companies or other similar firms that would be financially pressured during these times. However, 78% of the loans on its books are to the commercial space. Of that 78%, the lion's share is classified as commercial and industrial. Of this amount, 13% does relate to the finance and insurance space. The next largest category, however, is real estate rental and leasing at 10%. This is followed by healthcare and social assistance at 8%, with four other categories tying right behind that at 7% each. The remaining 29% of the 78% of commercial loans on its books involve commercial real estate. The remaining 22% of its loans in total, meanwhile, are on the consumer side, with the vast majority associated with real estate.

{kind=link}

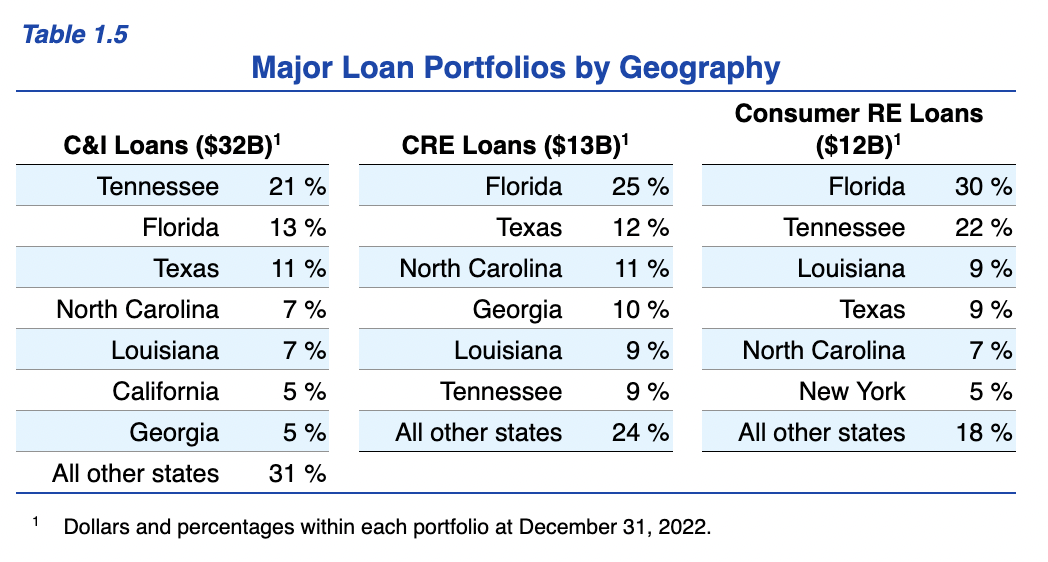

A lot of the banks that have fallen into trouble have a significant amount of exposure to the West Coast. The good news for investors is that this is not the case when it comes to First Horizon. Using data from 2022, I found out that the greatest exposure the company had was to the state of Florida. $11.01 billion, or 19.3% of all loans, involved borrowers in that state. This was followed by 18.5% in Tennessee, with Texas, Louisiana, and North Carolina, all representing significant amounts of exposure for the company as well.

{kind=link}

The geography and composition of the company's loan portfolio make me more comfortable with it from a fundamental perspective. But one thing that is not good is that a sizable portion of its deposits is classified as uninsured. Uninsured deposits are what fueled this banking crisis. Since the deposits are above the $250,000 limit typically covered by the FDIC, there is normally no guarantee that they will be protected should the bank fail. This could lead to a significant loss for depositors that could cause a bank run to develop. $30.30 billion, or 47.7%, of the company's overall deposits were uninsured last year. As high as this number is, it does mark an improvement over what was seen in 2021. For that year, 53.1%, totaling $39.76 billion, of its deposits were considered uninsured. It would be excellent to know to what extent the company has been impacted by recent economic developments. But management has not provided any substantive detail on this and we are unlikely to find anything further until the company reports earnings for the first quarter later this month.

{kind=link}

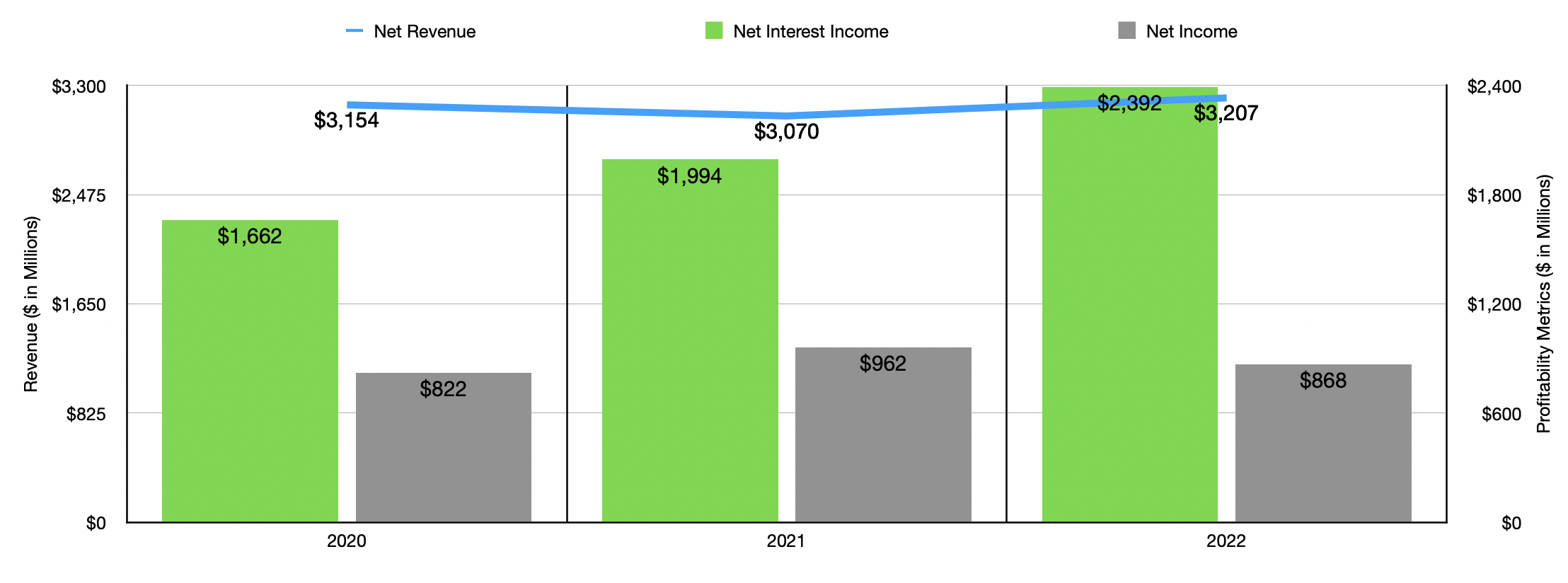

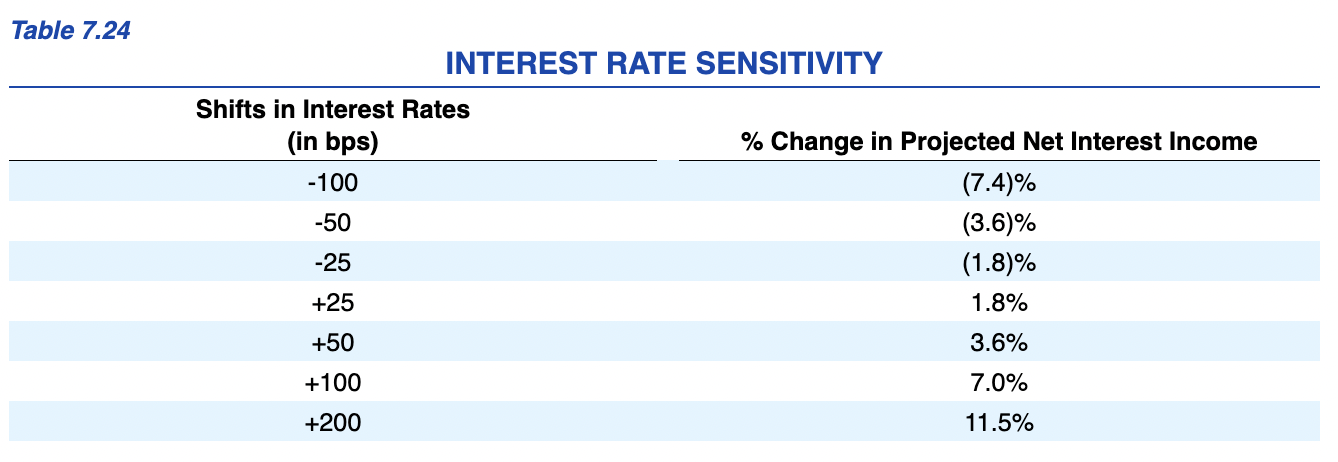

Even though the company did see a decline in deposits year over year, it is important to note that overall revenue for the firm has grown in recent years. Net interest revenue, for instance, grew from $1.66 billion in 2020 to $1.99 billion in 2021. In 2022, it came in at $2.39 billion. The larger loan balance in 2022 certainly helped. But the company undoubtedly benefited significantly from a rise in interest rates. In fact, in a sensitivity analysis that management provided, they revealed that for a 1% rise in interest rates, net interest income would grow by about 7%. The decline in other revenue-generating activities did offset this to some degree. But overall, the $3.21 billion in net revenue that the company reported last year was the highest it had been in the three years we were looking at.

{kind=link}

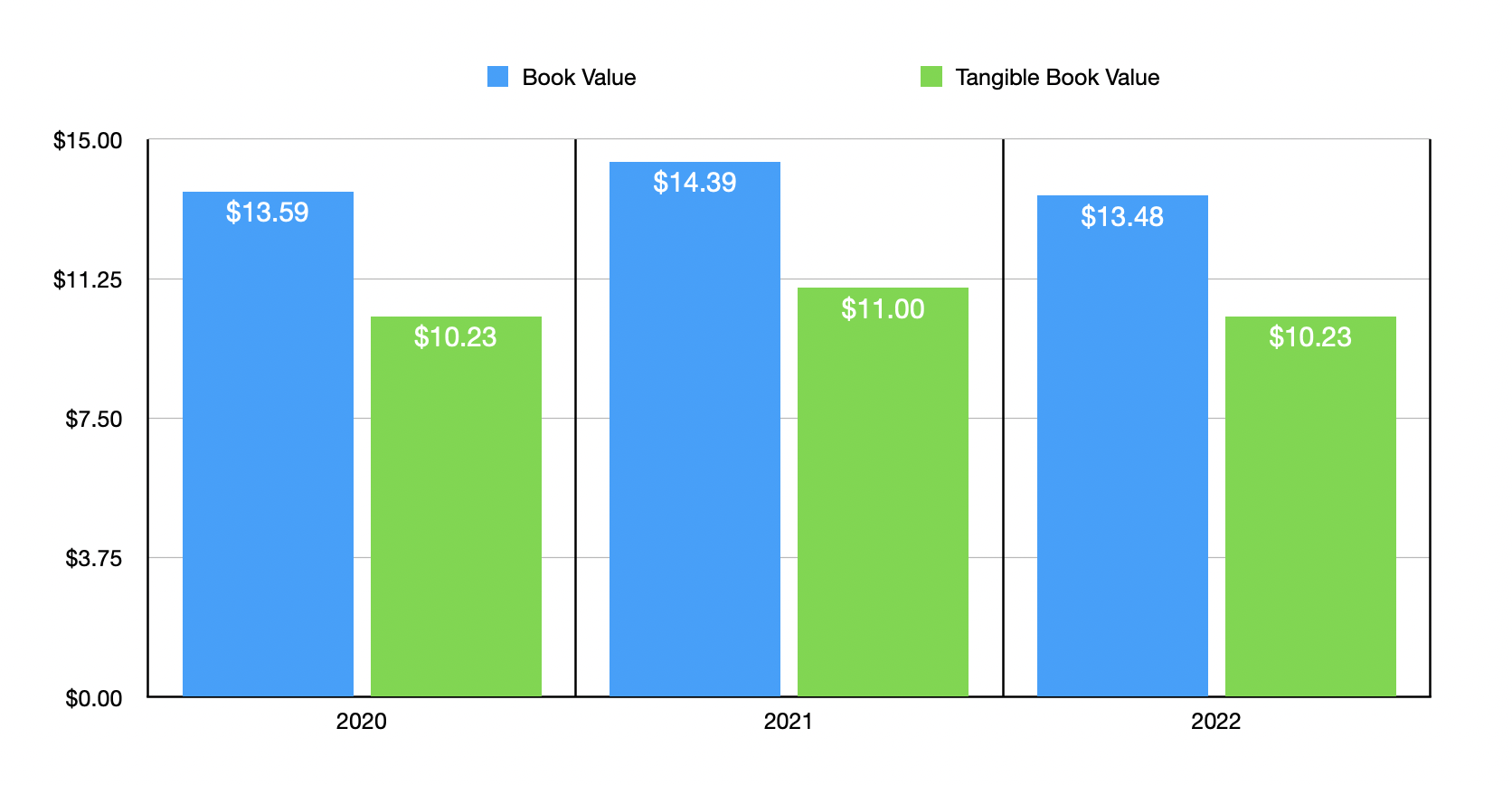

On the bottom line, the picture has been a bit more mixed. Net income jumped from $822 million in 2020 to $962 million in 2021. But then, in 2022, the metric declined to $868 million. You would think that the continued accumulation of profits would cause book value to rise. But this was not the case. Book value dropped from $14.39 per share in 2021 to $13.48 per share last year, while tangible book value dropped from $11 per share to $10.23 per share. Given a change in share count, plus adjustments to account for the original agreement, the effective buyout price for the company is a bit over $25 per unit right now. At the time the annual report was filed, it was about $25.15 per share. All of this implies a step up in the overall price that must be paid by TD Bank from $13.4 billion when the transaction was initially agreed upon to $14.2 billion today. That means that the company is slated to be acquired at 16.4 times earnings and at 2.5 times tangible book value.

{kind=link}

Takeaway

Although deposits were already declining prior to the banking crisis, and uninsured deposits on the books of First Horizon are rather significant in size, I don't believe that investors should fear significant pain for when the company reports results for the first quarter in the coming days. Having said that, there is no denying that the business has changed fundamentally since the deal was originally announced. Although loans have increased, deposits have declined. Both book value per share and tangible book value per share has dropped. Net profits are lower, and the effective buyout price is higher. You also have the aforementioned regulatory concerns that may or may not be cleared up in a timely manner.

This is not to say that the deal is going to fall through. At its core, First Horizon looks to be a solid company with attractive upside in the long run. In March of this year, TD Bank's CEO, Bharat Masrani, said that his company remains 'committed' to the transaction. However, when pressed on a potential price adjustment, he stated the following, "well we've just initiated the negotiations and, you know, once the negotiations are finalized, you know, we will be sure to give you further details". Truth be told, I wouldn't be surprised if some price adjustment does take place. But between where shares are right now, and the implied buyout price, we are looking at upside of 36.6%. Even if the deal does fall through, it would be difficult to imagine a scenario where the stock warrants material downside. This creates a very favorable risk-to-reward opportunity at this moment that, in my mind, justifies a 'strong buy' rating with the caveat that the bullishness of this rating is more associated with the risk-to-reward balance than the overall valuation of the firm from a value investment perspective.

For further details see:

First Horizon: A Great Risk-To-Reward Prospect Amidst TD Bank Uncertainty