FHN - First Horizon Makes For A Strong Prospect Heading Into Third Quarter Earnings

2023-10-11 15:55:25 ET

Summary

- First Horizon is due to report third quarter earnings in the coming days, and analysts have a rather negative outlook for the bank.

- Despite these concerns, the bank has performed well recently, though a lot of its bottom line improvement has come from a one-time gain.

- FHN shares look cheap, and while uninsured deposits are still high, they're coming down quickly while overall deposits are growing nicely.

One of the most depressed banking stocks that I have seen recently is none other than First Horizon ( FHN ). Earlier this year, shares plummeted after it was decided that it and TD Bank ( TD ) would not, in fact, consummate their merger. There already was a great deal of uncertainty at that time regarding whether or not the merger would take place. But that didn't stop the stock from falling more than 33%, down to around $10 per unit. That compares to the $25 per share that the enterprise was going to be absorbed for.

In response to the merger being called off, I ended up writing an article about First Horizon. And in that article, I called the company a "strong buy" because, in addition to receiving a $225 million payment from TD Bank because of the fallout of the deal, fundamental performance of the business was largely positive. This is not a suggestion that there was not some weakness. Deposits were on the decline and a rather sizable amount of deposits were classified as uninsured. But because of how cheap the stock was and the direction that most of its financial metrics were moving, I made the case that compelling upside would be on the table. Since then, however, we have not seen any of that upside. In fact, the stock is down another 1.9% at a time when the S&P 500 is up 5.3%.

As with any breakup, recovering does take time. The market needs time and proof from management that the weaknesses that justified such a plunge after the fallout of the merger have been addressed or are being addressed. When the company announced financial results for the second quarter of the current fiscal year, we saw some evidence that the picture was, indeed, improving. But clearly not enough to make investors optimistic again. Well, later this month, on Oct. 18, before the market opens, management will get yet another chance to prove to market participants that the worst for the company is behind it and that positive days lie ahead. Leading up to that time, there are some things that investors would be wise to pay careful attention to.

First Horizon Q3 preview: Revenue and profits are important

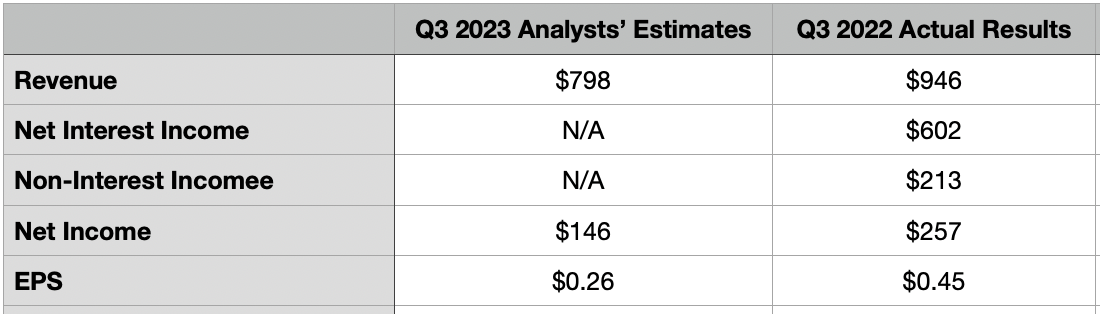

At the top of the list, investors should keep a close eye on the revenue and profit figures reported by management. For the third quarter of 2023, analysts are forecasting sales of roughly $798 million. When analysts talk about sales in the banking sector, they're referring to gross interest income and non-interest income combined. For context, in the third quarter of 2022 , First Horizon reported gross interest income of $733 million. When you add on to this non-interest income of $213 million, you get revenue of $946 million. So the expectation is that the picture will worsen compared to what it was last year.

{kind=link}

Very likely, this decline will be driven by a drop in overall assets for the bank. Back in the second quarter of last year, the average interest earning assets for the bank came in at $79.74 billion. By the end of the second quarter of this year, this had fallen to $75.35 billion. Even if we keep interest rates unchanged at, say, 3%, a decline of this magnitude would translate to $131.7 million in lower gross interest income. How assets are classified, as well as the interest rates involving them, also can play a significant role and how much gross interest income the company generates.

While this is important, I would argue that net interest income is far more significant. This is the gross interest income minus any interest expense incurred in order to capture that income. Because of how reliant revenue is on interest rates, the net interest income of the company serves as a sign of how good management is at capturing the spread between what the market is willing to lend out capital for and how much the company can get others to accept capital for. There's no estimate from analysts on this. But for context, net interest income in the third quarter of last year came in at $602 million.

{kind=link}

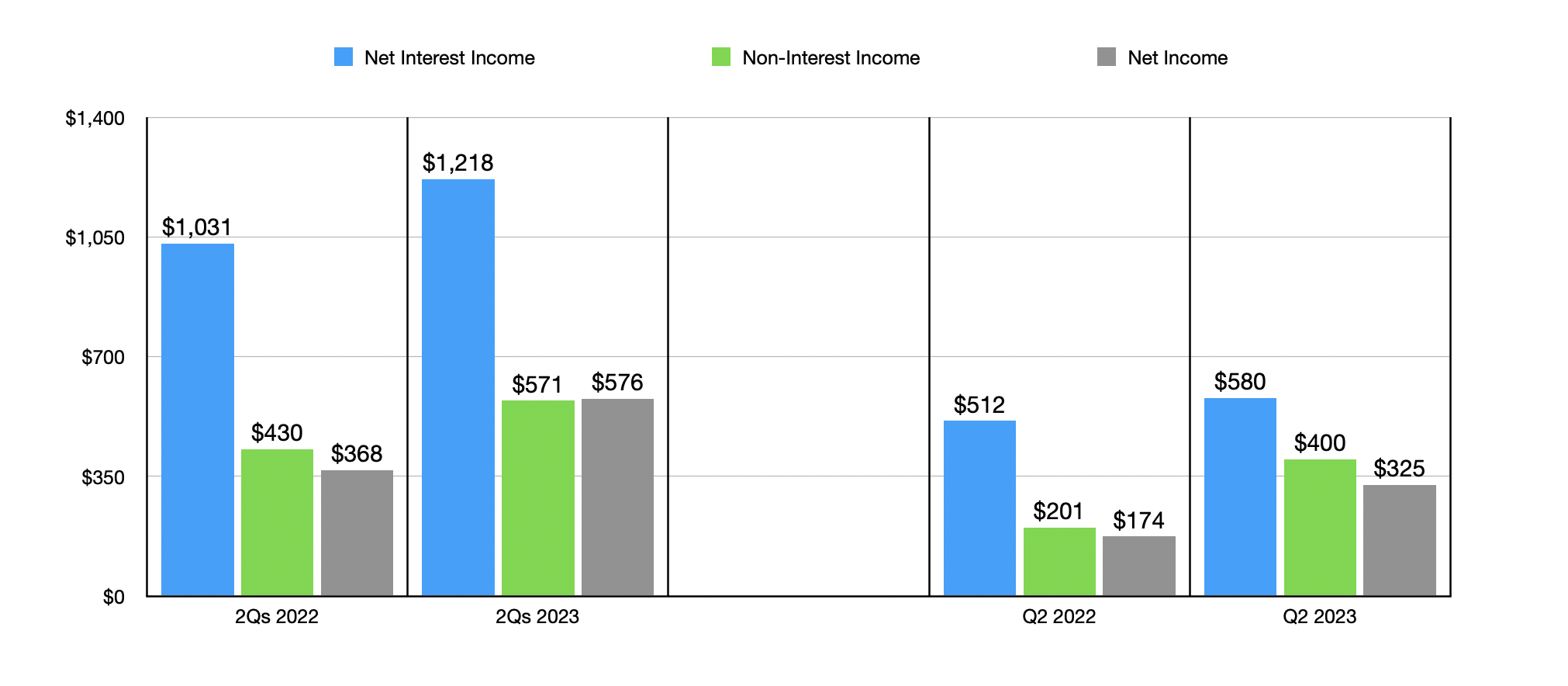

And finally, we have the issue of profits. For the current quarter, analysts are forecasting profits per share of $0.26. This would translate to net income of $145.8 million. By comparison, the same time last year, profits totaled $0.45 per share, or $257 million. Anybody looking at more recent financial performance might think this change is ludicrous. After all, in the second quarter of this year , First Horizon generated $325 million in net income. That's up from the $174 million generated at the same time last year. Meanwhile, for the first half of the year as a whole, net profits of $576 million dwarfed the $368 million reported the same time of 2022.

{kind=link}

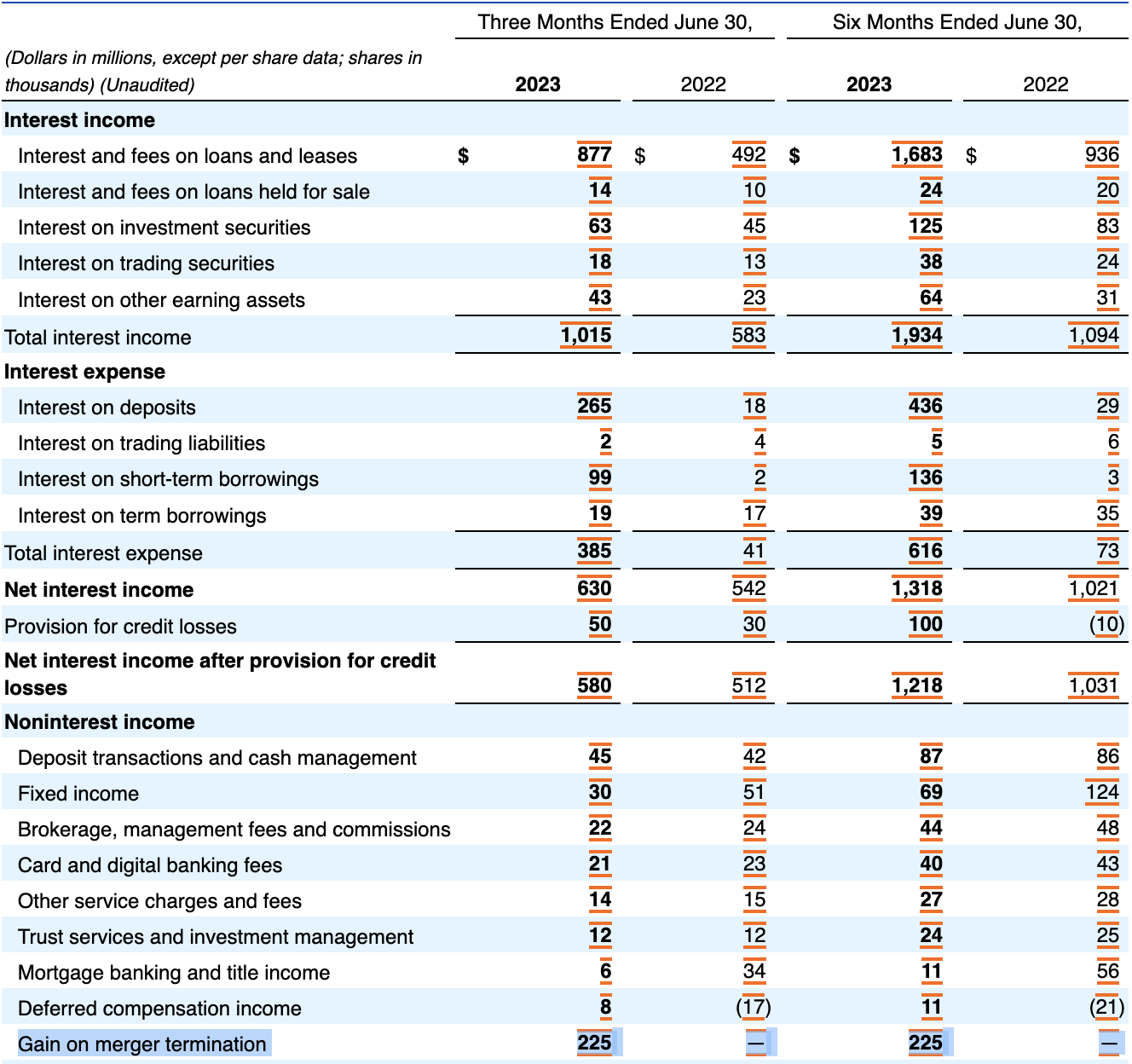

But this is what makes investing rather tricky. As I mentioned earlier in the article, First Horizon received $225 million associated with the termination of its merger with TD Bank. This was recognized in the income statement as a gain in non-interest income. Still, net interest income in the second quarter rose from $512 million last year to $580 million this year, while for the first half of the year it grew from $1.03 billion to $1.22 billion. But if we remove this gain, non-interest income in the most recent quarter dropped from $201 million last year to $175 million, while for the first half of the year it declined from $430 million to $346 million. There's also the fact that some of the company’s costs have risen over the past year. For the first half of 2023, personnel expenses were up 2%. Income tax expense was 62.9% higher, and the company went from contributing only $2 million to charity to donating $57 million the same time this year. There were other items as well, such as a near doubling in deposit insurance expense. But when you consider that this took it up from $15 million to $26 million, the overall impact on the company's bottom line was minimal.

Deposits will be critical

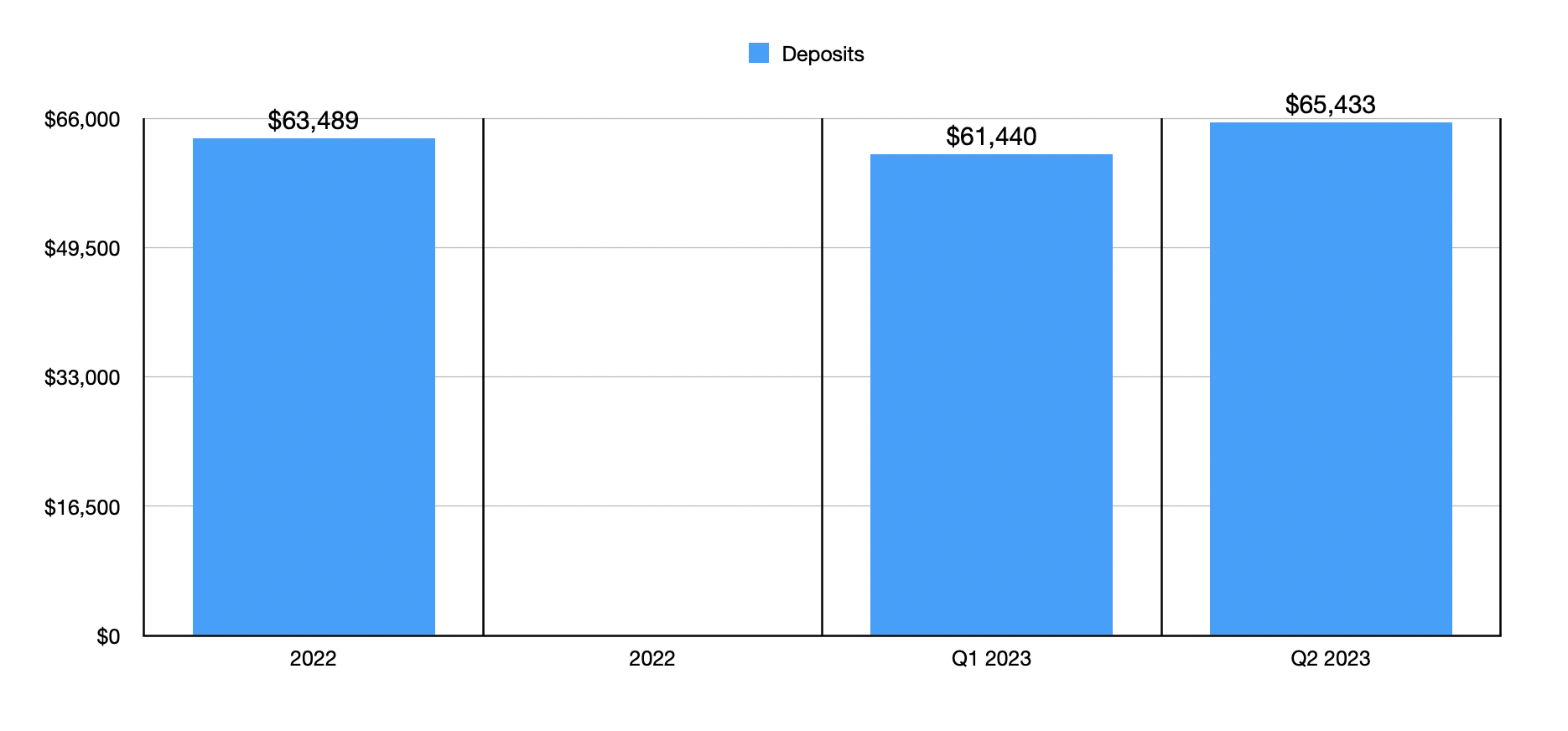

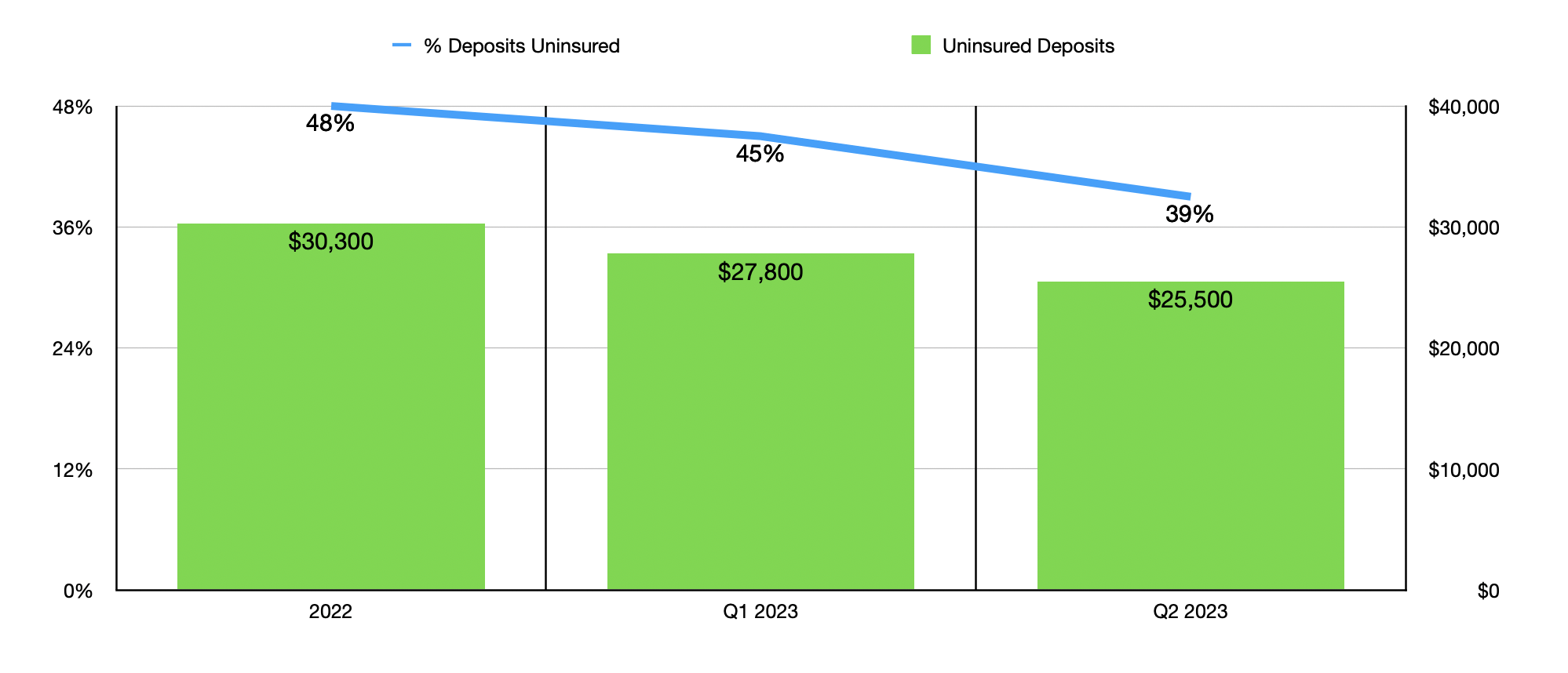

One of the biggest metrics that investors will be paying attention to will be the deposits reported by management. After peaking at $74.6 billion in the fourth quarter of 2021, deposits began a steady but consistent decline, eventually hitting $61.4 billion in the first quarter of this year. High interest rates resulted in depositors looking for yield elsewhere, and it's very likely that the banking crisis also scared money away from the company. After all, as recently as the first quarter of this year, 45% of the bank’s deposits were classified as uninsured. That's $27.8 billion in total.

{kind=link}

We do have some cause to be optimistic on this. In the second quarter of this year, deposits for the bank grew to $65.4 billion. That's an increase of nearly $4 billion in the course of a single quarter. This came even as the value of uninsured deposits dropped $2.3 billion, taking exposure for the bank down to 39%. This is still higher than the 30% threshold that I like to see. But when I see this number plummet at a time when overall deposits are growing rapidly, I don't mind making some leeway for the company. If this trend continues, investors should most certainly be bullish on the matter.

{kind=link}

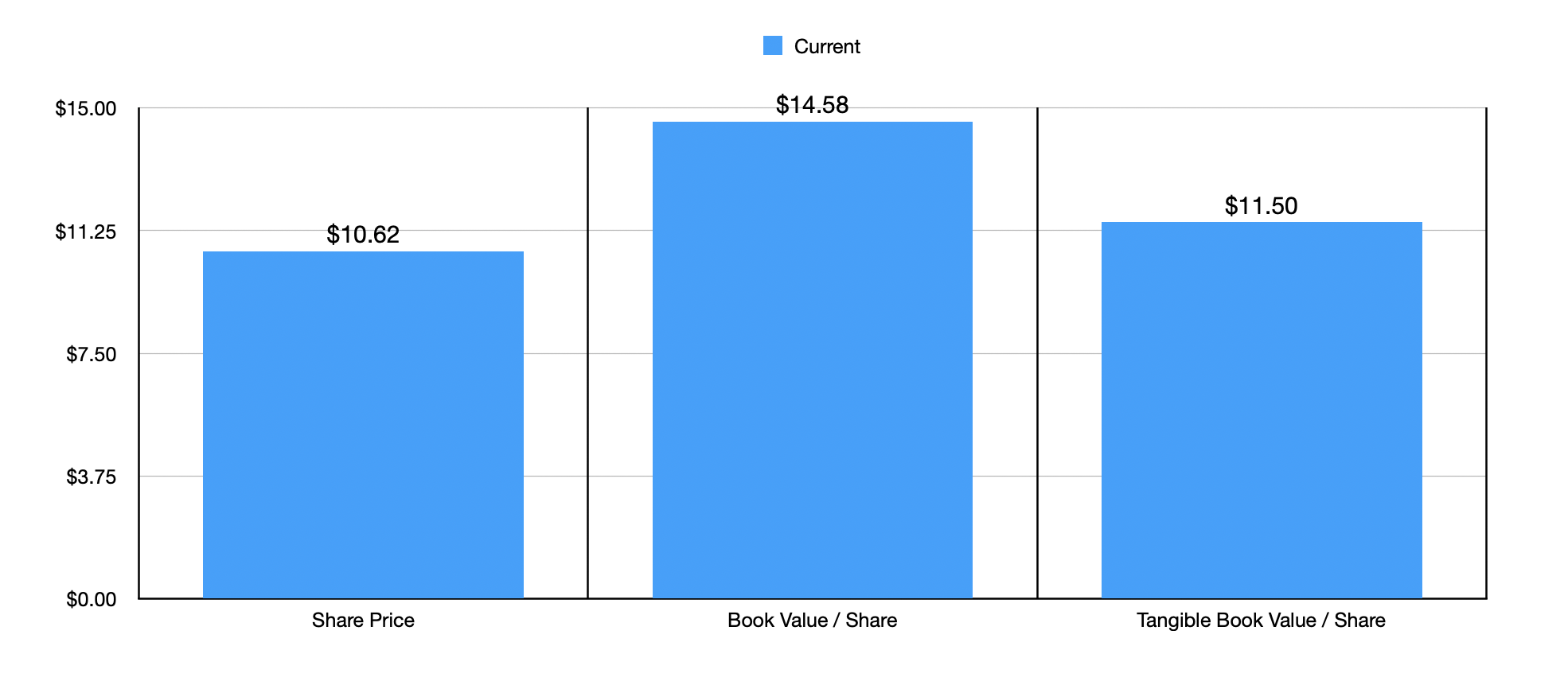

And of course, we still need to be mindful of how shares are priced. Using data from 2022, First Horizon is trading at a price to earnings multiple of 6.8. It's also trading at a 27.2% discount from its book value per share and at a 7.7% discount from its tangible book value per share. These are both great numbers to see, especially when combined with the low price to earnings multiple. We also have seen the net debt on the company's books drop from $4.6 billion in the first quarter of this year to just over $2.4 billion in the second quarter. So investors would be wise to continue watching on that front as well.

{kind=link}

Takeaway

Based on all the data provided, First Horizon looks to be a very interesting prospect at this time. Uninsured deposit exposure is still higher than I would like it to be. But it's moving in the right direction and doing so rapidly. Shares look cheap and, so long as the company can deliver on deposits, I believe that there's cause to be optimistic. Financial performance for the third quarter is being forecasted as rather weak, both on the top and bottom lines. So investors who think that analysts are being realistic in their assessments should probably approach this more cautiously. But until we see hard data suggesting otherwise, I have decided to keep the company rated a "strong buy" at this time.

For further details see:

First Horizon Makes For A Strong Prospect Heading Into Third Quarter Earnings