FR:CC - First Majestic Silver: Another Underwhelming Quarter

2023-11-19 02:10:09 ET

Summary

- First Majestic Silver had another underwhelming quarter with sales down sharply (Jerritt Canyon offline), and margins also significantly despite its highest-cost asset being in C&M.

- Meanwhile, we saw ~9% share dilution year-over-year through use of its ATM, and despite the violent correction, it continues to trade at a rich multiple from a P/NAV standpoint.

- In this update, we'll dig into the Q3 results, its per share metrics & and whether the stock finally getting attractive from a relative value standpoint.

The Q3 Earnings Season for the Silver Miners Index is nearly over and one of the most recent companies to report its results was First Majestic Silver ( AG ). Unfortunately, like Pan American ( PAAS ), it wasn't a great quarter, with First Majestic reporting lower revenue, lower operating cash flow, and significantly higher costs. Worse, these underwhelming results recorded were despite moving its highest cost operation into care and maintenance, and despite the benefit of much stronger metals prices after lapping easy comparisons from Q3 2022. In this update, we'll dig into the Q3 results, its per share metrics following the temporary suspension of operations at Jerritt Canyon, and whether the stock is nearing a low-risk buy zone.

La Encantada Mine - Company Presentation (La Encantada Mine)

{kind=link}

All figures in United States Dollars unless otherwise noted.

Q3 Production & Sales

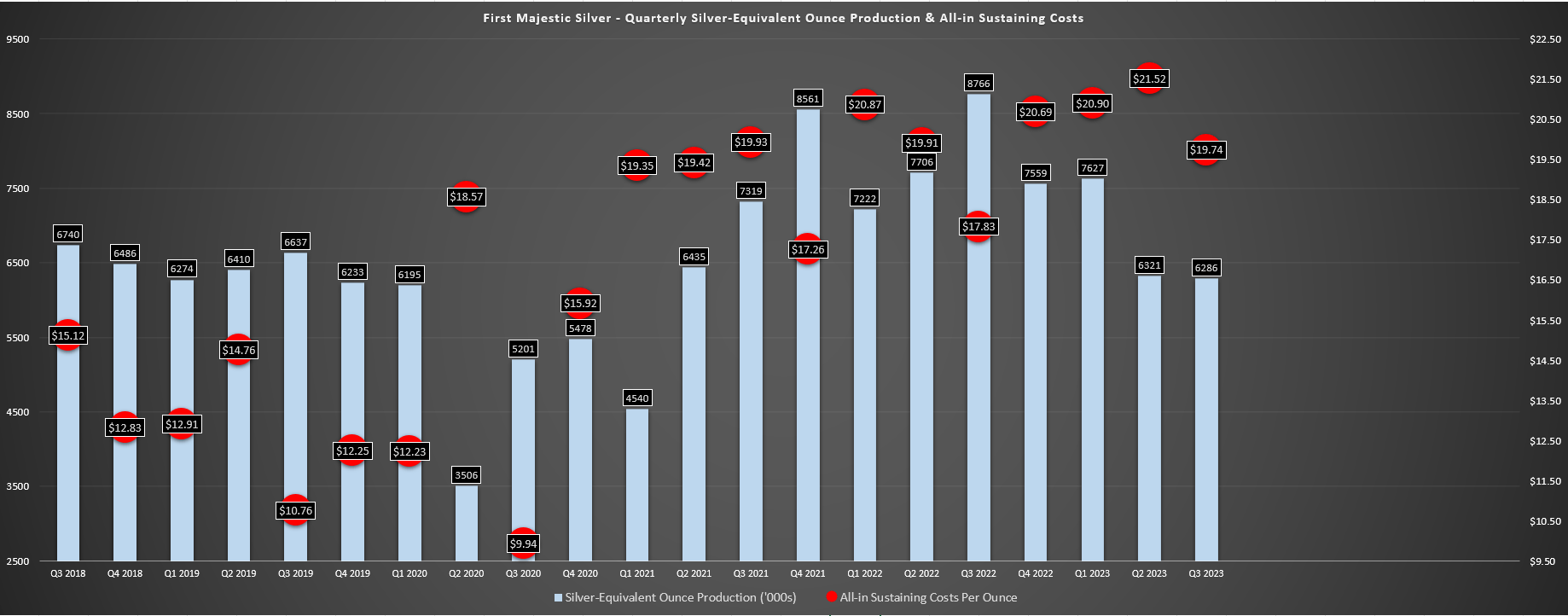

First Majestic Silver ("First Majestic") released its Q3 results earlier this month, reporting quarterly production of ~2.46 million ounces of silver and ~46,700 ounces of gold, translating to a 10% and 30% decline from the year-ago period, respectively. This sharp decline in production can be attributed to the suspension of operations at Jerritt Canyon (which contributed ~16,300 ounces of gold in the year-ago period), much lower production at San Dimas, and the weakest quarter in years at La Encantada related to water availability issues (collapse of a wall at end of Q2 that affected Q3 production). And while Santa Elena picked up some slack for gold and silver production, the extra ~40,000 ounces of silver and ~1,400 ounces of gold weren't nearly enough to offset the massive drop in output at its other mines.

For those unfamiliar, First Majestic announced it would wind down operations and reduce its workforce at Jerritt Canyon in March of this year, with the company calling out contractor inefficiencies, high costs, inflationary pressures and lower than expected head grades.

First Majestic Silver Quarterly SEO Production & AISC - Company Filings, Author's Chart

{kind=link}

Digging into the operations a little closer, San Dimas produced ~1.55 million ounces of silver and ~17,900 ounces of gold in Q2, a significant drop from ~1.65 million ounces of silver and ~23,700 ounces of gold in Q3 2022 due to much lower grades (237 grams per tonne of silver and 2.71 grams per tonne of gold). Worse, costs at this flagship asset soared to $193.41/tonne and $17.76/oz for total production costs and all-in sustaining costs [AISC], respectively, up from $10.97/oz AISC in Q3 2022. As for Santa Elena, it was a better quarter for production but inflationary pressures and the impact of a stronger Mexican Peso affected costs here as well, with ~348,000 ounces of silver and ~28,400 ounces of gold produced at $14.68/oz vs. $12.29/oz in the year-ago period. Higher production at Santa Elena was driven by throughput and silver grades, as well as the benefit of better recoveries with the addition of the dual circuit plant (95% gold recoveries vs. 92% in the year-ago period).

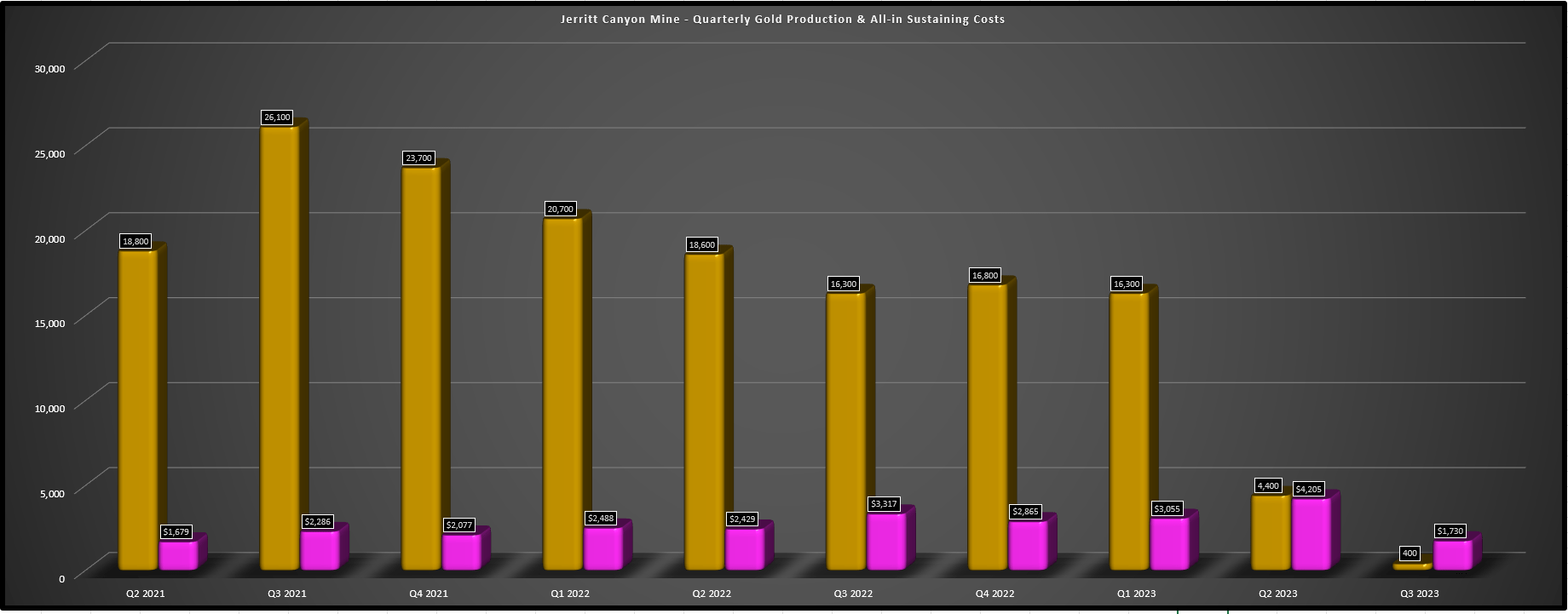

Jerritt Canyon Quarterly Production & AISC - Company Filings, Author's Chart

{kind=link}

Unfortunately, as noted earlier, the lack of production from Jerritt Canyon left a gaping hole in the company's production profile (shown above), with just 400 ounces produced in Q3 from process inventory following the suspension of mining activities in March. This is certainly a disappointing outcome for shareholders and relative to the projections for this asset, with Jerritt Canyon producing at an annualized rate of ~104,000 ounces even in its best quarter, miles below the expected production profile of 200,000 ounces in 2024. In fact, the only positive from moving Jerritt Canyon offline earlier this year is that AISC dropped to their lowest levels in two years at $1,730/oz with just ~$100,000 spent on sustaining capital, and the cash burn has improved following one-time standby costs of $13.4 million year-to-date related to severance and demobilization.

"And I've said a number of times, we're expecting to see production in 2024 to be in the 200,000 ounce range from the current about 110,000 ounce range."

- First Majestic July 2021 Conference Call, discussing Jerritt Canyon

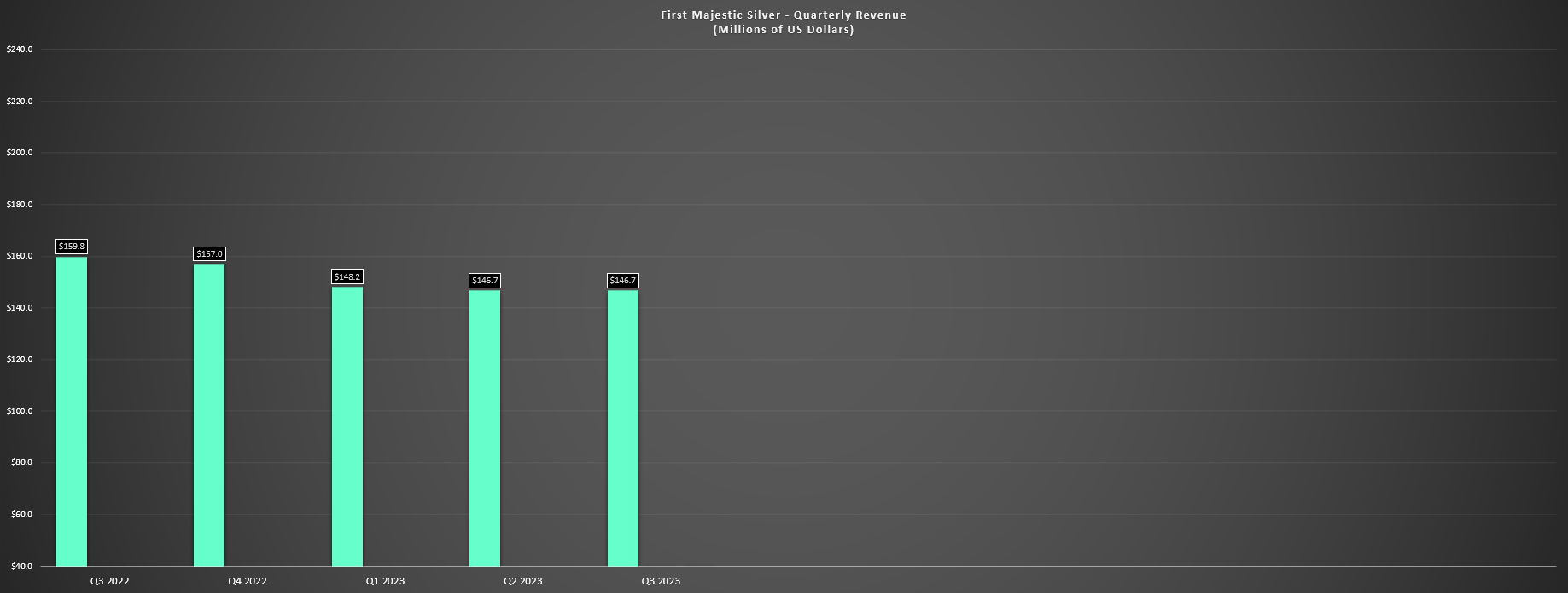

First Majestic - Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

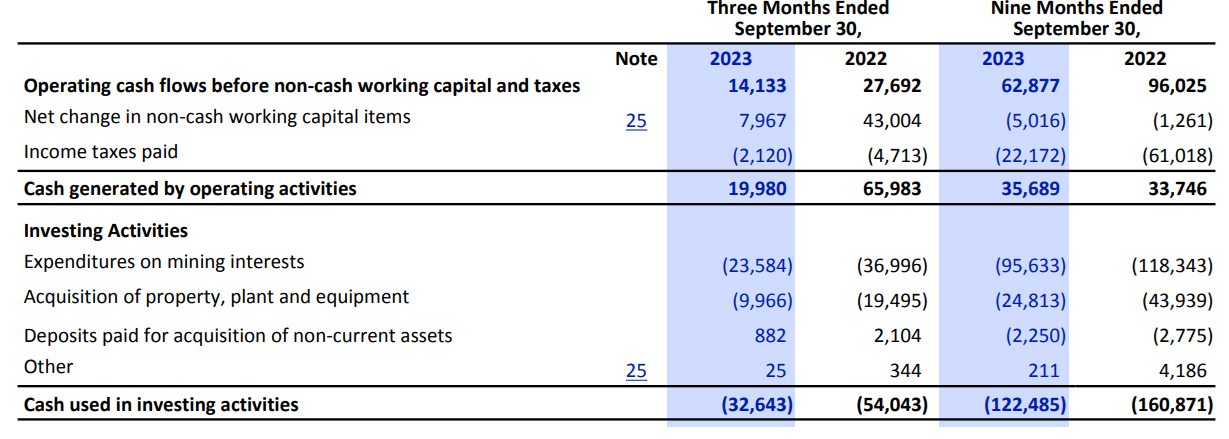

As for the company's financial results, there wasn't much to write home about either. This is because revenue was down 17% year-over-year to $133.2 million despite the benefit of higher metals prices ($22.41/oz average silver-equivalent ounce price vs. $19.74/oz in Q3 2022), and operating cash flow before taxes and working capital changes slid to $14.1 million (Q3 2022: $27.7 million). And while First Majestic noted that it generated free cash flow in the period, this was not the case, with its definition of free cash flow being operating cash flow vs. sustaining capital which represents only a fraction of total capex in the period ($13.5 million vs. $32.6 million). In fact, the company saw a free cash outflow of $18.5 million in Q3, with year-to-date free outflows of $59.6 million. Given the lack of free cash flow generation, the significant share dilution is not surprising, with First Majestic's share count up ~9% year-over-year on a weighted average basis, and with ~13.9 million shares sold year-to-date at an average price of US$6.62.

{kind=link}

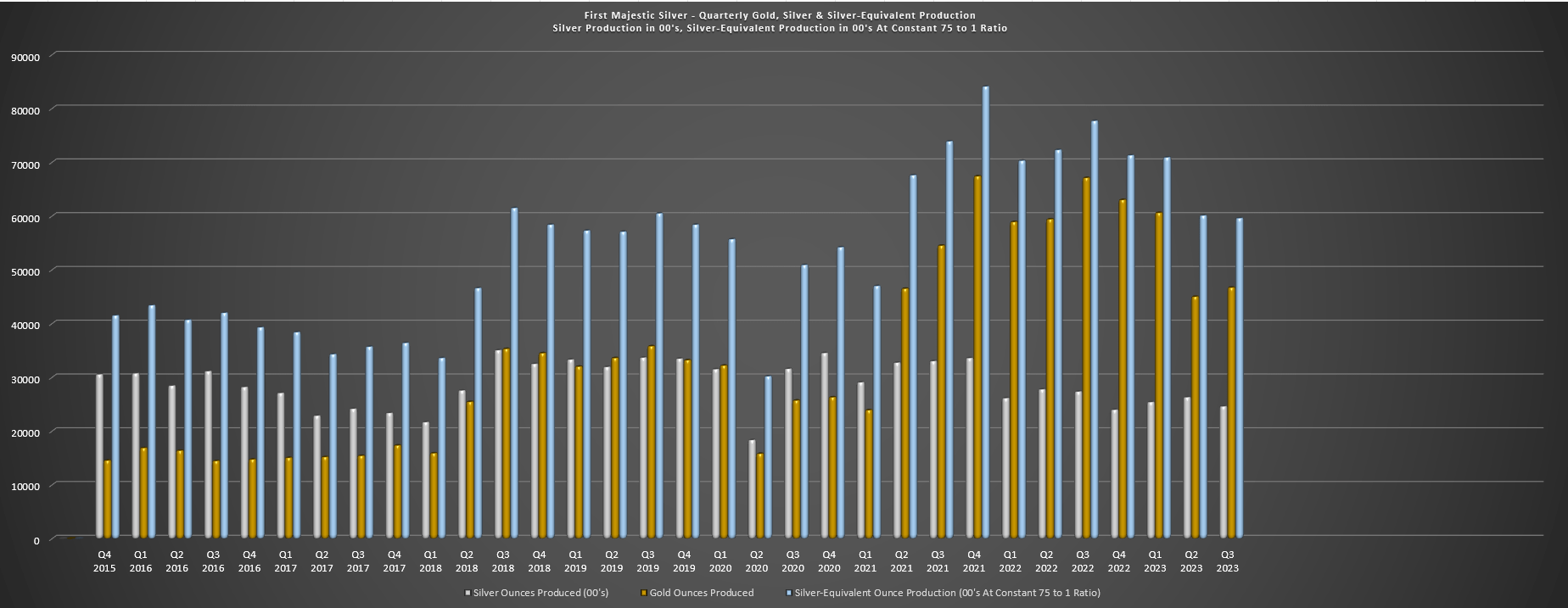

As noted in previous updates, growth is important, but far more important is growth per share . This is because growth that comes at the expense of significant share dilution means that investors are getting exposure to fewer ounces of silver-equivalent production per share held and the result is one is actually seeing their exposure to precious metals diluted by owning a given producer. Essentially, this means that an investor is not getting their desired leverage to gold/silver if production per share is in continuous decline. Obviously, this isn't ideal, since it makes little sense to own a more volatile and riskier producer of a commodity (vs. the metal itself) if it is not offering the leverage that one should get for taking on this added risk. And as we can see from First Majestic and despite a period of rising metals prices from Q3 2015 to Q3 2023, its share count has nearly doubled (~155 million shares to ~287 million shares) while silver-equivalent production is up less than ~50% on a constant 75/1 ratio basis, leading to significant erosion in production per share.

First Majestic - Constant Ratio Silver-Equivalent Production (2015-2023) - Company Filings, Author's Chart

{kind=link}

Costs & Margins

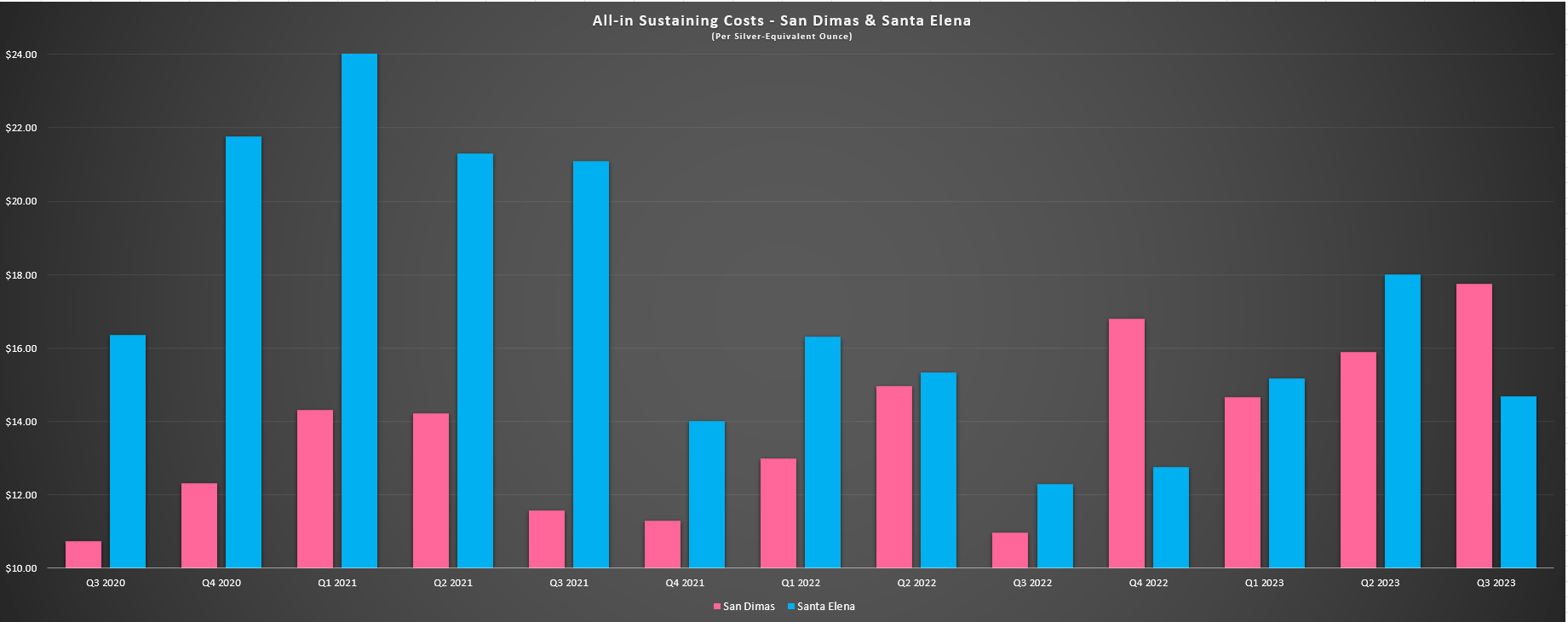

Moving over to costs and margins, the results were just as disappointing, with First Majestic affected more than some of its peers because of having all of its continuing production coming from Mexico where a rising Peso has resulted in much higher operating costs. This is quite clear in the below chart, with AISC at San Dimas and Santa Elena up sharply year-over-year and San Dimas' costs coming in at their highest levels in years at $14,.07/oz and $17.76/oz (cash costs and AISC, respectively). Some of this increase in San Dimas' costs can be attributed to the lower sales, less power utilization from its hydroelectric plant (lower expected rainfall) and restructuring costs related to workforce optimization, but these results are still quite disappointing, and the company isn't getting much help from an FX standpoint in Q4 with the USD/MXN continuing to trend lower towards its August lows.

San Dimas & Santa Elena AISC - Company Filings, Author's Chart

{kind=link}

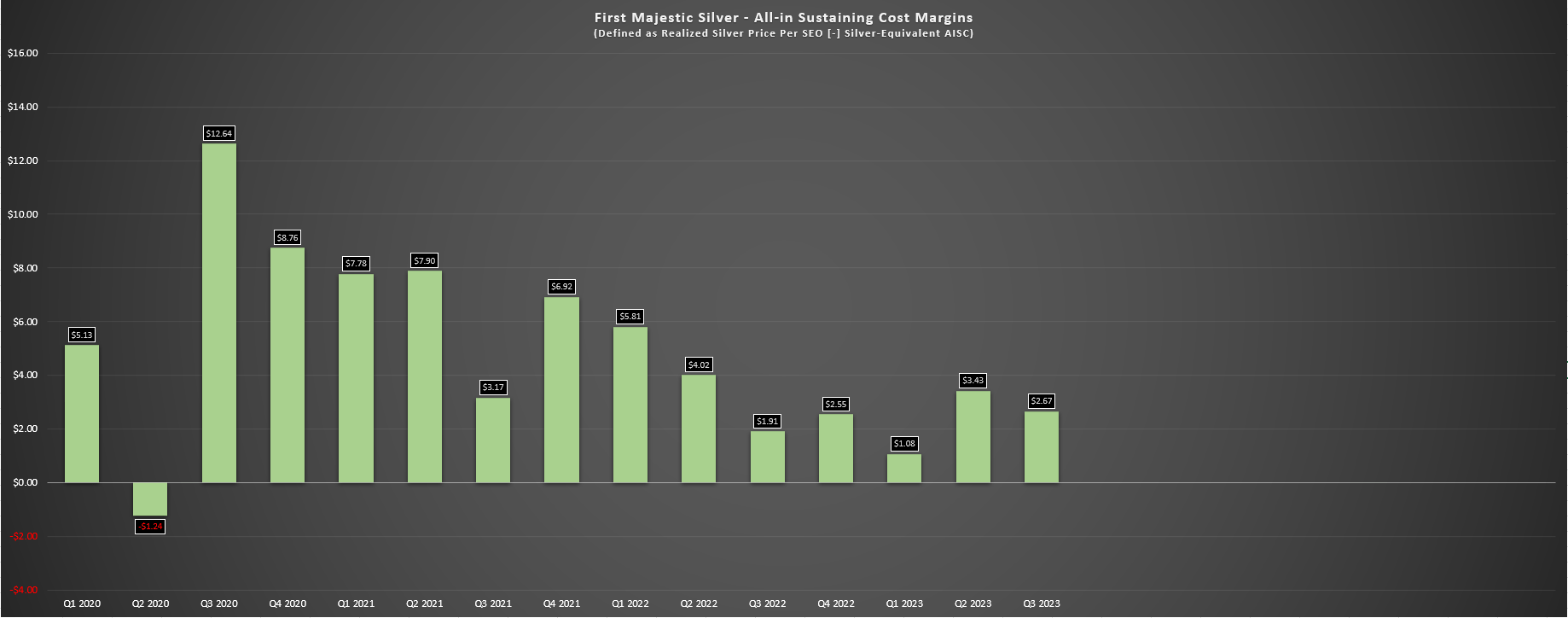

Unfortunately, cost performance wasn't any better at La Encantada, where AISC spiked to $29.86/oz vs. $18.61/oz in the year-ago period on the back of lower production and rising costs. The result is that First Majestic saw a limited improvement in AISC margins despite a near 15% increase in its average realized silver-equivalent price and with a little help from its bullion site where 61,000 ounces were sold at a higher price of $26.17/oz. In fact, AISC margins remained at depressed levels at $2.67/oz (~10% AISC margins), while year-to-date AISC is sitting at $20.70/oz vs. $19.44/oz in the year-ago period. On a positive note, the company will not have higher costs at Jerritt Canyon to drag on margins in 2024. However, the continued strength in the Mexican Peso makes it tough to be optimistic about AISC margins climbing back above 25% without further help from metals prices.

First Majestic - AISC Margins (defined as Realized Silver Price Per SEO [-] Silver-Equivalent AISC)

{kind=link}

Some investors might be puzzled by the violent correction in First Majestic's share price since its Q1 2021 peak and assume this is largely overdone and detached from fundamentals. However, one look at the company's margins suggests that much of this move is justified. This is because AISC margins are down over 65% in the same period and we can add ~30% share dilution to this figure following elevated sales under its ATM and the acquisition of Jerritt Canyon. So, with a 65% decline in AISC margins and 30% share dilution, I would argue that these are far more important figures to consider when trying to analyze the deterioration in the share price vs. simply looking at metals prices and assuming the stock should sit at similar levels. This is because margins matter even if miners are correlated to their commodity, and significant underperformance can occur when a producer is diluting at a pace well above its peer group (especially if the asset purchased responsible for much of that share dilution was impaired and there's still liabilities related to that asset with post-closure water treatment costs.

{kind=link}

Valuation

Based on ~309 million fully diluted shares and a share price of US$5.40, First Majestic trades at a market cap of ~$1.67 billion and an enterprise value of ~$1.55 billion. This valuation continues to leave AG trading at one of the richest P/NAV multiples sector-wide (~2.0x P/NAV) vs. an estimated net asset value of ~$780 million. To put this figure in perspective, Hecla Mining ( HL ) trades at ~1.40x P/NAV despite having a Tier-1 jurisdiction profile and a superior cost profile and several larger and more diversified gold producers continue to trade at less than 1.0x P/NAV following the violent correction we've seen sector-wide that has spared few stocks. Meanwhile, one can even find royalty/streaming companies trading at more attractive multiples like Sandstorm ( SAND ) at ~0.80x P/NAV, suggesting that even after this 70% correction, First Majestic remains fully valued with no margin of safety from a valuation standpoint.

{kind=link}

The most disappointing part about this is that First Majestic had the opportunity to its high-priced currency and cash in Q1 2021 to add a Tier-1 jurisdiction asset with a longer mine life to increase its weighted-average mine life, improve its margin profile and ideally diversify into more attractive jurisdictions. Several options could have been pursued among developers including Gold Standard (GSV) and Corvus (KOR) also in Nevada, and multiple options among producers were available at attractive prices like Wesdome Mines ( OTCQX:WDOFF ) or Orla Mining ( ORLA ) among producers. Unfortunately, while it picked the right jurisdiction given that Nevada's investment attractiveness has improved while Mexico has worsened, it got the wrong asset, and without significant optimization and much higher metals prices it's unclear whether Jerritt Canyon will ever generate positive free cash flow which is certainly disappointing given the opportunity cost and investments post-acquisition.

Summary

First Majestic had another underwhelming quarter in Q3 and it's hard to be that optimistic about Q4 given that the Mexican Peso has continued to strengthen against the US Dollar, wiping out most of the benefit of the higher metals prices in the period. Meanwhile, although First Majestic is in better shape financially with ~$140 million in cash, this is largely due to significant share dilution which has put a further dent in its per share metrics. Finally, while the stock may be down over 70% from its highs, it never belonged above $10.00 per share, let alone $19.00 when I warned against paying up for the stock.

{kind=link}

On a positive note, sentiment surrounding AG is arguably the worst it's been a decade and that is a key ingredient for hammering out a bottom in the stock. The issue is that despondency from a sentiment standpoint without an attractive valuation is not a setup I would be interested in as I am more interested in turnaround stories where the liquidation valuation exceeds the market cap and where I can see an accelerate re-rating if we see M&A. In AG's case, I don't see any way the company would liquidate this portfolio for over $1.2 billion (~$4.00 per share) especially given the ongoing tax disputes, and I don't see why any suitor would be interested in the portfolio as it would be margin dilutive for most companies. To summarize, I continue to see AG as an Avoid and I see far more attractive ways to get exposure elsewhere in the sector. One name is Victoria Gold ( OTCPK:VITFF ) which trades at less than 0.50x NPV in a Tier-1 jurisdiction and barely ~4x FY2025 EV/FCF.

For further details see:

First Majestic Silver: Another Underwhelming Quarter