FRMEP - First Merchants: Robust Results Make The 7.7% Yielding Preferred Shares Attractive

2023-08-09 12:26:01 ET

Summary

- First Merchants' financial performance in the second quarter showed improvement in net interest income and decreased non-interest expenses.

- The bank's ability to cover preferred dividends is strong, with less than 1% of net profit needed to cover the payments.

- The preferred shares have a small issue size and low dividend requirements, making a call in 2025 more likely.

Introduction

Although I'm generally not a fan of preferred share issues by financial institutions as the preferred dividends are usually non-cumulative in nature, there are some exceptions. As explained in previous articles I for instance have a long position in (OZKAP), the preferred share issued by Bank OZK (OZK) and I also initiated a long position in OceanFirst's (OCFC) preferred shares (OCFCP) after diving into the details of the preferred share .

I discussed the acquisition of Level One by First Merchants (FRME) in a previous article but given the recent turmoil in the banking landscape I wanted to update my view on the bank and have a closer look at the preferred shares.

The bank's financial performance in the second quarter

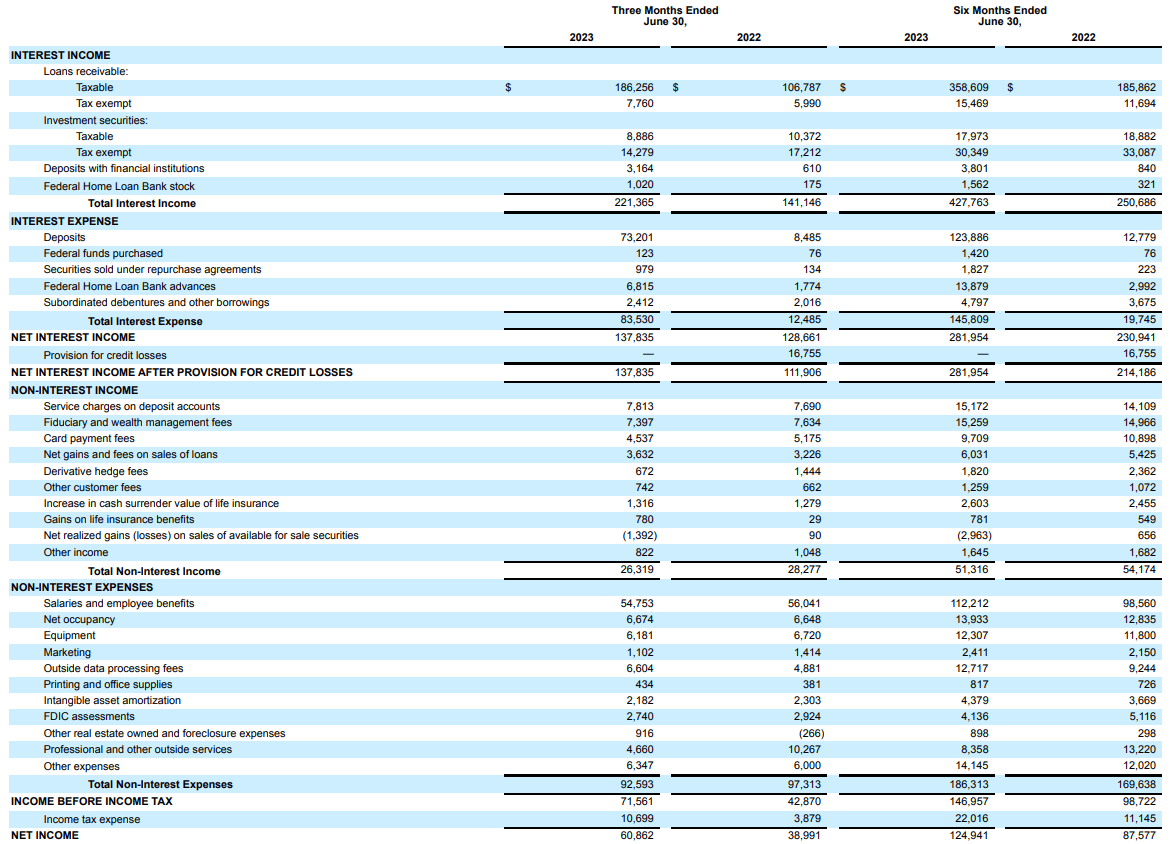

I was pleasantly surprised when I saw First Merchant's net interest income, as the bank actually performed pretty well. While the net interest income decreased compared to the first quarter, there's a clear year-over-year improvement. As you can see below, the total interest income increased to just over $221M while the interest expenses remained "limited" to $83.5M. While that still is almost seven times higher than the interest expenses incurred in the second quarter of last year, the net interest income still increased by about $9M to $137.8M .

{kind=link}

Additionally, the net non-interest expenses decreased compared to a year ago. The bank reported a total net non-operating expense of approximately $66.3M, which resulted in a pre-tax income of $71.6M. Surprisingly, there were no loan loss provisions recorded in the second quarter, and the net income was a very impressive $60.4M (after taking the preferred dividends into account). This resulted in an EPS of $1.02.

That's already encouraging for the preferred shareholders as well as it indicates the bank needed less than 1% of its net profit to cover the preferred dividends. And keep in mind the second quarter was actually worse than the first quarter as the bank needed less than $1M from the $125M net income in the first semester to cover the preferred dividends.

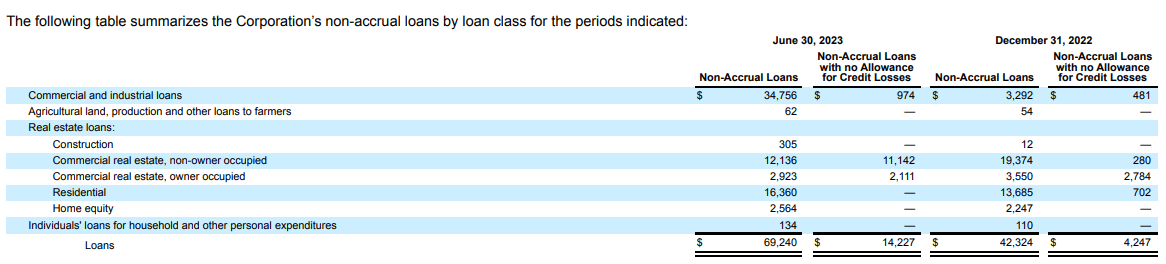

And while it perhaps was a little bit surprising to not see any loan loss provisions in the second quarter, let's not forget the bank already has recorded a total of in excess of $220M in provisions on a $12.27B loan book. That's a ratio of 1.70%. Meanwhile, the footnotes to the financial statements indicate just under $70M in loans are now on a non-accrual status while the total amount of loans past due is also increasing.

{kind=link}

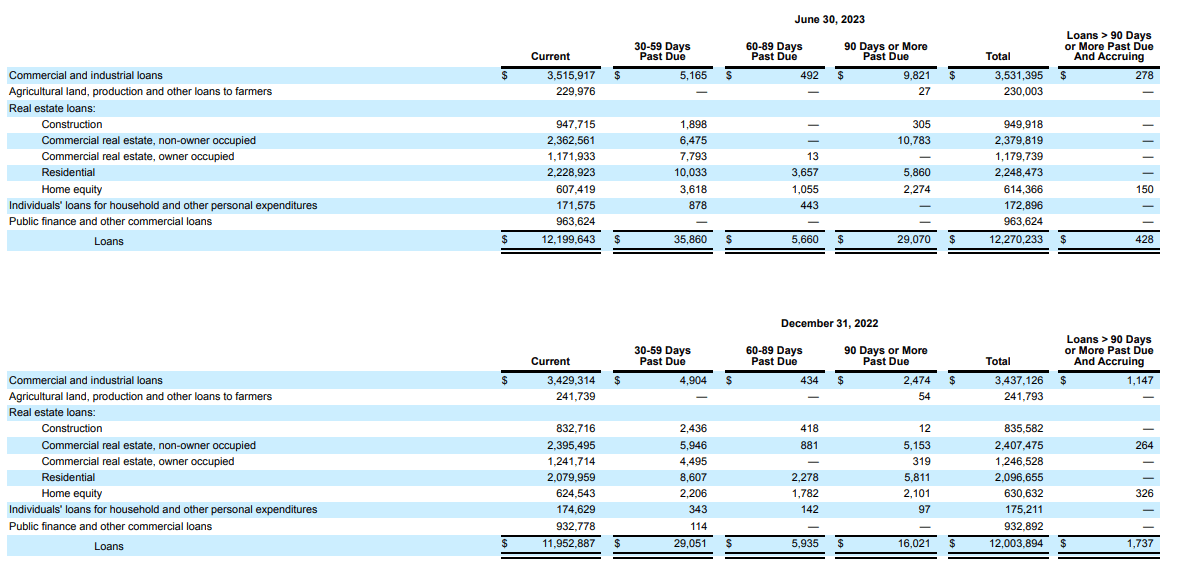

While $12.2B of the loans are classified as "current," about $70M is now "past due" of which half are in the 30-59 days past due category.

{kind=link}

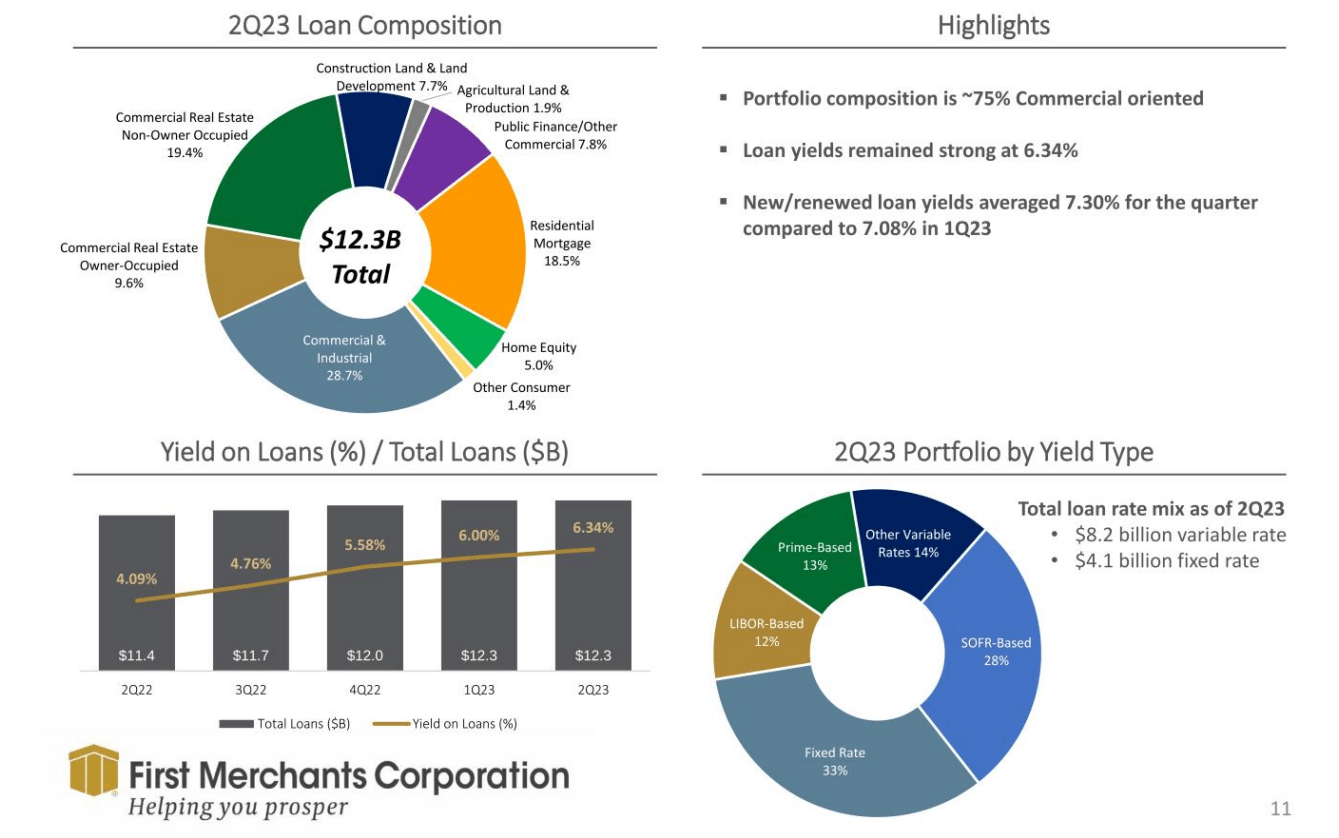

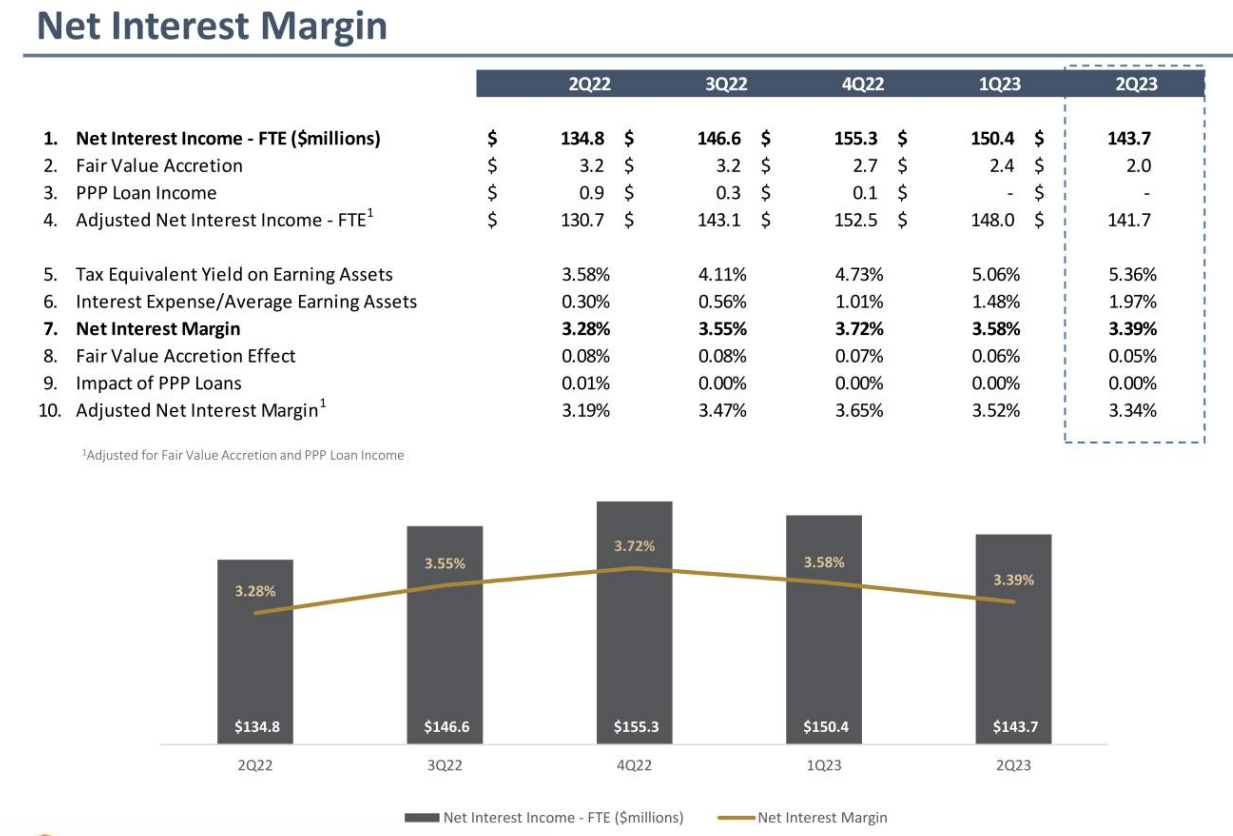

The bank doesn't seem to be too worried, and as shown earlier in this article, the reported earnings are strong enough to handle additional loan loss provisions should the need arise. And while the majority of the loan portfolio is indeed commercial focused which may deter some investors, this also means the variable interest rate component is much higher: about two-thirds of the loans has a variable rate and this has been a tremendous help for the bank to keep its net interest margin pretty stable.

{kind=link}

As you can see below, the net interest margin has been pretty consistent, and although it recently came down a bit, let's not forget the most recently underwritten loans in the second quarter had an average cost of debt of approximately 7.3%.

{kind=link}

Meanwhile, the cost of deposits is obviously increasing as well. The image below shows the trend and the cost of deposits will likely continue to increase. However, First Merchants should be able to mitigate the impact thanks to its predominantly variable rate loan portfolio.

The preferred shares are not unappealing

The bank has one series of preferred shares outstanding, the Series A which is trading with (FRMEP) as its ticker symbol. The preferred shares pay a quarterly preferred dividend of $0.46875 which works out to $1.875 per share per year for a yield of 7.5%. As the preferred shares are currently trading about 2% below the principal value of $25, the yield is currently approximately 7.7%. The preferred shares are non-cumulative and can be called from August 2025 on. The yield to call is approximately 8.75%. This is a fixed rate preferred share and will not reset in 2025. The $1.875 in annual dividends will just continue to be paid out.

As not First Merchants but Level One, a bank it acquired last year, issued the preferred shares, First Merchants may indeed call the shares in 2025 if it doesn't want to have preferred equity. I'm not sure why the preferreds weren't called during the takeover process but unless I glanced over it I also couldn't find a change of control provision in the IPO documents which would have been required to enable First Merchants to call the shares.

In the previous section of this article I already mentioned the preferred dividend coverage level looks excellent as the bank only needs a small portion of its net income to cover the preferred dividends. That's not only because the bank's financial performance has been relatively strong lately, but also because it's a very small issue size. There are only 1 million preferred shares outstanding with a principal value of $25, and as you can see below, the $25M in preferred equity represents less than 1.5% of the total equity side of the balance sheet. And that's a comfortable position to be in.

Investment thesis

Although the non-cumulative nature of the preferred shares is a deterrent, I do like this issue because of its small size relative to the equity on the balance sheet and the very low dividend requirements. While it obviously still is a risk, the bank should continue to be able to make the quarterly payments of less than $0.5M.

I currently have no position in the preferred shares but I like the risk/reward ratio and I will likely initiate a small long position in the near future. As it's a non-cumulative issue, I will keep that position limited and I realize I will have to keep an eye on the bank's financial results on a quarterly basis to make sure the loan book doesn't deteriorate too much.

For further details see:

First Merchants: Robust Results Make The 7.7% Yielding Preferred Shares Attractive