FRC - First Republic Bank: 4 Reasons To Buy

2023-03-15 14:50:20 ET

Summary

- The sharp decline in the regional banking sector presents a prime opportunity to buy regional bank shares cheaply, but only for investors who can handle the strong price volatility.

- I don't think many depositors will take money out of the bank due to the extra liquidity boost.

- FactSet provides insight into the risk exposure of 10 regional banks. First Republic came out strong from this analysis, with only 1.9% AOCI/TEC-AOCI.

- JPMorgan came out with an analysis that showed us the dramatic result of SVB's Financial's CET1 capital ratio. The CET1 capital ratio for First Republic is expected to be strong at 6%.

- First Republic's risk management is favorable because the bank does not invest in exotic derivatives, does not invest in junk bonds, does not issue credit cards or auto loans, and has no negative repayment loans.

Introduction

With several bank stocks down significantly, investors might be wondering if this is a buying opportunity of a lifetime. I seized this opportunity and bought large positions in First Republic ( FRC ), Comerica ( CMA ), Charles Schwab ( SCHW ), Western Alliance Bancorporation ( WAL ), PacWest Bancorp ( PACW ) and First Foundation ( FFWM ).

These financials all experienced sharp declines while their fundamentals were strong. What was particularly notable was the sharp decline of First Republic, which fell 80% from its peak. The bank has strong fundamentals because it serves high net worth customers with 0% net loan charge-offs.

In my article I give 4 reasons why I like First Republic, and before that I give some insights into the market situation.

What Happened To The Markets

Silvergate, Silicon Valley, and Signature, all major banks with exposure to cryptocurrencies, have been shut down by regulators mostly due to large losses on sales of its securities portfolio.

The regional banking sector is down significantly, and it all started last week with problems at Silicon Valley bank. SVB Financial is Silicon Valley’s holding company, a bank that specializes in financing start-up tech companies. Its stock price crashed 60% this week, for good reason. The company is in financial trouble now that it has announced a proposal to raise cash and put the company up for sale.

On March 8, SVB Financial announced the sale of its available-for-sale securities portfolio and sold about $21 billion in government bonds and other financial products. This will result in an after-tax loss of $1.8 billion for the first quarter of 2023. Available-for-sale securities are typically not sold until the company has an urging need for cash.

To avoid possible panic selling, the bank announced that it planned to offer $1.25 billion of common stock and $500 million of deposit shares. In addition, General Atlantic will purchase $500 million of common stock in a separate private transaction at the price of the public offering. The total value of this capital transaction is as much as $2.25 billion, and the company will use the net proceeds for "general corporate purposes." The total amount of $2.25 billion is significant because its market capitalization was only $16 billion (14%).

CEO Greg Becker calmly addressed the stock markets, but things turned out very differently. Depositors were shocked and pulled their money out of the Silicon Valley bank. Investors were also shocked and the stock price fell 60%.

Venture capital investors such as Founders Fund (Peter Thiel), Union Square, Tribe Capital and Founders Collective have advised their portfolio companies to place their cash elsewhere. The CEO of Y Combinator, Garry Tan, has also warned his network of start-ups that the solvency risk is real and that they too should reduce their exposure to the bank.

While Silicon Valley Bank was struggling due to rising interest rates and stagnant VC funding, the financial problems mainly arise in the bank run, many businesses and individuals were taking their cash out of the bank.

The withdrawal of deposits is disastrous for banks because they serve as collateral for loans. The Federal Deposit Insurance Corp. took over Silicon Valley Bank and it entered receivership after SVB Financial was shut down by California regulators. What I am particularly concerned about is that the growth in innovation will decline, because Silicon Valley was the main bank for boosting start-ups. This whole scenario reminds me of the 2008 financial crisis.

Once Of A Lifetime Buying Opportunity

I am not surprised that Silicon Valley bank is currently in trouble. In an earlier article , I pointed to a possible recession. When the yield curve inverts, it causes a decline in the equity market, and bank stocks are particularly vulnerable. I see that as a strong contrarian buying opportunity, which historically occurs about once every 10 years. Now, less than 4 years after the COVID crisis, this opportunity presents itself again.

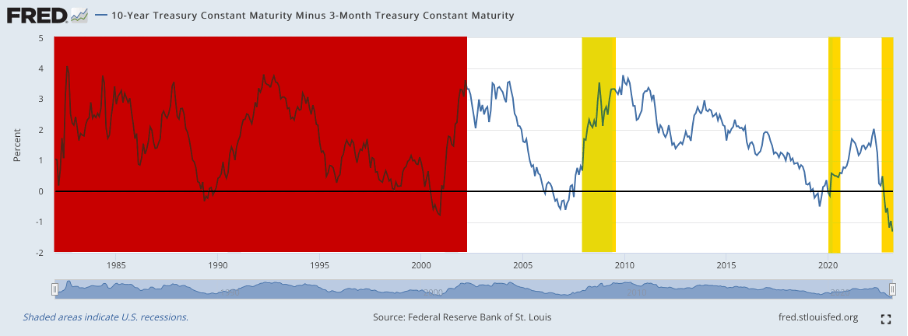

I have highlighted the -20% or more peak-to-trough moments of the SPDR S&P Regional Banking ETF ( KRE ) in yellow in the yield curve chart. Unfortunately, I do not have data prior to 2000. In the image below, we see that the ETF enters the bear market after the yield curve inverted. This is not remarkable because the yield curve inverts when short-term interest rates are higher than long-term interest rates.

Yield Curve Marked For Peak-Trough of the SPDR S&P Regional Banking ETF (FRED and author's own visualization)

{kind=link}

The inverted yield curve usually only occurs once every 10 years, so we are lucky to see this coming, as the prices of many bank stocks are currently favorable in my view. I have 4 reasons why I think First Republic specifically is an attractive stock investment.

Reason 1: Additional funding from JPMorgan and the FED

First Republic has plummeted from its all-time high of $210 in November 2021 to $40 now. On Monday, the stock sold for $19 per share. Investors are clearly panicking and wondering if First Republic is the next bank to be shut down by regulators.

We know First Republic is a solid bank with wealthy and creditworthy customers, which also makes it a bit risky because of the large uninsured amount of depositors. More than $140 billion of its deposits are in accounts that exceed the limit for federal deposit insurance.

First Republic received a new facility from JPMorgan (JPM) and JPMorgan gave First Republic access to $70 billion in funds. The Federal Reserve also offered the bank additional funding capacity under its $25 billion Bank Term Funding Program in exchange for high-quality collateral such as Treasuries.

The additional liquidity boost of $70 billion is expected to cover more than 40% of total deposits of $176 billion. That means that a lot of depositors will have to withdraw their money before problems arise, which I don't think will happen.

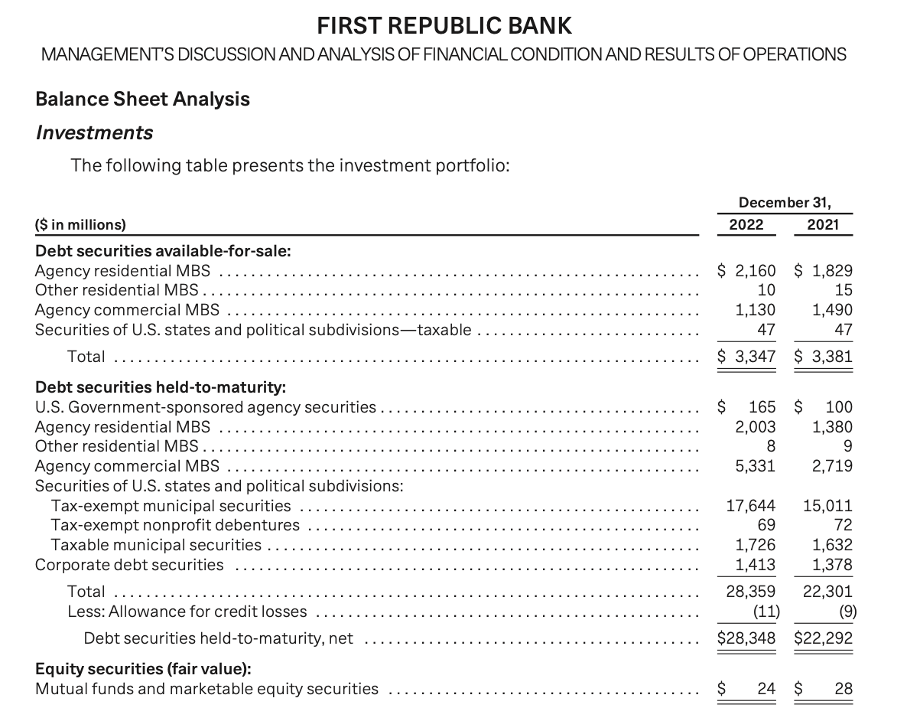

The problems at SVB Financial stemmed from large unrealized losses in the investment securities portfolio. First Republic showed some interesting data on investment securities and the available-for-sale portfolio in its Q4 2022 results :

The total combined investment securities portfolio (consisting of available-for-sale, held-to-maturity and equity securities, excluding any ACL) represented 15% and 14% of total assets at December 31, 2022 and 2021, respectively.

The weighted average duration of the available-for-sale portfolio was 4.4 and 3.9 years at December 31, 2022 and 2021, respectively. The weighted average duration of the held-to-maturity portfolio was 10.8 and 10.6 years at December 31, 2022 and 2021, respectively.

When contrasted to SVB Financials' portfolio allocation of 57%, the combined 15% of investment securities is a pittance. This reduces the possibility of suffering significant unrealized losses as a result of falling bond prices.

First Republic Bank Balance Sheet Analysis (First Republic Investor Relations)

{kind=link}

Reason 2: Low exposure to unrealized losses as a % of total equity

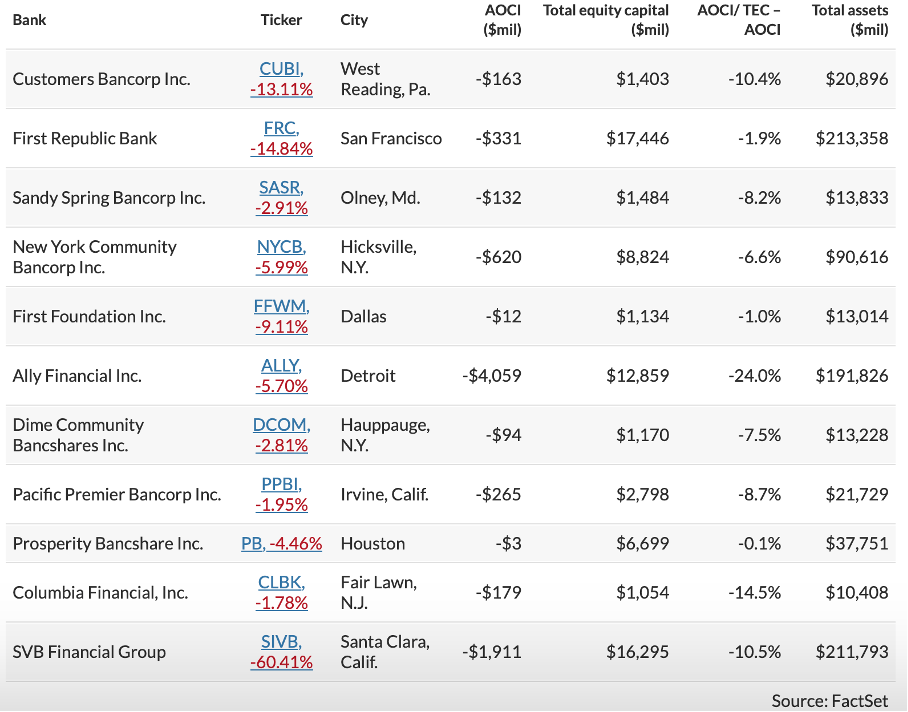

The markets are in mayhem as investors flee the market out of fear of bank runs. Western Alliance Bancorporation fell 21%, PacWest 51% and First Foundation 32%. Those banks have the same red flags as Silicon Valley Bank; they have a large exposure to unrealized securities losses as a % of total equity.

One way to get insight into the risk exposure of certain regional banks is to divide the negative AOCI by the bank's total equity minus AOCI (by adding the unrealized losses on AFS securities back to total equity). FactSet provided the list of 10 regional banks with similar red flags to SVB Financial.

AOCI/TEC-AOCI (FactSet and MarketWatch)

{kind=link}

We see that Ally Financial's ( ALLY ) AOCI decline of -24% is the largest on the list. This could put Ally at great risk, as I wrote in an article earlier this month.

The list above shows that First Republic did not report significant AOCI losses relative to its total equity minus AOCI, this is due to the fact that only 15% of its assets consist of its total combined portfolio of investment securities.

Investors should realize, however, that this is a snapshot of the status quo. The yield curve is still deep in the red, so banks are likely still vulnerable to additional unrealized losses.

Reason 3: The impact of unrealized losses on capital ratios

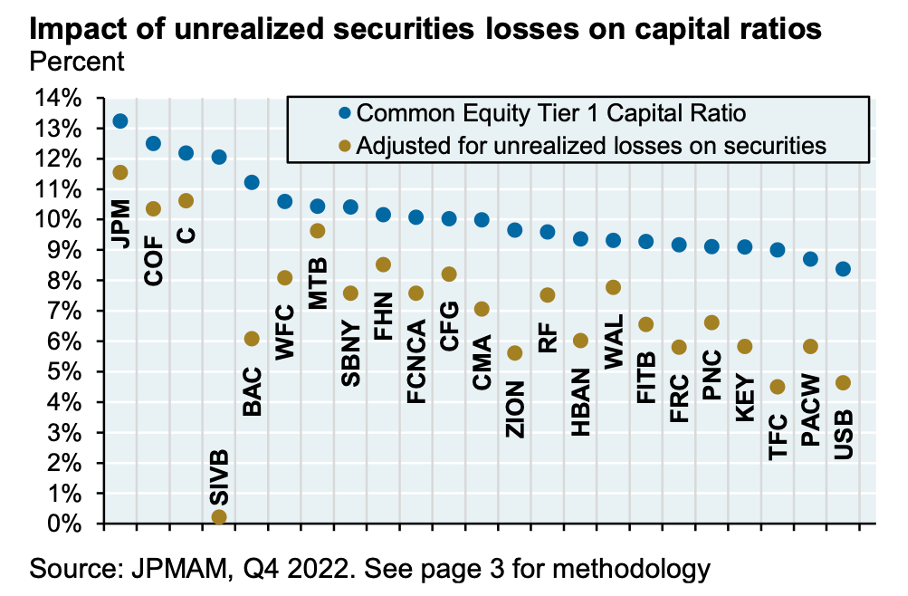

JPMorgan came out with an analysis of SVB Financial's impact on the banking system and how other banks would be affected. It offered us a chart showing the common equity tier 1 capital ratio adjusted for unrealized losses on securities.

JPMorgan gave clear thoughts on the main cause of Silicon Valley Bank's financial problems:

Between Q4 2019 and Q1 2022, deposits at US banks rose by $5.4 trillion and due to weak loan demand, only ~15% was lent out; the rest was invested in securities or kept as cash. Banks designate these securities as being “available-for-sale” (AFS) or in “hold-to-maturity” ((HTM)) portfolios instead. SIVB relied extensively on HTM treatment for its growing securities portfolio: since 2019, its AFS book grew from $14 to $27 bn while its HTM book grew from $14 to $99 bn. Selling HTM securities is complicated, since it results in larger parts of the portfolio being suddenly marked to market, which can in turn then result in the need for a capital raise.

What clearly stands out in the chart below is that the common stock tier 1 capital ratio, adjusted for SVB Financial's unrealized losses, is about 0%.

And what I'm particularly pleased about is that First Republic continues to maintain a strong 6% tier 1 capital ratio, as projected by JPMorgan.

Some strong words from the company’s CEO Michael J. Roffler:

First Republic’s capital and liquidity positions are very strong, and its capital remains well above the regulatory threshold for well-capitalized banks.

Impact on unrealized losses on capital ratios (JPMorgan )

{kind=link}

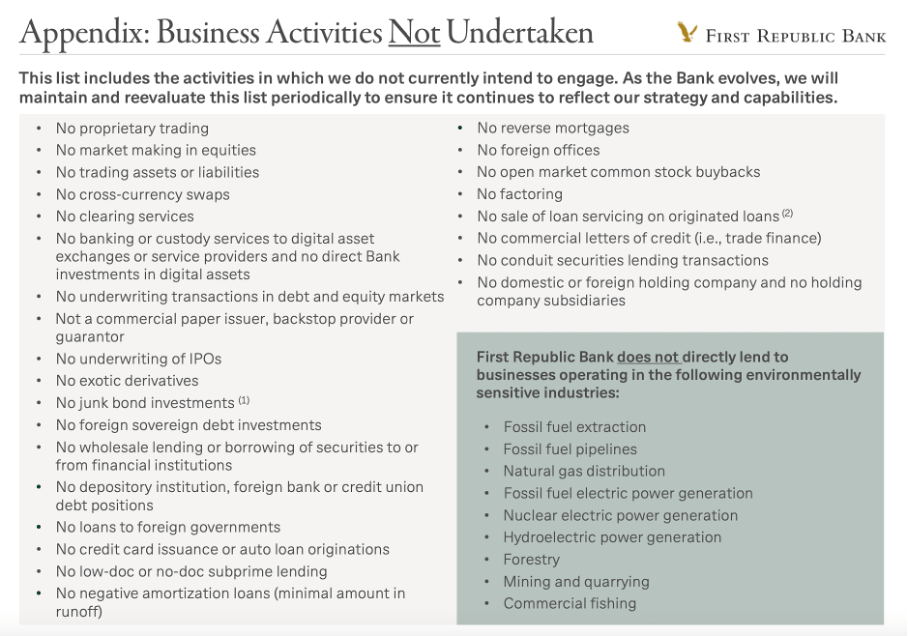

Reason 4: First Republic is a less risky bank

I also think its business activities are less risky than those of other banks. The bank offers us "Not Undertaken Business Activities" in its fourth quarter 2022 investor presentation .

First Republic does not trade in exotic derivatives, invest in junk bonds, does not issue credit cards or auto loans, and has no negative amortization loans. Therefore, the bank's operational risk is less than that of other banks in my view.

First Republic Fourth Quarter Earnings (Business activities not undertaken)

{kind=link}

Key Takeaway

The sharp decline in the regional banking sector presents a prime opportunity to buy regional bank shares cheaply, but only for investors who can handle the strong price volatility.

First Republic is a regional bank with affluent customers, and with loan write-offs of only 0%, its creditors appear creditworthy. But because many deposits are uninsured, there is a risk that depositors could take money out of First Republic. JPMorgan offered the bank $70 billion in liquidity, and the Fed offered additional funds under its Bank Term Funding Program. So I don't think many depositors will take money out of the bank due to the extra liquidity boost. And since its portfolio of investment securities accounts for only 15% of its total assets, I don't expect it to suffer huge losses if depositors flee. FactSet also provides insight into the risk exposure of 10 regional banks. First Republic came out strong from this analysis, with only 1.9% AOCI/TEC-AOCI. Looking ahead, JPMorgan came out with an analysis that showed us the dramatic result of SVB's Financial's CET1 capital ratio. The CET1 capital ratio for First Republic is expected to be strong at 6%. Moreover, First Republic's risk management is favorable because the bank does not invest in exotic derivatives, does not invest in junk bonds, does not issue credit cards or auto loans, and has no negative repayment loans. I see this as a unique opportunity, but only for the brave. I have diversified my risk into 6 stocks, as mentioned in the introduction. Therefore, I don't mind if one of the banks whose shares I own closes, as I believe the extremely low prices of these shares offer me a favorable risk/reward. Let's hope for the best.

For further details see:

First Republic Bank: 4 Reasons To Buy