FRC - First Republic Bank: Blood On The Street

2023-03-13 16:36:51 ET

Summary

- After losing heavy on Friday already, First Republic Bank stock crashed by as much as 70% on Monday, prompting a trading halt.

- In this article, I will have a look at First Republic Bank's finances - highlighting key consideration regarding the bank's balance sheet and income statement.

- The First Republic selloff appears more like an emotion-driven response to an unfortunately unique event rather than a reasonable trade anchored on fundamentals.

- With the note that this is a very high-risk trade, I assign a "Strong Buy" recommendation.

What a day for First Republic Bank (FRC). After losing heavily on Friday already, FRC stock crashed by as much as 70% on Monday, prompting a trading halt. Now, I am excited about the opportunity because I believe that the selloff has pushed FRC far below the bank's intrinsic value. If you have ever wondered what a "blood on the street" investment opportunity looks like, well, this is it. And in this article, I explain why I am buying.

Before discussing First Republic Bank's balance sheet , let's take a step back and quickly review what happened to SVB Financial Group (SIVB). In a previous article, I have tried to "simply" explain what happened to SVB Financial -- here is the abbreviated explanation:

The COVID-crisis prompted an unprecedented liquidity flood. This liquidity flood, which has been seen as a Fed put, provoked a boom in venture capital activity. This boom flushed start-ups and founders with cash, and Silicon Valley Bank, which has positioned itself as the bank for the venture capital market, enjoyed an inflow of deposits ... growing from $61.7 billion in 2019 to $173 billion as of December 2022.

Now, what should SVIB do with these deposits? With a compressed NIM spread (which was another consequence of QE), writing loans was not very attractive. So, SVIB decided to park the excess liquidity in U.S treasury securities and similar low-yield risk-free notes. Although these securities have been considered 'risk free', with the end of QE and start of QT these securities depreciated sharply in lock-step with rising interest rates. (Remember that the value/ price of a bond is inversely related to the interest rate level).

SIVB suddenly needed to struggle with falling prices of its holdings of fixed income securities. Meanwhile, concerns about a depreciating asset base were compounded by an outflow of deposits, as savers were seeking higher yield opportunities than parking cash at a bank. A balance sheet crunch was looming. And after the market woke up to SIVB's struggles, the meltdown materialized quickly.

The Balance Sheet Is Fine

The SVB Financial Group collapse was likely rooted in the decision to invest client deposits in "overvalued treasury securities," locking in a super-low yield and exposing the bank to the risk of rising interest rates. With that in mind, bank investors/ bargain hunters must ask one key question: to what extent did each bank expose itself to duration risk in its investment portfolio?

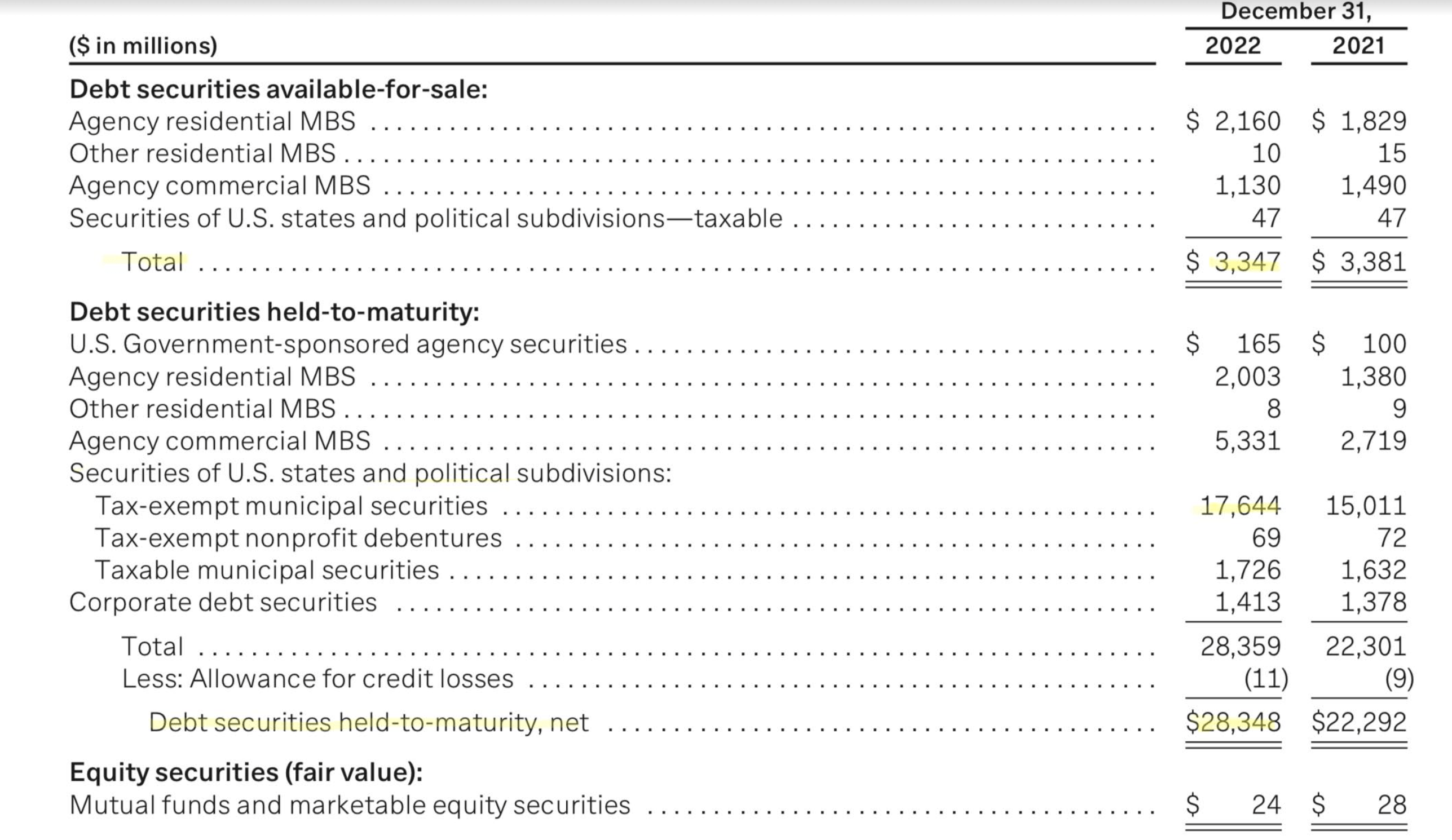

The investment portfolio of the First Republic is somewhat stretched, but stable and of good quality. The major risk asset (according to the current market narrative), investment securities, accounts for less than 15% of the bank's total asset base (about $31.6 billion). Moreover, less than 2% of these assets ($3.3 billion) are categorized as available for sale.

With regards to duration risk, FRC's latest 10-K filing disclosed that the risk is comfortably below levels that are concerning:

the weighted average duration of the available-for-sale portfolio was 4.4 and 3.9 years at December 31, 2022 and 2021, respectively. The weighted average duration of the held-to-maturity portfolio was 10.8 and 10.6 years at December 31, 2022 and 2021, respectively.

{kind=link}

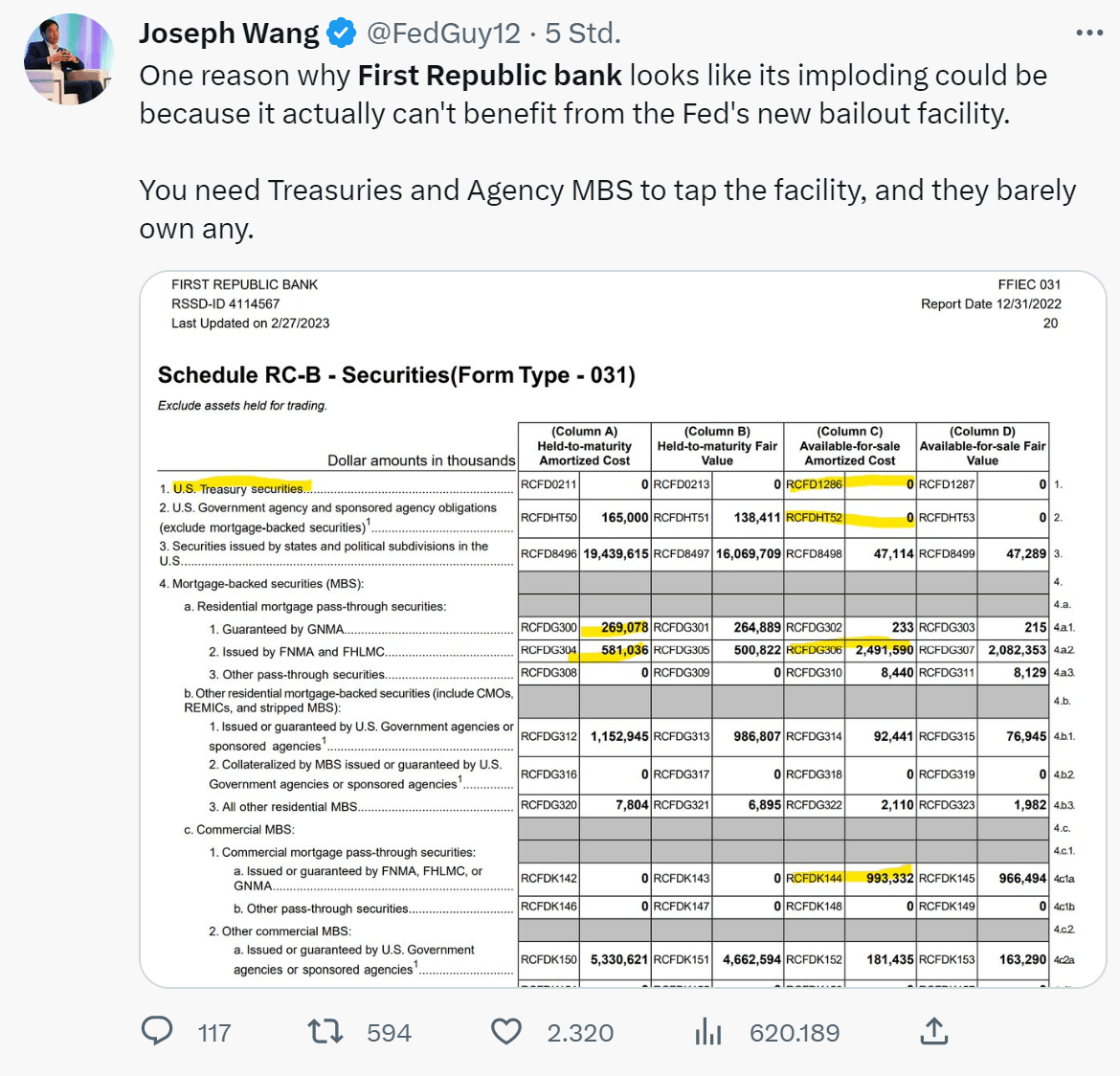

FRC's latest 10-K filing also highlights that the bank has invested about $17.6 billion in tax-exempt municipal securities, with an average credit rating of AA and an average issuer exposure of less than $40 million. This is conservative, and good news. But, due to exposure to municipal securities, analyst Joseph Wang pointed out that FRC doesn't benefit much from the FED's $25 billion Bank Term Funding Program, which is aimed to stabilize the financial system through accepting Treasuries and Agency MBS as collateral at par value.

{kind=link}

Although Mr. Wang's observation is technically correct, FRC management has already partnered with JPMorgan Chase & Co. ( JPM ) to resolve this issue -- securing access to a total of $70 billion in funds (likely through collateralized lending of said municipal bonds).

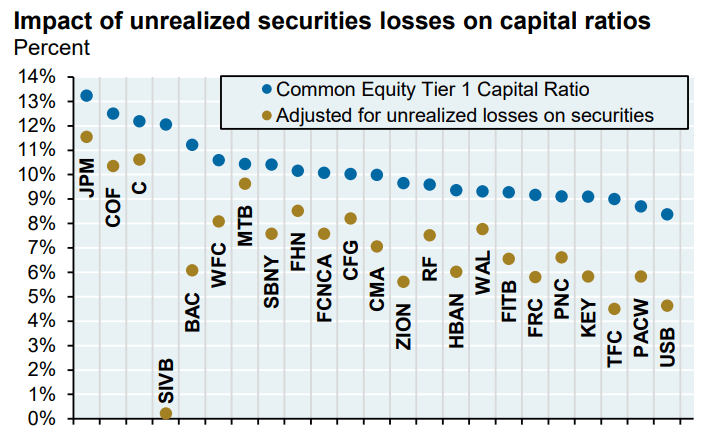

Talking about JPMorgan: the bank's research team did an excellent job modelling the impact of unrealized losses on the capital ratios of selected banks. Referencing the chart below, investors will note that SIVB's adjusted capital ratio dropped to "Zero," while FRC's respective ratio defends a level above 6% points.

{kind=link}

Don't Ignore The Business Value

Admittedly, solvency and liquidity is now the major consideration for every bank investor. But, if a bank survives the storm, bargain hunters will eventually turn to a second considerations: what is the value of the bank's operations?

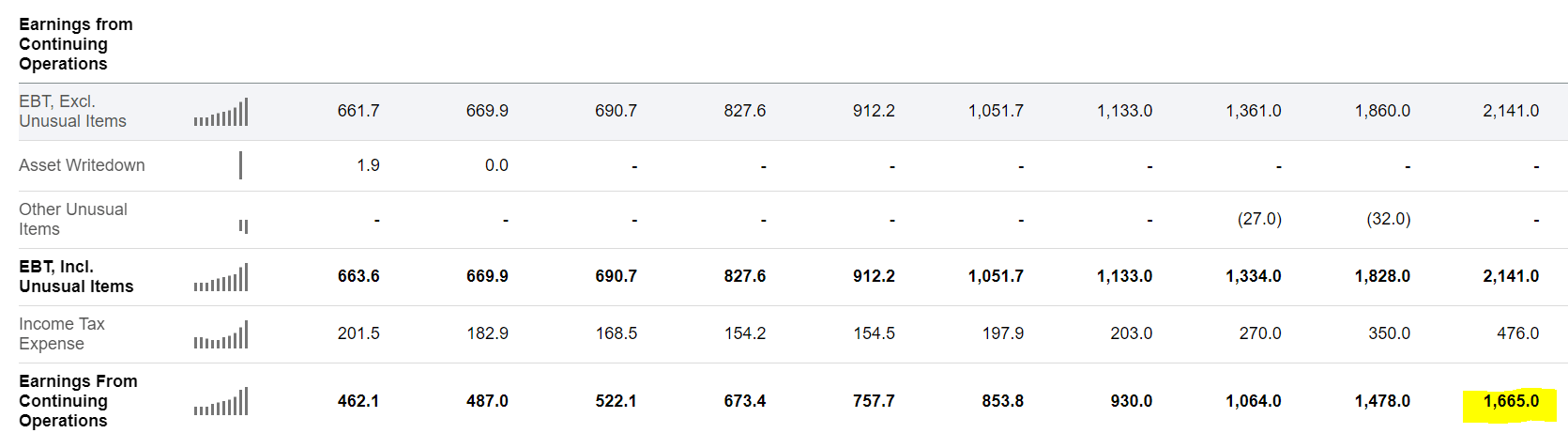

I would like to point out that for the past decade, FRC has materialized steady profitability and value accumulation. Notably, not only was there no single year when FRC recorded losses, but also was there no single year when FRC's 't+1 profitability' didn't top the previous years' earnings level.

With that frame of reference, FRC closed FY 2022 with $1.7 billion of operating income. And accordingly, valued at a $12 - $15 billion market cap (given the level of volatility it is hard to pinpoint a reference), FRC is trading at a P/E of below x10--a bargain.

{kind=link}

High Risk!

In my opinion, the market currently positions itself unreasonably risk-averse towards banks. And I strongly believe that smart risk-taking will eventually be rewarded.

But yes, investors should acknowledge that due to balance sheet leverage, banks expose investors to elevated tail risk as compared to businesses outside of the banking industry. And, reflecting on the events of the past few days, I would not rule out that First Republic Bank equity holders could lose every cent of their investment. Every investors should decide for him-/ herself if he/ she can take such risk.

Buy The Panic

Reflecting on a solid balance sheet, paired with strong profitability, the First Republic Bank selloff appears more like an emotion-driven response to an unfortunately unique event (the SVB collapse) rather than a reasonable trade anchored on fundamentals.

I like to view First Republic Bank stock at $30/share as a very attractive bargain opportunity. And, with the note that this is a very high-risk trade, I assign a "Strong Buy" recommendation.

For further details see:

First Republic Bank: Blood On The Street