FRC - First Republic Bank: I See No Value In The Equity

2023-04-19 07:30:00 ET

Summary

- First Republic Bank is on life support.

- The value of equity is deeply negative.

- The loan portfolio is largely fixed and funding costs have just gone up materially.

- It is equivalent to holding a long-duration bond on a 10:1 leverage and just receiving a margin call.

- I see limited upside and high risks in buying the shares.

In my prior article , I shared my view on the Japanification of the U.S. banking system and the birth of a new class of zombie banks.

I believe that First Republic Bank ( FRC ) is clearly an example of such a zombie bank.

Many commentators have focused on the unrealized losses on its Held-To-Maturity ("HTM") securities portfolio. However, the real issue in my view is the mostly fixed-yield loan portfolio, which originated in the low-interest rates era, that is now an albatross around its neck. That portfolio, if marked-to-market, suggests that the value of its equity is deeply negative. Some investors are hopeful that a recovery may take place but I do not see many plausible avenues for a sustained recovery. The yield on its loan portfolio is fixed for many years at very low rates considering its cost of funds currently.

Paradoxically, the only thing that can save FRC is a deep recession forcing rates to decline precipitously but more on that later.

Having gone through several Investor Relations presentations by the FRC team (recent example here ), I do acknowledge that credit risk on loan assets has been exceptionally well managed.

On the flip side, there appears to be complete mismanagement of interest-rate risks. The loan book, to a large extent, is a long-duration fixed interest that was locked in a low-rates era whereas the funding cost is mainly driven by short-term interest rates. Asset and liability matching is a fundamental aspect of the banking business model and really, it is banking 101. I am quite shocked by the failure of risk management in this instance.

The share price in the last 12 months is compared to the Invesco KBW Regional Banking ETF ( KBWR ) below:

Starting from Q3-2022, it appears that some investors already spotted the interest-rates mismatch and pressure on net-interest margin ("NIM"). Clearly, the Silicon Valley Bank Collapse (SIVBQ) exacerbated the issue as it dented confidence in the banking system as well as forced deposit outflows, and subsequently drove repricing of deposit costs higher for many banks.

The Loan Book

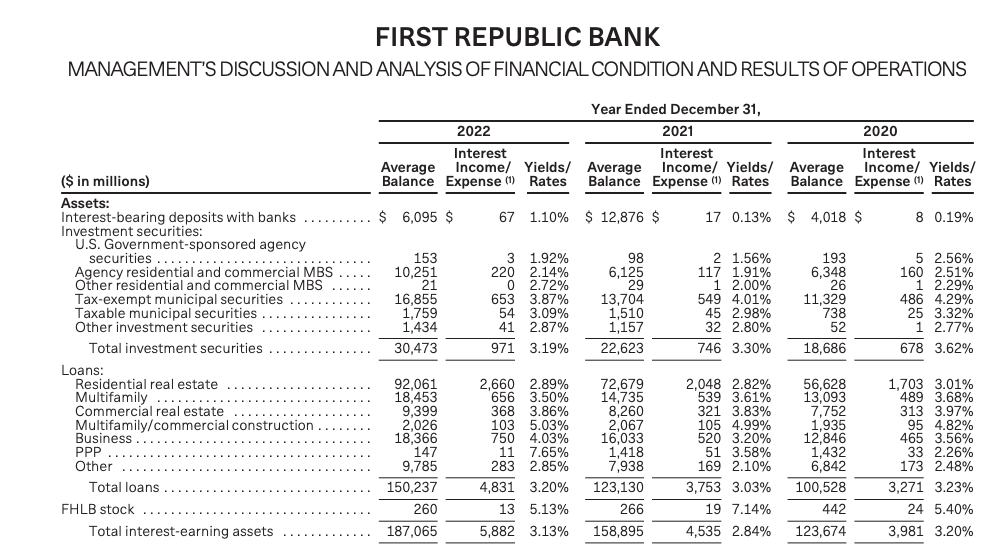

FRC's asset and loan book and associated yields as of 31/12/2022 are provided below :

{kind=link}

As you can see from above, the majority of the book is Residential real estate ($92 billion) that is yielding only 2.89% whereas the total interest earnings assets are 3.13%.

The deposits as of 31/12/2022, are provided below:

{kind=link}

As you can see, the cost of deposits is a mere 0.71%. Except that this figure is an average across 2022. The end-of-period cost of deposits would be substantially higher which will be the starting point for Q1 2023.

More importantly, the banking turmoil and huge deposit outflows would mean that the marginal cost of deposits for FRC is in the range of 4% to 5%.

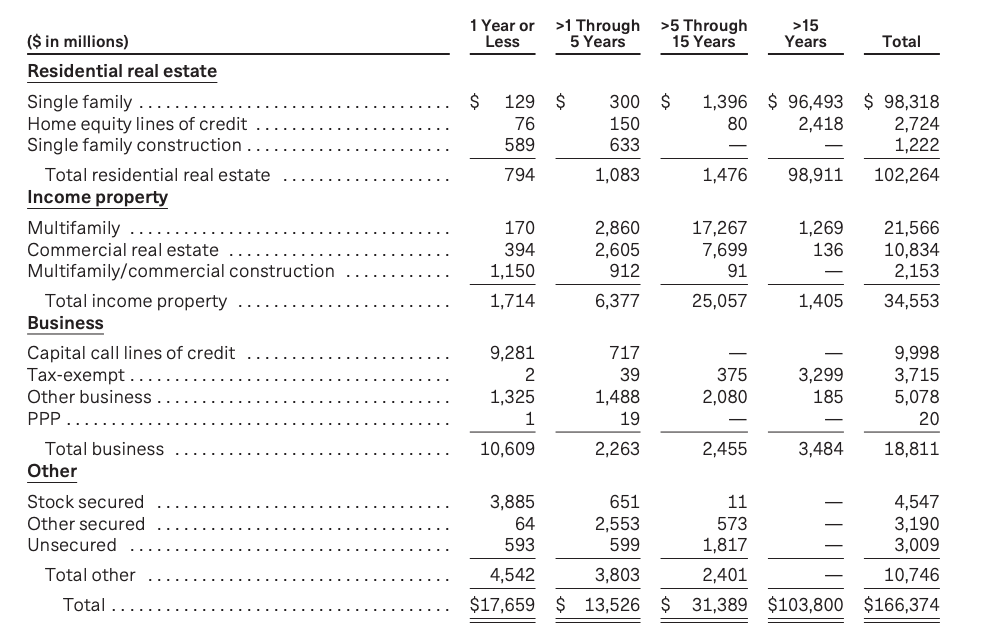

The maturity profile of the loan assets is shown below:

{kind=link}

As can be seen, these are long-duration assets whereby $103 billion (62%) of the book matures after 15 years, mostly driven by single-family residential real estate.

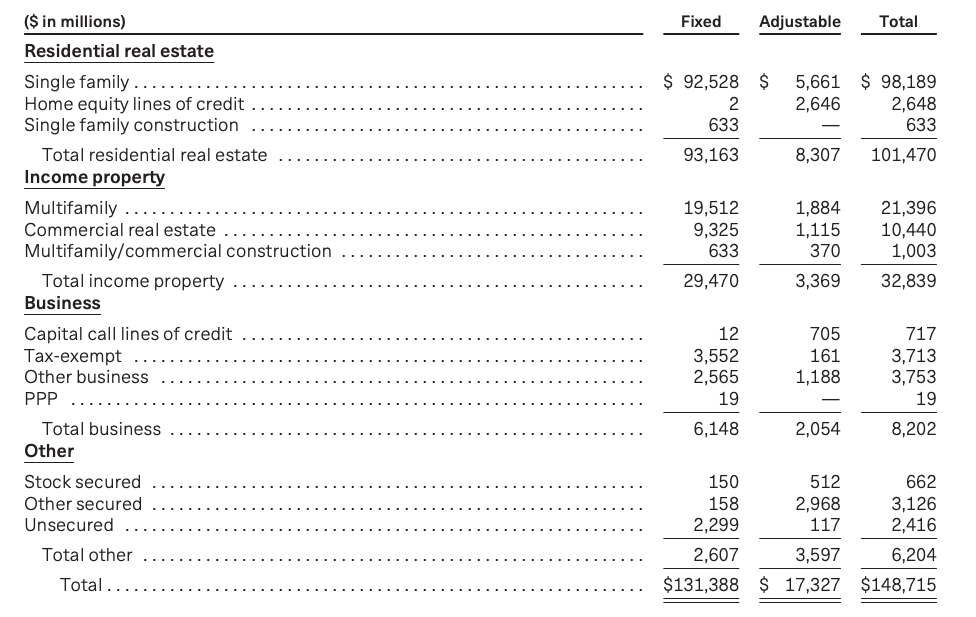

A deeper look at the composition of the assets (variable versus fixed) is provided below:

{kind=link}

The majority of the loans ($131 billion) are fixed for at least one year.

Further breakdown is provided in the table below:

Additionally, close to 60% of the Single Family loans provided are interest-only loans and the majority of these only begin to amortize in 2028 and beyond:

{kind=link}

To summarize, parts of the FRC loan book are effectively equivalent to a long-duration bond which are held on margin given the fixed yield on the majority of its assets. The management team did not hedge its interest-rate risks. According to this Bloomberg article , the loan book is the key reason why an acquisition transaction hasn't taken place and estimates that a mark-to-market of the loan book will result in a ~$19 billion impairment whereas the current value of the tangible equity is less than $14 billion. Additionally, the HTM losses as shown below (as of 31/12/2022) are ~$4.6 billion.

FRC 10-K

What Can Save The Bank?

Customers with fixed loans with low rates (especially on interest-only terms) are not going to refinance the loans anytime soon. The problem faced by FRB is that its marginal funding costs are now in the range of 4% to 5% and the bank is essentially on life support provided by the large banks ($30 billion of deposits) and other emergency lending from the Federal government. According to the Bloomberg article, analysts are expecting ~$40 billion of deposit outflows in Q1 2023.

Paradoxically, the thing that can help the bank is a deep recession and rates falling precipitously as a consequence. As noted before, the credit risk of the loan book is very well-managed so any losses would be more than offset by lower cost of funds.

Final Thoughts

FRC's unfortunate position in my view is completely self-inflicted and a direct result of the colossal failure of risk management. FRC focused on credit risk management but the obvious blind spot was interest rate risk and asset/liability matching which is simply banking 101. The bank holds a position equivalent to a long-duration bond given fixed yield on most of its loans which is leveraged ~10 to 1 (as a bank) and just received a "margin call" (the margin call in this analogy are the deposit outflows).

Facilitating an acquisition is quite challenging because a would-be acquirer would need to mark-to-market the book and absorb a multi-billion write-down even if it acquired the common shares for $0.

The loan assets are largely set in stone and not going to reprice to the current rates environment any time soon. I also find it difficult to believe that low-cost deposits will return to this bank en masse either.

The only hope is that interest rates will decline and the bank will, over time, remix the loan assets to higher-yielding assets.

The Fed is concerned about systemic risk and additional banking turmoil and would like to facilitate an orderly transaction. I suspect in such a scenario, the price paid for the equity may be nominal. The coordinated deposit injection by the large U.S. banks, in my view, was designed to prevent further contagion. Whilst I believe that these deposits are safe, protected by the capital and debt structure, I believe the equity holders may get completely wiped out.

Given the above, I see a limited upside in the share price near term and adverse asymmetric risk/reward binary outcomes. I will continue to monitor developments and especially the upcoming earnings release including end-of-period deposit cost and what it means to the going-forward profitability of FRC. At this juncture, FRC looks and feels to me like a zombie bank that is on life support by the Fed.

For further details see:

First Republic Bank: I See No Value In The Equity