FRC - First Republic Bank Q1 Earnings: Equity Is Likely Worthless Avoid

2023-04-24 22:40:00 ET

Summary

- The Q1 earnings release was not pretty.

- Deposit outflows were higher than expected at $103 billion.

- First Republic Bank is on life support.

- I suspect it is being readied for a sale transaction.

- My view remains that the equity is worthless and suggest to avoid.

In my recent article on First Republic Bank ( FRC ), I saw no value in the shares. The 1Q earnings validated my view. I think there is a meaningful probability the share price may go to $0 in the next few months, probably due to a transaction being consummated. FRC is on life support at the moment by the Fed and this is not going to be sustainable in the medium term. The Fed will likely want to find a path to an exit as soon as practicable.

The deposit outflows of $102 billion were much worse than I and the Street expected. The adjusted net-interest margin ("NIM") was reduced to an adjusted 1.66% from 2.45% in the prior quarter. Note, however, that this is an average quarterly figure for Q1'2023, the full impact is going to be reflected in the next quarter. So treat this figure as a rear-view mirror as opposed to the true NIM.

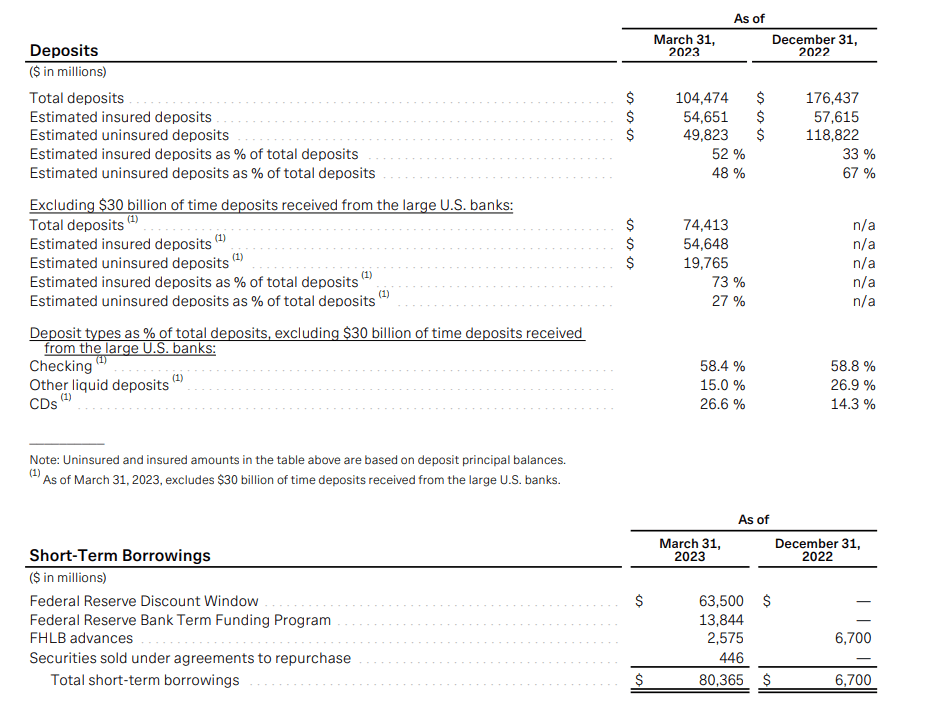

The deposits and long-term borrowing composition as of the end of Q1 are shown below:

{kind=link}

FRC Investors Relations

All the short-term borrowings and large chunks of the deposits will be attracting interest rates of 4% to 5.15%. Note that the $30 billion of deposits from the large U.S. banks are included in the figures above.

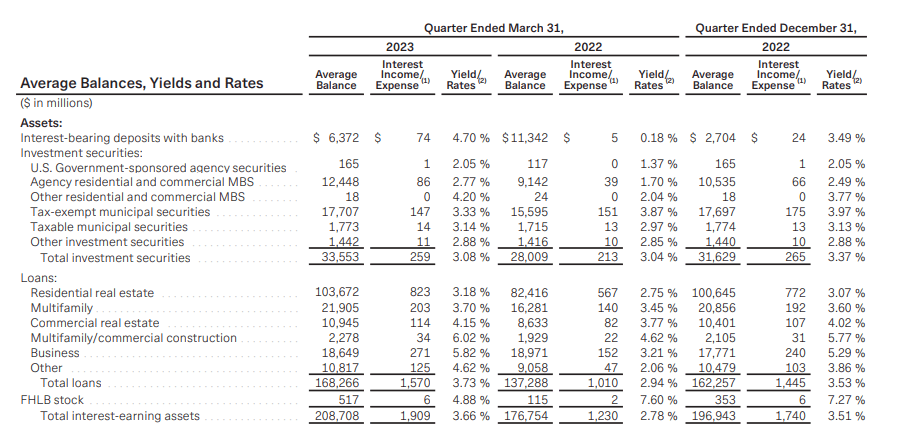

The vast majority of its asset's earnings balances (such as $103 billion of real estate loans and $33 billion of investment securities earn lower yields of 3.18% and 3.08%).

{kind=link}

FRC Investor Relations

This is a significant negative carry that is simply not sustainable as it will erode FRC's capital base and feed that vicious cycle of lack of confidence and instability.

Management Actions

The management team shared that the following in terms of mitigating actions:

- Providing off-balance sheet liquidity solutions for clients. The objective is to ensure customers remain in the eco-system of FRC even if they do not directly deposit with the bank.

- Educating customers on optimizing their FDIC deposits insurance options (e.g. by splitting deposits between family members or other banks)

- Deleveraging the balance sheet by reducing origination volumes as well as shifting the model to originate-to-sell in the secondary market whilst retaining the servicing.

- Meaningfully reduce the cost structure by eliminating 20% to 25% of the headcount during the second quarter. These include reductions in compensations for senior management, real estate consolidation, and non-essential projects.

Finally, management also hinted that they are "we are pursuing strategic options to expedite our progress while reinforcing our capital position" without providing any further color on what these may be.

The Path Forward

The actions taken by management, in my view, are going to have an impact only at the margin and perhaps buy some more time. The structural position of their business in the current rates environment is disadvantageous and is going to profusely bleed massive losses in the quarters to come. The true NIM picture will only show in the next quarter. I also do not see a viable path for it to recover a large portion of the $102 billion of low-cost deposits it lost during March 2023.

Additionally, I highly suspect that FRC is subject to heightened regulatory scrutiny and oversight by the Fed currently. In such a scenario, shareholders' interests are unlikely to be prioritized. The current priority is to prevent a systemic event and contagion to other banks whereby the preferred path remains a sale transaction to another bank. The complicating factor is the capital hole estimated in my prior article at around $25 billion. I believe that the mitigating actions taken by the management team (especially the deleveraging) are designed to prepare the bank for M&A transactions.

Final Thoughts

Reading the tea leaves from the Q1 disclosures and earnings call indicate to me that FRC is in dire straits. All the signs are flashing bright red:

- The deposits outflows of $102 billion were materially higher than expected and not showing any signs of recovery;

- The short-term borrowing from the Fed at above 5% stand at a massive $80 billion;

- The capital hole is estimated at ~$25 billion;

- Deleveraging is a prolonged exercise and will be costly;

- Both the common and preferred dividends are suspended indefinitely;

- The management team did not open the earnings call for Q&A avoiding the tough questions (for example, NIM projection for the next quarter)

The above suggests to me that shareholders' interests are not a priority in the current circumstance and probably would come last. Previously, I described FRC as a zombie bank but I suspect, at some point in the next few months, it will be sold. In such a scenario, the equity is worthless. Betting on a recovery here does not make sense to me. I continue to avoid FRC stock like the plague.

For further details see:

First Republic Bank Q1 Earnings: Equity Is Likely Worthless, Avoid