FRC - First Republic Bank's Very Real Path To Survivability

2023-04-05 02:58:02 ET

Summary

- First Republic Bank has suffered significant deposit outflows since March 9 and the health of the bank is still unclear, given the limited information shared by management.

- Doing a deeper analysis of the financials, it is clear that FRC would need to shrink its balance sheet, which would impact profitability, regulatory ratios, and tangible book value.

- Although the path to survivability is narrow and risky, in our view, very real and has the potential to reach a $30 per share tangible book value.

Editor's note: Seeking Alpha is proud to welcome The Ten-Q Analysis as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Background

There is still no concrete news from First Republic Bank (FRC) regarding its internal health since the run on the bank last month. Investors have very limited information to go by - the most relevant being the 10-K for the year-end 2022 and the 8-K released on Mar 16. Analyzing these documents, and making some reasonable assumptions, it appears that First Republic will be able to weather this storm and emerge with a tangible book value of approx. $30 per share.

Why First Republic

The last 3 weeks have been dramatic (to say the least) for the banking sector in general and for First Republic Bank in particular. Starting with the crash of Silicon Valley Bank on March 8th, the run on First Republic Bank and other regional banks has taken a toll on the deposit base and consequently on the survivability of these banks.

First Republic Bank has become the firewall after the fall of Silvergate, Silicon Valley Bank and Signature Bank in the US and the forced takeover of Credit Suisse (CS) by UBS (UBS) orchestrated by the Swiss regulators. Another failure in the US would mean a further loss of confidence and flight from local regional banks and further bank failures would be both a regulatory and financial nightmare scenario.

The Federal Reserve's Bank Term Lending Program ((BTFP)) facility essentially ensures that banks like First Republic do not need to go into receivership in the near future, since they can borrow at par against their long dated assets without the need to sell them immediately. The cost of such borrowing could impact their profitability and hence an impact on available capital, but that is a slow death scenario rather than a sudden death (like that of SVB).

Net Outflow of Funds

Now let's analyze what the current outflow impact may look like on the liquidity situation at FRC. As of their last financial statement (Dec 2022), First Republic had an uninsured deposit of $119.5 billion out of a total deposit base of $176.4 billion (approx. 68%). There have been several estimates of how deep the deposit outflow was and range from $70 billion to $90 billion.

A rough calculation using First Republic's 10-K filing for year-end 2022, the 8-K filing on March 16, 2023 and WSJ estimate of the outflow:

Authors estimate based on data from FRC 2022 K-1, 8-K from Mar 16 and WSJ (Mar 19)

Since the borrowing from Fed (discount window + BTFP) for Mar 22 ($164 billion) and Mar 29 ($153 billion) have similar levels as for Mar 15 ($165 billion), we assume that most of FRC's borrowing from the Fed have not been returned.

Cash available on Mar 15 did not include the $30 billion uninsured deposits from the 11 largest US banks.

Liquidity Sources

It is quite clear by now that First Republic has handled the liquidity situation given that anywhere from $70 billion to $90 billion of deposits may have left the bank. This is primarily thanks to the Fed Discount Window and the Bank Term Funding Program which has been available since March 12. In addition, $30 billion has been deposited for 120 days by the top 11 US banks as uninsured deposits on March 16. This ensures that FRC does not need to resort to a fire sale of the assets to fill in for the lost deposits.

Since FRC is likely not going to die of liquidity squeeze, the bank can evaluate other options in order to realign the balance sheet. Here, we explore one such option in a stand-alone scenario by selling assets rather than parts of the business or doing an equity or debt raise.

Shrinking the Balance Sheet

First Republic would need to shrink its asset portfolio in order to match the deposit outflow. While doing this, it may have to sell assets that are at or close to carrying value in order to minimize the realized losses and hence keep its equity ratios intact.

FRC 2022 K-1

Here are some possible assets that can be sold while minimizing losses and hence the impact on equity (Source: FRC 2022 K-1).

Author's estimate based on data from FRC 2022 K-1

We assume that loans originated in Q4 2022 and Q1 2023 should be marked very close to the carrying values and should have minimal losses if sold. The above estimate shows that approx. $70 billion of deposit outflow can be covered by selling approx. $77 billion of assets, while booking about $7.6 billion of losses. In addition, according to our estimates, the fair market value of debt securities may be 2-3% higher now than reported at the end of 2022 (due to a drop in interest rates since then), further reducing the loss.

In addition to the sale of assets, First Republic can let the loans roll-off its balance sheet and reduce it over time. Based on the latest K-1, our estimate is that for the full year 2022, approx. $14 billion of older mortgages rolled off the balance sheet - it is possible that some of these were refinanced earlier in the year due to lower interest rates still available then. In Q4 2022, approx. $1.2 billion of mortgages rolled off the balance sheet, which is significantly lower than the full year average, possibly because of higher interest rates. Assuming the same trend (as Q4 2022), we would assume that approx. $5 billion of loans can roll off the balance sheet in the next 12 months.

Impact on P&L

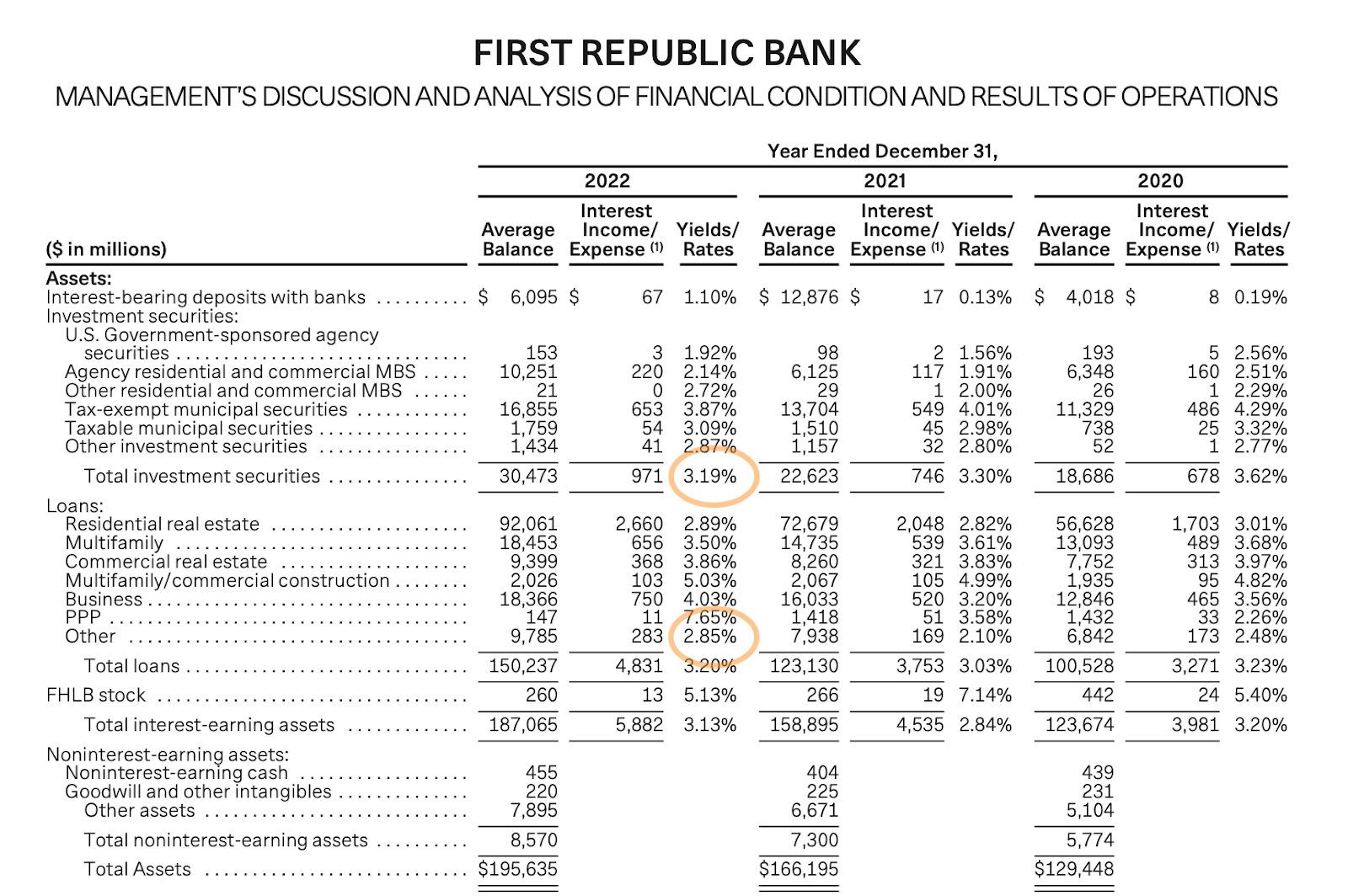

Next, we calculate the potential impact of selling these assets on the P&L of the bank. According to the 2022 K-1, the available-for-sale and hold-to-maturity investment securities yielded on an average about 3.19% for the year 2022. We assume that the loans originated in Q4 2022 would yield approx. 6.5% based on the prevailing mortgage rates at the time. The impact of loans originated in Q1 2023 is not considered since we are working with a baseline P&L of 2022 full year results in which these loans were not included. The 'other loans' category had an average yield of approx. 2.85% in 2022.

{kind=link}

Based on these numbers, we arrive at the following impact to the revenue:

Author's estimate based on data from FRC 2022 K-1

In addition to the impact on the revenue side, we can calculate the impact on the expense side of the P&L. Based on the latest 10-K report, FRC paid $654 million in interest expense on the deposits for the full year 2022. However, compared to the 10-Q for Q3-2022, it appears that $428 million of the interest expense on deposits was incurred in Q4. Annualized and computed on a year-end deposit of $176.4 billion, it appears that interest expense was running at about 1%. Assuming $90 billion of deposit drawdown we arrive at a drop in interest expense of approx. $0.9 billion.

Assuming a worst case $90 billion deposit drawdown and a $77.2 billion asset sale, FRC would need to cover about $20 billion using Fed or FHLB borrowing at a cost of approx. 5%.

Based on these assumptions, here is our estimate of the impact to pre-tax income:

Author's estimate based on data from FRC 2022 K-1

In addition, the cancellation of dividend on common stock (although does not impact P&L), but will improve cash flow by another approx. $190 million (based on 2022 K-1). Adding back stock based compensation expense and depreciation (total approx. $400 million in 2022) could make FRC cash flow positive even with a reduced balance sheet.

If the more expensive borrowing from the Fed discount window can be eliminated over the next 12-18 months, with a combination of deposit increases, loan roll-off at the rate of $1-2 billion per quarter and cost controls, there is a clear path to pre-tax income in the range of $0.7 billion to $1 billion.

Impact on Tier 1 Leverage Ratio

The Tier 1 capital leverage ratio at the end of 2022 was 8.51% based on a Tier 1 capital of $17.6 billion and average assets of $206 billion (as reported in 2022 K-1). Assuming a reduction of $77 billion of assets and a Dec 2022 asset base of $212 billion, the new asset base would be ~$135 billion.

Estimate of the impact on Tier 1 leverage ratio under these assumptions and based on redemption of senior notes on Feb 12, 2023:

Author's estimate based on data from FRC 2022 K-1, 8-K (Feb 13)

The new Tier 1 capital after adjustment for the redemption of senior notes (in Feb 2023) and the estimated loss on the sale of assets, would be about $10.5 billion. The new Tier 1 leverage ratio comes to around 7.8%, which is still considered well capitalized under regulatory standards.

Impact on Tangible Book Value and Common Equity

FRC reported total equity of $17.4 billion at the end of 2022 and reducing the preferred equity, the common equity was $13.8 billion and a tangible book value of $13.6 billion. After adjusting for the redemption of senior notes and the assumed loss on sale of assets, we arrive at an equity of $9.3 billion, common equity of $5.7 billion and a tangible book value of $5.5 billion.

Estimate of the impact on common equity and tangible book value under these assumptions:

Author's estimate based on data from FRC 2022 K-1, 8-K (Feb 13)

Using outstanding common shares of 183.2 million at the end of 2022 (from K-1) and 186.2 million now (increased due to stock offering on Feb 8 comprising of 2.5 million shares and greenshoe option), we compute that the tangible book value would drop from $74.2 to approx. $30 per share.

The Path Forward

There are a limited number of options that can help First Republic make this transition into the new normal. Let's explore some of these and also the ones that are most likely to succeed.

-

An outright acquisition is not likely because the mark-to-market losses on the loan portfolio would leave a large unfilled gap in the balance sheet.

-

A share capital increase using a public / private offering also seems unlikely because of the depressed share price and significant dilution that would be required.

-

The option that we have discussed so far (and which seems most likely) is selling assets with the least amount of unrealized losses and covering the remaining shortfall through Fed and FHLB borrowing - and such borrowing, in our opinion, can be brought down in the next 12-18 months using a combination of deposit increases, loan roll-offs and cost cutting.

-

In combination with the above, FRC can sell convertible bonds that are more favorable to the cash flow in the immediate term but have a sweetener in the end (e.g.: a zero-coupon convertible bond at an attractive conversion price).

-

Another option would be to sell off a portion of the business such as the Investment and Wealth Management business which could raise enough capital and shore up the balance sheet.

The path forward for FRC is not without its risks:

-

We assume that FRC is able to sell the assets at close to fair market value. It is possible that some of these assets may have to be sold at a discount to fair market value. Since most of the asset to be sold would likely comprise of tradable debt securities or high quality loans, it is likely that they can be sold at close to fair value.

-

It is possible that the deposit outflow is greater than that projected in this scenario, in which case, the cuts required could be deeper and would threaten the viability of this approach.

Conclusion

With the Fed's Bank Term Funding Program, it is unlikely that banks like First Republic would go into receivership in a hurry, since the borrowing allows them time to align their balance sheet. The path is not easy, but is nonetheless very real. With a high power advisory team from JPMorgan (JPM), Lazard (LAZ) and McKinsey helping them, it is our opinion that First Republic would be able to come out of this as a strong (albeit smaller) regional bank but the transition to the new normal would be painful in the next 12-18 months.

For further details see:

First Republic Bank's Very Real Path To Survivability