SI - First Republic Bank: Systemic Exposure Risks Exist

2023-03-14 08:18:42 ET

Summary

- First Republic Bank took a beating recently, as concerns mount over its ability to remain in stable condition.

- This follows real pain that should have been seen from a mile away that has impacted similar financial institutions.

- Risk absolutely exists here, but upside potential could also be on the table for investors who don't mind that risk.

Not since the early days of the COVID-19 pandemic have we seen market turbulence of this magnitude. The fact of the matter is that the economy has gone from looking incredibly robust to looking perilous in less than a week. A string of bank failures, starting with Silicon Valley Bank, which is owned by SVB Financial Group ( SIVB ), has created a great deal of uncertainty and has elevated the risk profile for every market participant. They say that hindsight is 20/20. This is absolutely true. Looking back now, this risk should have been top of mind for regulators, investors, and more. And yet, almost nobody, myself included, saw it coming.

There will be significant losses during this time for some investors. Having said that, there also could be some attractive opportunities. One prospect that warrants some interest is First Republic Bank ( FRC ). On March 13th, shares of the company plunged, closing down 61.8%. The fear here is that the firm could face some of the contagion that has spread over into the financial sector. Structurally, there are some issues with the company that would lend itself to being susceptible to current market conditions. But as of yet, it has not been pushed into the same corner that its peers have been. For investors who don't mind a higher-risk prospect that could offer some significant upside, this may be a firm worth buying into.

Understanding what has happened

Before we get into discussing First Republic Bank specifically, it would be helpful to provide some insight into what has already transpired and why. Last week, the federal government took over Silicon Valley Bank after it became clear that a large bank run had developed. Had you mentioned the possibility of such a bank run a couple of weeks earlier, the thought would have seemed ludicrous. After all, the company had $211.8 billion of assets and deposits totaling $173.1 billion as of the end of the 2022 fiscal year . Although certainly not the size of some banks out there, the failure of the company makes it the second-largest bank failure in the history of the US.

What’s really remarkable is how fast all of this happened. You see, banks are structured to be able to handle withdrawals. They do this by holding a certain amount of their capital in the form of cash, while having a sizable chunk also in available-for-sale securities. As of the end of its 2022 fiscal year, for instance, SVB Financial Group had $13.8 billion in cash and cash equivalents. It also had $26.1 billion in available-for-sale securities. These are securities that are usually dated for short-term investments that the company can sell while realizing little to no loss if need be. The company then had $91.3 billion in held-to-maturity securities that, by definition, have longer durations. These can be more susceptible to fluctuations in interest rates. But if they are held to maturity, they collect the amount they are supposed to regardless of the economic environment.

In a typical environment, this kind of setup would probably be fine. But this is an unusual company in an unusual environment. Anybody watching closely would have definitely noticed that no longer than last Thursday when the company saw attempted withdrawals of about $42 billion. Of course, the actual carnage began a bit earlier than that. With withdrawals coming in earlier last week, the company sold $21 billion worth of bonds that consisted mostly of U.S. Treasuries. That occurred on Wednesday. But because of the interest rate environment and the need to raise the capital quickly, the company ultimately booked a $1.8 billion loss on the transaction. The firm tried to cover this by issuing common and preferred stock totaling $2.25 billion. But that deal collapsed rather quickly. It was then that, last Friday, the bank went into receivership under the FDIC.

Fortunately for depositors, the government has said that all accounts within the bank will be made whole. This was a wise move, but it did little to stop the contagion from spreading. Signature Bank ( SBNY ), an enterprise with $110.4 billion worth of assets and $88.6 billion of deposits, was ultimately seized this past Sunday after, on the prior Friday, depositors withdrew $10 billion. That collapse makes it the third-largest banking failure in the history of this country. We also saw some other shockwaves through the system. For instance, Silvergate Capital Corporation ( SI ) announced last Wednesday that it would be winding down its operations and liquidating its bank. While there are some similarities between it and the other two banks, there are some differences as well. For starters, it was a far smaller bank to begin with, with assets of only $11 billion. But operationally, it also was special in the sense that it focused on the cryptocurrency space.

A long time coming

My formative days in investing came during the financial collapse of 2008 and 2009. The lessons I learned during that time caused me to always be on the lookout for Black Swan events. Knowing what I know as of this writing, I recognize that I failed entirely to see exactly what was around the corner and what should have been obvious. In the economy, some of the most financially unstable companies are venture-funded startups. High startup costs, low revenue, and significant costs for ramping up operations, all make this space susceptible to changing market conditions. Even companies that are fairly sizable today that are still relatively young and that were funded by venture capital before becoming publicly traded can generate significant net losses. A great example of this can be seen by looking at Robinhood Markets ( HOOD ), with a market capitalization of $8.1 billion and a net loss in 2022 of just over $1 billion.

Where a low-interest rate environment could be fuel for these types of companies, a high-interest-rate environment can prove a death blow. And when you really look deep into the data, you will see that these developments have been building up for several months. To understand what I mean, we should look at both the low end of the startup market, and the high end. On the low end, we have the startups that are just raising capital. Although comprehensive data it's hard to come by when it comes to the really early-stage firms, we do have a glimpse at some of the first outside funding that those businesses receive. A plethora of data regarding these types of companies exist on the crowd-raising platforms out there like StartEngine and WeFunder.

{kind=link}

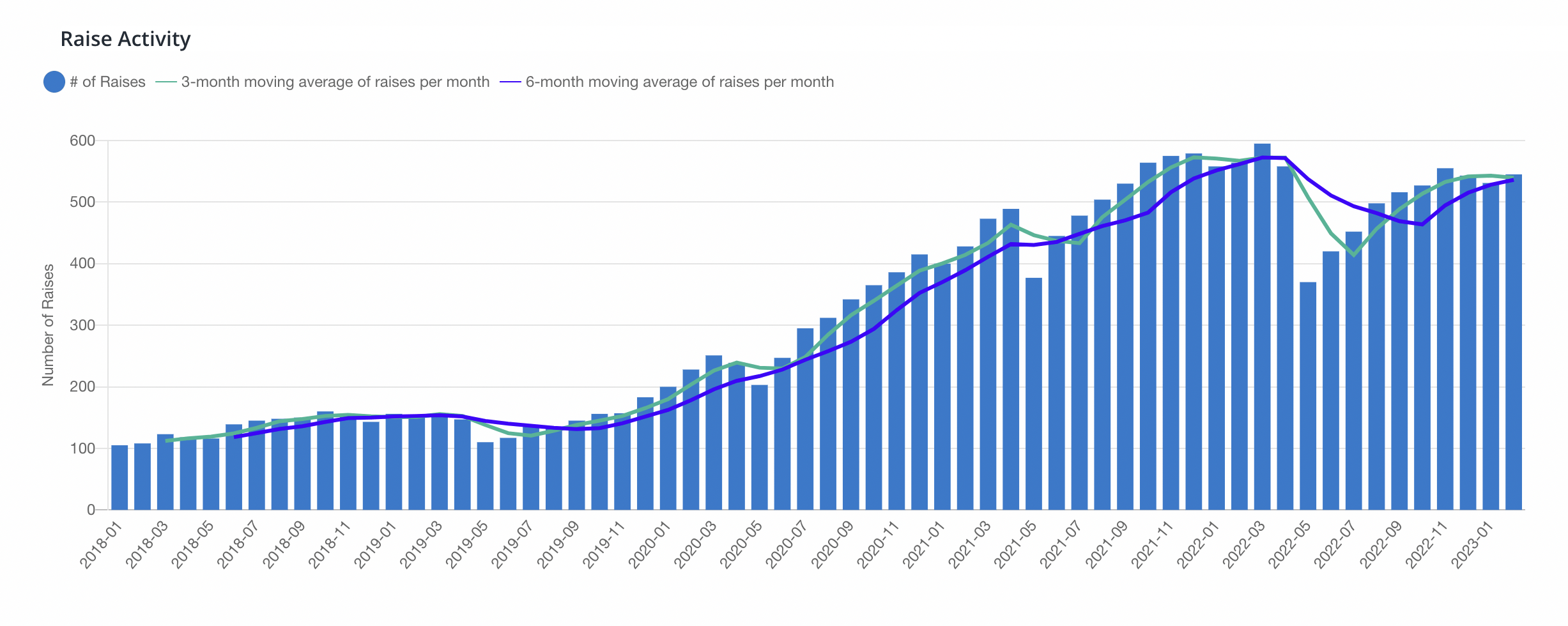

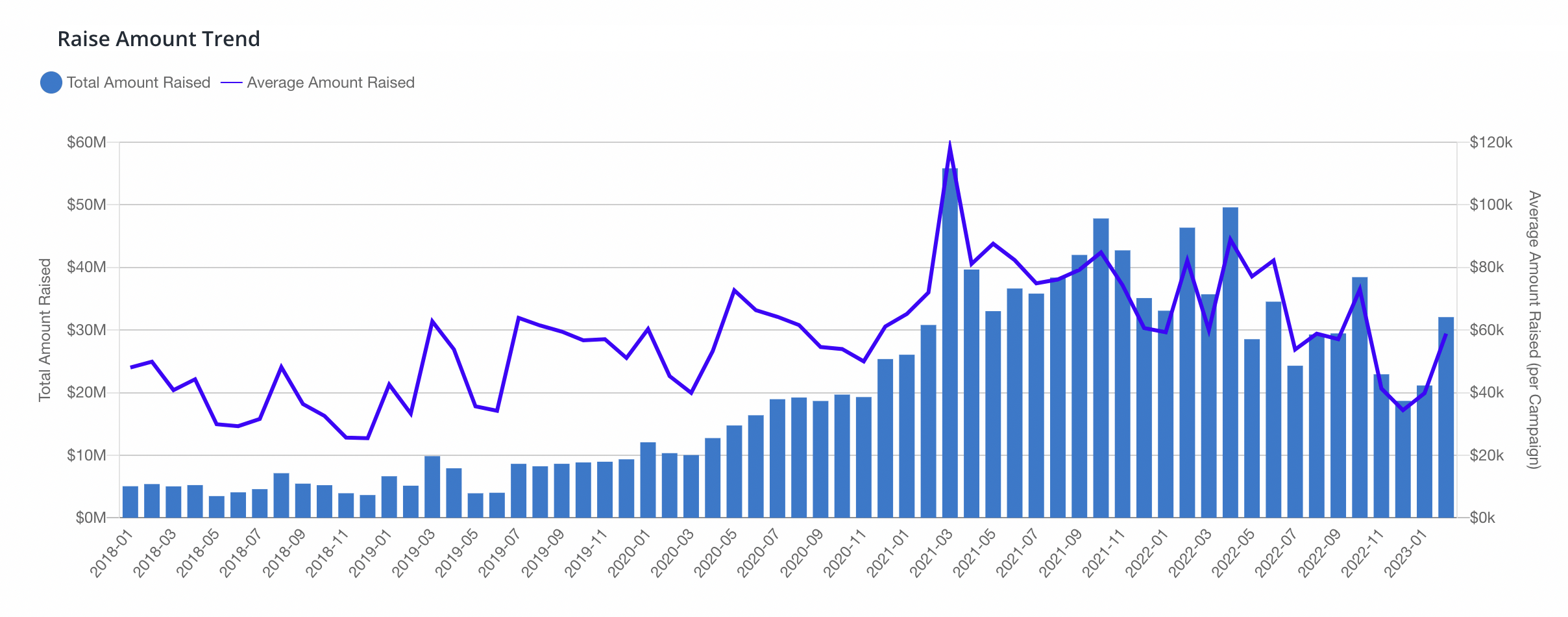

Aggregating the data, we get some interesting results. As you can see in the chart above, we have started seeing, over about the past year, year-over-year declines in the number of raises from companies that are raising outside capital. In February of this year, for instance, only 545 companies were raising. That’s down from the 564 experienced the same month one year earlier. In the chart below, you can also see a more startling trend. In addition to the number of raises dropping, the total amount being raised has also declined. In February of this year, for instance, the startups that were raising money succeeded in capturing only $32.1 million. That's a significant decline from the $46.4 million reported the same time one year earlier.

{kind=link}

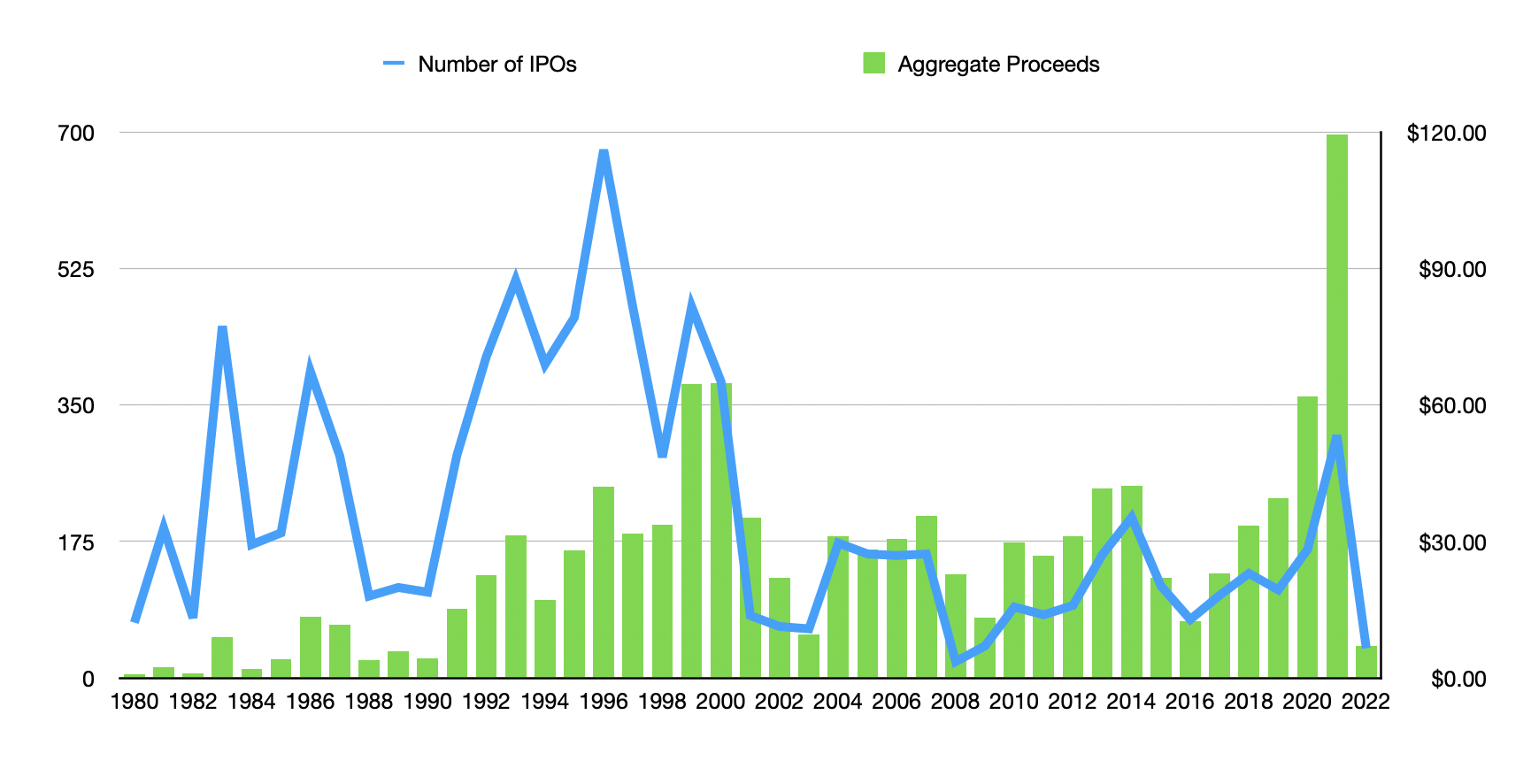

When you move to the higher end of the spectrum, you have the companies that are going public. This is often seen as the end of being a startup and the beginning of being a ‘big boy’ company. We don't have quality monthly or quarterly data on this. But we are fortunate enough to have annual data. And frankly, the 2022 calendar year was awful. During that year, there were only 38 IPOs. That's down from the more-than 20-year high of 311 experienced in 2021. In fact, in order to get a number at or below this, we have to go back to 2008 when there were only 21 IPOs. When looking at the amount of capital raised, the picture is even worse. In 2022, the IPOs generated gross proceeds of $6.98 billion. This was down from the $119.36 billion seen one year earlier. To see a number at or below this point, we have to tread back all the way to 1990 when the 110 IPOs that year brought in a paltry $4.27 billion.

{kind=link}

What this data establishes is that we are seeing a lack of funding across the startup spectrum. The smallest companies are seeing less capital come in, while the largest companies that could be considered startups are also seeing the same thing. And if you're seeing both the top and bottom of the startup community experiencing pain, you're likely seeing the same kind of pain for the companies in the middle. It wouldn't be surprising if the 2023 fiscal year is even worse for all parties involved. It was this exact pain that caused a firm like Silicon Valley Bank to experience the downside it ultimately saw. When funding is in short supply for companies that are losing large amounts of cash in order to operate and grow, they must resort to drawing down capital from their bank accounts.

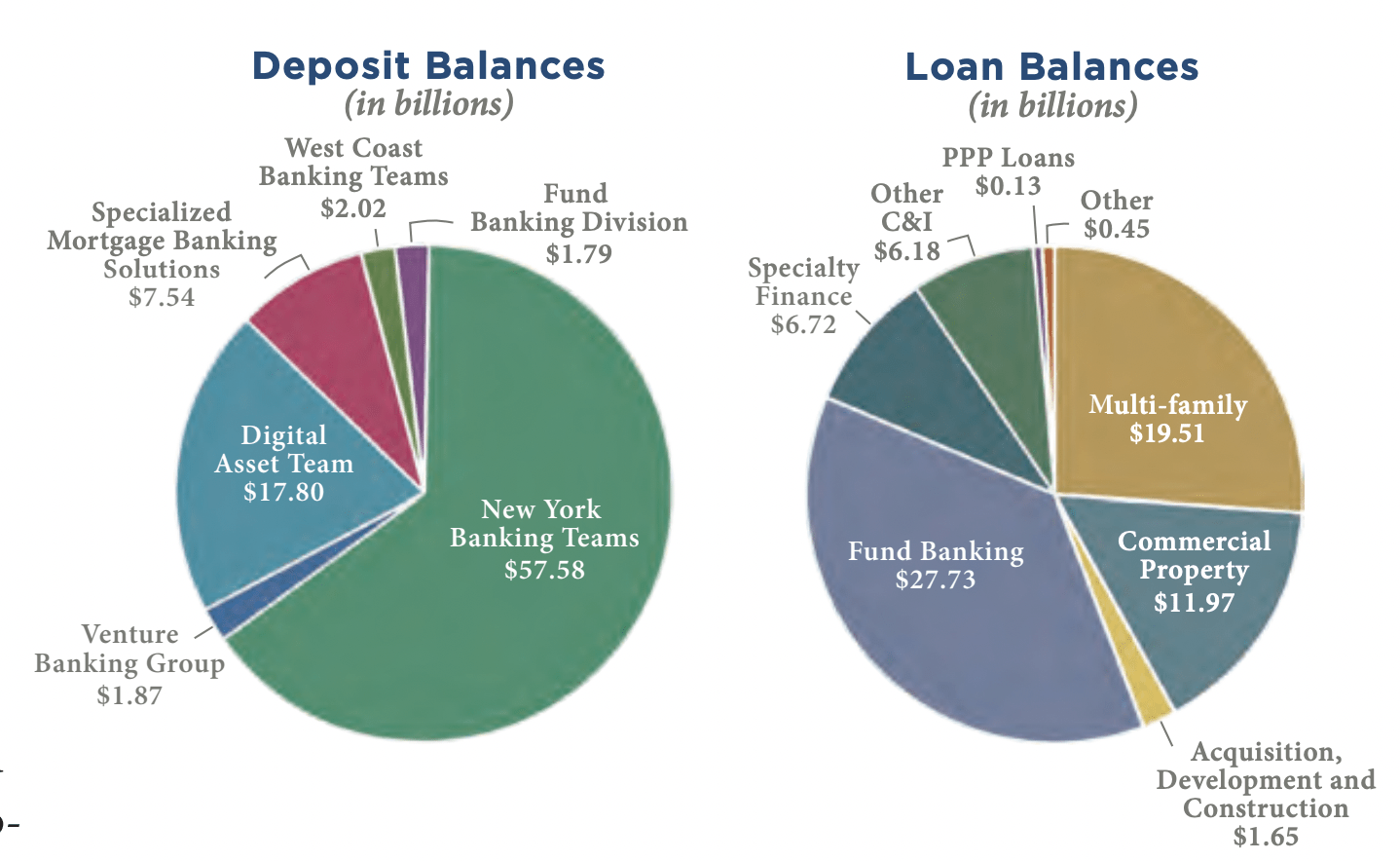

The same kind of phenomenon that affected Silicon Valley Bank undoubtedly impacted Signature Bank. For context, it would be helpful to dig a bit deeper into its own financial condition. Of the $74.3 billion in loan balances on its books, $27.7 billion is related to its fund banking division. This unit provides financing and banking services to the private equity industry. Specifically, it provides capital call lending to large funds, as well as their limited partners. In fact, since launching this operation in 2018, it has grown to become one of the five largest lenders within the private equity space. On the deposit side of things, the company has some exposure as well. Outside of the wide array of other services that may have some overlap, the firm has $1.9 billion in deposit balances under its venture banking group. This particular part of the firm caters to venture capital companies and the portfolio companies in which they invest. In addition to the aforementioned deposit amount, it also had $501 million in loans to these parties at the end of 2022.

{kind=link}

The company is also exposed to the cryptocurrency space. Although not exactly related to the problems we are dealing with when it comes to higher interest rates, it is no secret that cryptocurrency has taken a beating over the past year. As of the end of 2022, the digital asset team that the company has boasted $17.8 billion in deposits. To the company's credit, it did start reducing its exposure to not only this space but also the aforementioned spaces last year. But the exposure is significant nonetheless. And when you add in the problems associated with cryptocurrency market, such as the fact that substantially all of cryptocurrency is worthless, it shouldn't be a surprise to investors that the company faced these problems. It should also be mentioned though that, at least in the case of Signature Bank, that the company did not engage in lending on digital assets, nor did it invest in digital assets or custody any of them for any of its clients over the years. If it had, it might have faced issues far earlier than this.

First Republic Bank carries risk as well

The way I see it, the problems that we are facing right now are not all that surprising. First Republic Bank may offer investors some upside from here, but it’s also not without its risks. On March 13th, shares of the company closed down 61.8%, driven by fears about potential contagion. This came after the company announced that it had bolstered its liquidity, increasing it to roughly $70 billion. If the company were to fail, it would be monumental. After all, the company ended the 2022 fiscal year with $212.6 billion in assets, and with deposits of $176.4 billion. Total equity for the company came out to $17.4 billion, and it held assets under management and assets under advisory of $271.2 billion.

{kind=link}

I understand why the business is experiencing scrutiny. First, let's start with the bad. On the deposit side of things, management has not been as detailed as I would like. But what we do know is that 40% of all of their deposits come from the San Francisco Bay area, while another 19% come from New York. 9% comes from Boston, while 8% comes from Los Angeles. These are all major areas for the same kind of startups and early-stage businesses that would be most likely to need their capital quickly. It would be different if the vast majority of their deposits involved consumers. But actually, 63% of all deposits are from business clients.

{kind=link}

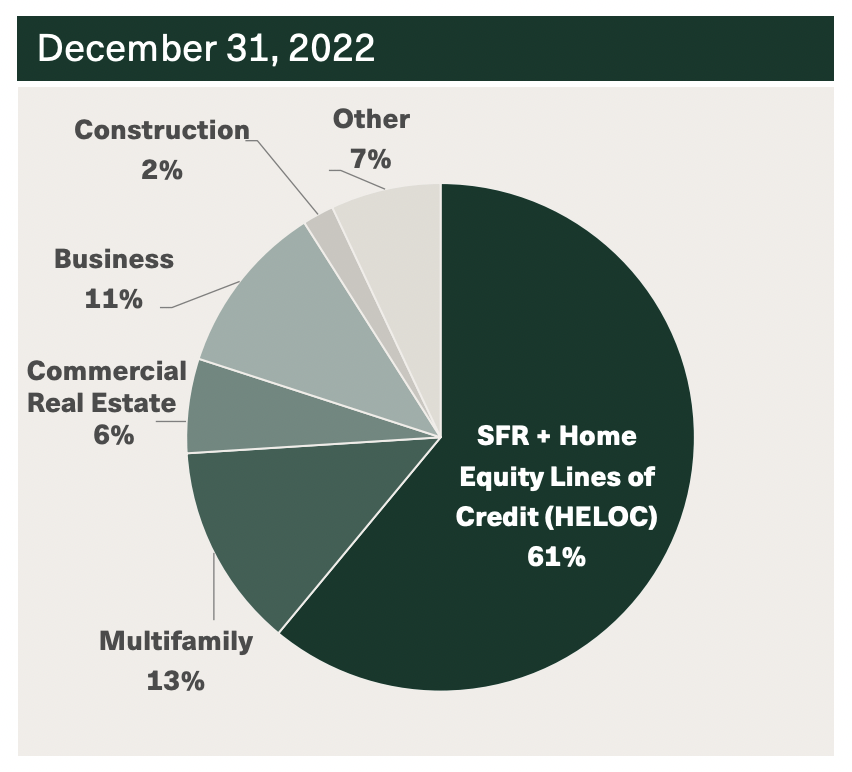

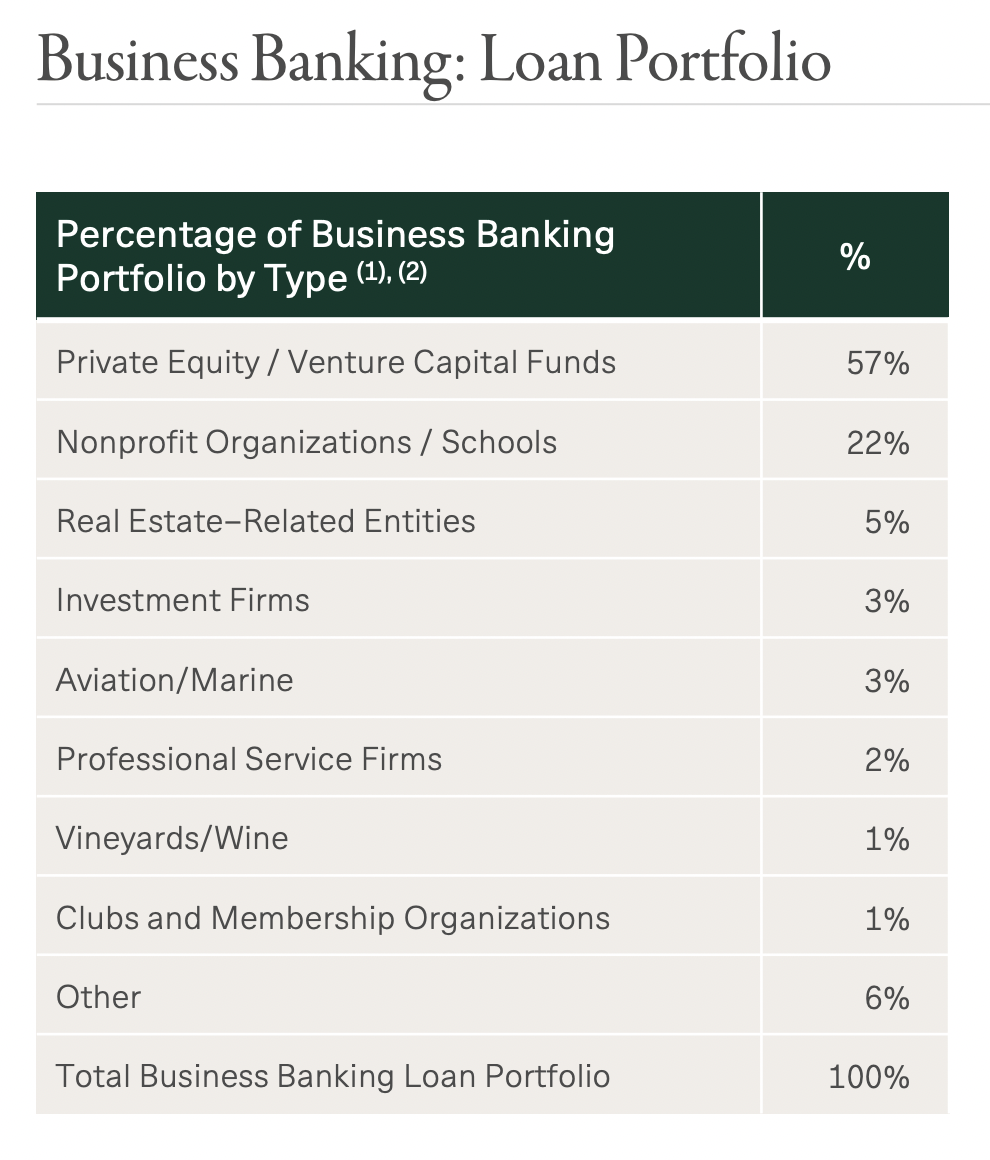

On the loan side of things, the company is much more insulated. 59% of all of its loans, totaling $98.8 billion, involve single-family residences. Another 2% is in the form of home equity lines of credit, while about 1% is attributable to single-family construction activities. Another 13% of loans involve multifamily properties, with around 1% involving multifamily and commercial construction activities. The firm also has about 6% of its loans tied up in commercial real estate. When you get to business loans, that number comes out to about $18.8 billion, or 11% of all loans outstanding. Of its total loan balances, however, almost $10.7 billion involves exposure to private equity and venture capital clients, as well as the firms they invest in. This on its own is not enough to put the company in jeopardy. But when you factor in the risk that comes from the large exposure to deposits, it could add on additional pain.

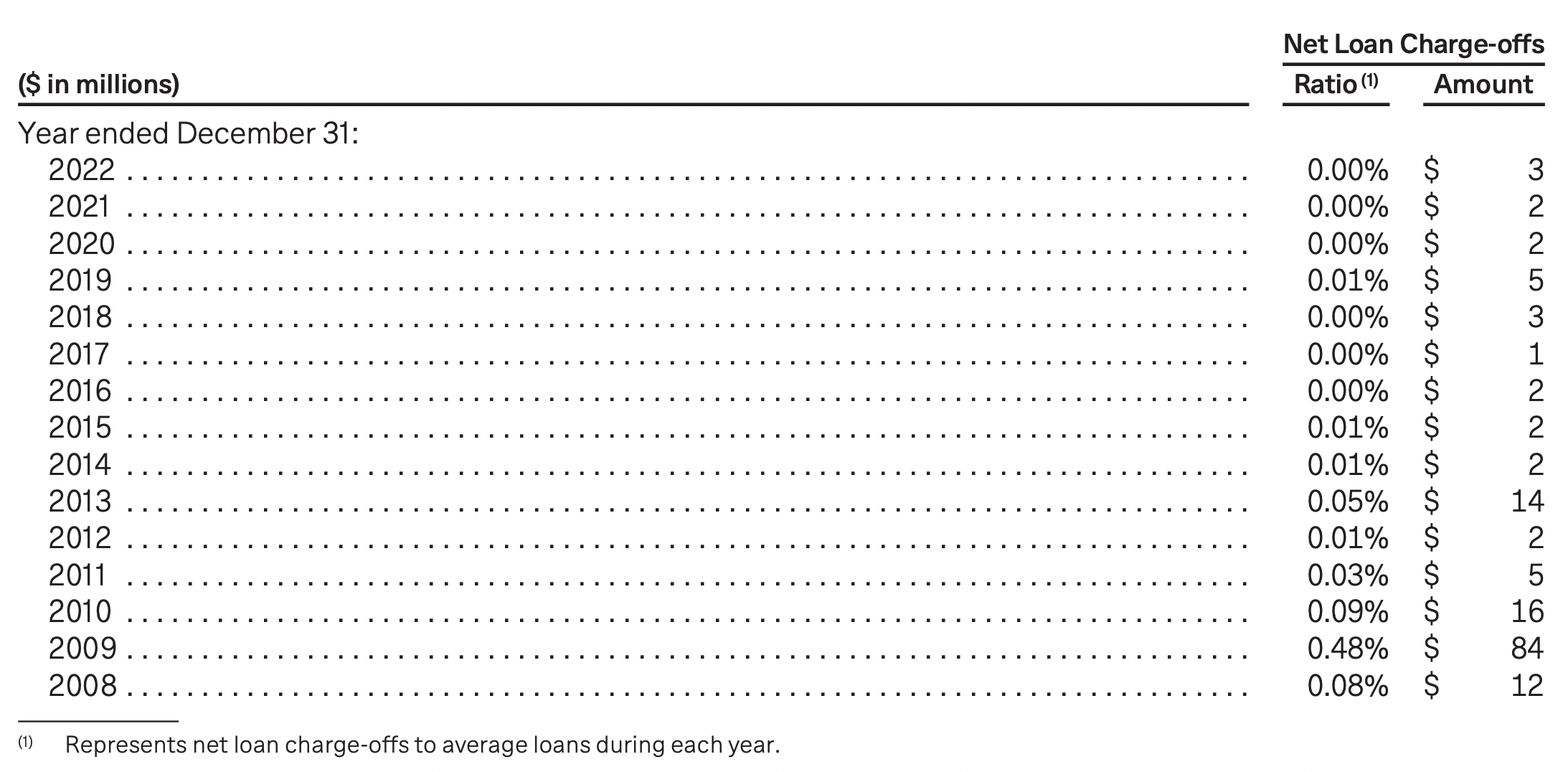

To be fair to the company, it does have a good track record on the loan side of things. Over the past several years, the company has had almost no net loan charge-offs. The worst year for the business, not surprisingly, was in 2009. That year, the company wrote off $84 million worth of loans. But that accounted for only 0.48% of the value of the loans on its books. Because of this track record and the overall loan composition, I'm not so worried about that side of the business. Rather, I am concerned about the deposit exposure.

{kind=link}

This doesn't mean that investors should stay away from First Republic Bank. The company clearly has an elevated degree of risk. If it does see a run on deposits, it could find itself in a great deal of pain. Management describes the company as being geographically diverse. But we need to look at where those deposits come from, I think that it has some systemic exposure. In the event that the firm can fend these issues off, however, it could result in a great deal of upside for investors. Consider, for instance, the firm's tangible book value. On a per-share basis, it came out to $74.19 by the end of the 2022 fiscal year. That's significantly higher than the $31.21 that shares are currently going for. What this means is that, in theory, buying up the stock and seeing an orderly liquidation where assets are sold off at book value could result in more than a doubling of money for investors. The overall book value per share is a bit higher at $75.38. This translates to a price to book value ratio of 0.41. For context, as of March 10th of this year, the average for a bank was 0.89.

Takeaway

Fundamentally speaking, the picture we are facing is fascinating. But it's also very painful. Investors would be wise to tread cautiously at this point. Having said that, there could be some opportunities. Although I personally am not planning to invest in First Republic Bank at this time, unless I take a gamble with some long-dated call options, I can understand why some risk-loving investors or speculators would be drawn to the firm. For sure, the situation the company is dealing with is not yet as bad as what we have seen with other players in the space. But it could get there depending on what happens in the coming days and weeks.

For further details see:

First Republic Bank: Systemic Exposure Risks Exist