FRC - First Republic Bank: This Is Not SVB And I'm Buying

2023-03-14 11:05:55 ET

Summary

- First Republic Bank fell ~60% on March 13 on fears that it could be the second bank to experience a run after SVB's fall.

- FRC's asset base is much more heavily weighted toward long-term loans, which makes it less susceptible to losses compared to SVB.

- SVB, on the other hand, had invested a good chunk of its deposits into shorter-term securities which declined in value as the Fed hiked interest rates.

- Trading at a single-digit P/E against last year's earnings, this is a great stock to buy while the rest of the market is fearful.

It's been all over the headlines: First Republic Bank ( FRC ) has been pinpointed as the next domino to fall in the wake of Silicon Valley Bank's (SIVB). It's not difficult to understand why the masses may think that to be the case: both are Silicon Valley-concentrated banks, and both have an unusually high exposure to both high net-worth clients and tech/VC firms. And in this highly interconnected modern world, fueled by social media, rumors of bank runs unfortunately lead to the very thing itself. These days, bank "runs" are more like bank sprints.

First Republic fell more than 60% on March 13, tallying YTD losses to more than 70% (the chart below shows one-day trading action in First Republic; the stock briefly sunk below $25 before rallying to close at $36). Versus mid-2022 highs above $170, the stock has shed more than 80%. Needless to say, general confidence in this name is very low: but is that warranted?

I'll cut to the chase here: I'm buying First Republic in the wake of its fallout.

We'll get the headlines out of the way first before digging into deeper analysis, and these already should inspire some confidence. First, yesterday alone federal regulators announced that SVB depositors will be made whole regardless of deposit insurance limits . While the U.S. is still moving to auction off SVB as a going concern and is not backstopping to rescue the company, this move should assuage depositors in other banks like First Republic that their assets are in good hands even in the chance of another run.

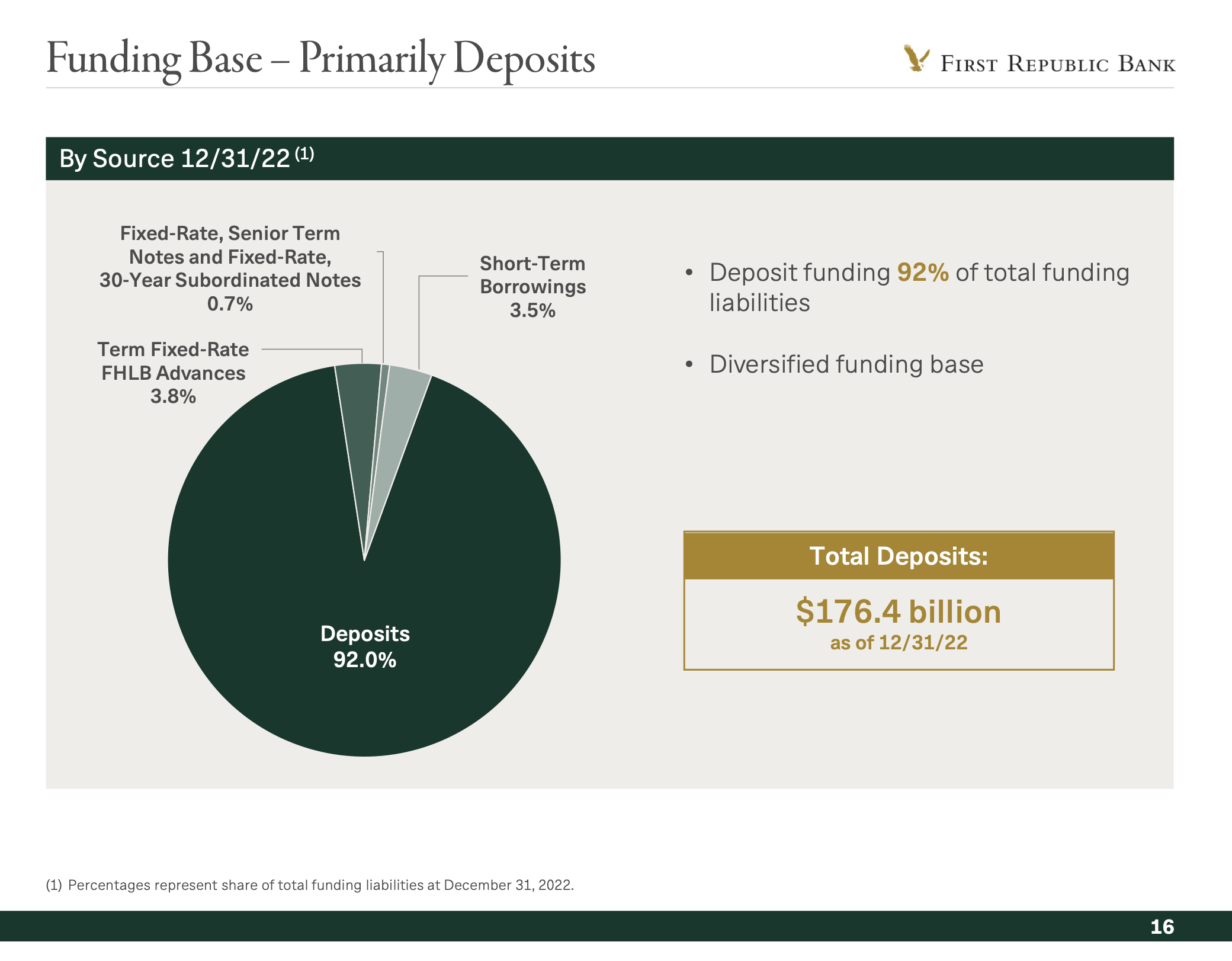

Secondly, First Republic got a huge lifeline from J.P. Morgan and the Federal Reserve, amounting to $70 billion in fresh liquidity. Note that First Republic is a very small bank whose overall balance sheet only amounts to ~$200 billion. The deposits total, meanwhile, stands at ~$176 billion as of the end of 2022.

First Republic deposits (First Republic Jan 2023 investor presentation)

{kind=link}

In simple terms, roughly 40% of First Republic's depositors could pull out - and this emergency funding lifeline would cover the shortfall.

Silicon Valley Bank had the unfortunate position of being first and unprepared in this unprecedentedly volatile environment; with the benefit of foresight, First Republic had time to shore up its capital position.

First Republic's asset mix is more favorable than SVB's

Okay, so we've hopefully gained some more confidence on the deposits/liabilities side of the balance sheet equation, both with additional emergency funding plus the lower chance of a second bank run with the U.S. government's promise to make depositors whole.

What we'll discuss next is the difference in the two banks' asset bases. What triggered fear in Silicon Valley Bank in the first place is the fact that SVB was heavily exposed to shorter-term securities that have dropped severely in value since the Fed started raising rates at a rapid pace.

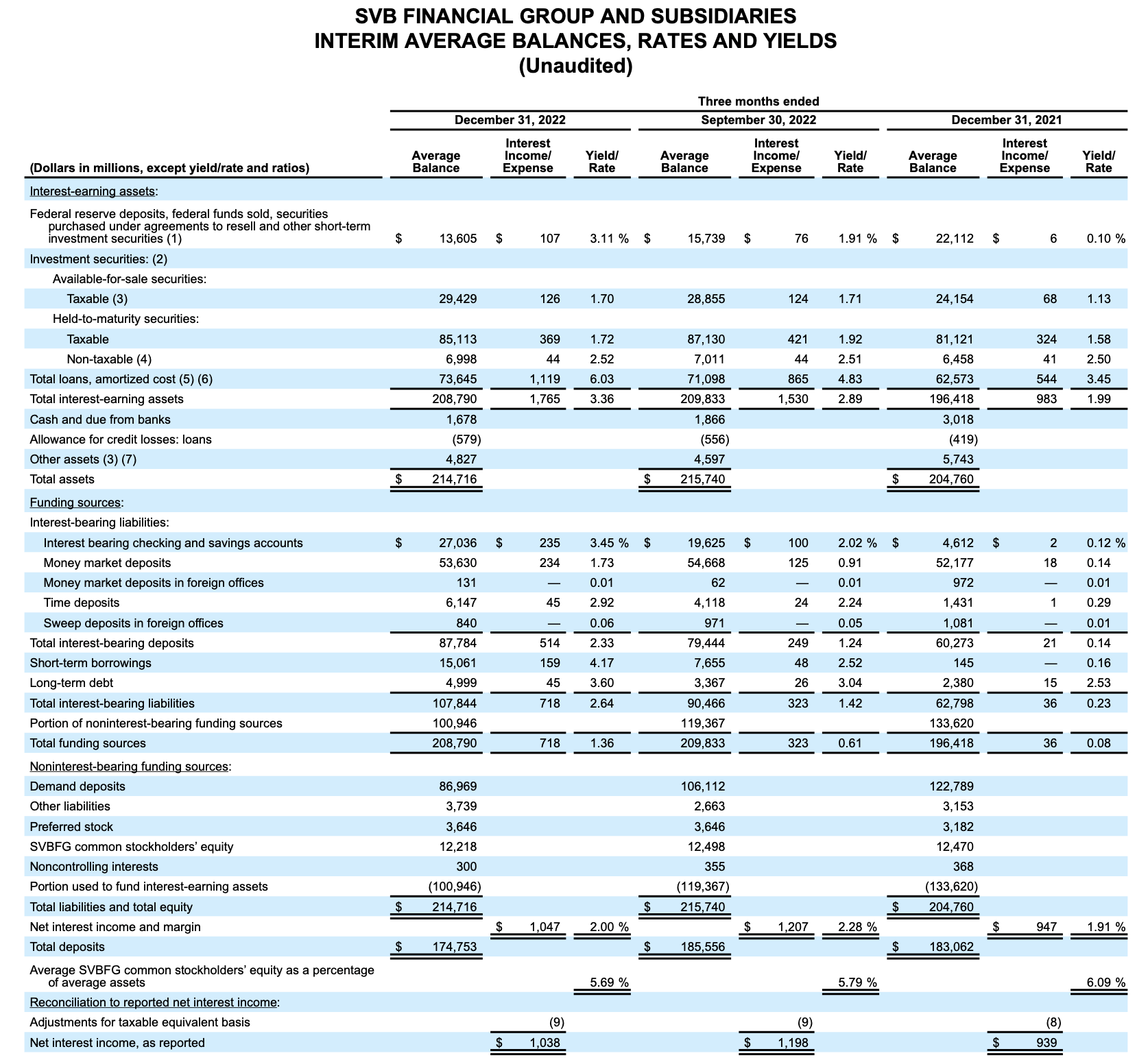

Here is a look at SVB's 2022/December-end balance sheet:

SVB December 2022 balance sheet (SVB Q4 earnings release)

{kind=link}

Of the company's $209 billion in interest-earning assets, $128.1 billion (or roughly 65%) of the company's assets were held in securities. Loans of $73.5 billion represented a much smaller percentage of the total (note as well that loans carried a much higher yield of 6.03%, though that is a reflection of SVB's riskier portfolio that caters toward more speculative innovation-economy credits and VC lending). The storyline here is simple: awash in post-pandemic deposits from startups that had raised fresh VC funding in the tech boom of the past few years, SVB was taking in deposits faster than it could lend the money out, so it turned to bonds and bills as a supposedly risk-free way to earn yield on those deposits (on which it paid an average of 2.33% in the fourth quarter).

Unfortunately of course, bond investors' biggest fears played out this year with the Fed's rate hikes. Securities aren't marked to market on the balance sheet, but the -8% trailing twelve-month performance of AGG, the iShares U.S. Aggregate Bond Index ETF and one of the most popular bond ETFs in the market, illustrates what a big hole SVB was facing if the majority of its assets were similarly devalued.

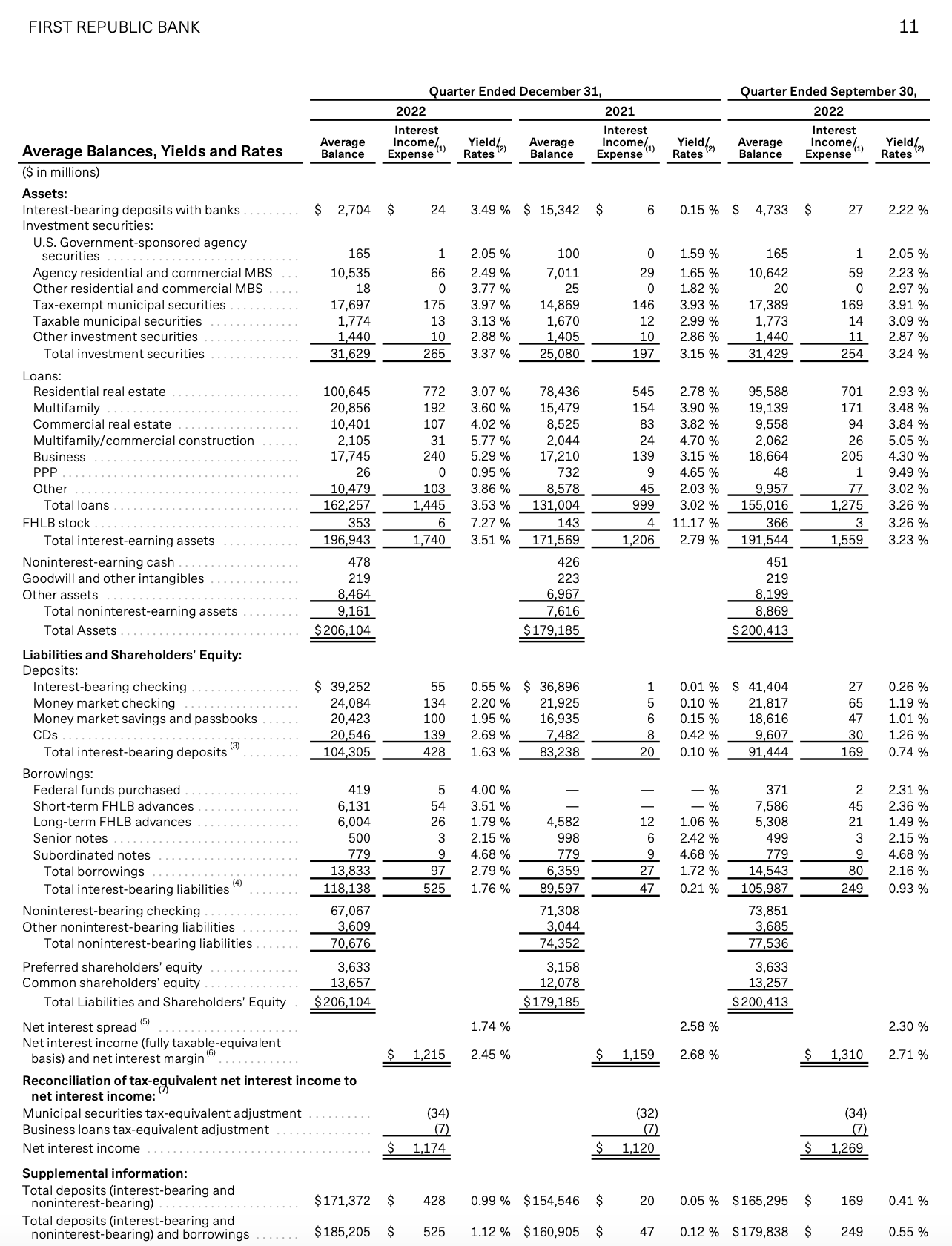

First Republic, on the other hand, is in a different position. Take a look at its balance sheet below:

First Republic Bank December 2022 balance sheet (First Republic Q4 earnings release)

{kind=link}

First Republic's balance sheet size is very similar to Silicon Valley Bank, with $196.9 billion in interest-earning assets. The mix, however, is starkly different: investment securities of $31.6 billion represents 16% of First Republic's total, while loans of $162.3 billion represents 82% and the lion's share of First Republic's asset base. I'll emphasize again here: First Republic has more than 2x the loan volume of SVB, and less than a quarter of its loan exposure. This means that First Republic is more heavily weighted toward longer-duration assets that aren't as sharply exposed to short-term interest rate risk and devaluations.

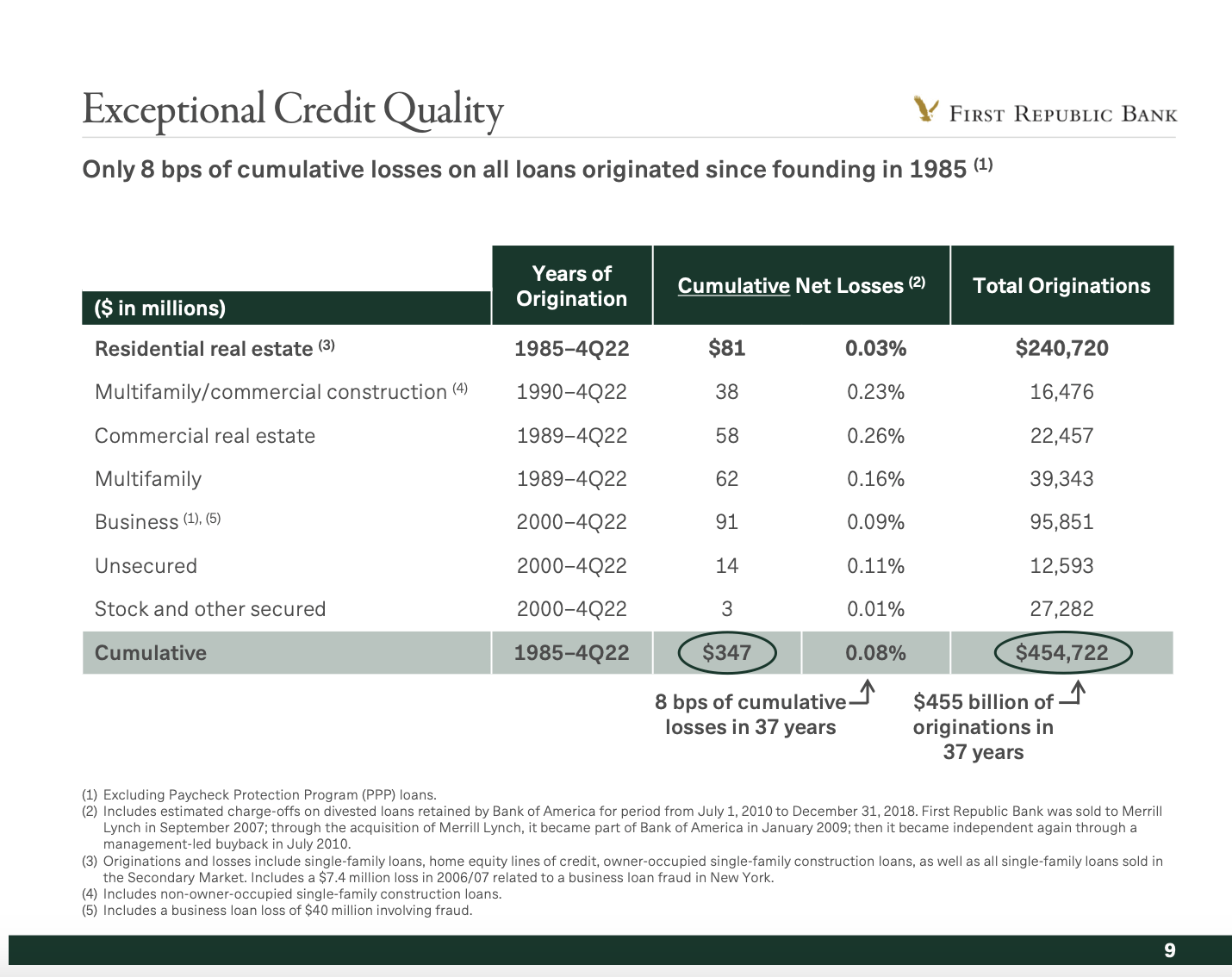

Now, since First Republic's focus here is loans, we would be remiss not to discuss credit quality. Fortunately, First Republic has had an excellent track record on this front. Of $455 billion in cumulative loan originations since its founding, it has only experienced 8bps of net losses and charge-offs as shown in the chart below:

First Republic credit quality (First Republic Jan 2022 investor presentation)

{kind=link}

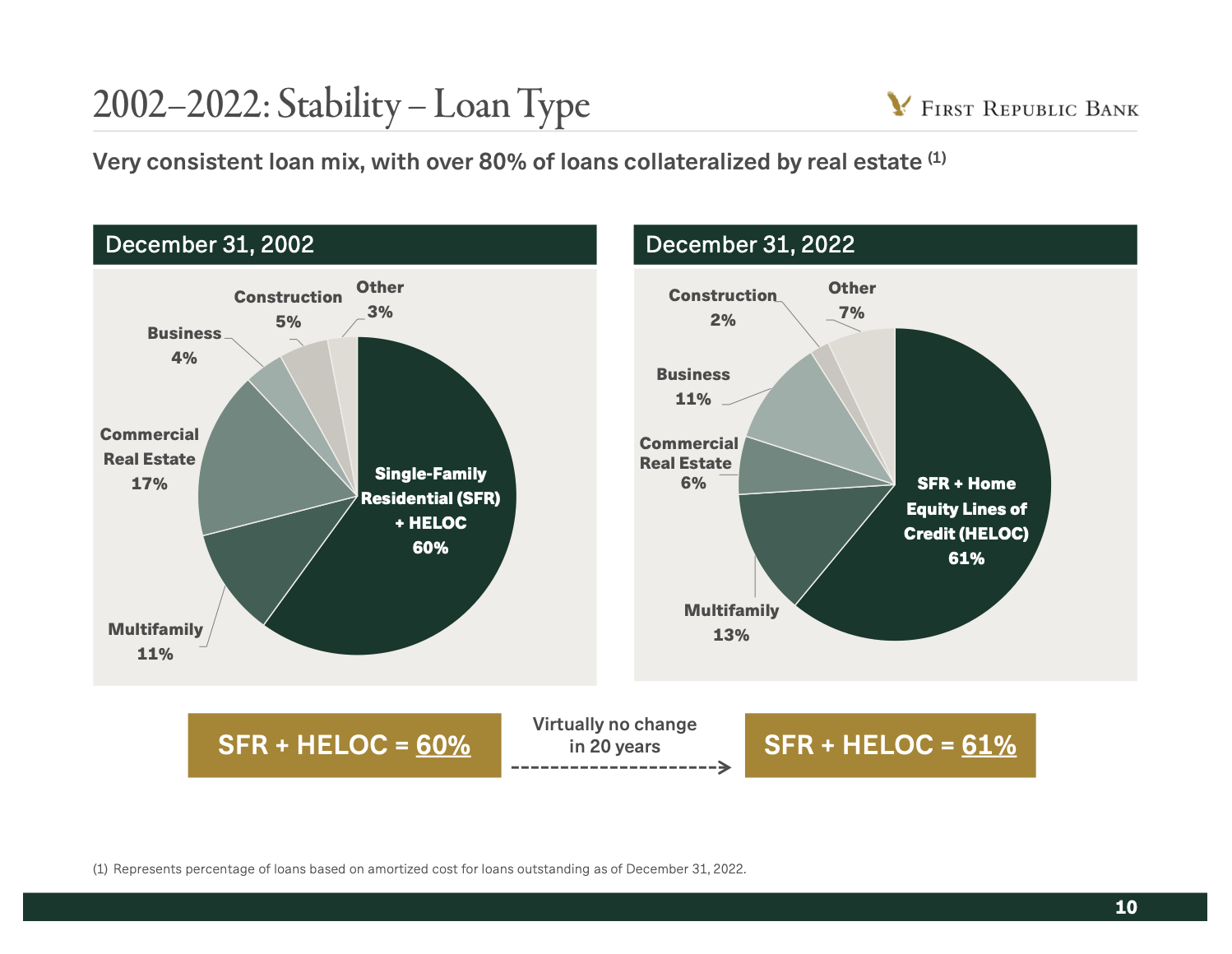

The majority of First Republic's loan portfolio, meanwhile, is in real estate and construction loans, while "business and other" loans represent 18% of the loan portfolio in total:

First Republic loan mix (First Republic Jan 2022 investor presentation)

{kind=link}

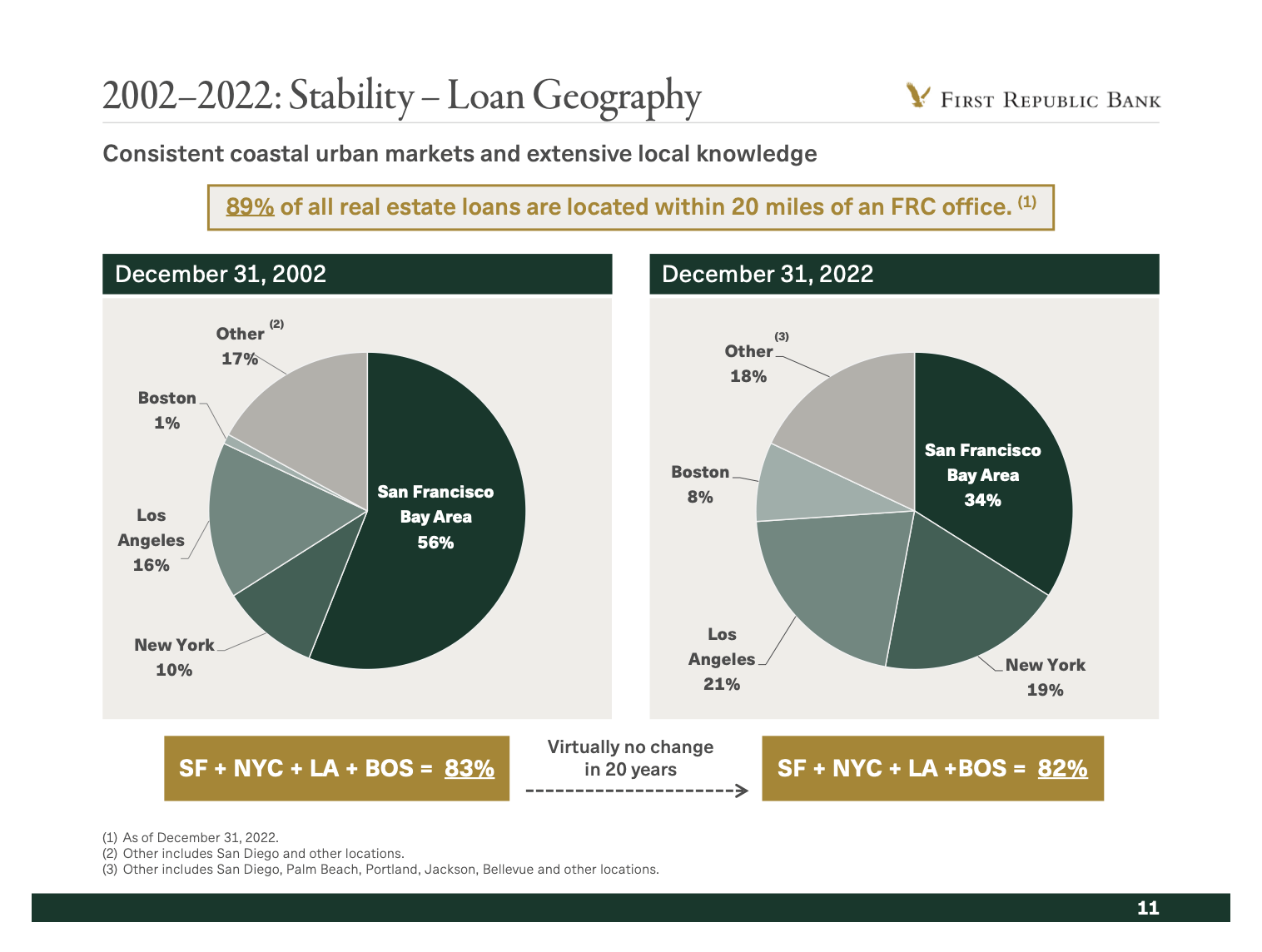

A side note here on real estate loans: we like the fact that First Republic has diversified its geographic exposure in its real estate book away from its San Francisco Bay Area home market over the past twenty years, which helps to insulate against credit losses in case a tech-centered recession does take place in Silicon Valley.

First Republic real estate diversification (First Republic Jan 2022 investor presentation)

{kind=link}

Now, First Republic's loan concentration (which we are indicating is a positive vis-a-vis Silicon Valley Bank) to real estate would be a huge red flag if we were facing a 2008-style real estate recession. But while the housing market is certainly in a cooldown phase, it's hardly the same signals as in 2008. Home prices are staying aloft; sellers are staying on the sidelines because they don't want to let go of lower interest rates, and supply remains low. The only risk on the horizon is the recent spate of layoffs leading to loan foreclosures, but so far we haven't seen this en masse.

So overall, First Republic's balance sheet has much more benign exposure to mark-to-market losses as SVB. The only risk here is actual earnings potential/net interest income. You'll note that First Republic's Q4 loan yield of ~3.5% is much less than SVB's ~6% (again, thanks to First Republic's penchant for relatively lower-risk real estate loans as opposed to speculative tech lending). Though presumably a portion of First Republic's portfolio (HELOCs, multifamily and commercial real estate loans) have a floating-rate structure that will benefit alongside the higher interest rate environment, the company's residential portfolio is likely more skewed toward traditional fixed mortgages. The net here: First Republic's deposit costs will likely increase as it has to match more attractive interest rates that both banks and brokerages are offering, but its net yield on its loan books may not rise as quickly.

Key takeaways

Due to the risk pointed out above, it's fair that First Republic's valuation got cut. Consensus is currently calling for both EPS and revenue to contract this year. However, the fact that First Republic lost tens of billions of market valuation in a single day on the assumption that it will follow in SVB's footsteps - when its underlying balance sheet looks so different than SVB's - is a fantastic opportunity to buy.

For further details see:

First Republic Bank: This Is Not SVB, And I'm Buying