FRC - First Republic Bank: Why Failure Is Not An Option

2023-04-03 13:33:17 ET

Summary

- Given how the US big banks and the Federal reserve had supported FRC during the recent banking crisis, we reckon the latter's prospects remain safe in the short term.

- However, investors also need to calibrate their expectations, since we expect to see reduced deposits due to the deposit outflows to big banks and money market funds alike.

- As a result, FRC may be unfortunately downsized, due to the reduced deposits, higher cost of funding, and lower assets ahead.

The Last Line Of Defense

It seems like First Republic Bank ( FRC ) has become the classic example of when failure is not an option, since it represents the all-important health of mid-sized US banks. In our opinion, the longer FRC survives the banking crisis, the better the optics appear, significantly supported by the massive injection of cash from the big US banks and the Federal Reserve thus far.

In the meantime, we will be discussing the health of the bank, which has naturally triggered the pessimism surrounding its stability and forward execution.

In FY2022, FRC reported $471M (+805.7% YoY) of gross unrealized losses in $3.81B (+11.4% YoY) of available-for-sale [AFS] securities, with a ratio of 12.3% (+10.8 points YoY). At the same time, the bank recorded $4.83B (+9030.1% YoY) of gross unrealized losses in $28.35B (+27.1% YoY) of held-to-maturity [HTM] debt securities, at a ratio of 17% (+16.2 points YoY).

Due to the massive expansion in the unrealized losses, it was no wonder that the stock had fallen as it did by early March 2023, significantly worsened by the unfavorable US Treasury yield curve.

While it makes no sense to refer to FY2022's outdated numbers, FRC reported $119.5B (+2.3% YoY) of uninsured deposits in the latest fiscal year, comprising 67.7% of its total deposits of $176.4B (+12.8% YoY). Given that checking and savings accounts also comprised $151.22B (+1.5% YoY) of the bank's total deposits, it was unsurprising that Mr. Market was extremely concerned about a bank run then. This was significantly worsened by the market rumors, which implied $70B in deposit outflow s by mid-March 2023.

However, here is where we are cautiously optimistic about a reversal in the intermediate term. The bank's HTM portfolio boasts a relatively long weighted average duration of 10.8 (+1.8% YoY) years, suggesting that it may not realize these losses after all, due to the Fed's target inflation rate of 2% over the next few years.

In addition, the Federal Reserve's recent Bank Term Funding Program [BTFP] ensures that any banks, including FRC, may be able to meet their liquidity needs in the short term, further reducing the chances of realizing losses. As of March 15, 2023, the bank also reported that it had a cash position of $64B . This was on top of the borrowings from the Federal Reserve for $109B at a rate of 4.75% and the Federal Home Loan Bank [FHLB] for $10B at a rate of 5.09%.

However, that does not mean that risks have completely disappeared, due to FRC's elevated costs of funding from these recent borrowings, compared to its FY2022 levels of 0.51% and FY2021 levels of 0.18%. Then again, the risks were probably shared by many banks as well, since JPMorgan ( JPM ) analysts reported that FHLB borrowings rose drastically to $241B for small banks and $230B for large banks by March 24, 2023.

While the elevated interest rate environment contributed to the increase in the bank's interest expenses to $888M (+227.6% YoY) and the provision in credit losses to $107M (+81.3% YoY) in FY2022, we were not concerned at all. This was because the net effect had been positive, with its net interest income rising to $4.72B (+16.5% YoY) at the same time.

However, approximately $108B in deposits had flowed from smaller banks to bigger banks, with $273.3B flowing to money market funds, due to the pessimistic sentiments surrounding mid-size banks. The combination of reduced deposits and increased funding costs suggests FRC's reduced profitability, in our view.

Therefore, due to the bank's supposed downsizing, we reckon that the moderation in FRC's stock price is warranted, especially since it is reportedly considering the sale of part of its businesses to raise cash and cut costs, and also considering the recent suspension of its dividends.

In addition, FRC may face more headwinds ahead, from the potentially tightened banking regulations . The regulators are now deliberating a proposal where banks may be required to hold more capital on their balance sheet, while similarly improving their stress test models.

While the proposal is designed to ensure self-contained bank failures, we reckon the bank's long-term prospects may be impacted due to the stricter cash and asset requirements.

So, Is FRC Stock A Buy , Sell, or Hold?

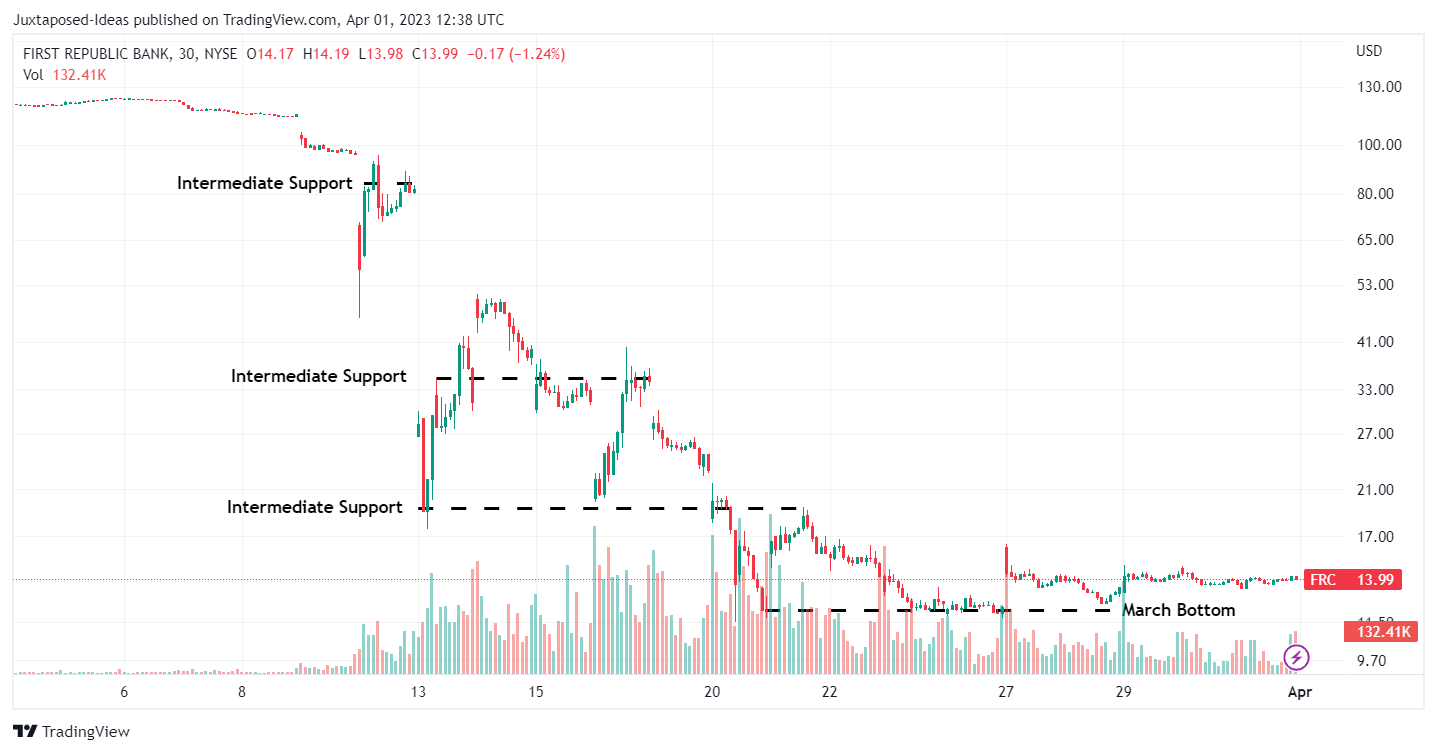

FRC 1Y Stock Price

{kind=link}

At the time of writing, the FRC stock has already bounced from its March 2023 bottom of $12.18 to $13.99, suggesting an excellent support level, despite the drastic -88.35% plunge from pre-banking crisis levels. Assuming sustained support ahead, the stock may also slowly recover over the next few months, testing its intermediate support levels in the $20s.

Nonetheless, we prefer to prudently rate the FRC stock as a Hold here, despite the risks that may already be baked into its stock prices. This is due to the uncertain macroeconomic outlook, based on the Fed's projected terminal rate of 5.25% and a pivot probably only from 2024 onwards.

While it is hard to place a price target on FRC, market analysts have already drastically cut the bank's FY2023 EPS projections to $0.37 and FY2024 EPS to $2.17, compared to FY2022 levels of $8.25. Therefore, we reckon that it is unlikely that the stock may recover to its pre-banking crisis levels of $120s in the intermediate term, due to the impacted profitability.

In addition, FRC will need to find a way to return the $30B deposits to the US big banks and borrowings to the Federal Reserve/ FHLB, since those come with a strict deposit/ lending timeline of 120 days and 60 days, respectively, barring an extension. As such, the bank's prospects remain highly uncertain for the foreseeable future, in our view.

For further details see:

First Republic Bank: Why Failure Is Not An Option