UBS - First Republic: Dimon's Rescue Is Bad News For Commons

2023-03-22 11:20:37 ET

Summary

- We examine 3 pieces of new info to assess First Republic Bank's current situation.

- Explain why the rumored Dimon & Co's rescue plan, if true, is bad news to First Republic Bank's common shareholders.

- Connecting all the dots, I conclude it is best to avoid First Republic Bank common shares.

Background

In my last analysis of the First Republic Bank ( FRC ) 8k filing on March 16, 2023, I examined First Republic's balance sheet , its newly injected liquidity, and some napkin math to highlight my concern that, despite these supports, the Bank's insolvency is still a real possibility.

3 pieces of New Info

Since then, while First Republic Bank hasn't filed any additional SEC filings, 3 pieces of intriguing information have surfaced. They are:

- JPMorgan Chase (JPM) CEO Jamie Dimon led the efforts to stabilize the Bank ( article from Seeking Alpha)

- $70B deposit withdrawal ( reported by WSJ, not confirmed by the Bank)

- First Republic Bank weights options to sell parts of its business ( article from SA).

In today's article, I will examine the above 3 pieces of information, explain whether and how they are related, uncover what wasn't said, and conclude my concerns.

Dimon to the Rescue

Let's start with Dimon's efforts to stabilize FRC.

Jamie Dimon leads effort to Stabilize First Republic Bank (Seeking Alpha)

The first question many folks might have is, JPMorgan (with other major banks) just injected $30Bn deposit, so why are additional efforts required to inject capital to stabilize the bank?

To answer that, let me take a step back, and provide some background.

In this crisis, First Republic fights multiple battles.

Liquidity Battle : this is rather straightforward as deposit withdrawal takes place, the bank needs cash to support that.

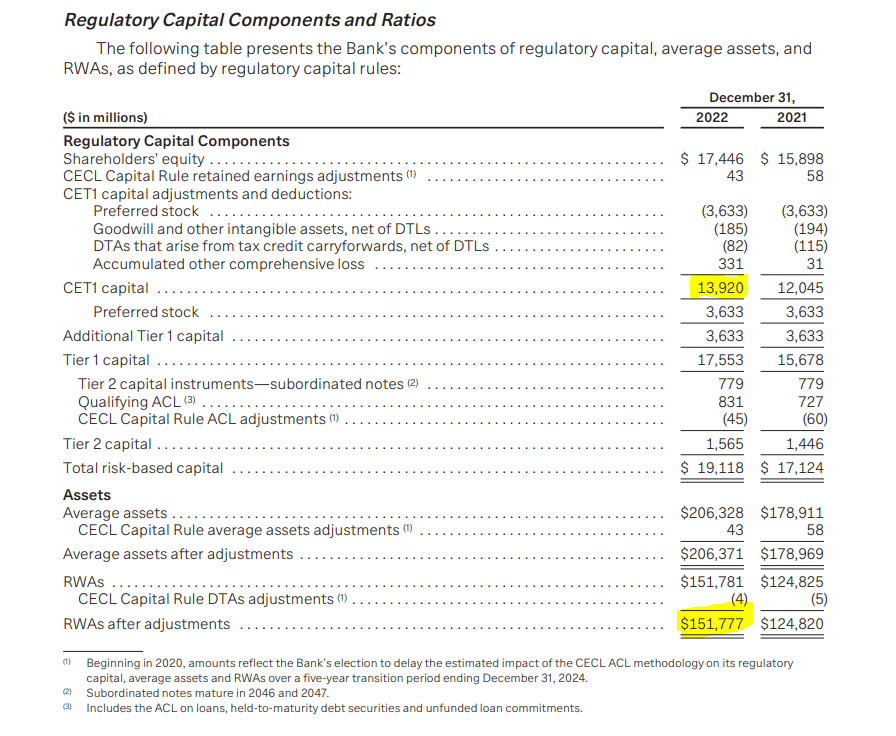

Regulatory Capital Battle : A bank is required to conform to a set of regulatory requirements (CET1 ratio being the most well-known one) set by Fed Reserve.

These ratio is designed to measure a bank's ability to withstand and defend financial distress. If these ratios are being breached, capital raise is mandatory to raise the ratio to at least the minimum requirement

The Liquidity battle

On March 19, a WSJ article said, "customers have pulled some $70 Billion in deposits, almost 40% of its total, according to people familiar with the matter."

$70 Bn is lower than my estimated $90Bn number, but within $65B to $95B range in my model (see below from my last article). The bank itself didn't confirm the rumored $70 Bn, but it is within a reasonable range to me.

A Thesis-Changing Filing To First Republic Bank's Bulls (author)

Assuming the $70Bn withdrawal figure is correct and the deposit base has been stable since, we know FRC received $10Bn From FHLB, up to $109Bn from Fed, and $30Bn from major banks. It should have sufficient liquidity to withstand the $70Bn withdrawal and keep the operation going.

So why does it need to weigh options to sell parts of its business to raise cash? There are a few possible explanations.

FRC's borrowing via Fed Discount Window is a short-term arrangement. It is expected to be paid back within 60 days, unless a Liability exception is granted to extend the borrowing. The Fed probably signaled not to expect prolonged extensions, if there would be any.

One might recall the March 12 headline that "First Republic gets $70B liquidity support from Fed and JPMorgan?"

I mentioned in the last article, it was puzzling to me that FRC didn't include this $70Bn liquidity in its March 16 filing, which was designed to ease customers'/investors' concerns. My guess is that $70B liquidity support might likely have contingency clauses, and might not be available anymore.

With the above two, First Republic Bank faces at least a $30Bn liquidity shortfall ($70B-10B-30B), thus explaining why it is weighting the option to sell part of its business to raise liquidity.

Let us examine its asset book to figure out how it is going to raise the cash.

A Thesis-Changing Filing To First Republic Bank's Bulls (author)

Here is the dilemma First Republic's management faces:

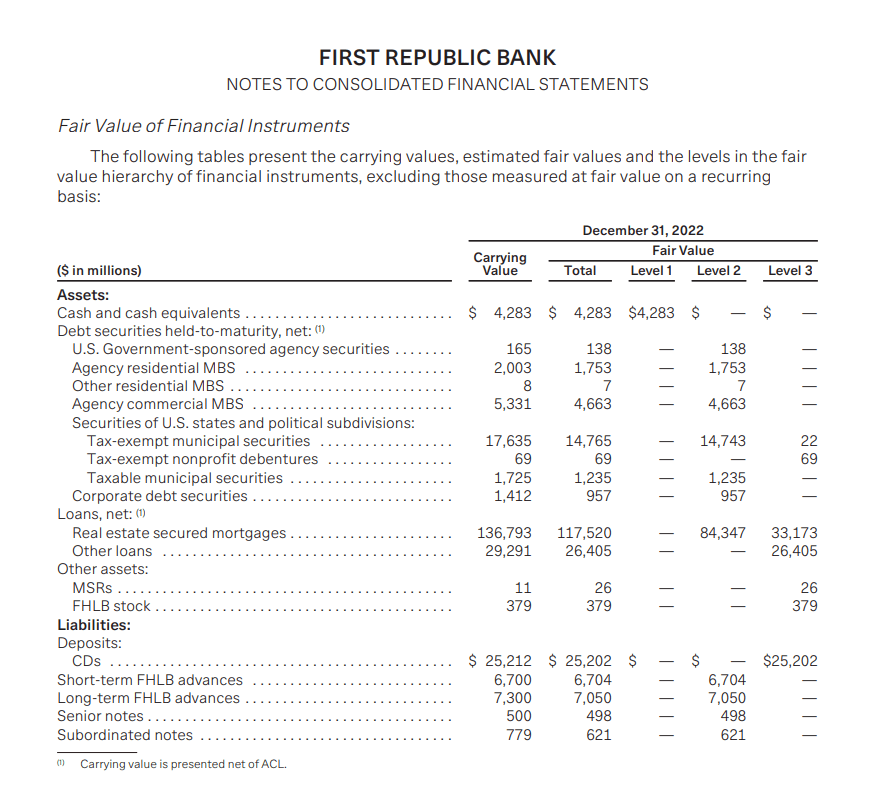

Selling any portion of the HTM portfolio would trigger a portfolio revaluation and realize its $4.8Bn unrealized loss. That would deplete its regulatory capital, and its regulatory ratio (e.g., CET1) would take a big hit.

Selling Adjustable Rate Loan won't have unrealized loss (caused by duration), however, unlike mortgage-based securities ((MBS)), these are real loans. The Bank needs to find appropriate counterparties discretely so the loans could be sold at or close to their fair value, without causing market panic.

It certainly wouldn't want to sell Fixed rate loan, as these unrealized losses would be far more significant (20%+).

If I model a 10% discount to fair value to unload its adjustable rate loan, together with AFS ($3.3Bn), it would raise $30Bn cash, tightly fit the $30Bn liquidity gap after $70Bn deposit withdrawal.

Regulatory Capital Battle

Its current CET1 ratio is 9.2% (CET1 ratio requirement is 7%).

A napkin math to assess its CET1 ratio sensitivity to asset sale is:

If the sale price to carrying value discount is at or near its current CET1 ratio, then selling loan assets by and large won't have material impact to its CET1 ratio.*

For example, in this case, if FRC sells $20Bn loan at a 10% discount, it will roughly bring its CET1 ratio down by 20bps, from 9.2% to 8.95%.

* there are certainly more nuances to it, e.g., RWA calculation. The formula above offers a simple and directional correct estimate.

{kind=link}

Thus, at a first glance, selling $30Bn adjustable rate loan won't breach its CET1 ratio, thus no immediate capital raise needed to improve CET1 ratio.

Why Dimon to the Rescue?

There are a few possible explanations.

- Unloading assets hit a larger discount than I model above

- The withdrawal is projected to be more than $70Bn as reported last Friday (keep in mind, the bank didn't confirm that number).

If the news is true (that Dimon leads the effort to raise capital for FRC), it hints one or both above are true.

Another possible explanation is the Bank expects operating loss going forward (at least for a period of time), which deplete regulatory capital. I will get back to that in a late section.

Why Bad News to Common shareholders?

If recent UBS Group AG ( UBS ) acquisition of Credit Suisse Group AG ( CS ) tells us anything - it is in a banking crisis, the target would not be valued based on its reported Tangible Book Value, it would be valued under a distressed liquidation scenario.

FRC has $13.5B Tangible Book value (reported in its Y22 10k filing), If we take into consideration its $4.8B unrealized loss in its HTM portfolio, and $22Bn fair value to carrying value gap for its loan portfolio, it is Tangible Book Value under liquidation scenario is roughly negative ~$13B.

FRC has roughly $200Bn assets in its book. Even to a big bank (e.g., JPM, Citigroup), we are talking about taking on 5-10% additional assets to the book, with a negative $10Bn+ TBV baggage (under liquidation scenario). it is difficult for any of these major banks to make a case to acquire it at any cost near its market cap in today's environment.

{kind=link}

If we take a look at UBS and CS case, FINMA took extraordinary and controversial measure to completely wipe out AT1 bondholder interests and offer additional backstop loss guarantees to facilitate this $3B acquisition deal, despite the fact Credit Suisse has a near $30Bn Tangible Book Value.

Could U.S. banks borrow a page from the Swiss to facilitate a sweet deal for FRC shareholders? First, there are only $3.3Bn preferred stocks in the creditor stack other than commons, not to mention there is no legal base whatsoever (unlike CS AT1 bonds situation) to preserve common equity while wiping out preferred ones.

In summary, I have a difficult time visualizing a scenario that an acquisition offer could benefit FRC common shareholders at this point.

New Economics

Now let us examine what FRC's profit and losses would look like going forward.

We assume First Republic stabilizes its deposit withdrawal since last rumored number ($70Bn), and successfully unloads portion of its loan book, and successfully raise capital. (very optimistic assumptions)

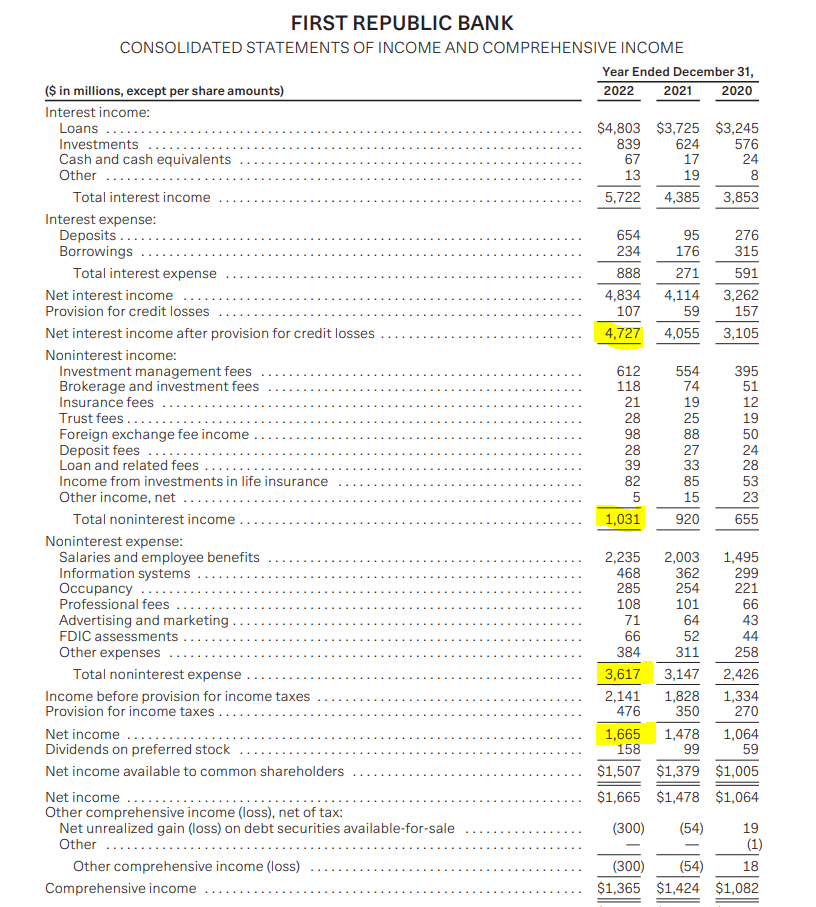

Its Net Interest Margin (4Q22) was ~2.65%, $70Bn withdrawal is about 40% deposit, as it is replenished by fed/banks injection, I estimate its interest expense increase from 0.4% to ~5%. So its net interest income going forward will reduce by ~$3.1Bn annually.

If we assume other revenue and cost structures unchanged, its net loss will be about $1Bn a year (net loss $250Mn a quarter).

{kind=link}

Can it cut costs by reducing staffing?

Sure, but that raises the question of whether it can keep its high-touch clientele, which is essential to its existence.

Connect the Dots

Over the next 60 days (or slightly longer if viability exception is granted by Fed), First Republic Bank is obliged to fill at least $30Bn liquidity gap.

It tries to sell a part of its asset book to raise cash to fill the gap. It appears as a part of unloading, its regulatory capital requirements might be breached which requires additional capital raise.

Raising capital through secondary offer in the public market is an unlikely scenario at this point. Thus it makes sense that Dimon & co. are behind the scene works on a capital raise rescue plan, as the last resort.

Under these circumstance, if we learn anything from UBS and CS deal, FRC would be valued as a -$10Bn+ baggage despite its 13Bn last reported Tangible book value. in my opinion, a common shareholder wipeout is the most logical result.

If First Republic Bank could endure the crisis by selling a part of its assets without a capital raise, its projected future P&L would take a significant hit, to an estimated $1Bn loss a year in the immediate future.

Conclusion

The stakes are high, the risk is real, and one should stay away from First Republic Bank common shares.

For further details see:

First Republic: Dimon's Rescue Is Bad News For Commons