FRC - First Republic: I See Almost No Viable Path To Equity Survivorship

2023-04-25 15:44:22 ET

Summary

- I compared First Republic's 1Q23 earnings results to my past assessment.

- I project my forward-looking perspective onto its dire 2Q23 situation.

- I explore various paths to its equity survivorship.

Background

I analyzed First Republic ( FRC ) situation quite intensively here and here during its rapid development in March 2023. I reviewed various press releases, analyzed management's commentary, and more importantly what the management didn't say, and tried to assess its situation and predict its future.

With yesterday's earnings release, I will compare my past assessment to its current state (according to 1Q23 ER), and then develop a forward-looking view into its next quarter(s).

A Quick Review

Let us review a few of my predictions (models) from my last 2 articles.

Deposit Outflow: I predicted an estimated $90B deposit outflow as of Mar 15, with a possible range between $65Bn to $95Bn.

Deposit Outflow Prediction (Author SA article)

According to its earnings release yesterday, First Republic endured a total of $102Bn deposit outflow in 1Q23, and 'deposit activity began to stabilize beginning the week of March 27, 2023'.

My modeled $90B outflow prediction is by and large accurate.

Asset Unloading | task force reduction: I predicted such a large-scale deposit outflow (supplemented by high-cost funding) would result in negative carry quickly, and the Bank would be left with few (inferior) choices to battle this ugly new reality, including task force reduction and asset unloading

According to its earnings release yesterday:

The Bank also expects to reduce its workforce by approximately 20-25% in the second quarter...

The Bank is taking actions to strengthen its business and restructure its balance sheet. These actions include... decrease loan balances to correspond with the reduced reliance on uninsured deposits. Through these actions, the Bank intends to reduce the size of its balance sheet.

Both task force reduction and asset unloading are on the card.

What's Next

We predicted 1Q23 quite pretty accurately, now the obvious question is what's next and what would 2Q23 look like?

I will take a quick detour to examine its 1Q23 results, analyze under-the-hood data, connect the dots, then provide my forward-looking view, which the management team didn't offer an opportunity to communicate with investors. (as yesterday's ER has no Q&A session)

1Q23 Earnings Results

Let us address the elephant in the room first, deposit outflow.

The official line is deposits dropped 35.5% to $104.5Bn, the footnotes added that $104.5Bn deposits include $30Bn from the large US banks. Adjusting that, deposits actually dropped from $176Bn to $74.5Bn, a 58% decline.

But a closer look reveals an even uglier picture: its non or low-interest yield deposits suffered even more loss (from 68% to 77%) as detailed in the tweet below. This is a piece of crucial information, and I will get to that in a late section.

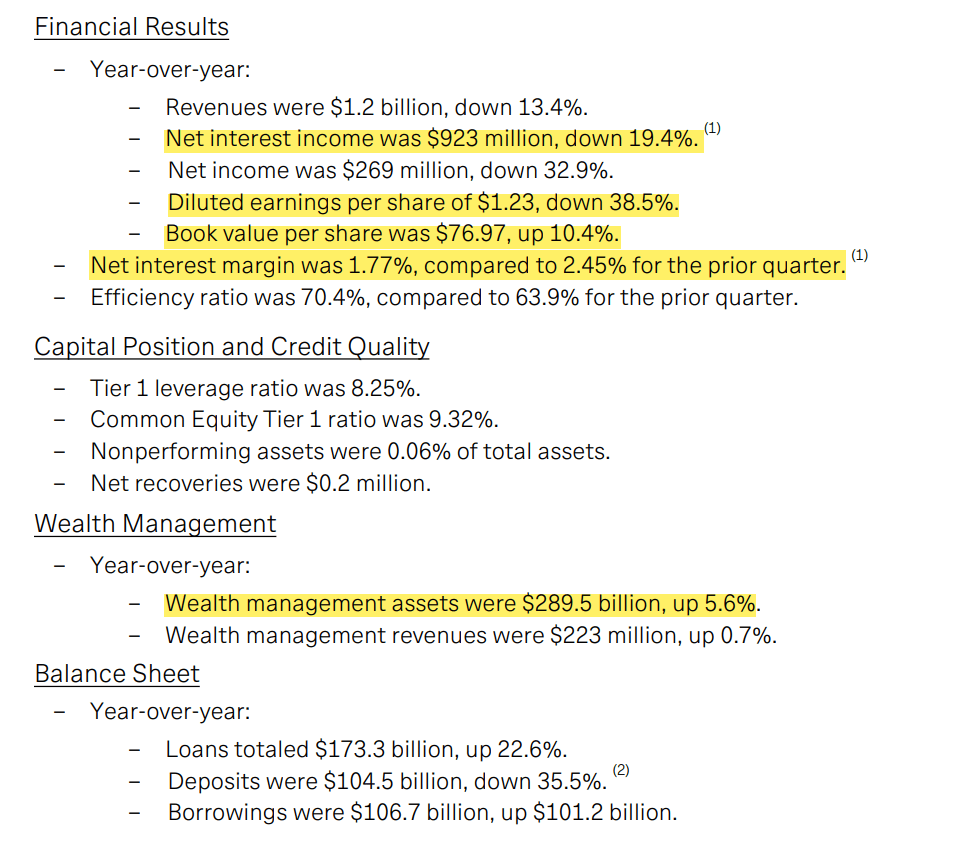

Other KPIs: while the management acknowledged the challenges the Bank is facing, they managed to strike a few positive tones highlighting its 1Q23 financial results:

{kind=link}

Many of these 'positive' numbers (such as Book Value, and WM assets) arguably have little relevance to assessing the Bank's current situation, I will just leave them alone.

I would like to highlight its reported Net interest margin, which appeared far less alarming than the reality.

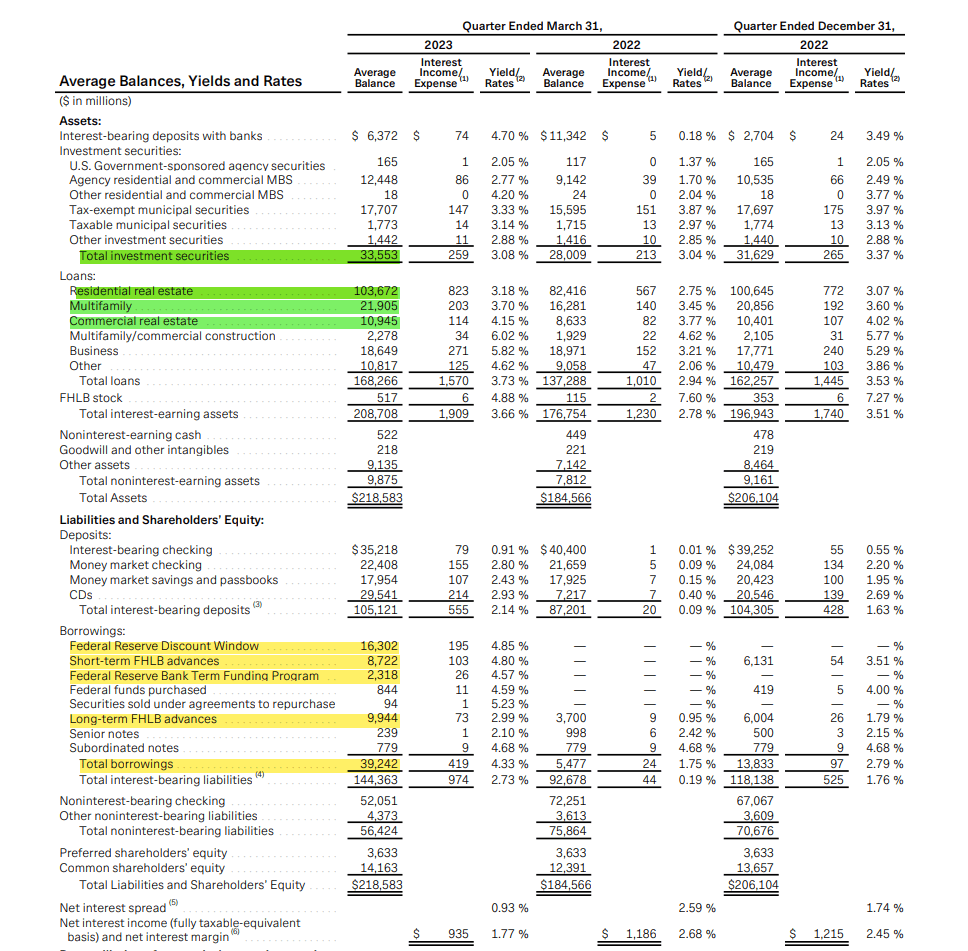

It dropped ~30% QoQ to 1.77%, yet still a very healthy margin. However, what the management didn't remind you is this number, as it shall be, includes its usual business operations from Jan to early March, as you can see from the table below, its average balance of Fed borrowing was under $40Bn (which increased to over $100Bn by the quarter end).

{kind=link}

2Q23 Forward-Looking View

Now let us turn a page, and take a look at the next quarter.

Net Interest Margin: Its ~$210Bn liability book includes $20Bn non-interest deposits, $54Bn interest-bearing deposits, $30Bn from banks, and $105Bn from various Fed programs.

For modeling purposes, I use the 1Q23 number (2.14%) for low-yield interest-bearing deposits, and 5% for Banks and the Fed borrowings.

Thus, the average yield for the liability book is 3.78%.

2Q23 Yield Model (Author)

Let us start by assuming its asset book remains steady from 1Q23 to 2Q23, its $209Bn asset will generate an average yield of 3.66% (using 1Q23 numbers), thus its Net interest margin will be dropped from 1.77% in 1Q23 to -0.12% in 2Q23.

That would incur ~$60Mn net interest deficit.

In 1Q23, its operating expense was $852Mn, its non-interest income was $286Mn. If we model a 25% reduction in its operating expense (quite a generous assumption), and non-interest income unchanged, that would result in another $350Mn in operating loss.

Combining the above 2, I model the Bank runs a roughly $410Mn loss in 2Q23, assuming (generously) no further material deposit outflow, and taking task-force reduction in full account.

$410Mn seems like a big number. However devastating, it is bearable for a bank at First Republic's scale during normal times.

But we are not at normal times. First Republic is on life support (at the mercy of the Fed, and other major Banks), so it is hard to make an argument that these sponsors would allow First Republic to play along without a concrete turnaround plan to run a safe and sound operation.

What Could be the Plan?

If I have a magic wand for the management, I would wish the low-cost deposits that left came back. Management mentioned a few times as a part of what they want to achieve, but it stays on the wish list, with no concrete plan yet. To be fair, it is quite challenging, if not impossible, to visualize a path in which a meaningful portion of these deposits could come back quickly.

How about unloading low-yield assets, and reducing high-yield funding to hopefully reach a not-too-negative operating loss?

A closer look at the asset side of its book reveals some serious issues.

For its $200Bn asset book, it requires 0.8% NIM to offset its operating expense.

Unloading its low-yield AFS and HTM securities (total $33Bn) is ideal to improve its NIM, however, that would trigger significant unrealized loss, which would put immediate pressure on its regulatory capital. I believe it should be clear by now that First Republic stands no chance to raise funding at almost any cost, today.

Most of its loan earns interest rate in the 4%-6% range, unloading them won't improve NIM meaningfully. The other viable choice is its $103Bn residential RE at an average 3.18% interest rate.

A closer look again reveals some bad news: the vast majority of its residential RE is 15Y+ loans and at an interest rate about 300bps lower than today's market rate.

Simple math is unloading them would result in a ~30% haircut to its amortized cost, it won't go far (~$45Bn) before it wipes out its entire tangible book value, in my view.

First Republic (Y22 10-K filings)

{kind=link}

In summary, I just don't see a viable path to anywhere near operational breakeven by unloading assets.

Any Viable Path to Equity Survivorship?

If there is a taker in the market, depending on the terms of the deal, I believe First Republic might survive in one form or the other.

We haven't heard any news, and I maintain my position as discussed in the last article that I don't see any potential acquirer paying anything near its current market value.

If the Bank goes down this route, I don't think any equity shareholders' interest could be meaningfully preserved.

Here comes the last path to explore its equity survivorship: First Republic is allowed to continue to be on life support, continue to cut costs to the bone, hopefully running at ~$400Mn loss a quarter, buying time, and hope the Fed cuts interest rates aggressively to a point that it can unload assets without a devastating haircut. We are talking about at least 150 to 200bps to make math potentially work.

There are a lot of ifs and wishful thinking here, so much so that I couldn't call it a credibly viable path. But, as narrow as it is, the path exists, and in my opinion, the best (though remote) chance equity shareholders have.

I just couldn't think of enough justifications to continue to hold the equity, personally.

For further details see:

First Republic: I See Almost No Viable Path To Equity Survivorship