FRC - First Republic: The Contagion Is Here - Survival At Stake Now

2023-04-26 09:30:00 ET

Summary

- Although we have been optimistic about a smaller bank model, the drastic bank run has made restructuring the only option for FRC.

- Combined with the expensive short-term borrowing and impacted profitability, the bank has a relatively challenging uphill task in the near term, worsened by the rising inflationary pressure.

- With the increased likelihood of recession, FRC's forward stock performance remains highly speculative, especially given the stock's elevated 29.52% short interest.

The FRC Investment Thesis Is Still Shaky

First Republic Bank's ( FRC ) deposit base had been drastically drained by -$103.7B/ -58.7% during the recent banking crisis (after deducting the $30B of time deposit from the US big banks) to $72.7B by April 21, 2023. With the reduced lower-cost funding options, we are uncertain how it expects to fund the bank moving forward.

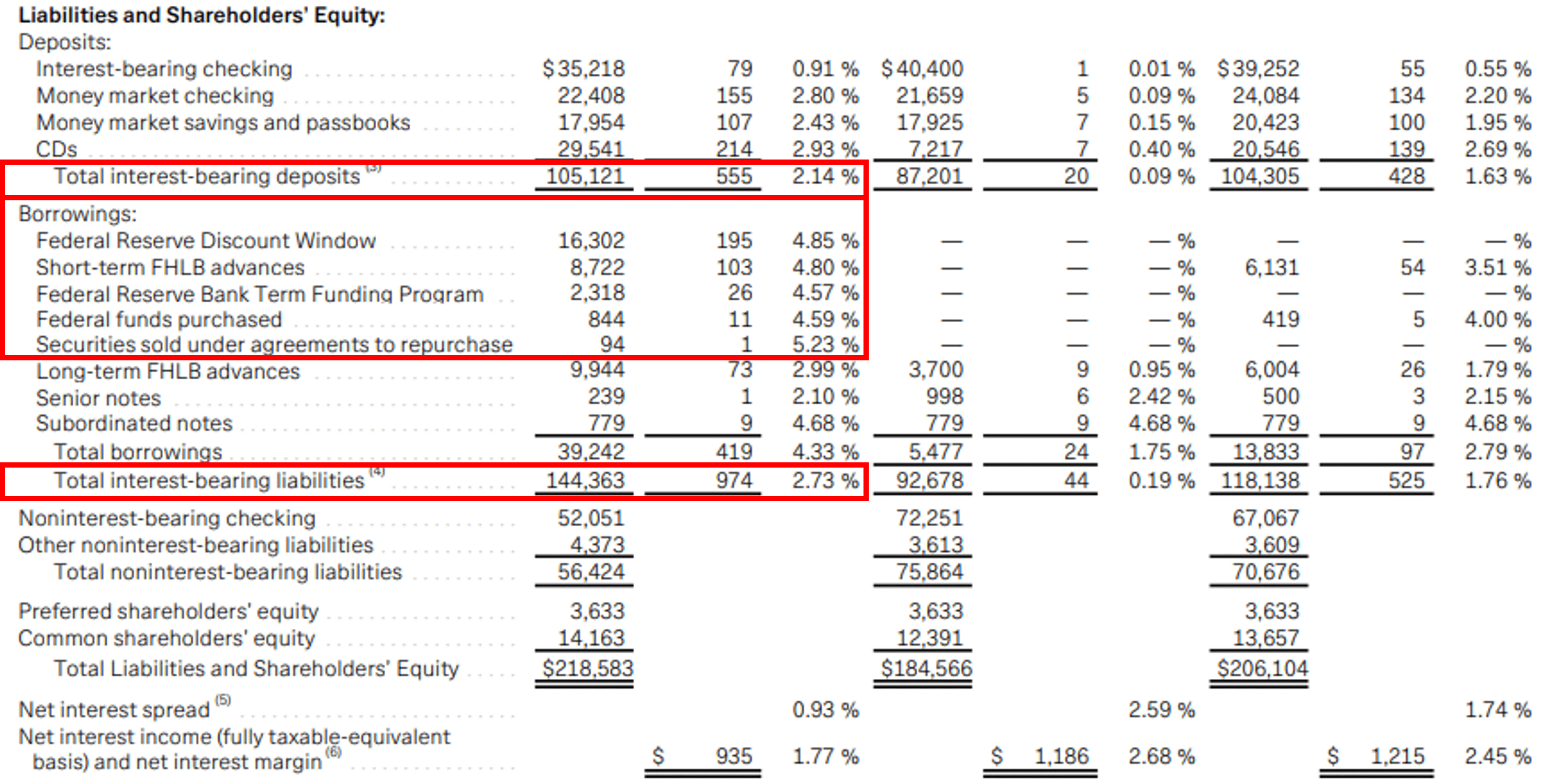

In addition, due to the "unprecedented deposit outflows," the bank also had to rely on elevated borrowings of $106.66B by the latest quarter, expanding drastically by +671.5% from $13.83B in FQ4'22 and by +1,840% from $5.5B in FQ1'22.

Notably, FRC's total interest-bearing liabilities rose to $144.36B at an average annualized rate of 2.73% and interest expense of $974M by FQ1'23, compared to $118.13B/ 1.76%/ $525M in FQ4'22, $92.67B/ 0.19%/ $44M in FQ1'22, and $88.3B/ 0.79%/ $171.97M in FQ1'19 .

FRC's Borrowings With Elevated Interest Rates

{kind=link}

In addition, investors must pay attention to FRC's short-term funding from the Federal Reserve and Federal Home Bank Loans by the latest quarter, which came with eye-watering interest rates of 4.85% and 4.80%, respectively. At the same time, the costs for its interest-bearing deposits had similarly risen to 2.14%, compared to 1.63% in FQ4'22 and 0.09% in FQ1'22, thanks to the Fed's sustained interest rate hike thus far.

These had naturally impacted the bank's Net Interest Income to $935M and Net Interest Margin to 1.77% in FQ1'23, compared to $1.21B/ 2.45% in FQ4'22 and $1.18B/ 2.68% in FQ1'22. Given that most of the moderation occurred in March 2023, we reckon its actual performance may only be truly reflected by FQ2'23, potentially indicating its drastically impacted profitability.

Then again, investors might be encouraged by the increase in FRC's single-family loans to $101.1B by the latest quarter, by +2.3% QoQ and +23.5% YoY. Since most of its clients were usually of high net worth and " sterling credit scores ," the chances of a default (for loans without deferred principal payments) seemed unlikely through the economic downturn ahead.

This strategy might have explained the bank's excellent non-performing assets at 0.06% in FQ1'23, against 0.05% in FQ4'22 and 0.08% in FQ1'22. This feat was naturally impressive, matching JPMorgan (NYSE: JPM ) at 0.06% and improved than Bank of America (NYSE: BAC ) at 0.32% at the same time.

However, with FRC still on the much-needed Federal Reserve lifeline, it is natural that the stock remains compressed thus far. Its forward execution remains uncertain due to the increased likelihood of a mild recession by H2'23 as well, especially worsened by its impacted balance sheet.

For now, the bank has outlined its pursuit of " strategic options to expedite our progress, while reinforcing our capital position." It appears that FRC is exploring major restructuring to survive as a much smaller bank, which is a prudent strategy, in our opinion.

Firstly, FRC is "focusing on increasing our insured deposits" from its new and existing client base, while also moderating its uninsured deposit ratio from henceforth.

Perhaps this is why the bank's insured deposit ratio has risen tremendously to 73% of total deposits by FQ1'23, compared to 32.3% by FQ4'22, with the deposit outflow already stabilizing since March 27, 2023.

For now, FRC also tries to offer attractive Annual Percentage Yields of between 1.30% and 1.55% for passbook savings accounts, compared to big banks such as JPM at 0.01% and BAC at 0.01%, though lower than online bank peers, such as Ally Financial (NYSE: ALLY ) at 3.75% and SoFi Technologies (NASDAQ: SOFI ) at 4.20%.

Furthermore, the bank also provides excellent CD rates of up to 4.95% for five months, compared to JPM at 4% for three months, BAC at 3.51% for seven months, and ALLY at 3.40% for six months. For clarity, SOFI does not offer CDs at the moment.

Secondly, FRC also aims to moderate its loan volumes while similarly selling off to the secondary market , potentially reducing the size of its assets on the balance sheet. This strategy may allow the bank to further decrease its reliance on expensive short-term borrowings, as discussed above.

Thirdly, the bank is also looking to "significantly reduce" operating costs through lower executive compensations, smaller lease spaces, terminating non-essential projects, and laying off up to 25% of its headcount by FQ2'23.

Based on the efforts above, FRC seems to be a major work in progress, on top of needing to prove itself to its clients and investors. The same cadence is reflected in its stock prices, suggesting Mr. Market's reduced confidence in its forward execution.

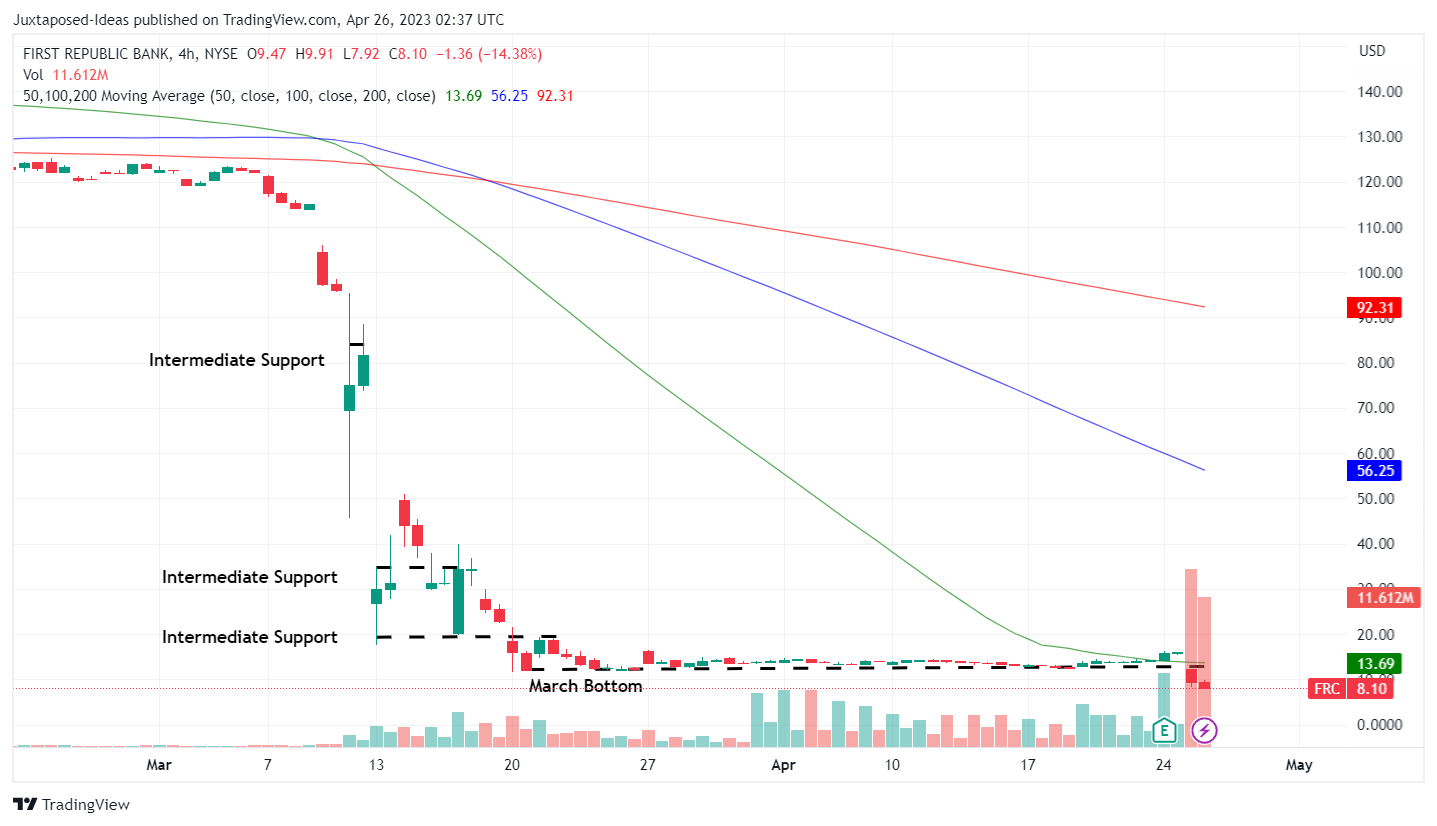

FRC 2W Stock Price

{kind=link}

For now, the FRC stock has already found a new rock bottom at $8.10, triggered by the ugly FQ1'23 earnings call. However, investors looking to add here must be reminded of the bank's potential underperformance ahead, especially since all dividends have been suspended on common and preferred stocks.

On the one hand, assuming a moderate return in deposits and sustained moderation in the bank's short-term borrowings, we reckon these depressed levels may offer a rather attractive risk-reward ratio for highly speculative portfolios.

On the other hand, there is also the possibility that everything goes south in the near term, with the federal government bailing out FRC, similar to the Silicon Valley Bank and Signature Bank in March 2023. Naturally, shareholders' capital has been wiped out then.

With many safer banks to deposit and invest in, we can understand Mr. Market's wait-and-see stance for now, due to its potential for failure ahead.

Therefore, we prefer to prudently rate the FRC stock as a Hold (Neutral) here, due to the potential volatility ahead. Anyone who adds here must be willing to weather moderate to high levels of risk, in our view, especially due to the stock's elevated short interest at 29.52%, despite the drastic corrections thus far.

Lastly, the Fed is likely to raise interest rates by another 25 basis points in May 2023, further impacting the bank's execution in the near term.

For further details see:

First Republic: The Contagion Is Here - Survival At Stake Now