FWRG - First Watch Restaurant Group: A Quickly Growing Breakfast Concept With A Share Price That's Already Full

2023-04-04 13:56:43 ET

Summary

- Changes in morning routines and employees returning to the office offer First Watch Restaurant Group potential growth opportunities.

- The company has ambitious plans for future expansion, despite mass competition.

- It taps into Millennial and Gen Z trends of breakfast foods and healthy dining options.

- Strong growth appears to be already priced in and I see little upside at these levels, so I rate the stock a Hold currently.

The Opportunity

Taking its name from the nautical term of the first shift of the day, First Watch Restaurant Group (FWRG) operates a chain of US based restaurants specializing in and open only for breakfasts, brunches and lunches - so called 'day time meals'. According to RKMA, as cited in the company’s S1 , these meal times make up 63% of all restaurant sales, which also leaves the company with a potential lever for future revenue growth - who doesn’t love breakfast for dinner?

The Thesis

The breakfast taking out and eating out segments have a 10-year annualized growth potential of 7.2%, according to Grand View Research . In my view, a growing market and a pure-play option makes First Watch Restaurant Group an interesting investment opportunity. Looking at what can happen to the stocks of successful restaurant chains makes the chance to get in relatively early to this 2021 IPO, which is down around 18% from its initial offering price, an intriguing one.

A look at the company's earnings slides or its S1 clearly highlights its focus on fresh food, selling trendy items that are highly desired by Millennials and Gen Z, such as avocado toast, smoothies and pancakes as well as a selection of gluten-free and vegan options. A search on Google Maps shows that the vast majority of the company's restaurants receive very high reviews of around 4.5 upwards. I warn you not to Google Image search ‘First Watch menu’ if you are hungry!

The company designs its restaurants to reflect its “Urban Farm” brand and tap into the rustic chic vibe that gives its diners the simultaneous feeling of being in a contemporary setting whilst nostalgically remembering a simpler time. New restaurants are constructed to seat 120 plus diners and often offer patio/outdoor seating. It is the exact place I'd imagine influencers who work at Google go to update their Instagram whilst eating their breakfast and drinking their health drinks!

The Story Since IPO

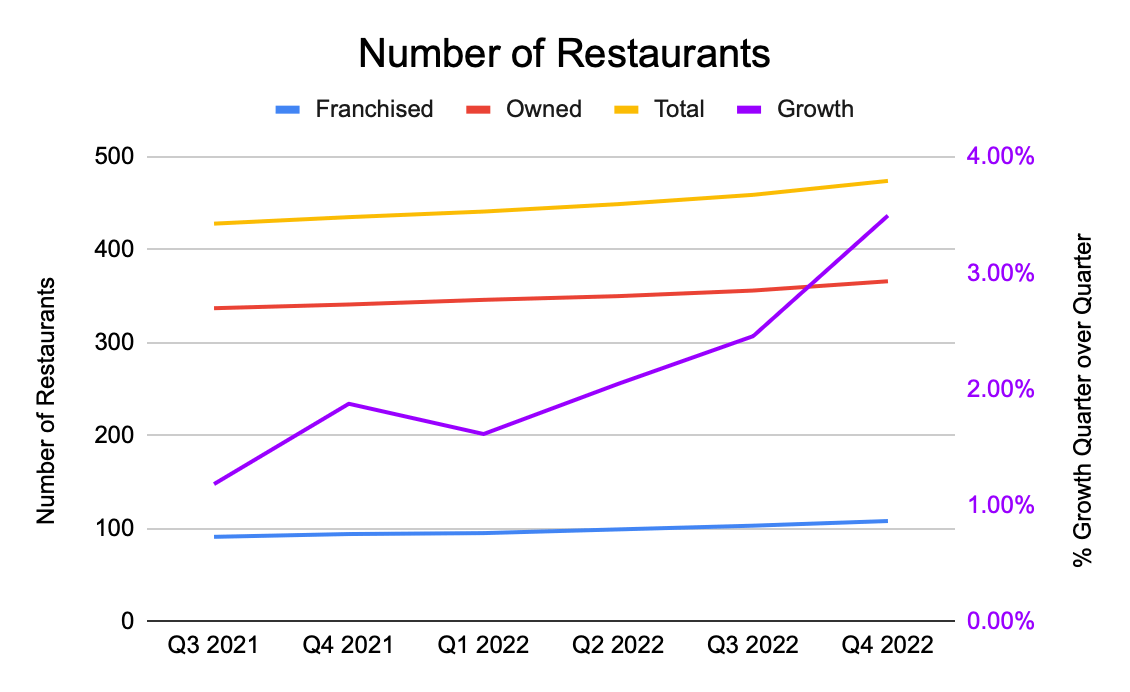

The company has been growing since its IPO at the end of 2021 and its growth is starting to accelerate (see purple line). It now operates nearly 500 restaurants in 29 states, around a fifth of which are franchised with the rest company owned. The company cites in its Q3 2021 press release that it believes their brand has the potential to reach more than 2,200 restaurants. Let’s take a look at those numbers and see how much value there is for us to invest at today’s prices.

{kind=link}

Growth of Number of Restaurants since IPO (Compiled by Author based on data from Company)

Valuing First Watch

Let’s start with the company’s belief that they can reach 2,200 restaurants US wide. The most recent quarter on quarter growth was 3.49%. Although this rate is accelerating, let’s be conservative and use 3.49% as an expected growth rate to see how long it would take to reach 2,200. I calculate that this figure is reached in exactly 10 years.

| Q1 2023 |

| 492 |

| Q4 2025 |

| 730 |

| Q3 2028 |

| 1079 |

| Q2 2031 |

| 1587 |

| Q2 2023 |

| 510 |

| Q1 2026 |

| 757 |

| Q4 2028 |

| 1117 |

| Q3 2031 |

| 1643 |

| Q3 2023 |

| 529 |

| Q2 2026 |

| 784 |

| Q1 2029 |

| 1157 |

| Q4 2031 |

| 1702 |

| Q4 2023 |

| 548 |

| Q3 2026 |

| 813 |

| Q2 2029 |

| 1199 |

| Q1 2032 |

| 1762 |

| Q1 2024 |

| 568 |

| Q4 2026 |

| 842 |

| Q3 2029 |

| 1242 |

| Q2 2032 |

| 1825 |

| Q2 2024 |

| 589 |

| Q1 2027 |

| 872 |

| Q4 2029 |

| 1286 |

| Q3 2032 |

| 1889 |

| Q3 2024 |

| 611 |

| Q2 2027 |

| 904 |

| Q1 2030 |

| 1332 |

| Q4 2032 |

| 1956 |

| Q4 2024 |

| 633 |

| Q3 2027 |

| 937 |

| Q2 2030 |

| 1379 |

| Q1 2033 |

| 2026 |

| Q1 2025 |

| 656 |

| Q4 2027 |

| 970 |

| Q3 2030 |

| 1429 |

| Q2 2033 |

| 2097 |

| Q2 2025 |

| 680 |

| Q1 2028 |

| 1005 |

| Q4 2030 |

| 1480 |

| Q3 2033 |

| 2172 |

| Q3 2025 |

| 705 |

| Q2 2028 |

| 1041 |

| Q1 2031 |

| 1532 |

| Q4 2033 |

| 2249 |

Author's Calculations

First Watch cites in its S1 that from the 3rd year of a newly opened restaurant being opened, it would have an operating margin of 19% . This seems like a fairly good target. Larger chains that are optimized for scale and efficiency such as McDonald's and Restaurant Brands have average 5-year EBIT margins of 40.65% and 34.91%, whilst younger and quicker growing chains like Chipotle are at 8.47%.

Let’s use that in our assumptions along with a revenue growth rate of 15% during this 10 years of quick expansion. Using the company's 19% EBIT estimate and a free cash flow margin of around 8% based on my expectations of the sector, I get a full-year 2033 that looks a little like this:

2033 - Revenue $2,954 billion

2033 - EBIT $561 million

2033 - FCF $106 million

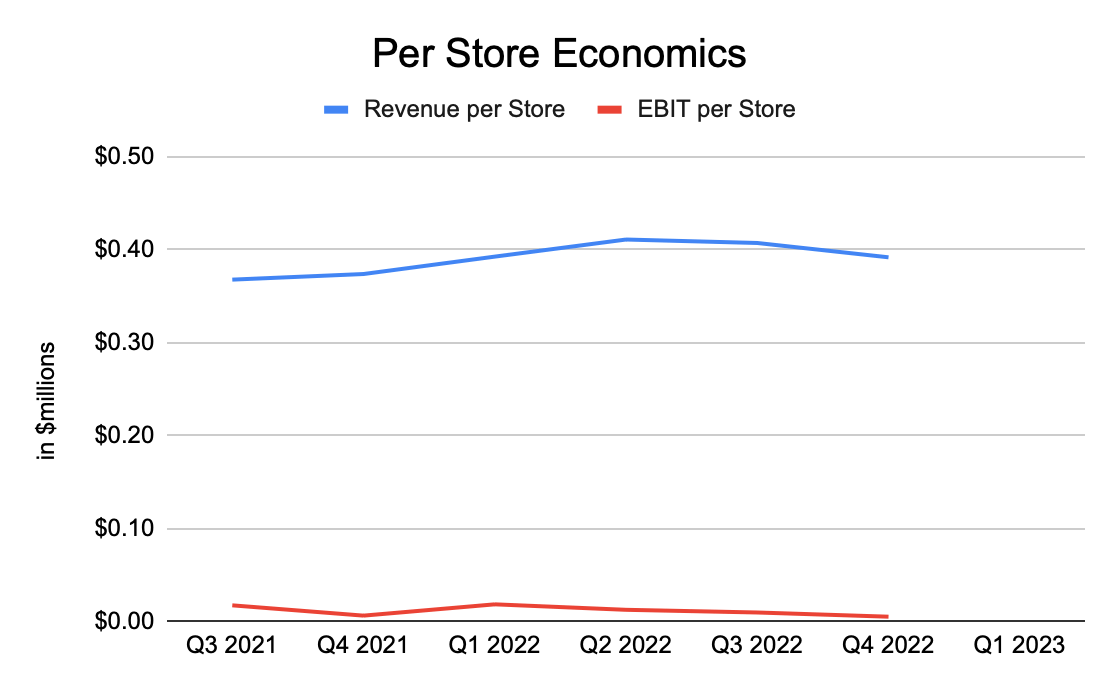

Simplifying the numbers by dividing the revenue and operating margin companywide by the number of restaurants, not taking into consideration that the company states that its operating margins increase after the first year of opening new stores as they establish themselves in a new area (pg. 37 of the company's S1 cited above), the current unit economics of its restaurants are quite flat albeit only using post IPO data.

{kind=link}

Unit Economics of Each Restaurant (Simplified) (Compiled by Author based on data from Company)

This is a metric potential investors have to keep an eye on. For retail and restaurants, one wants to see the number of stores/restaurants increase as well as the sales per store or restaurant. The company itself is forecasting in its Q4 2022 Earnings Presentation a same-store sales growth of 6-8%. So far, First Watch is growing its store count without necessarily improving its per store economics. As it scales and head office becomes more efficient, I would expect this to quickly change.

Applying sector average EV/EBIT, Price to FCF, and Price to Sales multiples (taken from sector medians on Seeking Alpha), and assuming a static share count, we arrive at the following future valuations out 10 years for 2033:

| EV/EBIT |

| 13.06 |

| $1,348.54 |

| FCF Multiple |

| 11.88 |

| $1,266.90 |

| Price to Sales |

| 0.86 |

| $2,540.50 |

| Restaurant Level |

| * |

| $1,504.80 |

| Future Market Cap |

| $1,770.73 |

| Future Share Price 2033 |

| $29.91 |

Author's Calculations

*Note, the Restaurant Level valuation was calculated by multiplying 2200 stores x 400k per store x 19% EBIT margins with an effective tax rate of 25% (Company S1, p85).

Averaged out, we have a future valuation for the whole company of $1.77 billion. Assuming the same number of shares, this is a share price of just under $30, representing a return of around 7%. While this is not a bad return, at this price I don’t believe it will beat the market unless there were changes that I will explain in this next section.

How Can First Watch Beat The Market and Change My Hold to a Buy?

There are levers that can be pulled to increase the upside. The company could either surpass its expectation of 2,200 stores or grow more quickly and improve its margins as new stores become established. Operating margins could expand from scale and offer more than the 19% expected. Further, it could use the breakfast concept as its core business and then branch out into new concepts and new brands.

All of these things could support growth. But the two I am most interested in are all-day service and international expansion.

The concept of high-quality breakfast and brunch food being offered in cosy and clean restaurants is certainly one that I can see being successful outside of the US. Long-term trends towards health-conscious options and premium foods is one also being experienced in Europe, too. Further, as popularized in Scrubs, ‘Brinner’ or eating breakfast food for dinner or later meals is definitely a marketing strategy that I would like to see in the future. Yes, it would then put the company even more competitively up against many other restaurants, but extending its opening hours could potentially be a way to improve revenues and buy core ingredients at a larger scale, improving margins.

The other way that I foresee the company offering a market-beating return would be increasing franchise-owned business as a proportion of its total restaurant count. As you can see from the chart below, the company is slowly increasing the proportion of franchised restaurants.

| Quarter |

| Franchise Owned |

| Company Owned |

| Restaurants |

| Proportion of Company Owned |

| Q3 2021 |

| 91 |

| 337 |

| 428 |

| 78.74% |

| Q4 2021 |

| 94 |

| 341 |

| 435 |

| 78.39% |

| Q1 2022 |

| 95 |

| 346 |

| 441 |

| 78.46% |

| Q2 2022 |

| 99 |

| 350 |

| 449 |

| 77.95% |

| Q3 2022 |

| 103 |

| 356 |

| 459 |

| 77.56% |

| Q4 2022 |

| 108 |

| 366 |

| 474 |

| 77.22% |

Compiled by Author based on data from Company

My View Looking at Full Year 2022 Earnings

First Watch looks like the type of restaurant I would enjoy eating breakfast. As an investor who is staring down the barrel of 40, I might be slightly above the target market, but the drive for premiumization and health consciousness is certainly in the zeitgeist in developed markets, and there is a niche to be filled by being the big name in the breakfast and brunch space. There is plenty of room for consolidation of this fragmented market.

I like to see management being realistic in their forward projections, particularly for recent IPOs where there isn't sufficient data for me to use the numbers as my own guide.

Before I looked at the FY2022 earnings, I revisited their outlook from FY2021 . The company had projected same-restaurant sales growth in the high-single digits, whilst they actually came out much higher than that at 14.5%. They forecast revenue growth in excess of 15% and were actually able to grow revenue by 21.5%. Their adjusted EBITDA estimate was in the range of $67.0 million to $71.0 million and came out in the middle at $69.3 million. Finally, they predicted that there would be between 30-35 new company owned restaurants opened and 8-13 franchised restaurants. They actually opened 29 company owned and 14 franchised. My observations here is that leadership know their business and were either slightly conservative or spot on with their FY estimates. Something I definitely like to see.

For the upcoming full year of 2023, management is guiding for 6-8% same restaurant sales growth, which sounds to me like price adjustments to negate the effect of inflation on their raw ingredients and increased labor costs rather than real organic growth. They are forecasting revenue growth of 15-19%, which sounds healthy. I would like to see a 18% compound annual growth and a doubling of revenue from here in the next 4 years. They expect adjusted EBITDA in the range of $76.0 million to $81.0 million. Assuming that management hit around the mid guidance again, $78.5 million would see a YoY growth of around 13%. Finally, 45-51 new restaurants are forecast of which 38 to 41 would be company-owned and 10 to 12 franchise-owned. They are calculating this net of 3 restaurant closures. I could not find a detailed reason for these closures and would like to see management clearly cite these looking forward.

Summary

First Watch, whilst currently a pure play on the breakfast and brunch trends, has plenty of competition from other restaurant brands and concepts that also offer meals during these times. Not only are First Watch battling the McDonald’s ( MCD ), Wendy’s ( WEN ) and Starbucks ( SBUX ) of the world, but there are other smaller chains also looking to franchise their breakfast concepts, such as Sunny Street Cafe, which offers potential franchisees a lower initial cost than First Watch.

Restaurants and cafes are so abundant that the serving of breakfasts and other meals becomes increasingly commoditized. First Watch has a strong brand, a clear concept that is trendy and is benefiting from longer term changes in consumer tastes and is growing quickly but unless they can open more restaurants than they think, expand internationally, widen their operating hours or use a mix of pricing power and scale to increase profitability (or preferably a combination), I believe that the share price is already full baked and is a hold from here.

I am going to watch the next couple of quarters and pay particular attention to franchisees, margins and the speed at which they are opening new restaurants. If the company can offer another year of guidance being met, then I might be onboard for the ride. Until then, First Watch is very much a company I will continue to follow.

For further details see:

First Watch Restaurant Group: A Quickly Growing Breakfast Concept With A Share Price That's Already Full