FCFS - FirstCash Holdings: Consumer Delinquencies Creeping Up

2023-09-07 09:51:00 ET

Summary

- FirstCash Holdings is the largest pawn operator in the U.S. and Latin America. It also owns an LTO payments business that is available in over 10,500 retail locations.

- The Pawn business is countercyclical and should perform well as low income consumers struggle. However, the LTO payments business is hyper cyclical and focuses on high risk consumers.

- Given the uncertainty regarding loss ratios in the LTO payments business and FirstCash's elevated valuation, I remain neutral on FCFS stock.

Late last year, I downgraded FirstCash Holdings ( FCFS ) stock to a hold rating. Although I was constructive on the countercyclical nature of the pawn business, I was concerned its newly acquired America First Finance ("AFF") lease to own ("LTO") payments business is highly cyclical and could suffer from a pending recession. Since my downgrade, FCFS has essentially tread water, returning -5.3% in total return compared to 16.5% for the S&P 500 (Figure 1).

Figure 1 - FCFS has gone nowhere since downgrade (Seeking Alpha)

With recession fears receding as economic growth has continued to be robust, has the outlook improved for AFF, and does FCFS deserve another look?

Brief Company Overview

First, a refresher on the company for those not familiar. FirstCash Holdings Inc. is the largest operator of pawn stores in the U.S. and Latin America, with over 2,900 retail locations. FirstCash also operates a retail point-of-sale ("POS") payments solution that provide lease-to-own loans to credit constrained consumers.

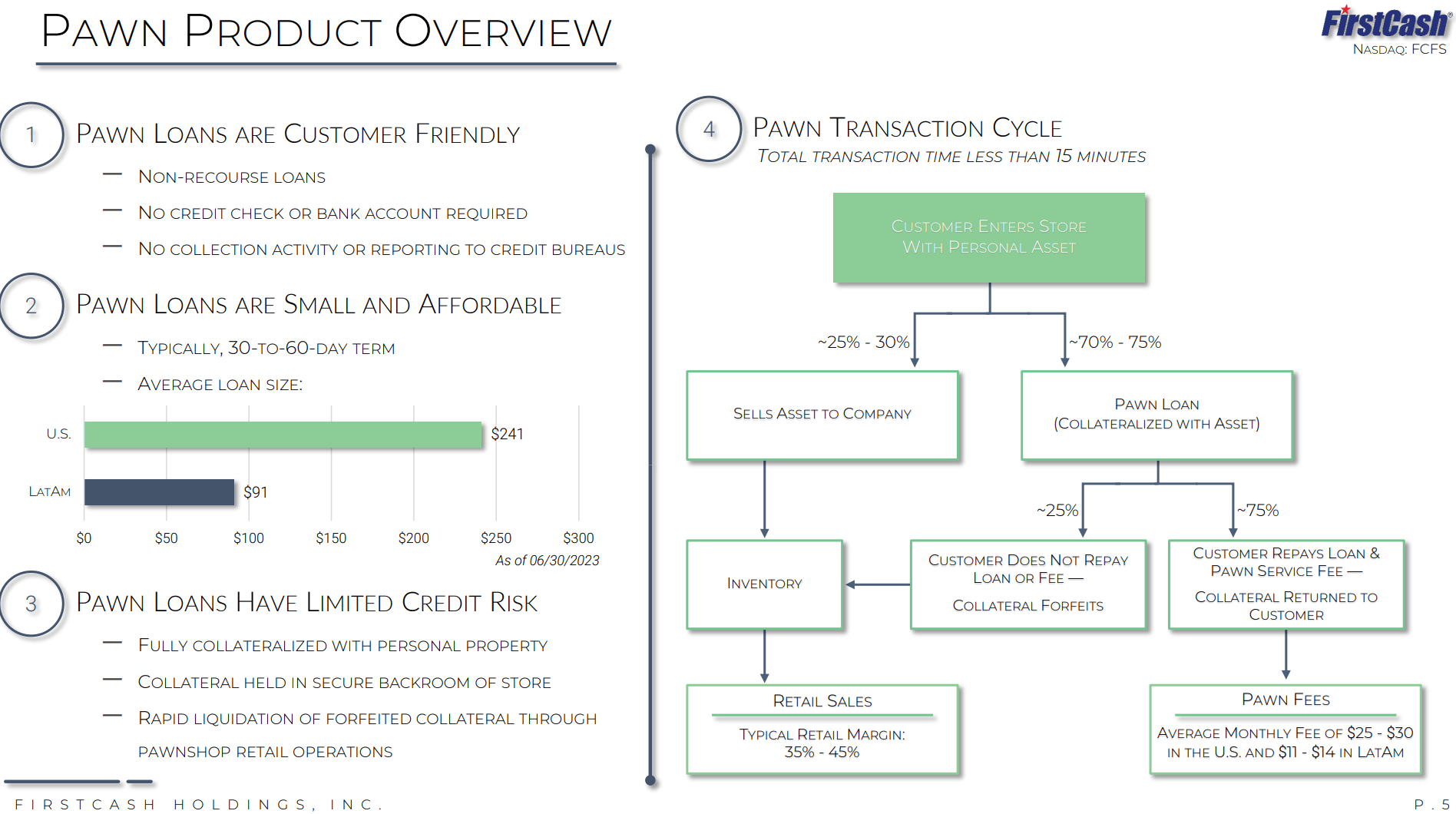

Contrary to popular belief, although pawn loans are typically made to credit constrained consumers, the credit risk associated with these loans are very low as the loan receivables are fully collateralized at a fraction of the collateral's market value (Figure 2).

{kind=link}

Figure 2 - Pawn loan overview (FCFS investor presentation)

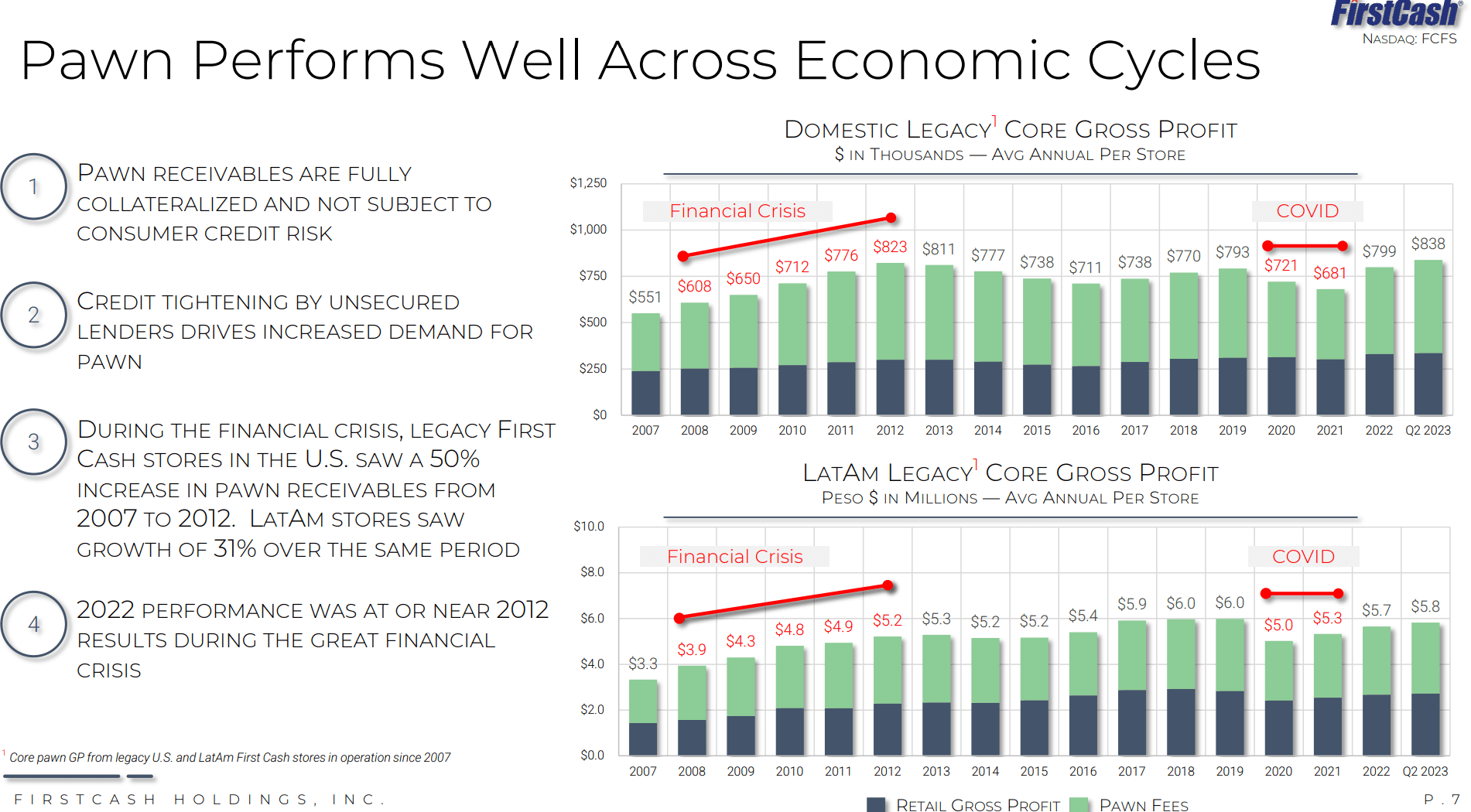

Historically, utilization of pawn services tend to be countercyclical, as financially stretched consumers increase their use of pawn loans and other alternative credit solutions during tough economic periods. In fact, during the Great Financial Crisis, receivables per store for FirstCash actually saw an increase from $551k in 2007 to $823k in 2012, reflecting financial hardship on low-income consumers (Figure 3).

{kind=link}

Figure 3 - Pawn performs well during tough economic times (FCFS investor presentation)

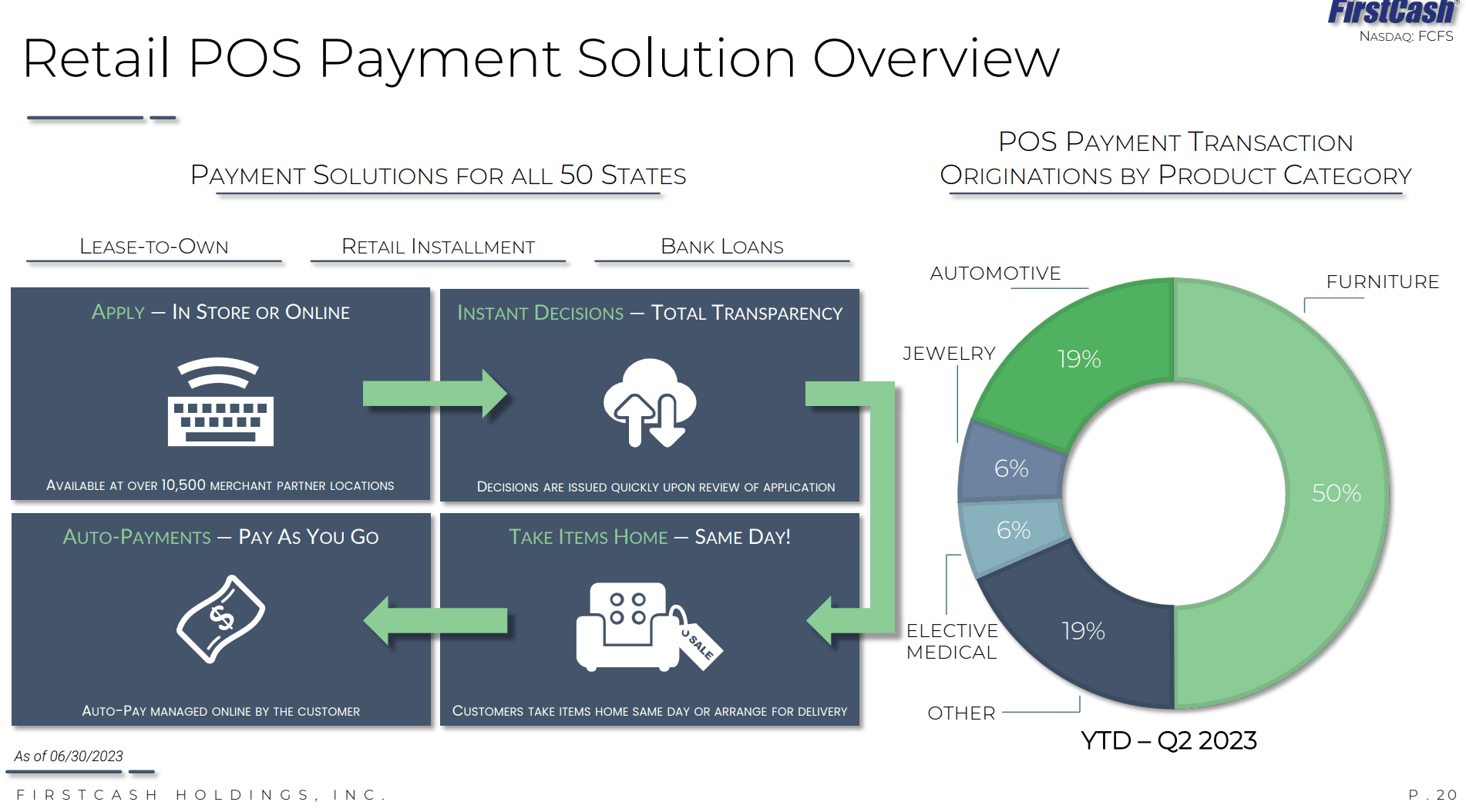

However, in late 2021, FCFS acquired America First Finance, a provider of Point of Sale ("POS") LTO payment solutions. Credit constrained consumers basically apply for LTO loans to purchase big ticket items at thousands of retail stores across the country (Figure 4). As of Q2/23, FCFS' LTO payment product is available in over 10,500 retail locations.

{kind=link}

Figure 4 - POS LTO payments overview (FCFS investor presentation)

The POS LTO business, while targeting the same customer segment as the core pawn loan business, has vastly different fundamentals as loans are made on the retail purchase price of the merchandise. Loss ratios are expected to be high, due to the consumer segment, but is made up through high interest rates charged on the loans.

Latest Quarter Continued To Show Strong Growth

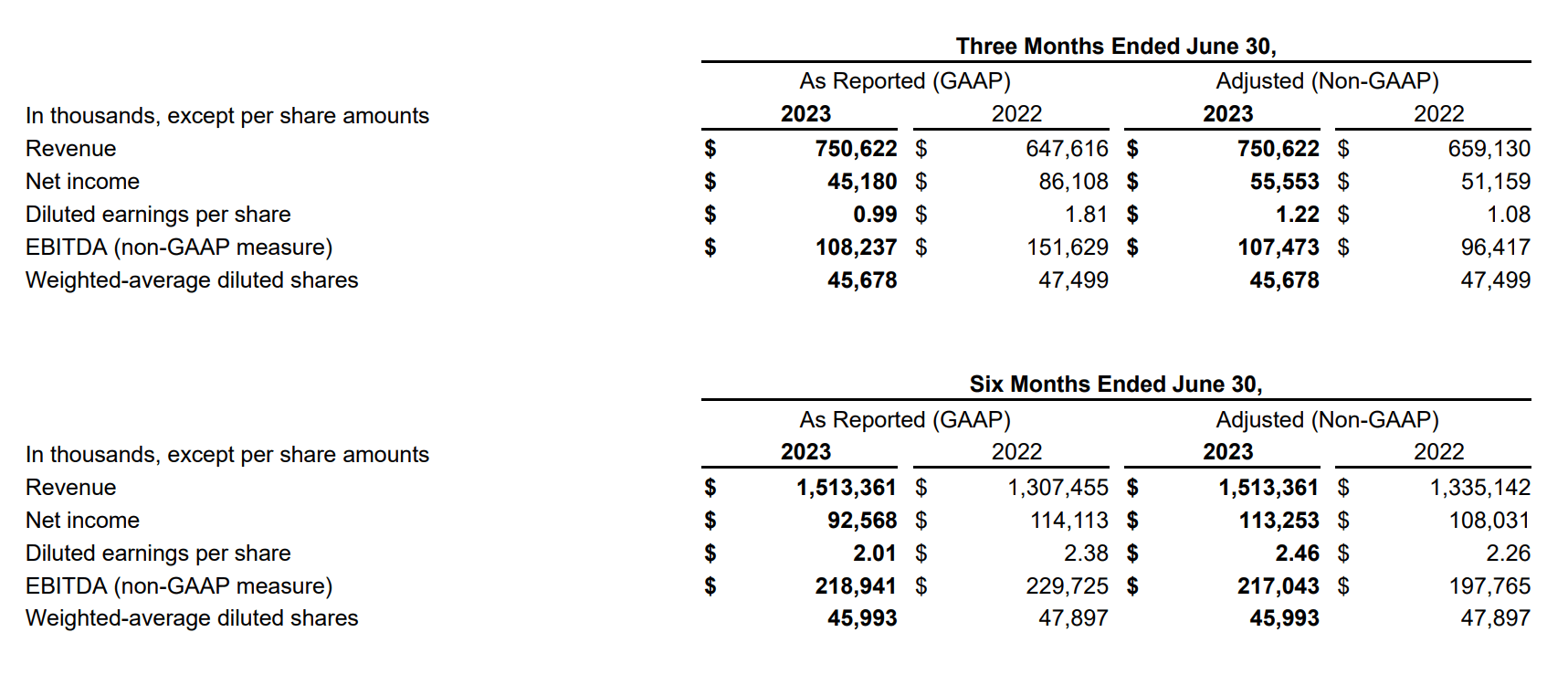

Recently, FirstCash reported its fiscal Q2/23 results that showed strong growth in both revenues and earnings. For the quarter, revenue was $751 million, $19 million ahead of analyst estimates. Adjusted EPS was $1.22, $0.14 ahead of consensus (Figure 5). YTD, revenue was $1.51 billion, an increase of 13.3% YoY while adjusted EPS was $2.46, an increase of 8.8% YoY.

{kind=link}

Figure 5 - FCFS performed well so far in 2023 (FCFS investor presentation)

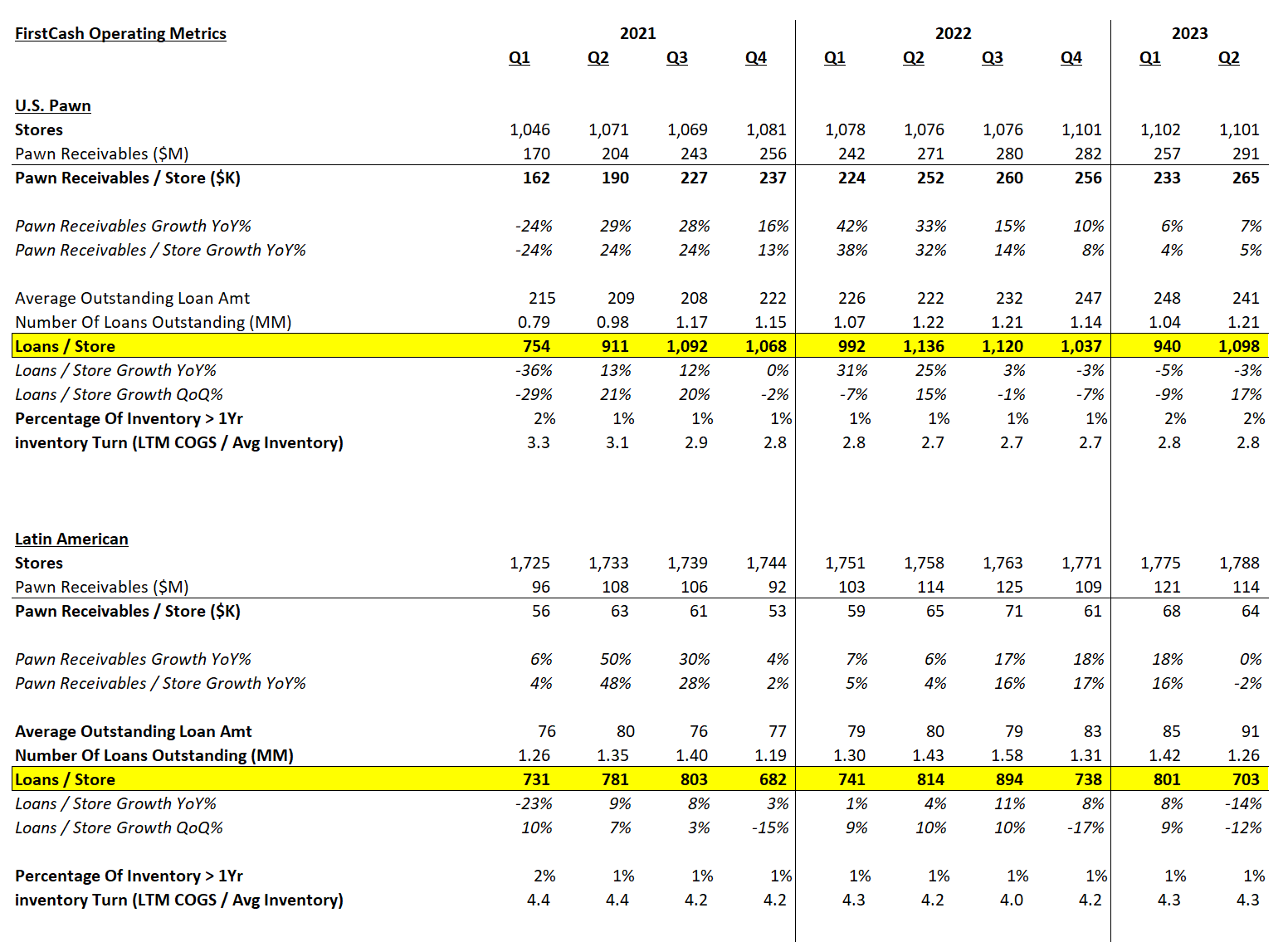

Operationally, FirstCash's U.S. pawn business continued to perform well, with loan receivables growing 7% YoY although loans / store declined by 3% YoY in the seasonally strong second quarter. Average loan balance remains elevated to recent history at $241 / loan (Figure 6).

{kind=link}

Figure 6 - FCFS pawn operating metrics (Author created with data from company reports)

Operating results in the Latin American segment was not as strong as loan receivables were flat YoY. Loans / store declined 12% YoY while average balance grew from $80 to $91.

LTO Payments Is The Focus Of My Attention

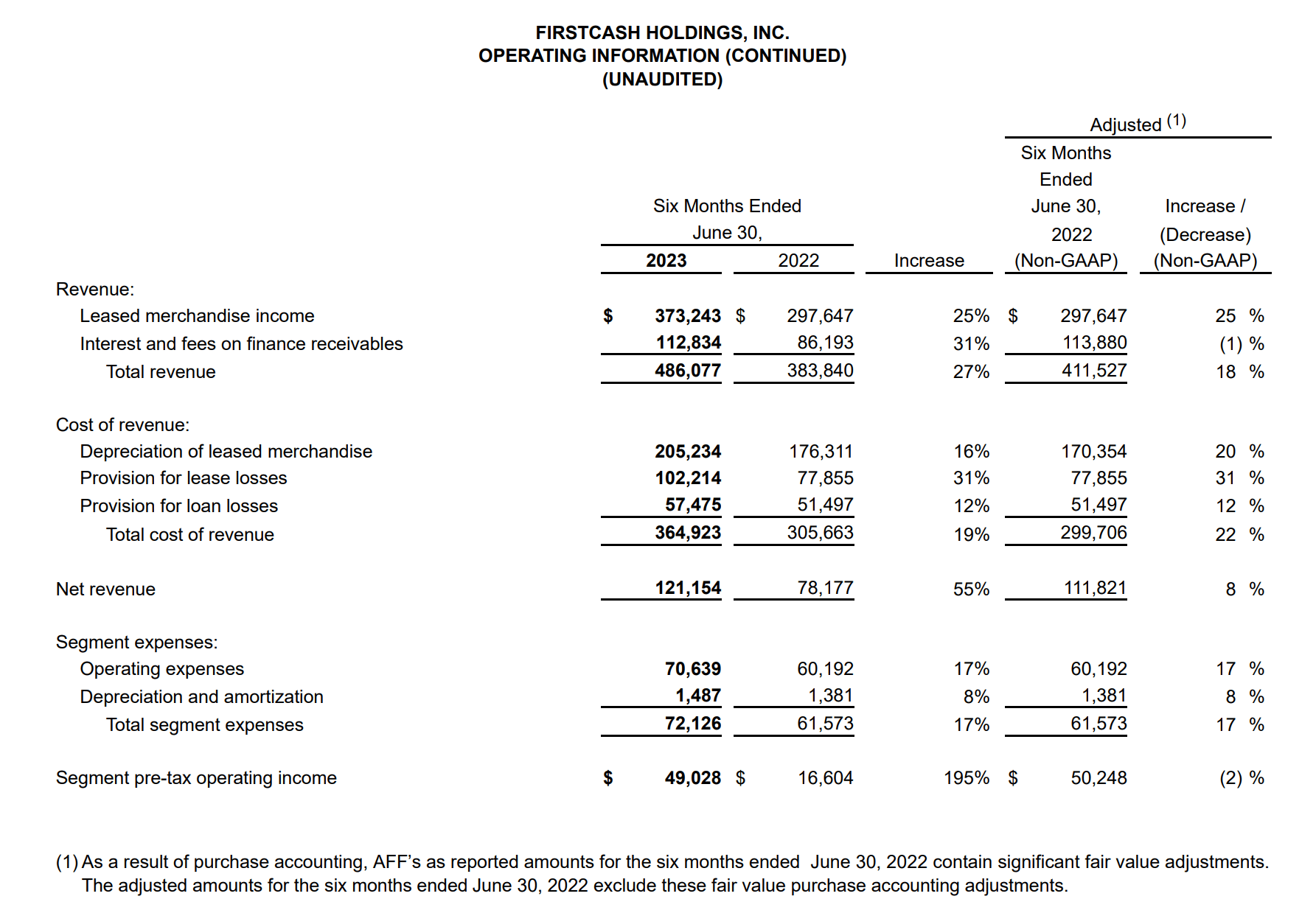

In the key American First Finance segment, operating results saw YTD revenues grow 18% YoY to $486 million (comparing to adjusted financials in Figure 7 below). However, revenues net of depreciation of leased merchandise and provision for losses only grew 8% YoY.

{kind=link}

Figure 7 - AFF operating results (FCFS Q2/23 press release)

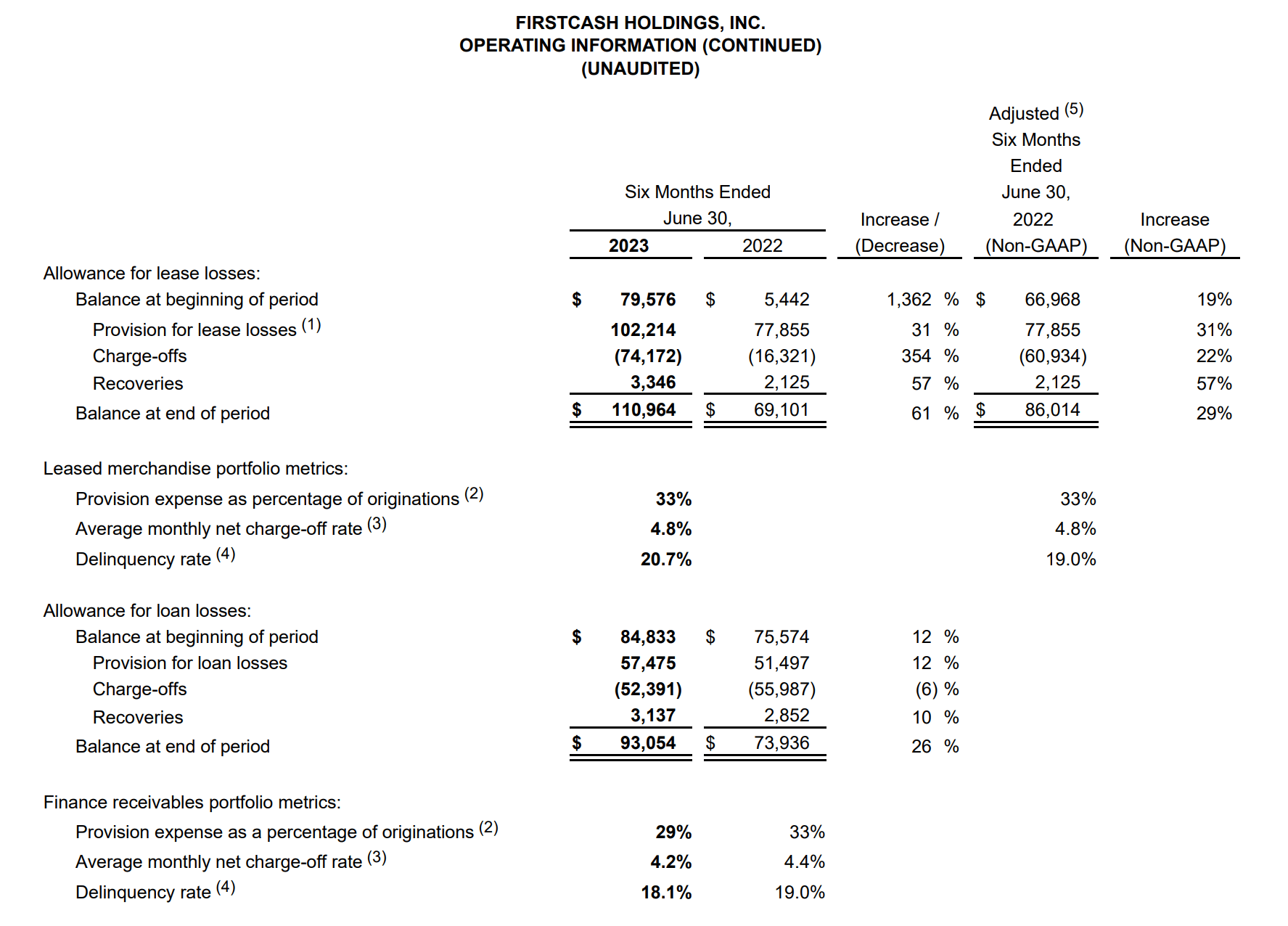

Credit metrics deteriorated in the lease portfolio, with delinquency rates of 20.7% vs. 19.0% YoY and 17.3% in Q1. The average monthly net charge-off rate was 4.8% in Q2, the same as the prior year and a slight improvement against Q1's 5.0% (Figure 8).

{kind=link}

Figure 8 - AFF credit metrics (FCFS Q2/23 press release)

Within the loans portfolio, delinquency rates improved to 18.1% from 19.0% YoY, but slipped QoQ from 16.1% in Q1. The average monthly net charge-off rate was 4.2% vs. 4.4% YoY and 4.3% in Q1.

Early Signs Of Credit Deterioration?

Readers who followed my research know that I am quite bullish on the countercyclical pawn business, as I have a buy recommendation on FirstCash's largest peer, EZCorp ( EZPW ).

My hesitation on FirstCash was entirely due to the cyclical LTO payments business. So far in 2023, we have seen provision for lease and loan losses climbed 23% YoY from $129 million to $160 million. However, this is mostly a result of the growth in origination volumes, from $391 million in H1/22 to $506 million in H1/23 (+29% YoY). As a percentage of originations, PCLs actually declined from 33% to 32%.

Looking forward, I am concerned that PCLs and/or writeoffs may increase, as we have seen delinquency rates increase QoQ on both the lease and loan portfolios. Delinquencies is a forward looking indicator and suggest the credit quality of AFF's customers may be deteriorating.

Core Customer Is Struggling

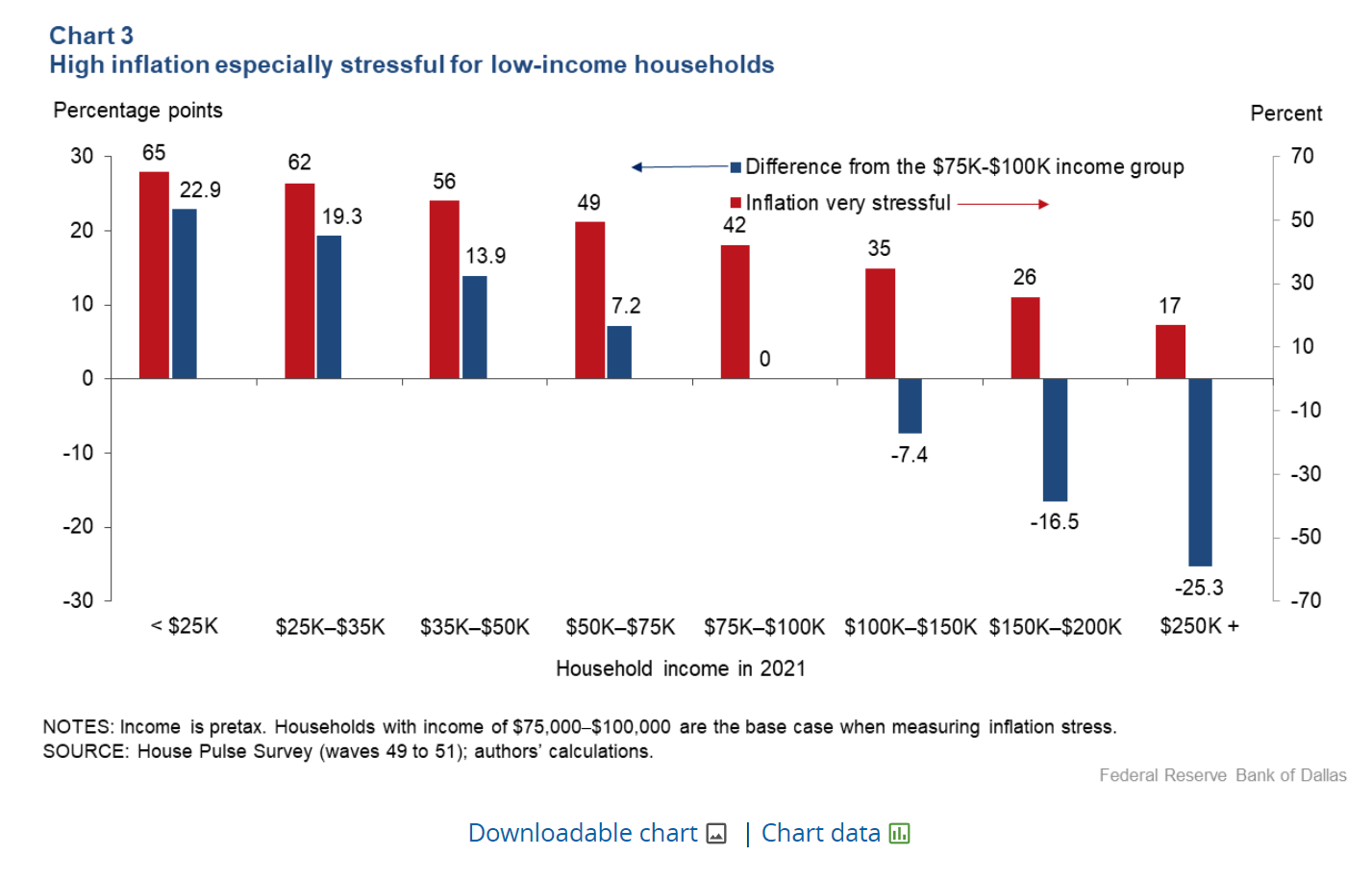

The pressure on AFF's customers is understandable, as inflation has been hitting low-income consumers particularly hard. According to the Dallas Fed, low income households are particularly stressed by high inflationary pressures (Figure 9).

{kind=link}

Figure 9 - High inflation is hitting low income households hard (Dallas Fed)

For example, Dollar General ( DG ), the dollar store chain with close to 19,000 stores, recently had to reduce its full year guidance as the core low-income customer continues to struggle in the current economic environment. Dollar General's CEO had this comment regarding the customer:

On the customer, she still is challenged, and we talked about that in the first quarter and that continues. Our customer, what she's telling us is that certainly as gas prices are less than last year, but they're accelerating throughout 2023, and she's still feeling the headwinds of the SNAP reduction and also the lack of tax refunds. And her savings are gone. And so certainly, she is still living with the inflationary pressure. So certainly, the customers are challenged.

In fact, according to a recent Bloomberg news article, many struggling consumers are resorting to 'buy now pay later' ("BNPL") services like Afterpay and Klarna to afford everyday essentials like groceries.

FirstCash/AFF Not Built For Recession

The problem for AFF is that it lends on the retail value of merchandise. Although the LTO lease payments are priced for high losses (PCLs over 30% of originations), actual loss ratios may surge even higher during recessions as consumers default on payments.

More importantly and maybe more problematic, LTO payments tend to be utilized for big ticket items like furniture and appliances which are difficult to repossess. Traditional LTO players like Aaron's ( AAN ) and Rent-A-Center (now part of Upbound Group) have large store networks such that when customers default on payments, merchandise can be repossessed, refurbished, and re-leased quickly. AFF, which relies on FirstCash's network of relatively small footprint pawn stores, is not physically set up to handle large volumes of big ticket items like beds, sofas, and TVs.

Resumption Of Student Loan Payments May Be A Risk And An Opportunity

Another upcoming risk/opportunity for FirstCash is the pending resumption of U.S. federal student loan payments in October .

According to a Bank of America survey , this will impact more than 43 million Americans, who, on average, will have to budget an extra $200-400 per month to repay student loans. A recent Consumer Financial Protection Bureau ("CFPB") article suggests that one in five borrowers could struggle financially once the student loan repayments resume.

For FirstCash's U.S. Pawn business, struggling Americans could be a boon to business, as consumers have no choice but seek alternative credit solutions. At the same time, this could lead to elevated losses on the LTO payments business.

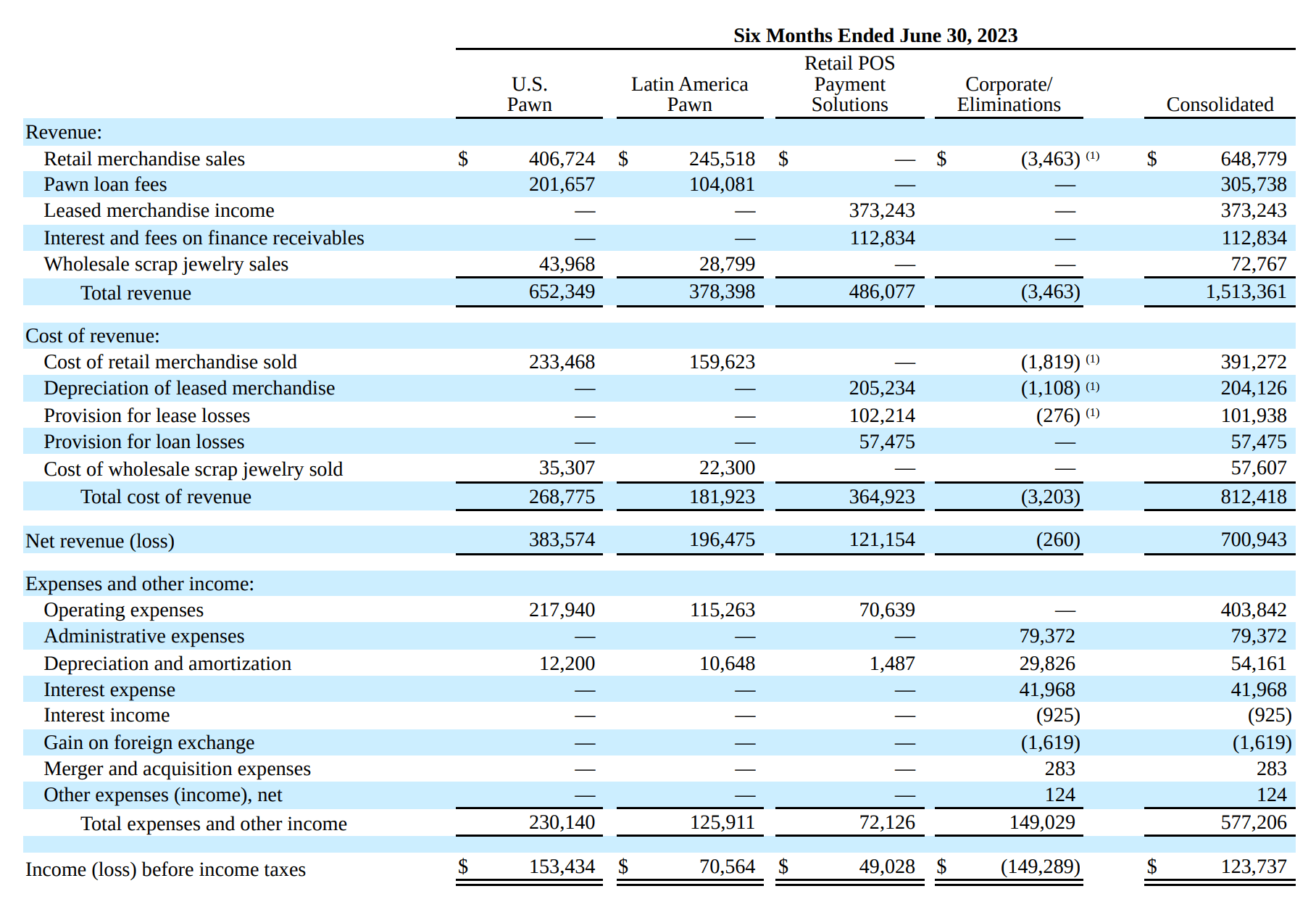

On net, I believe the resumption of student loan payments should be beneficial to FirstCash, as the U.S. Pawn business contributed $153 million in operating income in H1/23 compared to $49 million for LTO Payments (Figure 10)

{kind=link}

Figure 10 - Pawn contributes more to business than LTO payments (FCFS 10Q report)

Valuation Remains Elevated

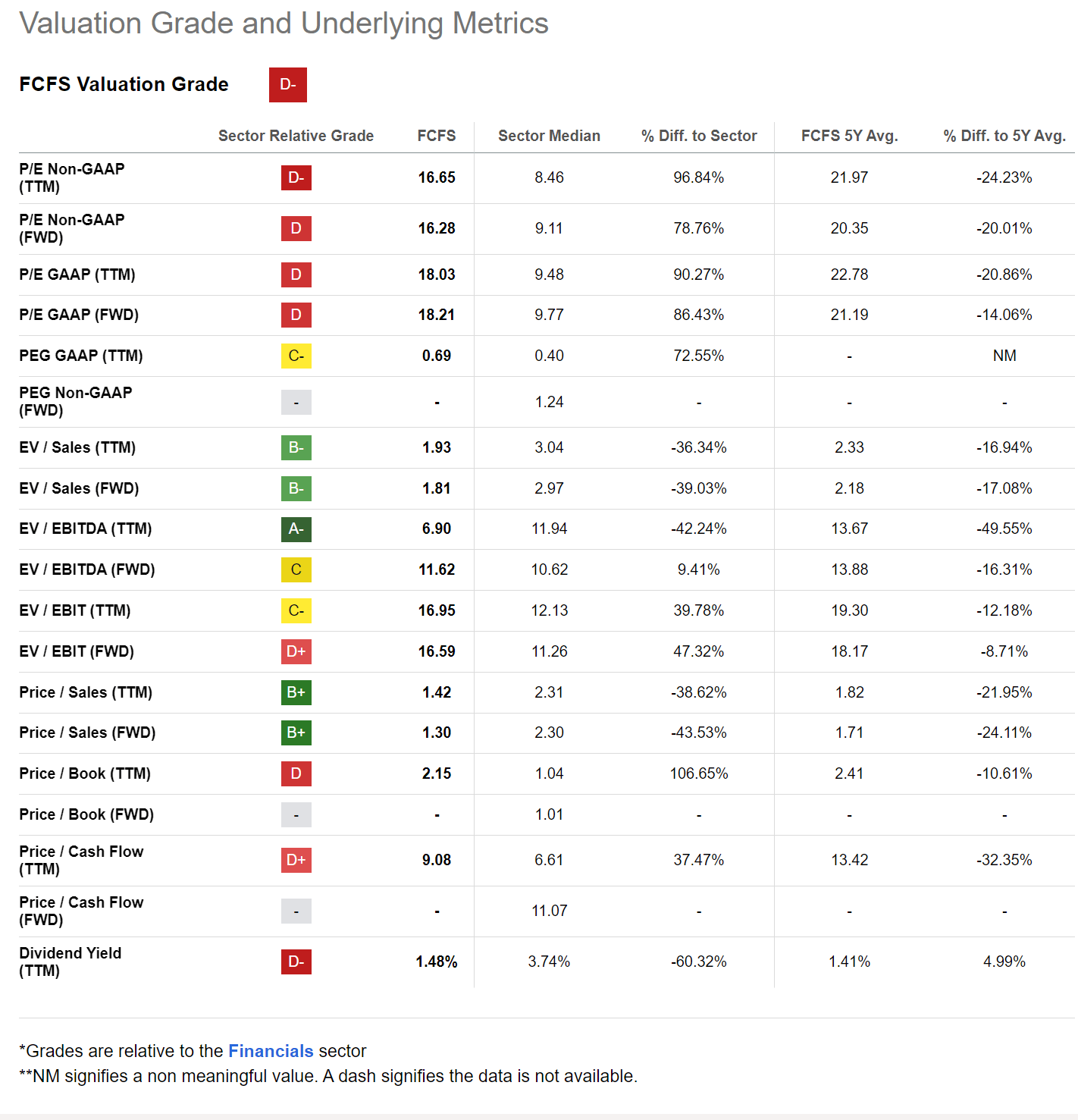

After last year's rally, FirstCash continues to trade at elevated valuations of 16.3x Fwd Non-GAAP P/E vs. 9.1x for the sector (Figure 11).

{kind=link}

Figure 11 - FCFS trades at elevated valuation multiples (Seeking Alpha)

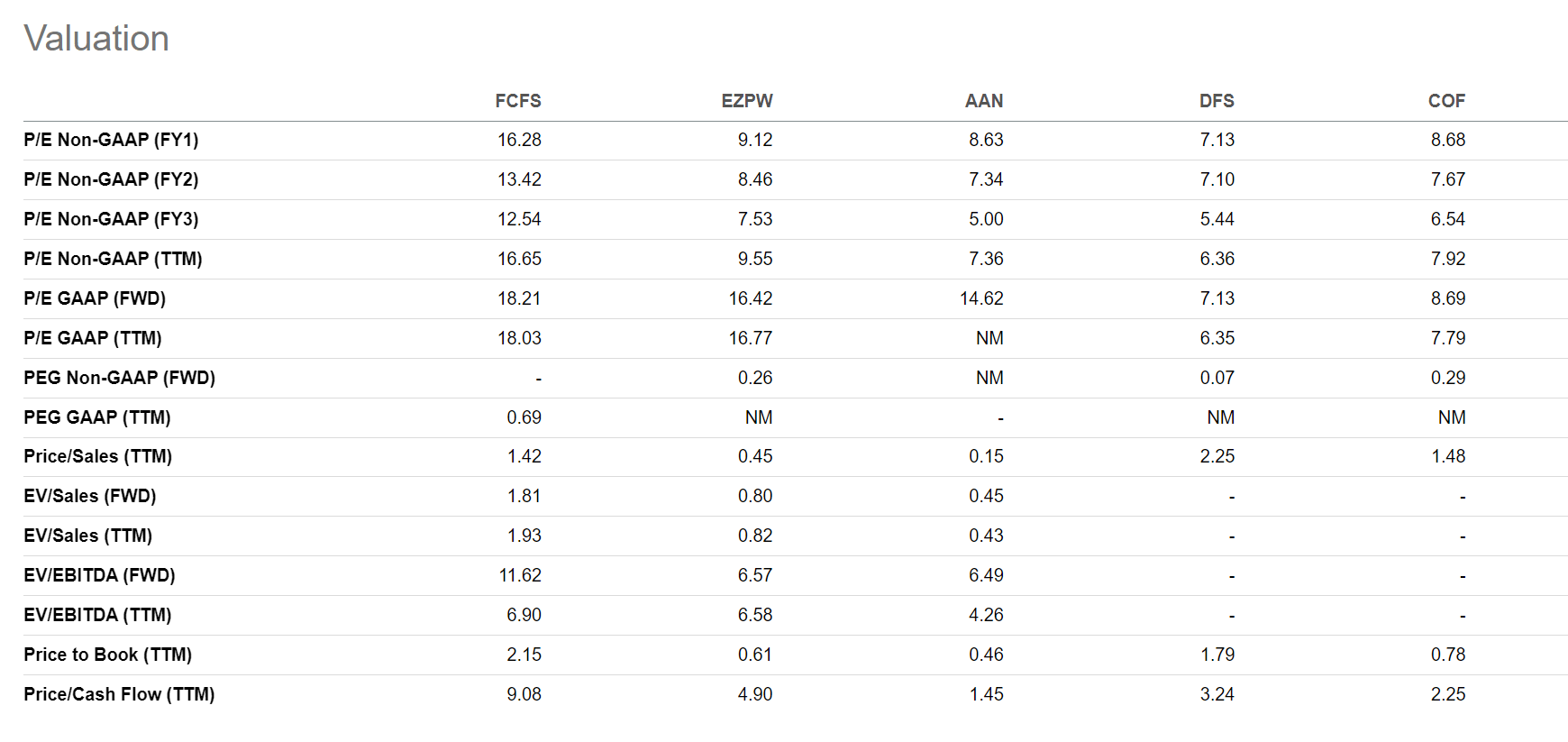

Relative to peers, we can see that FCFS's 16.3x Fwd P/E is trading at a large premium compared to pawn pureplay EZPW (9.1x), LTO peer AAN (7.3x), and consumer credit peers DFS (7.1x) and COF (8.7x) (Figure 12).

{kind=link}

Figure 12 - FCFS is trading at a big premium to peers (Seeking Alpha)

Conclusion

Although I like FirstCash's countercyclical pawn business, I remain concerned about potential credit deterioration in the LTO payments business. While a struggling consumer should benefit FCFS on net, the uncertainty regarding ultimate loss ratios in LTO payments leave me on the sideline. Furthermore, with FCFS trading at a large premium to its peers, I am hesitant to recommend its shares as a buy. I maintain my hold recommendation.

For further details see:

FirstCash Holdings: Consumer Delinquencies Creeping Up