FCFS - FirstCash Holdings: Will Credit Continue To Be Benign?

Summary

- FirstCash Holdings is a leading operator of pawn stores in the U.S. and Latin America. Pawn is countercyclical and does well in challenging environments.

- So far, credit conditions have been benign in FCFS's consumer lease-to-own business. However, with major consumer lenders expecting a deterioration in credit, how long can these conditions last?

- FCFS trades at a steep premium compared to pawn, LTO, and consumer lending peers. I suggest investors tread carefully.

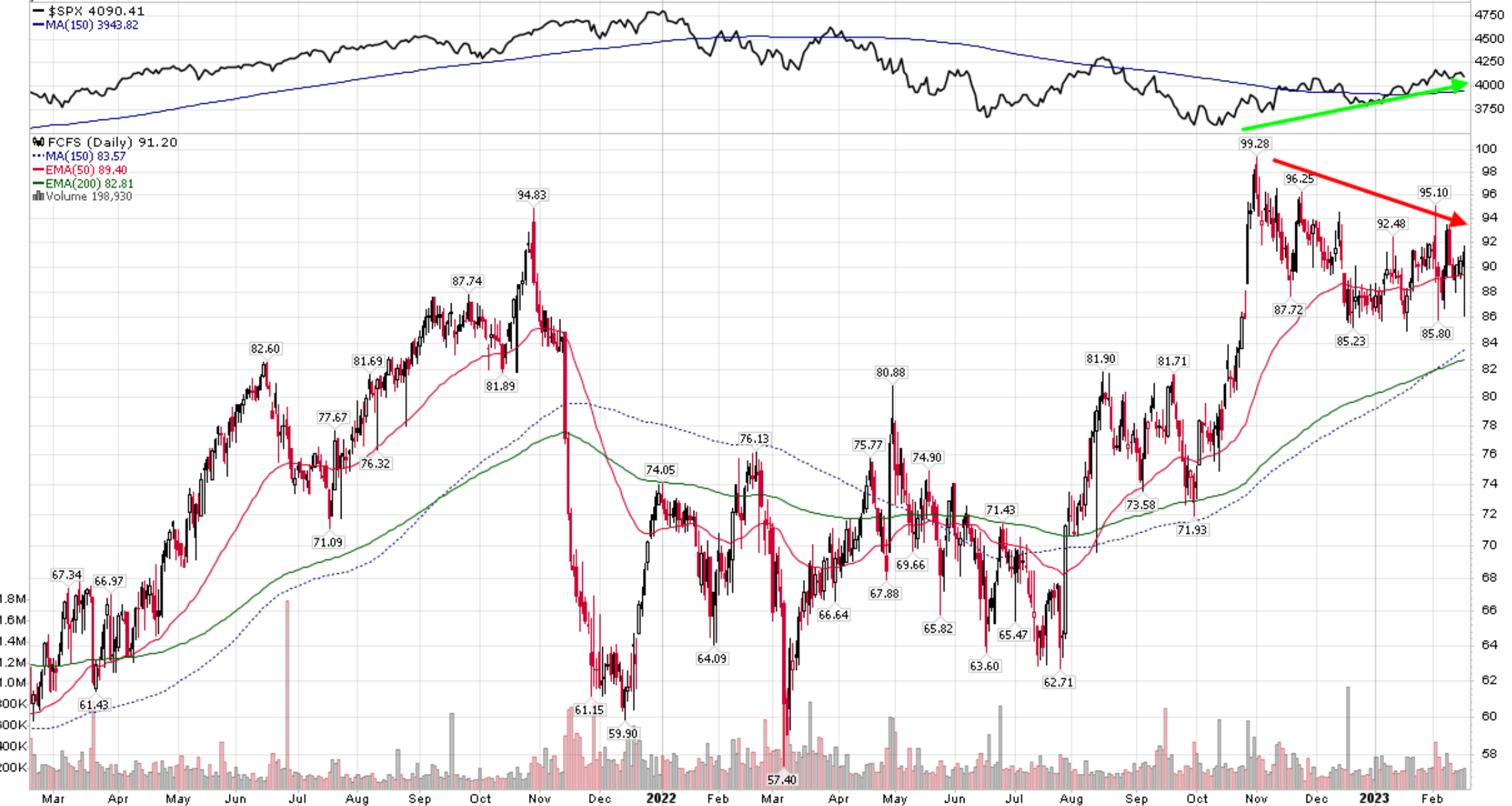

Back in early November, I wrote a cautious article on FirstCash Holdings, Inc. (FCFS), suggesting investors should take profits after a spectacular run in the stock, which saw FCFS reach new all-time highs despite weak equity markets. Subsequent to my article, FirstCash's stock price has stalled, retreating by over 5% while equity markets have rebounded significantly, justifying my caution (Figure 1).

Figure 1 - FCFS stock price has stalled (Author created with price chart from stockcharts.com)

{kind=link}

Recently, the company reported its fiscal fourth quarter results for 2022. Have my thoughts on FCFS changed since my last article?

Strong Fourth Quarter To Close The Year

FirstCash capped off an outstanding year with strong fourth quarter results, as the company reported revenues of $749 million (+49% YoY) and dil. EPS of $1.72 (+143% YoY) (Figure 2).

Figure 2 - FCFS Q4/22 financial summary (FCFS Q4/22 earnings release)

{kind=link}

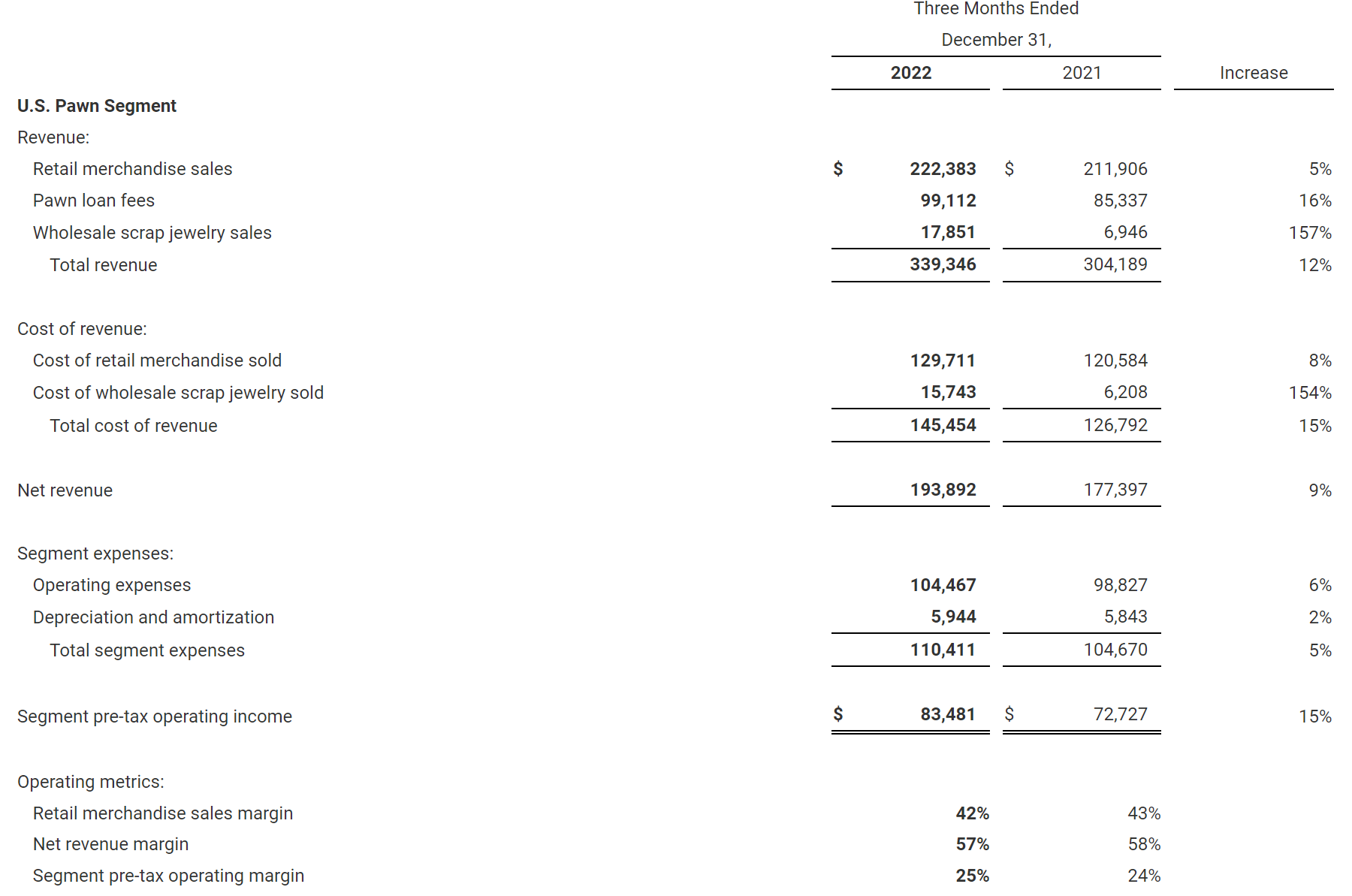

Operationally, FCFS's U.S. Pawn segment performed well, with pawn loans outstanding ("PLO") growing 10% YoY to $282 million and operating income growing even faster at 15% YoY to $83 million (Figure 3).

Figure 3 - FCFS U.S. pawn business performed well (FCFS Q4/22 earnings release)

{kind=link}

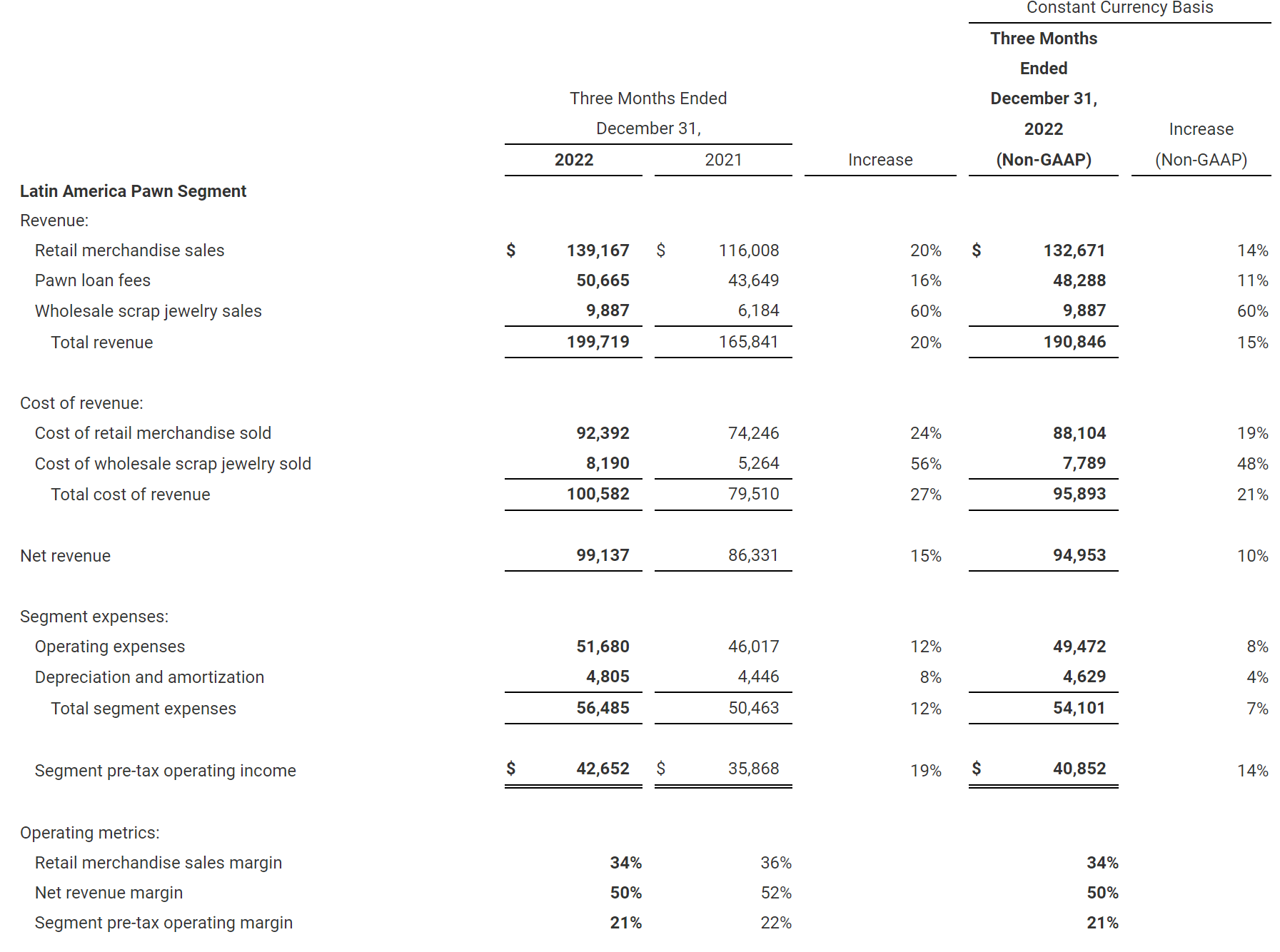

However, the Latin American operations appear to have slowed down a bit due to seasonality. Although PLO grew 18% YoY to $109 million, it actually declined 13% QoQ from $125 million last quarter. However, operating income still grew 19% YoY to $43 million vs. $37 million in Q3 (Figure 4).

Figure 4 - FCFS Latin American pawn business slowed down in Q4 (FCFS Q4/22 earnings release)

{kind=link}

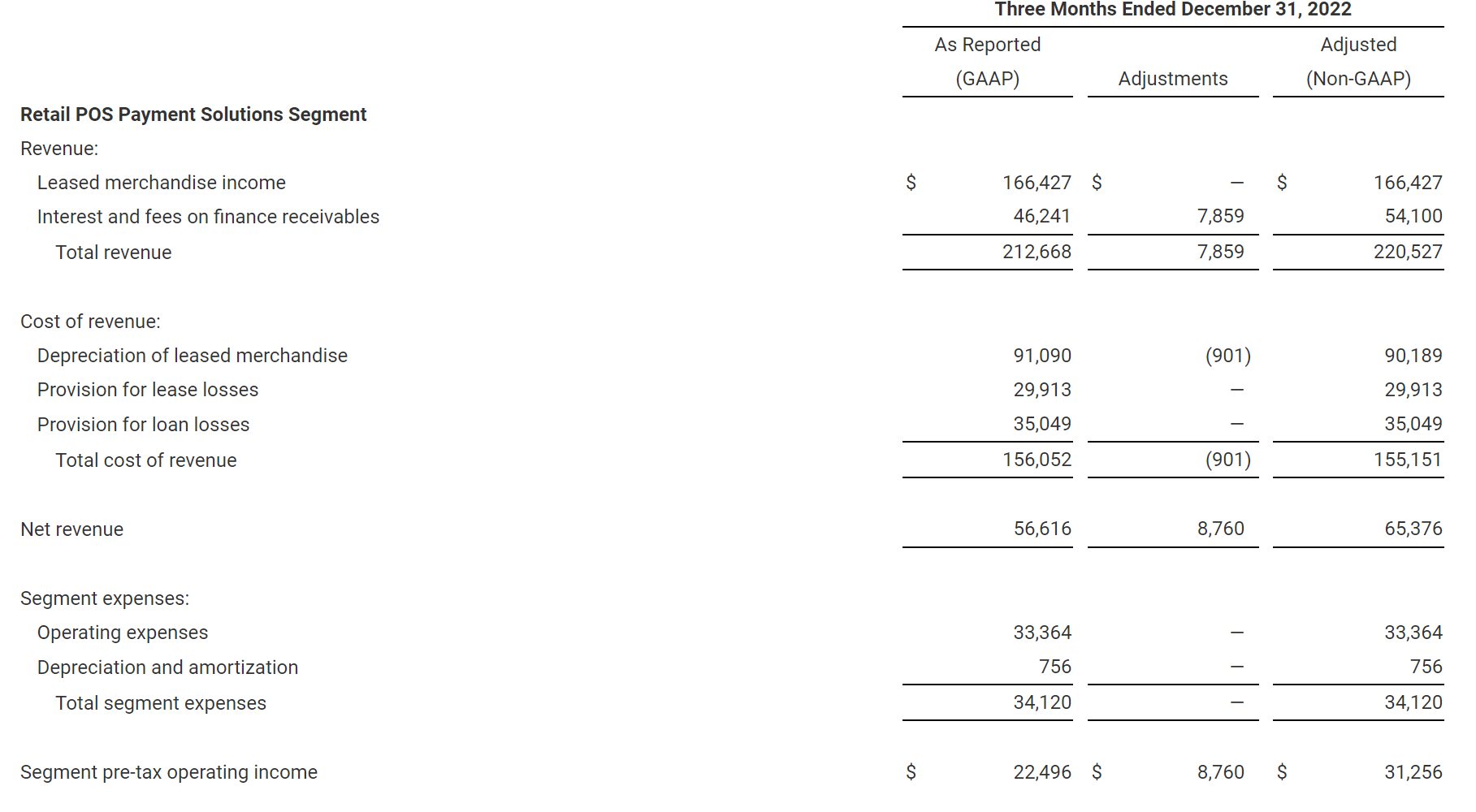

Finally, FCFS's Retail POS payment solutions business, America First Finance ("AFF"), saw adj. revenues of $221 million and adj. operating income of $31 million vs. $214 million in adj. revenues and $28 million in adj. operating income in Q3 (Figure 5).

Figure 5 - FCFS Retail POS payment solutions business performed well (FCFS Q4/22 earnings release)

{kind=link}

Importantly, provision for loan and lease losses at AFF were $65 million or 29.5% of adjusted revenues in Q4, better than the full year run-rate of 30.6%, suggesting benign credit conditions despite economists calling for a recession.

Credit Has Been Performing Far Better Than Expected

To be honest, AFF's consumer credit has performed far better than expected in the last few months despite deteriorating credit conditions in the rest of the economy. For example, when the big 4 American money-center banks (JPM, BAC, C, WFC) reported their fiscal 2022 fourth quarters, the banks collectively set aside $5.4 billion in provisions for credit losses in their consumer divisions, a 64% QoQ increase (Figure 6).

Figure 6 - Q4/22 Consumer Provision for Credit Losses at JPM, BAC, C, and WFC (Author created with data from the companies' respective Q4/22 earnings releases)

AFF, with higher exposure to low-income/poor-credit history consumers, should theoretically have experienced worse credit loss trends than the big banks, not an improvement in credit losses.

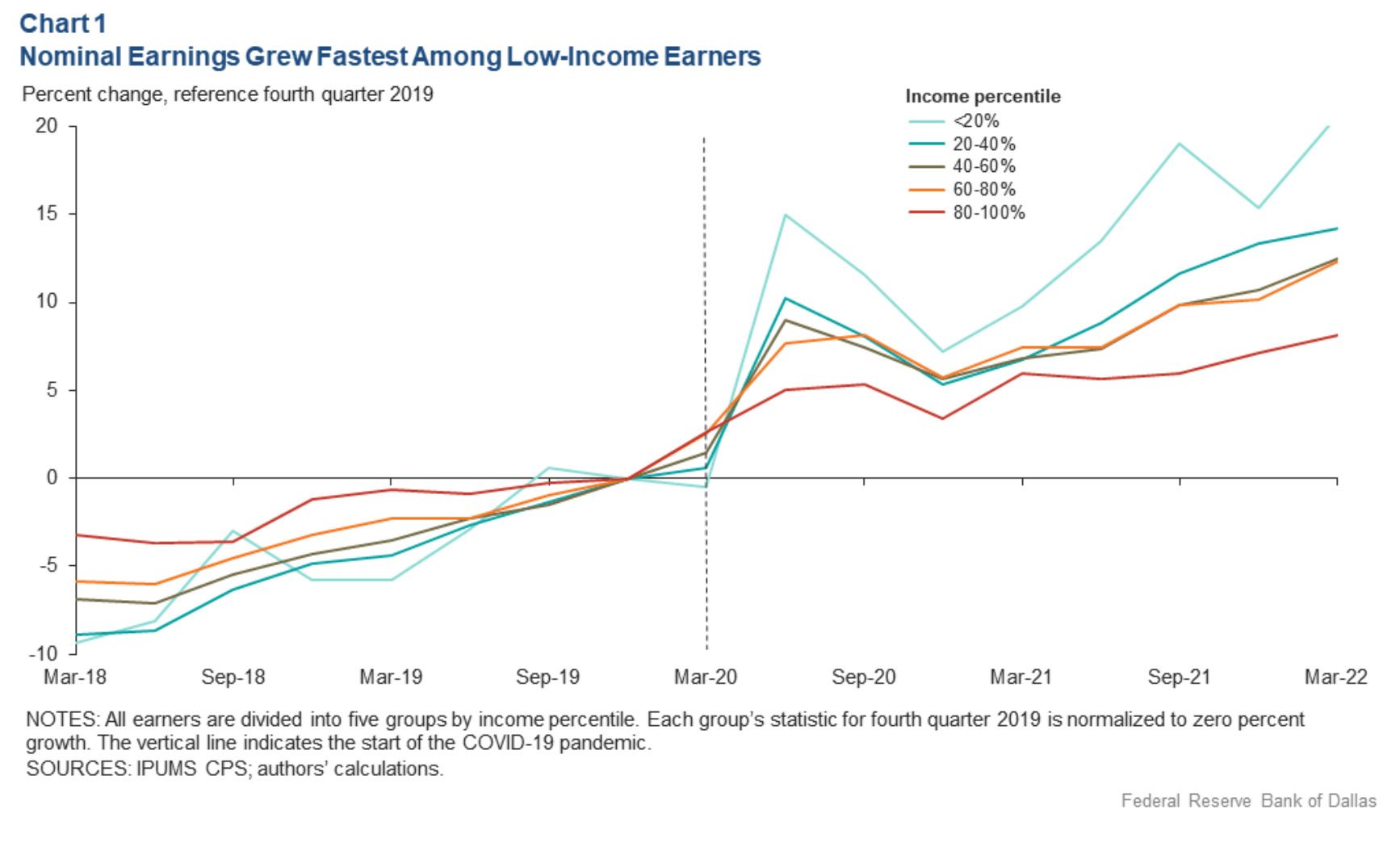

One potential explanation for the unexpectedly strong credit performance of AFF's portfolio is the extremely tight labor market, especially for blue-collar unskilled jobs. Tight labor markets have allowed nominal earnings for low-income workers to grow at the fastest pace in the past few quarters, according to the Dallas Fed (Figure 7).

Figure 7 - Low-income workers have seen fastest income growth (Dallas Fed)

{kind=link}

With plentiful jobs and rising incomes, the low-income/poor-credit history consumers that AFF serve may actually be flush with cash flow and thus have been able to service their lease-to-own ("LTO") obligations.

Will Credit Continue To Be Benign?

The key question for investors is whether these benign credit conditions will persist into 2023 and beyond? FCFS's management certainly believe so, as they are forecasting "year-over-year growth in gross transaction volumes of 8% to 12% in 2023, primarily from increased merchant door counts, which should result in similar expected growth in revenues for 2023." With respect to credit, FCFS expects "estimated lease and loan loss provisioning rates for 2023 to remain consistent with 2022".

I continue to have a more cautious view, as I do not believe a wave of rising consumer credit delinquencies and defaults will spare AFF's low-income / poor credit history customers. Already, we are seeing credit card issuers like Discover Financial Services ( DFS ) guiding to a doubling of net charge off rates from 1.82% in 2022 to 3.5-3.9% in 2023. I think it is only a matter of time before AFF experiences significantly higher delinquencies and defaults.

Pawn Expected To Drive Growth In 2023

On the pawn operations, FCFS continues to see pawn as the largest driver of revenues and earnings in 2023, as "inflationary economic environments have historically driven increased customer demand for both pawn loans and value priced merchandise offered in pawn stores. In addition, credit tightening from competing unsecured lenders has historically driven additional demand for pawn products."

I believe it is inconsistent for management to expect the pawn business to continue to grow due to inflationary pressures on FCFS's customers, while at the same time expecting no deterioration in credit performance on the LTO leasing business.

Either pawn is going to grow significantly due to macroeconomic pressures on consumers, in which case AFF's low-income customers should also suffer; or labor markets will remain tight, supporting benign credit losses, in which case the pawn business should not see strong demand growth.

Valuation Remains Elevated

After the 2022 rally, FirstCash's valuation remains quite elevated, with the shares trading at 15.3x Fwd P/E vs. 9.9x for the sector (Figure 8).

{kind=link}

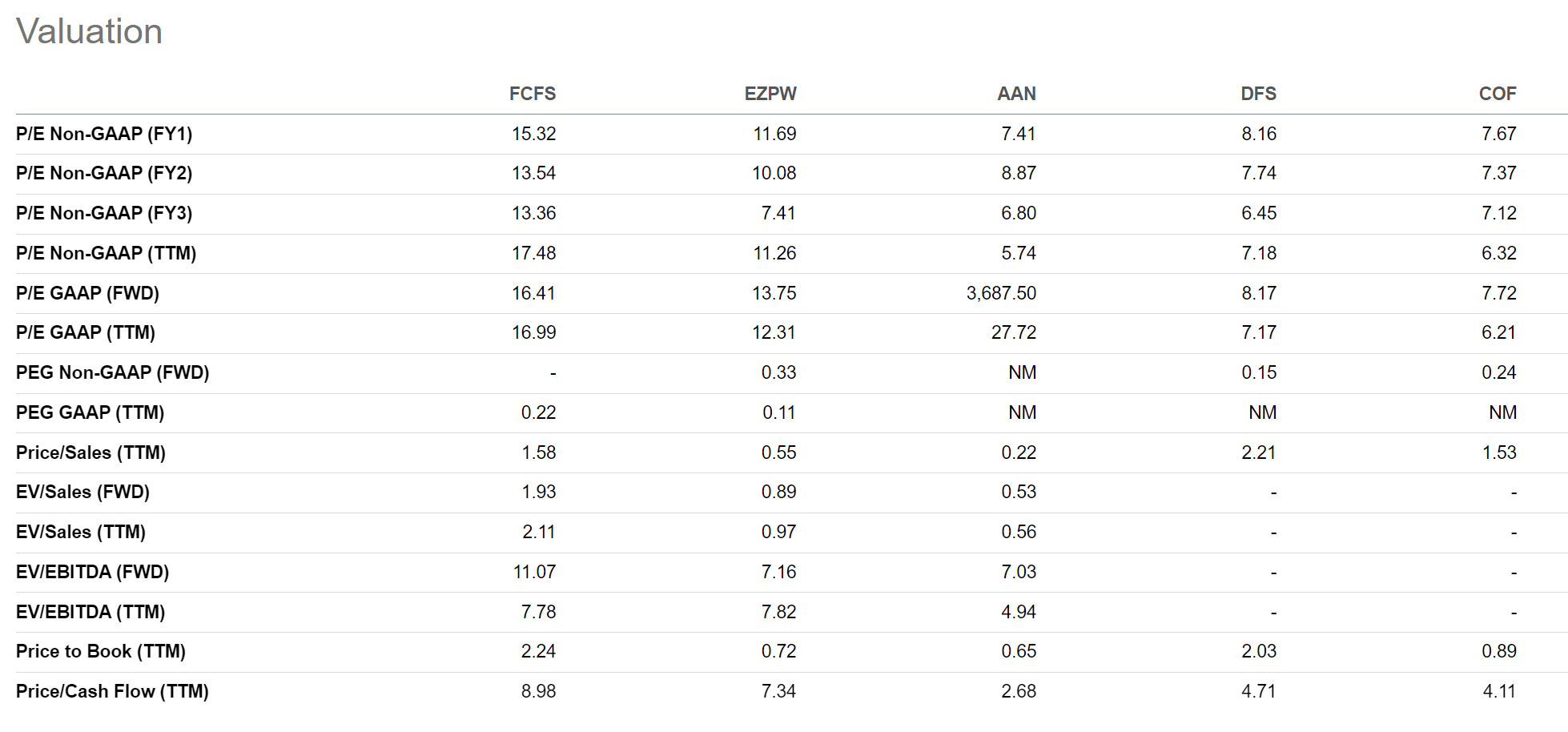

FCFS's valuation premium is especially pronounced when viewed against pure-play pawn operators like EZCORP, Inc. ( EZPW ) which trades at only 11.7x Fwd P/E. Alternatively, we can compare FCFS to a LTO peer, The Aaron's Company ( AAN ), which trades at 7.4x Fwd P/E or consumer lending peers Discover Financial Services ( DFS ) and Capital One Financial ( COF ) which trade at 8.2x and 7.7x Fwd P/E respectively (Figure 9).

{kind=link}

AAN, DFS, and COF are likely pricing in a broad deterioration in credit, which explains their discounted valuation.

Conclusion

While I continue to like FirstCash's countercyclical pawn business, I remain concerned about potential credit deteriorations in FCFS's LTO business. Management's expectation for continued growth in the pawn business is inconsistent with benign credit expectations in the LTO business. FCFS continues to trade at a significant premium to pawn, LTO, and consumer lending peers, which makes me hesitant to recommend its shares.

For further details see:

FirstCash Holdings: Will Credit Continue To Be Benign?