DUKB - FirstEnergy: A Few Positives But Some Concerns

Summary

- FirstEnergy is a major electric utility serving much of the mid-Atlantic region.

- The company is positioned to deliver solid total returns over the next few years, although it would be nice to have more visibility than the company has provided.

- The company's debt load is a bit high and it has some large maturities in the few years that could prove a drag on earnings as it rolls them over.

- The company can sustain its 3.65% yield, although the lack of dividend growth is rather irritating.

- The company is quite attractively priced right now so might be worth buying despite the problems.

FirstEnergy Corp. ( FE ) is a large regulated electric utility that serves customers in several Mid-Atlantic states. The utility sector has long been one of the more popular ones among conservative investors due to its relatively stable cash flows and high yields. FirstEnergy is no exception to this as it boasts a 3.65% yield as of the time of writing and has generally consistent cash flow. It has not been quite as popular with investors as several of its peers though and as a result, the company has one of the more attractive valuations in the sector. This is something that could prove quite appealing to someone buying today, particularly given FirstEnergy's respectable forward earnings growth. The company is not without risks though as its balance sheet is a bit weaker than some of its peers but it is still not altogether unreasonable. Overall, there might be some reasons to consider an investment in FirstEnergy today.

About FirstEnergy Corp.

As stated in the introduction, FirstEnergy Corp. is a regulated electric utility that serves customers in Ohio, Pennsylvania, Maryland, West Virginia, Virginia, New Jersey, and New York.

FirstEnergy Corp.

Several parts of this service area are among the most populated in the United States and FirstEnergy boasts more than six million customers in its service territory. This makes the company one of the largest utilities in the United States. However, there are not a great many differences between the characteristics of large and small utilities. The most important characteristic of these companies is that they tend to enjoy remarkably stable cash flows. This is due to the nature of the product that they provide. As most people consider electric service at their home or business to be a necessity, they will typically prioritize paying their utility bill over discretionary expenses during times when money gets tight, such as during a recession. This is something that could prove to be very important today given the widespread expectation that the United States will enter into a recession during 2023. This is a characteristic that is shared by FirstEnergy as we can see by looking at its operating cash flows. Here they are for the past eleven quarters:

{kind=link}

Admittedly, there are more fluctuations here than we would normally expect to see from an electric utility. However, we can balance them out over time to reduce the impact of payment timings, changes in commodity prices, and other things. Here are the company's operating cash flows over the same period, but using the trailing twelve-month figures:

{kind=link}

Here we can see a great deal of stability regardless of economic problems. We do see some weakness in 2020 though, but this is not entirely unexpected. As everyone reading this can certainly remember, many states implemented lockdown orders during the Spring of 2020 that required their citizens to remain at home and curtail unnecessary traveling. More importantly, businesses were told to shut down and employees were told to work from home. As a result of this, there was far less electricity being consumed by the commercial and industrial sectors than during normal times. We also had a substantial number of people left unemployed and unable to pay their electric bills. These two factors resulted in FirstEnergy Corp. receiving less money than normal during 2020 and early 2021. These problems have largely been resolved now, though.

We can still see that FirstEnergy managed to weather the pandemic without a huge amount of damage to its operating cash flows. This is something that could prove appealing today as the economy is widely expected to enter into a recession sometime during 2023. It is uncertain exactly how deep and severe the recession will be but it seems likely that it will not be nearly as bad as the one that was caused by the lockdowns in 2020. A recession will impact those companies that depend on discretionary spending much more than they will a utility, as we can clearly see from FirstEnergy's performance. This helps the company's investment case since it would generally make more sense to be invested in a firm that is likely to be able to maintain its financial strength through such an event.

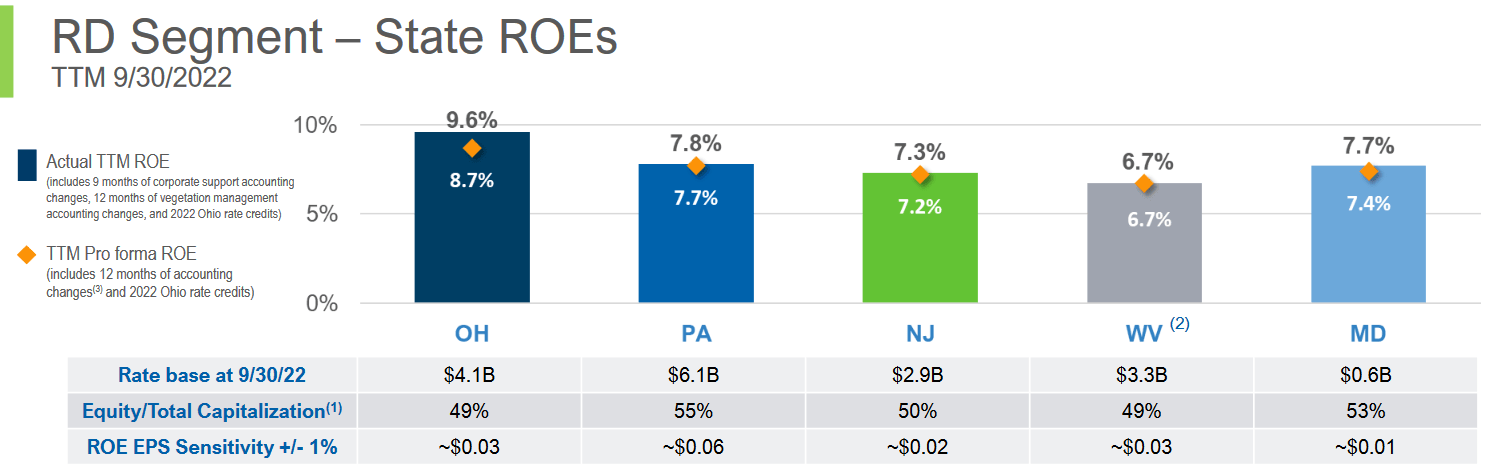

As investors, we are naturally interested in much more than simple stability, though. We also desire growth. Fortunately, FirstEnergy is likely to deliver this going forward. The primary way that it will do this is by growing its rate base. The rate base is the value of a utility company's assets upon which regulators allow the company to earn a specified rate of return. This rate of return is usually around 10%, although several of the states that FirstEnergy operates in have a lower allowed rate of return:

{kind=link}

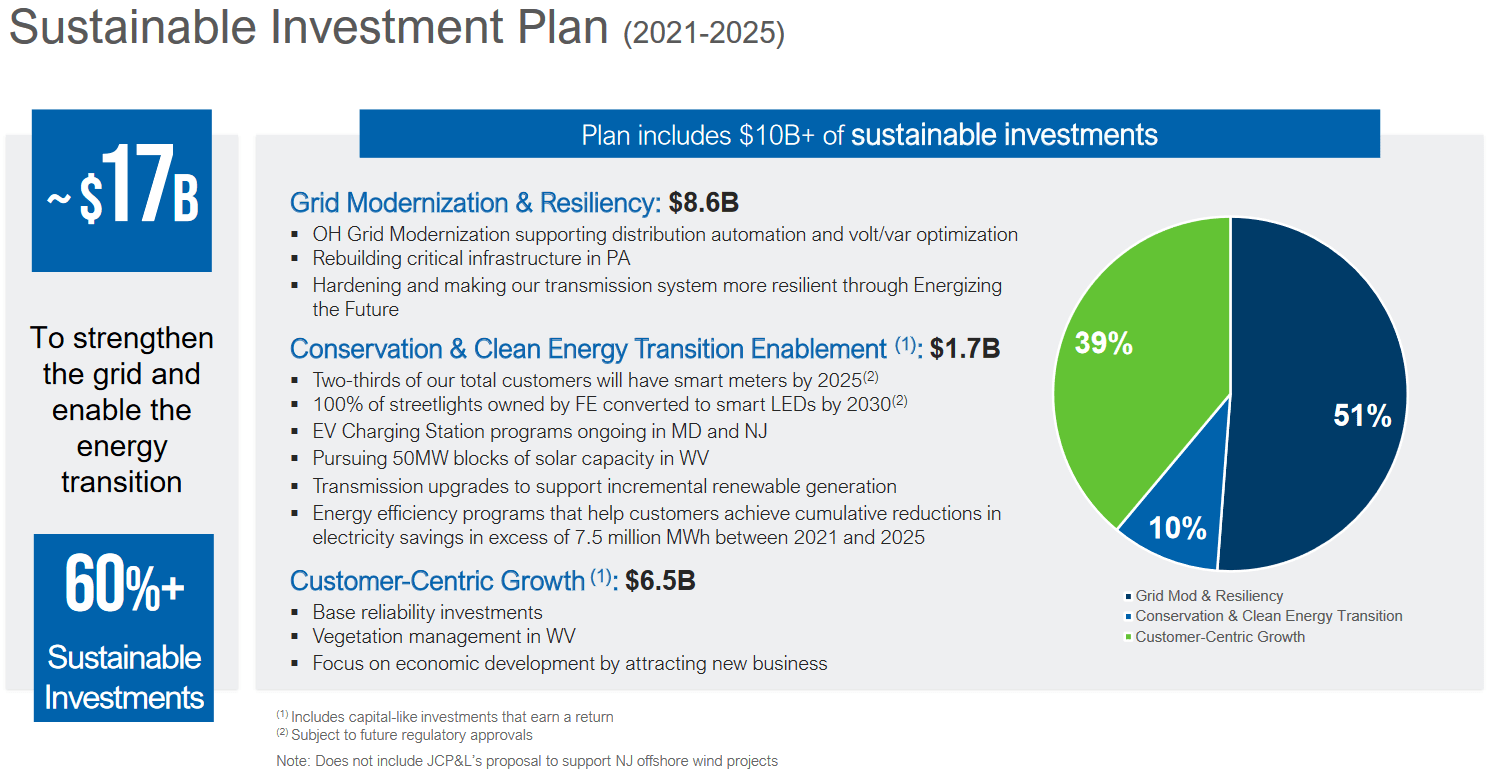

This is rather disappointing as it does mean that FirstEnergy is not as profitable as it would be if it operated in several other states around the country. However, our overall thesis does still work. The fact that the allowed rate of return is a percentage means that any increase in the size of the rate base will allow FirstEnergy to increase the price that it charges its customers in order to earn that allowed rate of return. The usual way that a utility company will grow its rate base is by investing money into upgrading, modernizing, or even expanding its utility-grade infrastructure. FirstEnergy is planning to do exactly this as the company is currently planning to invest $17 billion over the 2021 to 2025 period in order to increase its rate base:

{kind=link}

This is a very different time period than what is in the plans that FirstEnergy's peers have presented and I will admit that it is a bit disappointing. We do not care that much about what the company did back in 2021 as that is already reflected in the company's earnings and stock price. At this point, even 2022 is not really relevant, although most peers are presenting this. I would like to see the company's plans for the 2023 to 2027 period during its next earnings release but I somewhat doubt that FirstEnergy will actually present this. The company will likely represent this plan, which will already be a few years old. That is disappointing from an investment perspective and shows a lack of shareholder friendliness.

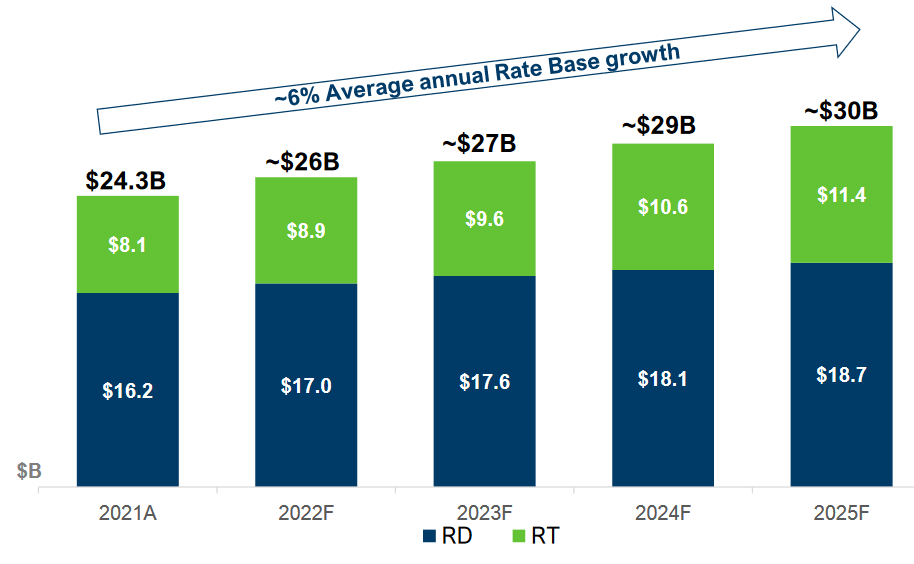

Despite the company's presented plan not covering the time frame that we really want, we can still see that it should result in growth. In particular, the company should be able to grow its rate base from $24.3 billion at the end of 2021 to $30 billion by the end of 2025:

{kind=link}

We can see above that the company's rate base should be approximately $26 billion today but FirstEnergy has not released its final numbers yet (that should be in a few weeks). The company's plan should grow its rate base at about a 6% compound annual growth rate over the period, which is admittedly a bit less than some of its peers but it is not substantially below the industry average. The biggest thing that we will likely see here though is that the company's rate base is only expected to increase by $5.7 billion despite FirstEnergy spending $17 billion on this program. The biggest reason for this is that some of the company's spending will be on replacement assets, with the original ones being retired. These retired assets will have their value removed from the company's rate base, offsetting the impact of some of the spending. A more important factor though is depreciation, which constantly reduces the value of the company's assets. For example, something put into service during 2021 will have a lesser value for the purposes of calculating the rate base by 2025. The company's spending, therefore, needs to be sufficient to both overcome the impact of depreciation and still increase the value of the assets that are actively in service.

The growth in the rate base should be sufficient to grow FirstEnergy's earnings per share by 6% to 8% annually. When we combine this with the company's 3.65% dividend yield, that should result in a 10% to 12% total average annual return. That is actually quite a bit higher than most of the company's peers and when we combine this with the fact that the company has a somewhat lower valuation than many of its peers, which we will see later in this article, FirstEnergy should be fairly well positioned to deliver outsized returns to its investors.

Unfortunately, FirstEnergy has not shown that growth potential so far this year. In the first three quarters of 2022, FirstEnergy reported earnings of $1.42 per share compared to $1.57 per share in the prior year period. One of the biggest reasons for this is that the company incurred $0.22 per share of debt-related costs, likely due to it repaying $2.5 billion worth of debt in an effort to strengthen its balance sheet. This was a smart move despite the negative impact that it had on the company's earnings due to the rising interest rate environment that makes rolling debt over much more expensive than a year ago and the fact that the company generally has a weaker balance sheet than its peers, as we will see shortly. The company's weaker earnings performance this year does little to change the long-term growth thesis that we just discussed, however.

Financial Considerations

It is always important to analyze a company's financial structure before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. As this is normally accomplished by issuing new debt and using the proceeds to repay the maturing debt, a company's interest expenses may increase following the rollover depending on the conditions in the market. In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flows to decline could push it into financial distress if it has too much debt. Although utilities tend to have remarkably stable cash flows, bankruptcies have occurred in the sector. Indeed, a subsidiary of FirstEnergy itself went into bankruptcy protection back in 2018. Therefore, despite the generally stable cash flows, this is a risk that we should not ignore.

One metric that we can use to analyze a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of September 30, 2022, FirstEnergy had a net debt of $21.007 billion compared to $11.238 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 1.87. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| FirstEnergy Corp. |

| 1.87 |

| Exelon Corporation ( EXC ) |

| 1.55 |

| Entergy Corporation ( ETR ) |

| 2.14 |

| Eversource Energy ( ES ) |

| 1.41 |

| Duke Energy ( DUK ) |

| 1.40 |

As we can clearly see, FirstEnergy is not the most levered company on this list but it is still generally higher than most of its peers. This is a sign that the company may be relying too much on debt to finance its operations and thus may be at greater risk of financial distress than its less levered peers. This is a risk that potential investors should consider before making an investment in the firm.

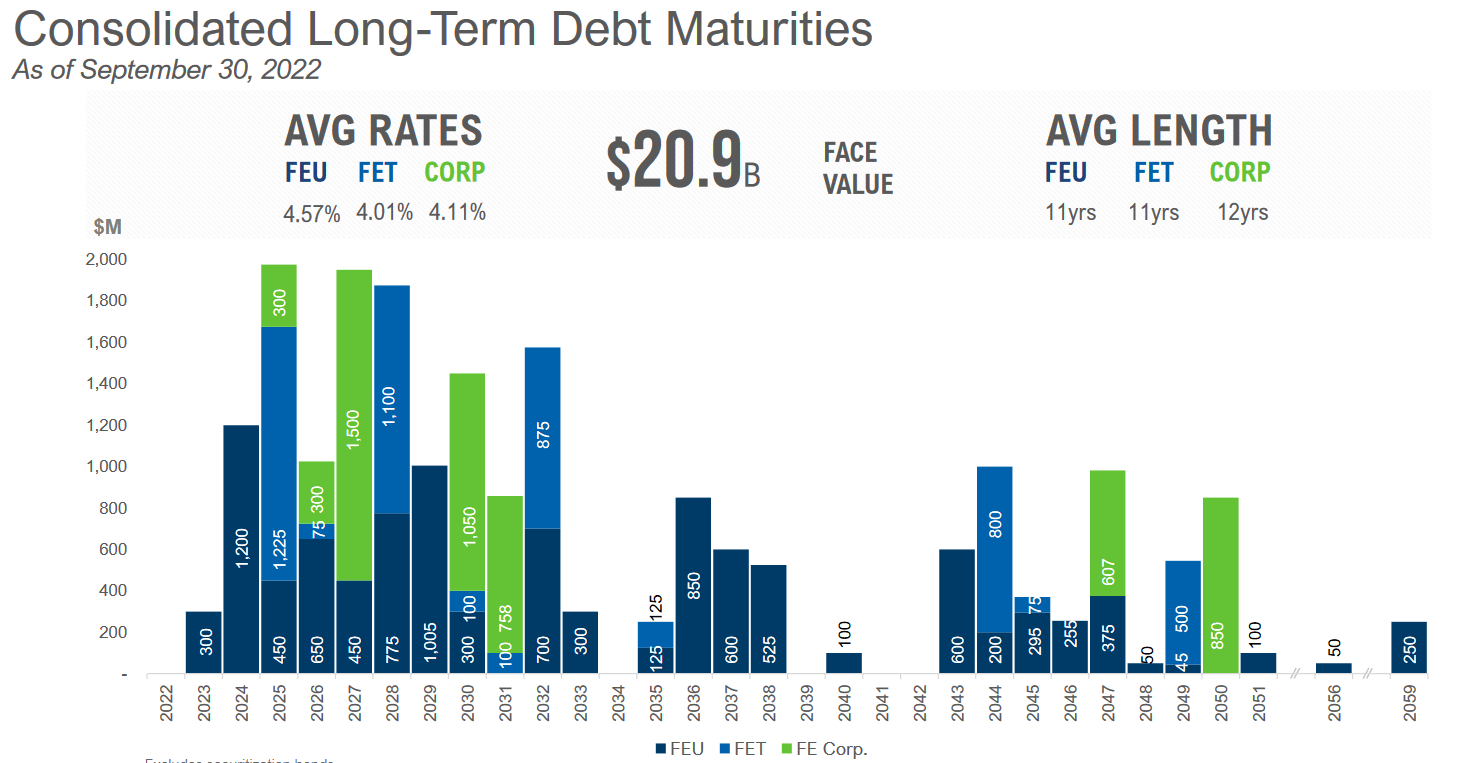

Fortunately, FirstEnergy has very limited debt maturities in 2023. We can see that here:

{kind=link}

We do, however, see that the company has a substantial amount of debt maturing in 2024 and 2025. This is something that could pose an issue because of the fact that the company may be forced to pay a higher interest rate when it rolls over this debt. This is not a huge concern in 2023 because the amount of debt that needs to be refinanced is very low. However, FirstEnergy could see its interest expenses increase in 2024 and 2025 when it has to refinance the maturing debt in those years. We admittedly do not know what interest rates will be in those years. The market is currently expecting the Federal Reserve to pivot sometime in 2023 and begin cutting rates again but I am not nearly as confident of this view. In fact, I would not be surprised if we see rates remain above 5% for the next few years. Thus, we may have a situation in which FirstEnergy will see higher interest costs going forward, which will act as a drag on its earnings per share growth.

Dividend Analysis

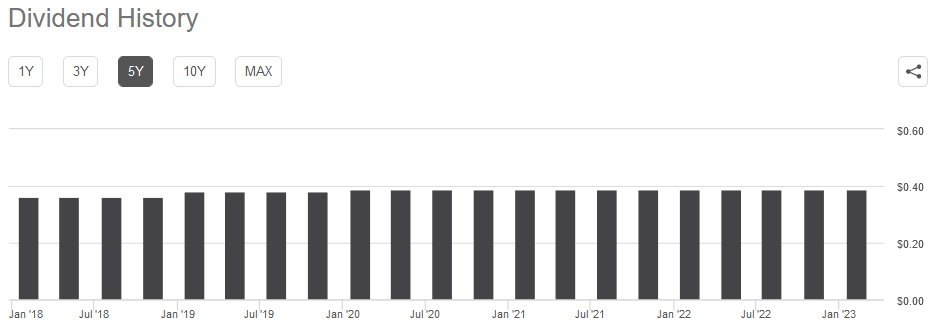

As stated in the introduction, one of the reasons that investors purchase shares of utility companies like FirstEnergy is because of the high dividend yields that these companies tend to possess. The reason for these yields is that utilities tend to be fairly low-growth entities so they aim to deliver a significant proportion of their total return to investors via direct payments. In addition to this, the low growth means that these companies' stocks are not as richly valued as many other companies so the dividend is a higher percentage of the share price. FirstEnergy is no exception to this high yield characteristic as the company currently boasts a 3.65% yield, which is quite a bit higher than the 2.36% yield of the U.S. Utilities Index ( IDU ). Unfortunately, FirstEnergy has not been nearly as good as its peers in terms of dividend growth. The company has actually kept its dividend flat since early 2020:

{kind=link}

The lack of dividend growth is quite disappointing during inflationary times, such as today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. Thus, it can feel as if we are getting poorer and poorer over time. The lack of growth does not help matters any since we need to reinvest the dividends in order to get more money from the company and that may not be possible for a retiree that is depending on their portfolio income to pay the bills. Although the company is generally holding the dividend flat in order to focus on strengthening its balance sheet, it is still something that makes FirstEnergy a second-drawer choice as far as utilities are concerned. It is still important to ensure that the company can actually afford the dividend that it pays out though since we do not want to have a situation in which it is forced to cut the payment and leave us with a lower income.

The usual way that we judge a company's ability to afford its dividend is by looking at its free cash flow. The free cash flow is the amount of money that is generated by a company's ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that is available for such purposes as reducing debt, buying back stock, or paying a dividend. During the third quarter of 2022, FirstEnergy had a levered free cash flow of $66.6 million. It is actually pretty rare for a utility to have a positive free cash flow during any period so this is something that is fairly nice to see. Unfortunately, it was not nearly enough to cover the $222.0 million that the company paid out in dividends during the quarter. At first glance, this could be quite concerning.

However, it is fairly typical for a utility to pay for its capital expenditures through the issuance of equity and debt while financing its dividend out of operating cash flow. This is mostly due to the incredibly high costs involved with constructing and maintaining utility-grade infrastructure over a wide geographic region. During the third quarter of 2022, FirstEnergy had an operating cash flow of $554.0 million. This is easily enough to cover the $222.0 million in total dividends that FirstEnergy pays out with a significant amount of money left over for other purposes. Overall, the company probably can maintain its dividend although I would still like to see some dividend growth. The company does actually have some room for said growth.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. One metric that we can use to value a utility like FirstEnergy is the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings growth ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that a stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few stocks that have such a low ratio in today's richly-valued market. This is particularly true in the low-growth utility sector. As such, the best way to use this metric is to compare FirstEnergy's valuation against those of its peer group in order to determine which company offers the most attractive relative valuation.

According to Zacks Investment Research, FirstEnergy will grow its earnings per share at a 6.45% rate over the next three to five years. This is in line with the 6% to 8% that we calculated earlier in this article so this estimate seems pretty reasonable. This gives FirstEnergy a price-to-earnings ratio of 2.67 at the current stock price. Here is how that compares to the company's peer group:

| Company |

| PEG Ratio |

| FirstEnergy Corp. |

| 2.67 |

| Exelon Corporation |

| 2.61 |

| Entergy Corporation |

| 2.63 |

| Eversource Energy |

| 2.95 |

| Duke Energy |

| 3.40 |

As we can see here, FirstEnergy's valuation is comparable to many of its peers, although it is still quite a lot cheaper than Eversource Energy and Duke Energy. As readers of my previous articles know, we frequently see utilities trading at price-to-earnings growth ratios above 3.0 right now so FirstEnergy is very reasonably valued compared to the industry as a whole. For the purposes of this comparison, I only opted to use some of the utilities that are somewhat comparable in size. Overall, the price here is quite reasonable, which is probably due to the risks surrounding FirstEnergy's debt load and the less attractive dividend history relative to the peer sector.

Conclusion

In conclusion, FirstEnergy does have a few things to attract investors to it. In particular, the company's impressive total return potential is difficult to ignore. However, it does have some risks surrounding it as it does have some near-term debt maturities and a somewhat weaker balance sheet than some of its peers. The company's lack of any significant dividend growth is also a major strike against it, particularly given today's inflationary environment. The price is reasonably attractive due to these problems though and thus it could still be worth a cautious purchase.

For further details see:

FirstEnergy: A Few Positives But Some Concerns