FE - FirstEnergy: Attractive Valuation But Higher Risks Than Peers

2023-06-16 13:52:30 ET

Summary

- FirstEnergy Corporation is a regulated electric utility that serves much of the Appalachian Basin.

- The company was affected more by the pandemic-related lockdowns than some of its peers, but it does still enjoy the stability that we typically appreciate.

- The company is positioned to deliver a 10% to 12% average total return to its shareholders over the next two years.

- The company's leverage is a bit higher than its peers, which unfortunately gives it a bit more risk than some other companies.

- FirstEnergy Corp. has a reasonably attractive valuation at the current price.

FirstEnergy Corporation ( FE ) is a regulated electric utility that serves a significant portion of the Appalachian region of the United States. The utility sector in general has long been a favorite among conservative risk-averse investors, such as retirees. There are some good reasons for this, as electric utilities typically have remarkably stable cash flows and a great deal of resistance to economic shocks.

FirstEnergy Corporation is not an outlier here, as it, too, enjoys these characteristics, despite the fact that it did have a bankruptcy several years ago that has somewhat tarred its image among certain investors. The company also has an attractive 3.99% dividend yield and an attractive valuation today, so the fact that it had some problems several years ago can probably be overlooked. It does still have a few issues though, which I outlined in my last article on the company. Overall, FirstEnergy might be a bit more risky than some other utilities but its valuation takes this into account.

About FirstEnergy Corporation

As stated in the introduction, FirstEnergy Corporation is a regulated electric utility that serves the states of Ohio, West Virginia, Pennsylvania, New Jersey, and Maryland. This is a somewhat economically depressed region as the decline of the steel industry and American manufacturing, in general, has caused many parts of it to struggle for decades. The region has been experiencing a revival though as Pittsburgh, Pennsylvania has become a hub for both the technology and healthcare industries, and of course, the incredible concentration of wealth in the Washington, D.C. metro area has crept up to parts of Maryland and South Central Pennsylvania.

However, one of the defining characteristics of electric utilities is that they are highly resistant to economic weakness. The revenues and cash flows of these companies do not usually vary by much regardless of macroeconomic events. This is certainly the case with FirstEnergy, which we can clearly see by looking at the company's operating cash flows. Here they are for the past eleven twelve-month periods:

{kind=link}

We can see a bit of a negative impact in the first two periods shown in the chart above. This was caused by the COVID-19 pandemic and the resulting lockdowns. As I mentioned in a previous article on FirstEnergy, the pandemic-related economic shutdowns had a bigger impact on FirstEnergy than on some other utilities. This is due to the fact that FirstEnergy's customers are more likely to be employed in blue-collar professions than we would find in a place like New York City or San Francisco. Although the manufacturing industry is not as dominant as it once was, the presence of the natural gas deposits of the Marcellus shale has created numerous jobs in that sector and other sectors supporting it. Basically, a significant proportion of the jobs in the area are ones that cannot easily be done remotely, which meant that the lockdowns impacted a large percentage of the company's customers, who ultimately fell behind on their electric bills. It seems pretty unlikely that such an event will occur again during our lifetimes, especially considering that the citizens of many areas are unlikely to accept lockdowns as an appropriate pandemic response in the future. FirstEnergy's cash flows have since recovered though and as we can see above, they exhibit a remarkable amount of stability over the past two years or so.

The reason for this general stability over time is that FirstEnergy provides a product that is generally considered to be a necessity for our modern way of life. After all, who among us does not have electric utility service to our homes and businesses? Indeed, how many of us know someone that does not have this service? As such, most people will prioritize paying their utility bills ahead of any discretionary expenses during times when money gets tight. That typically occurs during times when consumers are financially stressed, as they are today . It also occurs during recessions, which many are predicting will occur during the second half of this year. As such, it is a good idea to include some companies in your portfolio that will not be adversely impacted by problems in the broader economy. FirstEnergy certainly appears to fit the bill here.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, it is critical that any company that we are invested in grow and prosper with the passage of time. This is what drives our investment gains, after all. Fortunately, FirstEnergy Corporation is well-positioned to deliver growth to its shareholders over the next few years.

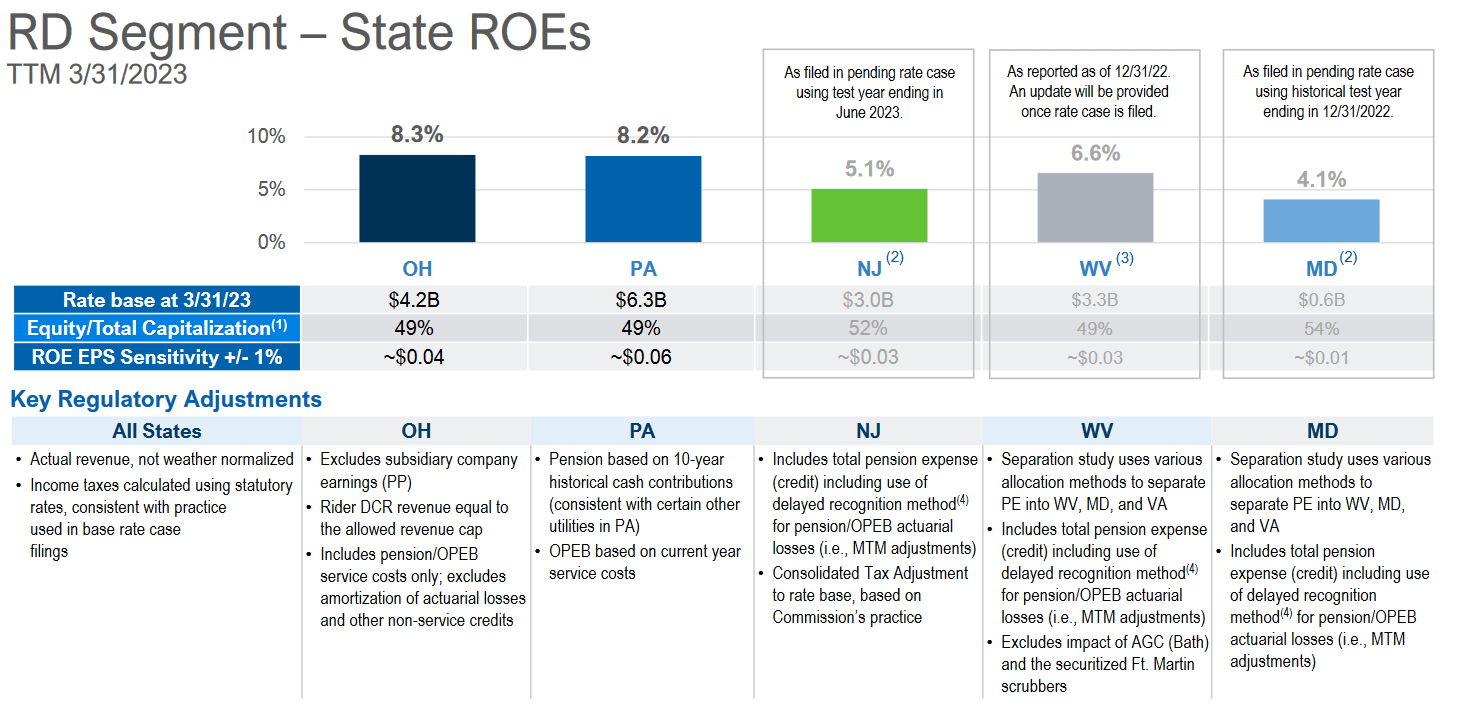

The primary way through which the company will drive growth is by increasing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. The actual allowed rate of return varies by state, but it is usually around 10%. As we can see here, FirstEnergy achieved a 4.1% to 8.3% rate of return in its service territory over the past year:

{kind=link}

As this rate of return is a percentage, any increase to the rate base allows the company to increase the prices that it charges its customers in order to achieve the regulatory-allowed rate. FirstEnergy has filed with regulators in Maryland, New Jersey, and West Virginia to do exactly that as its return on equity in those three states was quite a bit lower than is normally allowed.

The usual way that a utility increases the size of its rate base is by spending money to upgrade, modernize, and possibly even expand its utility-grade infrastructure. FirstEnergy Corporation is planning to do exactly this as the company is currently engaged in an $18 billion capital plan covering the 2021 to 2025 period:

FirstEnergy

I will admit that it would have been nice for the company's plan to have been updated, as most of its peers are now providing their plans for the 2023 to 2027 period. That provides far greater visibility into the company's plans and better allows investors to evaluate the company's long-term return potential. The fact that FirstEnergy has not provided any guidance beyond 2025 is disappointing, to say the least. Hopefully, the company will release an updated capital spending plan in the near future as it would be very disappointing to get into 2024 and only have one year of forward guidance.

With that said, the investment plan as presented should allow FirstEnergy to grow its earnings per share at a 6% to 8% compound annual growth rate through 2025. When we combine this with the stock's 3.99% current yield, we can see that investors should expect to receive a 10% to 12% total average annual return. That is certainly respectable and is a bit higher than most other utility companies are likely to deliver over the period. This adds a bit to the company's appeal, despite the lack of visibility.

Financial Considerations

It is always important to look at the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt. As newly issued debt has an interest rate that corresponds with the market interest rate, this can cause a company's interest expenses to go up following the rollover in certain circumstances. As interest rates in the United States are currently at the highest levels that we have seen since 2007, that is a very real concern right now. In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. Although utilities like FirstEnergy Corporation usually have remarkably stable cash flows, we have seen bankruptcies in the sector so this is a risk that we should not ignore. In fact, a unit of FirstEnergy itself declared bankruptcy back in 2018, so we should definitely pay attention to the company's debt load.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity will cover its debt obligations in a bankruptcy or liquidation event, which is arguably more important.

As of March 31, 2023, FirstEnergy Corporation had a net debt of $22.549 billion compared to shareholders' equity of $10.731 billion. This gives the company a net debt-to-equity ratio of 2.10 today. This represents a substantial increase over the 1.87 ratio that the company had at the start of the year, which is quite disappointing as it appears that the company is increasing its reliance on debt. When we consider the risks of debt compared to equity, we can clearly see that the company's risk profile could be changing for the worse.

Here is how FirstEnergy compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| FirstEnergy Corporation |

| 2.10 |

| Exelon Corporation ( EXC ) |

| 1.65 |

| Entergy Corporation ( ETR ) |

| 1.91 |

| Eversource Energy ( ES ) |

| 1.49 |

| Duke Energy ( DUK ) |

| 1.47 |

As we can clearly see, FirstEnergy Corporation is much more reliant on debt to finance its operations than several of the other largest utilities in the United States. The company is actually worsening in this respect, especially when we consider that a few others on this list such as Entergy, have seen their ratios get much better during the first three months of the year. Overall, the takeaway here is that FirstEnergy may be too reliant on debt as a source of financing, which could make the company somewhat riskier than its peers.

Dividend Analysis

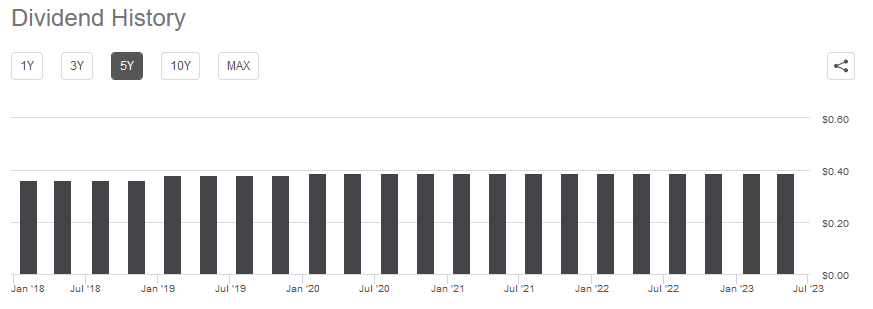

One of the biggest reasons why many people purchase common shares of utility companies is that they usually have higher yields than many other things in the market. As of the time of writing, FirstEnergy yields 3.99%, so that is certainly the case with this company. Unfortunately, FirstEnergy's dividend history is not nearly as good as many other utilities. This is because the company has kept its dividend flat since 2020:

{kind=link}

The problem with this relative to peers is that most companies in the sector increase their dividends on an annual basis. FirstEnergy does have a higher yield than many peers, but the fact that its dividend has been flat since 2020 means that it has lost a considerable amount of purchasing power over the past three years. This is due to the incredibly high inflation that the country has experienced over the period, which has resulted in the dividend being able to purchase fewer goods and services than it could in the past. As a result, anyone that is depending on their portfolios for income will likely feel as if they are getting poorer and poorer with the passage of time. That is a major problem for retirees right now.

Despite the lack of dividend growth, it is still important that we analyze the company's ability to sustain its dividend. After all, we do not want to be the victims of a dividend cut, since such an event would reduce our incomes and almost certainly cause the company's share price to decline.

The usual way that we determine a company's ability to cover its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was generated by a company's ordinary operations and is left over after the company pays all of its bills and makes all necessary capital expenditures. It is therefore the amount that is available for tasks that benefit the shareholders such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on March 31, 2023, FirstEnergy had a negative levered free cash flow of $1.0754 billion. This is obviously not enough to pay any dividends, yet the company still paid out $892.0 million in dividends over the period. At first glance, this is likely to be concerning as the company cannot afford to cover its dividends out of free cash flow.

However, it is common practice for a utility to finance its capital expenditures through the issuance of equity and debt. It will then pay its dividends out of operating cash flow. This is because the high costs involved in constructing, maintaining, and upgrading utility-grade infrastructure over a wide geographic area would other preclude shareholder returns. During the trailing twelve-month period, FirstEnergy Corporation reported an operating cash flow of $2.216 billion, which was easily enough to cover the $892.0 million in dividends that the company paid out during the period. Thus, it does appear that FirstEnergy can sustain its dividends at the current level and we probably do not have to worry about a near-term cut.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like FirstEnergy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few stocks that have such a low ratio in today's overheated market so the best way to use this ratio is to compare FirstEnergy's valuation to its peers in order to determine which firm has the most attractive relative valuation.

According to Zacks Investment Research , FirstEnergy Corporation will grow its earnings per share at a 6.45% rate over the next three to five years. That is in line with the 6% to 8% that we used earlier to calculate the company's projected total return based on its rate base growth, so it seems like a pretty solid estimate. This gives the stock a price-to-earnings growth ratio of 2.42 at the current stock price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| FirstEnergy Corporation |

| 2.42 |

| Exelon Corporation |

| 2.59 |

| Entergy Corporation |

| 2.69 |

| Eversource Energy |

| 2.57 |

| Duke Energy |

| 2.67 |

As we can see, FirstEnergy Corporation does have a somewhat more attractive valuation than its peers. This is probably due to the fact that the company looks to be riskier, as we discussed earlier. FirstEnergy does not trade at an exceptionally large discount though, so it might be best to wait until the stock offers a larger discount to its peers before buying in. With that said though, the stock is quite a bit cheaper than it was the last time that we discussed the company so it still might be worth picking up today.

Conclusion

In conclusion, FirstEnergy Corporation is a regulated utility that shares most of the recession-resistant characteristics of its peers but unfortunately appears to have a higher level of risk. The company is well-positioned to deliver very high total returns over the next few years though and it is more attractively priced than its peers. The biggest complaints here are that FirstEnergy Corp. has much higher leverage than other comparable companies and lacks the dividend growth that has become important during the recent bout of inflation.

For further details see:

FirstEnergy: Attractive Valuation, But Higher Risks Than Peers