DUKB - FirstEnergy Continues To Boast Stability In An Uncertain Environment Despite Q2 Weakness

2023-08-28 08:16:37 ET

Summary

- FirstEnergy Corp. is a regulated electric utility serving the Appalachian region of the US.

- The company's financial stability is reflected in its consistent revenues and operating cash flows.

- FirstEnergy's growth prospects lie in increasing its rate base through infrastructure investments, aiming for 6-8% annual earnings per share growth.

- The company's balance sheet is weaker than many of its peers, and its dividend coverage is tighter.

- FE's valuation reflects these higher risks.

FirstEnergy Corp. ( FE ) is a regulated electric utility that serves most of the Appalachian region of the United States. This is a fairly large geographic region that includes parts of six different states, each with different regulatory commissions:

{kind=link}

This unfortunately makes an investment in FirstEnergy almost like an investment in several different utilities at once. It is not exactly the same though, as the individual utility companies in each of these different states are owned by the same parent company so issues regarding its finances are reflected company-wide. This is something that is quite important since, as I pointed out in my last article about this company, FirstEnergy is much more highly leveraged than many of its peers. This could make it somewhat more heavily exposed to any further increase in interest rates than other electric companies, and Chairman Powell's speech at Jackson Hole on Friday strongly implied that more rate hikes could be coming soon. The company's second-quarter 2023 earnings results were not particularly impressive either, so that is another strike against it. The valuation is difficult to ignore though, as FirstEnergy is currently trading at a lower valuation than many of its peers and even possesses a lower valuation than it did when we last discussed this company in June. As such, it may be worth revisiting to see if the company could be a reasonable addition to a portfolio today.

About FirstEnergy Corp.

As stated in the introduction, FirstEnergy is a regulated electric utility that operates throughout much of the Appalachian region. This is a six-state region that includes the states of Ohio, Pennsylvania, New Jersey, West Virginia, Virginia, and Maryland. The company's service area does not include any of these states in their entirety, but it does manage to cover most of Pennsylvania outside of Philadelphia:

{kind=link}

Parts of this region are quite heavily populated, as the company's service area includes the suburbs of New York City, Pittsburgh, Pennsylvania, Washington, D.C., Baltimore, Maryland, and a few other major municipalities. The company's website states that the company serves about six million customers, which would make it one of the largest utilities in the United States in terms of customer base. However, as I have pointed out in numerous previous articles, the company's customer base alone does not impact the fact that it will possess certain characteristics typical of all utilities. The most important of these is that FirstEnergy enjoys relatively stable revenue and cash flow over time. This chart shows the company's revenue during each of the past eleven twelve-month periods:

{kind=link}

This chart shows the company's operating cash flows during the same eleven twelve-month periods:

{kind=link}

As we can see, the company's revenues were remarkably stable during each of the periods. The company's operating cash flows generally were, although we did see some weakness in 2020 as well as in the most recent quarter. The company primarily blamed its second-quarter weakness on weather, as temperatures throughout most of its service territory were lower during the second quarter of 2023 than they were during the equivalent quarter of 2022. As a result, fewer people were running their air conditioners in order to cool their homes and businesses. From the second-quarter 2023 earnings press release :

In the Regulated Distribution business, higher revenues related to utility investment programs and lower operating expenses were offset by lower customer usage, primarily due to mild temperatures across the company's service footprint, as well as lower pension credits and higher interest expense.

Total distribution deliveries decreased by 4.9% compared to the second quarter of 2022, primarily due to cooling days that were 40% below normal and 48% below last year. Load was down 1.1% on a weather-adjusted basis.

This, admittedly, runs contrary to all of the media reports that we have been seeing about temperatures being substantially above normal this year. However, the month of July in parts of FirstEnergy's service territory was quite hot this year, so perhaps we will see a positive weather impact reflected in the company's third-quarter results.

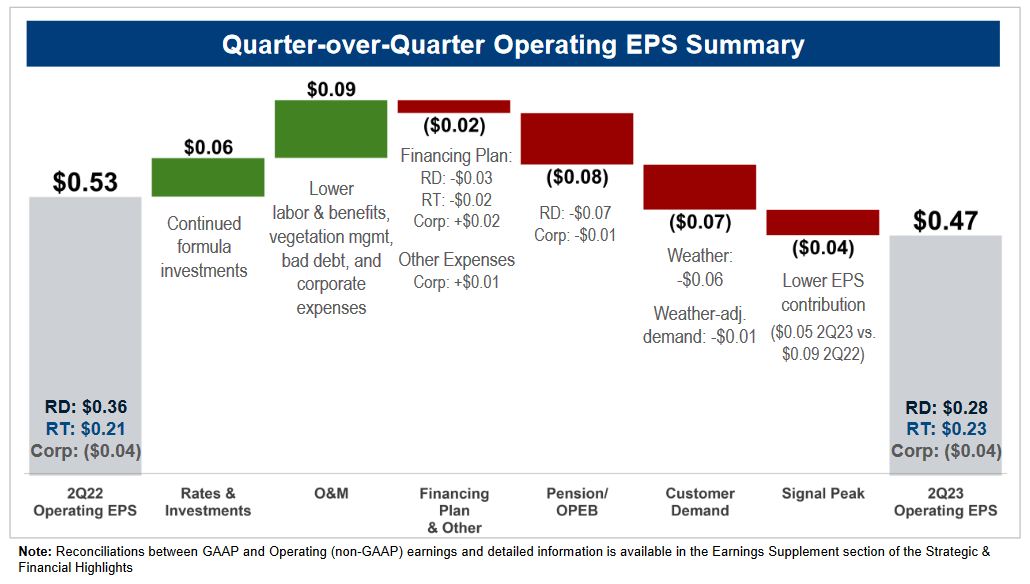

The company's operating earnings per share came in at $0.47 as opposed to $0.53 in the second quarter of 2022. As we can see here, the adverse impact that cooler weather had on the demand for electricity played a significant role in that:

{kind=link}

However, we do see that increased expenses related to the company's employee benefits also played a significant role in reducing its year-over-year operating earnings per share. The company stated that this was due to lower pension credits, so presumably its pension plan did not perform as well as it did during the same period of 2022. It did not provide any specific reason why pension credits were down year-over-year though, so this is just my speculation.

Other than the events that were just explained though, we can see remarkable financial stability over time. After all, its revenues went up pretty consistently from period to period. The company's operating cash flows were meanwhile range-bound except for 2020 and the most recent twelve-month period. The period of time covered by the charts above covered a variety of economic events, including the 2020 pandemic-related lockdowns that resulted in millions of people throughout the nation becoming temporarily unemployed, along with numerous business failures. The period also includes the revival of the economy and the onslaught of the highest inflation that the United States has seen in decades. Both these events have wreaked havoc on the finances of many ordinary people, which I have pointed out numerous times in other articles recently. None of these events had any real impact on FirstEnergy's financial performance though. I explained why in my last article on the company:

The reason for this general stability over time is that FirstEnergy provides a product that is generally considered to be a necessity for our modern way of life. After all, who among us does not have electric utility service to our homes and businesses? Indeed, how many of us know someone who does not have this service? As such, most people will prioritize paying their utility bills ahead of any discretionary expenses during times when money gets tight.

We are certainly seeing signs that money is getting tight for many consumers. For the first time ever, the number of people carrying debt on their credit cards has surpassed the number of people paying them off in full every month. This is despite the fact that credit card interest rates have surged recently. That is a sure sign that many consumers are starting to hurt. This adds somewhat to the appeal of FirstEnergy right now, since a company that has a proven track record of handling such situations with ease is exactly what you want to have in your portfolio to position yourself for whatever might come in the near future.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we want to see any company that we are in grow and prosper with the passage of time. Fortunately, FirstEnergy Corp. is well-positioned to do that going forward, which is a continuation of the trend that we saw earlier in this article. Please refer back to the chart of the company's revenues during the past several twelve-month periods for confirmation of this.

The primary way through which FirstEnergy will generate growth going forward is by increasing the size of its rate base. I defined the rate base in my last article on the company:

The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the prices that it charges its customers in order to achieve the regulatory-allowed rate. The usual way that a utility increases its rate base is by investing money into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure.

FirstEnergy has presented a fairly aggressive plan to the investors through which it intends to achieve this rate base growth. The company is currently planning to invest $18 billion into its infrastructure over the 2021 to 2025 period, which it expects will result in a 7% increase in its rate base during both 2024 and 2025. The company has not provided any information about its growth plans beyond 2024 and 2025, which is unfortunate as it limits our visibility. As I have pointed out before, several of the company's peers have presented plans including the 2026 and 2027 calendar years. In fact, one or two peers have even presented plans extending out past 2030. As such, we have a much more difficult time predicting where FirstEnergy will be in 2026 or 2027 than we do a company that has presented such information. That is disappointing from the perspective of a long-term conservative investor, which probably describes most people who would invest in an electric utility.

The company's rate base growth should allow it to produce 6% to 8% earnings per share growth annually through 2025. When we combine this with the current 4.30% dividend yield, FirstEnergy should be able to deliver a 10.5% to 12.5% total average annual return through 2025. That is a very respectable and attractive return for a utility company, and in fact, it does beat most of the company's peers. However, we only have a limited projection period here compared to peer firms that have shared their plans through 2027.

FirstEnergy has also stated that it is targeting 6% to 8% annual earnings per share growth over the long term. The company will probably seek to achieve this through rate base growth, but it has not provided any capital spending plans to support this ambition.

Financial Considerations

As mentioned earlier in this article, one of FirstEnergy's largest problems is that the company is much more reliant on debt to finance its operations than its peers. We can see this by looking at the net debt-to-equity ratio, which tells us the degree to which the company is financing itself with debt instead of wholly-owned funds.

As of June 30, 2023, FirstEnergy Corp. had a net debt of $23.8370 billion compared to shareholders' equity of $10.9710 billion. This gives the company a net debt-to-equity ratio of 2.17 today. This is actually quite a bit worse than the 2.10 ratio that the company had the last time that we discussed it, which is concerning. It almost appears that the company is going in the wrong direction with respect to its balance sheet. Here is how FirstEnergy Corp. compares to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| FirstEnergy Corp. |

| 2.17 |

| Exelon Corporation ( EXC ) |

| 1.68 |

| Entergy Corporation ( ETR ) |

| 1.92 |

| Eversource Energy ( ES ) |

| 1.58 |

| Duke Energy ( DUK ) |

| 1.53 |

At least FirstEnergy is not alone here with its ratio getting worse. In fact, all of these companies have higher ratios today than they did at the end of the first quarter. When we consider that the effective federal funds rate is currently at the highest level that we have seen since 2007, we do not want to see companies raising their debt loads. After all, that is certainly going to raise their interest expenses. For its part, FirstEnergy Corp. did cite rising interest expenses as a drag on its second-quarter earnings. That will probably continue to be the case going forward, so we should watch the company to see if it reverses its current trajectory and starts reducing its leverage.

Dividend Analysis

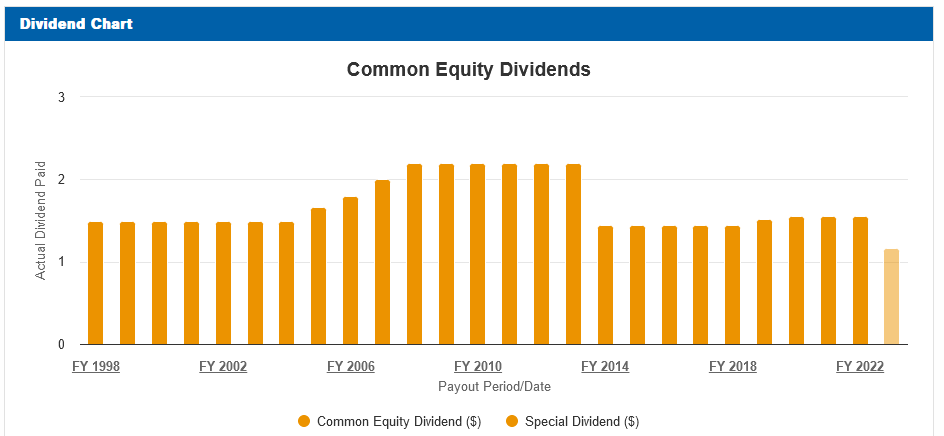

One of the biggest reasons why investors purchase shares of utility companies is because of the high dividend yields that they typically possess. FirstEnergy Corp. is certainly no exception to this as the stock yields 4.30% at the current price. That is substantially better than the 1.48% yield of the S&P 500 Index ( SPY ) as well as the 2.66% yield of the U.S. Utilities Index ( IDU ). Unfortunately, FirstEnergy has not been particularly consistent about increasing its dividend. In fact, it has been flat since 2020:

{kind=link}

This makes the company a rarity in the utility sector as most companies increase their dividends over time. The lack of dividend growth is also disappointing in today's inflationary environment. After all, FirstEnergy's dividend has lost purchasing power over the past two years. That is a very real problem for anyone that is dependent on their portfolio to generate the income that they need to pay their bills and support themselves, which describes many retirees.

As is always the case, it is important that we examine the company's ability to afford its dividend. After all, we do not want to be the victims of a dividend cut that reduces our incomes and almost certainly causes the stock price to decline.

The usual way that we judge a company's ability to cover its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, FirstEnergy Corp. had a negative levered free cash flow of $1.2740 billion. Obviously, that is not enough to pay any dividends, but the company still paid out $893.0 million to its shareholders. This is likely to be concerning at first glance as the company is not generating enough free cash flow to pay its dividends.

However, utilities frequently finance their capital expenditures via the issuance of debt and equity, while paying their dividends out of operating cash flow. This is because of the incredibly high costs involved in constructing and maintaining a utility-grade infrastructure network over a wide geographic area. In the twelve-month period that ended on June 30, 2023, FirstEnergy had an operating cash flow of $1.1870 billion, which was sufficient to cover the $893.0 million that the company paid out in dividends. However, there was not very much coverage here, so caution is still advisable. Overall, though, the dividend is probably reasonably safe.

Valuation

According to Zacks Investment Research , FirstEnergy will grow its earnings per share at a 6.45% rate over the next three to five years. This is relatively in line with the company's rate base growth over the next two years and it does fit management's ambitions for long-term growth. As such, it is probably reasonably solid. This gives the company a price-to-earnings growth ratio of 2.22 at the current stock price. This is quite a bit better than the 2.42 ratio that the company had the last time that we discussed it. Here is how FirstEnergy's valuation compares to its peers:

| Company |

| PEG Ratio |

| FirstEnergy Corp. |

| 2.22 |

| Exelon Corporation |

| 2.72 |

| Entergy Corporation |

| 2.50 |

| Eversource Energy |

| 2.63 |

| Duke Energy |

| 2.65 |

As was the case the last time that we discussed the company, FirstEnergy appears to offer a more attractive valuation than its peers. This is almost certainly due to the company's somewhat higher risks relative to its peers, which were already discussed. That does not necessarily mean that the company is a bad investment though, as the cheaper price accounts for the risks.

Conclusion

In conclusion, FirstEnergy continues to boast the overall stability that we have come to expect from it. The company posted some weakness in its most recent quarter, largely due to the weather, but overall, the thesis remains intact. This company should be well-positioned to handle the economic challenges that continue to mount. It does boast a weaker balance sheet and dividend coverage than some of its peers, but the valuation takes these extra risks into account.

For further details see:

FirstEnergy Continues To Boast Stability In An Uncertain Environment, Despite Q2 Weakness