V - Fiserv: An Undervalued Growth Play

Summary

- Fiserv is a fintech company with strong fundamentals, especially in its merchant acquiring segment that is reporting strong revenue growth.

- It has a good cash flow generation capacity, enabling it to perform acquisitions, reduce balance sheet leverage, and perform share repurchases at the same time.

- Its valuation is rather low and doesn’t seem to be warranted, providing a great buying opportunity for long-term investors.

Fiserv ( FISV ) has strong fundamentals and positive growth prospects ahead, but due to the current bear market, it is trading at low multiples. This makes it a great growth play in the fintech industry right now.

Company Overview

Fiserv is a fintech company, providing integrated information management and electronic commerce systems, enabling money movement for the financial industry. The company was founded in 1984 and has been listed since 1986 on the NASDAQ, while its current market value is about $64 billion.

Fiserv's solutions include transaction processing, electronic bill payment, merchant acquiring, and account processing, beyond others. Its core business is providing to banks, credit unions, fintech, small and large corporates, the technology services they need to smoothly operate and move money, which include core processing systems, and electronic billing and payment systems.

The company, therefore, operates in a highly competitive industry, and its major competitors include other technology companies in the financial industry, such as large payment companies Visa ( V ) and Mastercard ( MA ), plus other companies like Fidelity National Information Services ( FIS ), and ACI Worldwide ( ACIW ).

Business Strategy & Growth

Even though Fiserv is capable of serving customers of all sizes and operates globally in more than 100 countries, where the company has a stronger competitive advantage has been in the segment of small to midsized banks, which lack in-house processing units.

It has more than 10,000 customers worldwide and serves more than six million merchant locations every year. During the past year, Fiserv processed 78 million transactions in its merchant business, while its payment and fintech business processed more than 35 billion debit and network transactions. This large set of transactions provides data and insights for the company, which it uses to differentiate itself from other technology platforms available from competitors.

While Fiserv's business is spread across several services, the vast majority of its revenue comes from processing and services. Indeed, these activities generated 82% of the company's revenue in 2021, being primarily driven from account and transaction-based fees, under multi-year contracts that have high renewal rates. This means that most of its revenue has a highly recurring basis, providing good visibility regarding the company's revenue prospects over the medium term.

Geographically, while the company operates globally, it still generates most of its revenue domestically, given that over the past three years, it generated more than 85% of revenue in the U.S. every year (86% of total revenue was in the U.S. during 2021).

Fiserv's growth strategy has been a combination of organic initiatives, which have been supported by the move of financial transactions to online channels leading to rising transaction volumes over the past few years, plus acquisitions.

Fiserv has targeted businesses that provide a good operating complement, with the integration of First Data in 2019 being a transformative deal for the company. At the time, First Data was valued at about $22 billion and the merger was an all-stock deal, which led to a much bigger combined company in the payments industry.

It considerably increased Fiserv's exposure to the merchant-acquiring business and was the most complex integration in the company's history. Therefore, even though Fiserv has performed several smaller acquisitions and had a good track record, the execution risk was significant given that it was increasing its exposure to a business segment where it had a smaller presence.

Despite that, the integration was completed during 2021, ahead of schedule, and cost synergies amounted to some $1.2 billion, also above its target set in 2019 of around $900 million in cost savings over five years.

Beyond this large deal, Fiserv continued to perform small bolt-on acquisitions in recent years targeting companies that complement its own business, to enhance its position in the fintech ecosystem. For instance, it closed seven acquisitions during 2021, as part of its capital allocation policy, to offer a better customer proposition and have higher customer engagement across its business.

Going forward, Fiserv's growth strategy is not expected to change much, pushing for growth both through its existing customer base by offering new services, and also seeking acquisitions that are complementary to its operations and are financially accretive.

Financial Overview

Regarding its financial performance, Fiserv has a good financial history given that it has delivered growing top and bottom lines over the past few years, and generated strong cash flow at the same time.

In 2021 , Fiserv's annual revenue amounted to $15.4 billion, an increase of 11% YoY, with the merchant acceptance segment being one of the growth engines as revenue increased by 20% YoY in this segment. Its operating income was $2.3 billion, and its net income was $1.3 billion.

Revenue (Fiserv)

However, its adjusted net income was $3.7 billion, which excludes amortization of acquisition-related intangible assets. This is a non-cash charge on the company's P&L statement and is a better metric to analyze the earnings power of Fiserv. Moreover, this is also the best metric to compare against cash flow, given that its free cash flow was $3.5 billion (94% conversion rate), while compared to GAAP net income its conversion rate would be 269%.

This means that Fiserv's cash flow generation is quite good, given that it is close to 100% of its earnings, reflecting its tech-oriented business model with relatively low needs of fixed assets.

During the first nine months of 2022 , Fiserv has maintained good operating momentum despite the challenging economic environment, with organic revenue growth of 11% and expanded operating margin by 100 basis points compared to the same period of last year. The merchant acceptance segment has remained the segment with higher growth rates, reporting 17% revenue growth during this period.

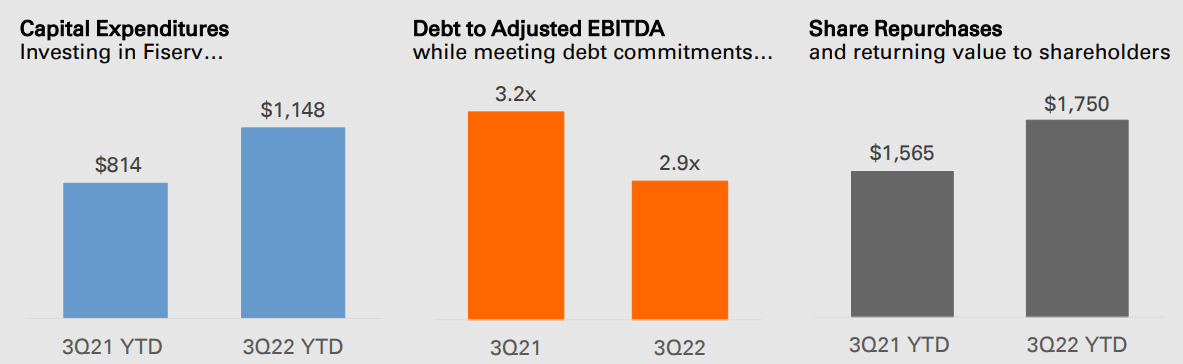

Its adjusted net income was near $3 billion in 9M 2022, up by 10.4% YoY, but while its cash flow generation remained quite good, with free cash flow its conversion rate declined to 71%, as Fiserv has increased its capital expenditures and share repurchases in recent months.

{kind=link}

Regarding its balance sheet, Fiserv's financial leverage is somewhat high, given that its debt-to-adjusted EBITDA ratio was near 3x at the end of last quarter, while many companies in the technology sector usually have low levels of debt. This leverage position is explained by Fiserv's acquisition history, which led to higher financial leverage than desired. Indeed, following the First Data acquisition, its leverage position increased significantly, and over the past few years one of its strategic goals was to reduce leverage back to the 3x target.

Fiserv is now close to its leverage target and is likely to maintain this position going forward, which means that large acquisitions aren't likely over the coming years, even though Fiserv should maintain its strategy of performing smaller deals that it considers to add value for the company.

Regarding its guidance for full year 2022, its target is to reach 11% organic revenue growth and achieve adjusted EPS of $6.48-$6.55, which are both up slightly compared to its previous guidance.

{kind=link}

This positive operating momentum is expected to remain strong in the next few years with analysts' estimates suggesting Fiserv's revenue should increase to more than $21 billion by 2025, and its adjusted net income is expected to be above $5.1 billion.

Regarding its shareholder remuneration policy, Fiserv does not pay a dividend and has historically preferred to distribute excess capital through share repurchases, a strategy that is not expected to change in the near future. In Q3 2022, it returned $750 million to shareholders through share buybacks, which annualized represents some 5% of its market value. Considering that Fiserv has a very good cash flow generation capacity and its leverage position is close to its medium-term target, most likely Fiserv will continue to use a large part of its free cash flow to perform share repurchases for the foreseeable future.

Conclusion

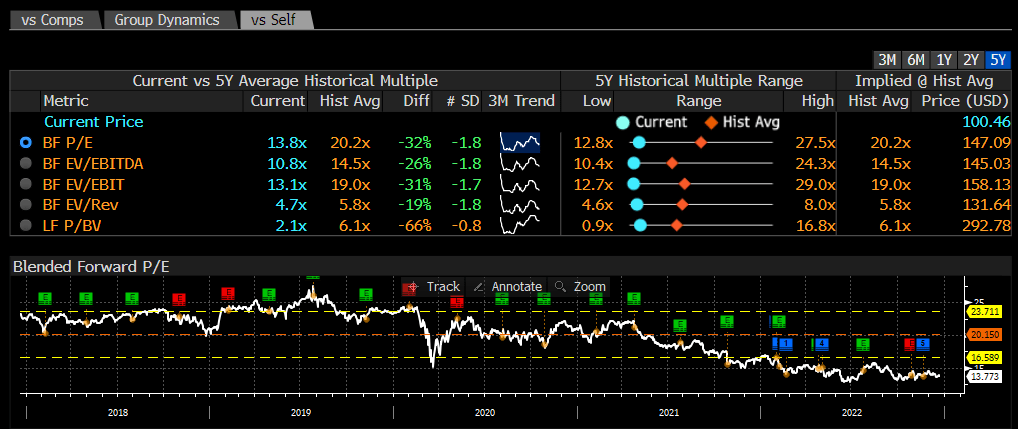

Fiserv is a company with strong fundamentals and relatively good growth prospects, both through its organic initiatives and acquisitions. Despite that, like many growth companies, its valuation has considerably de-rated in recent months, and Fiserv is now trading at some 13.6x forward earnings. This valuation is quite cheap and much lower than its historical valuation over the past five years, on average about 20x forward earnings, which means that Fiserv is currently undervalued.

{kind=link}

Therefore, Fiserv offers a good combination of growth and value, making it quite interesting for long-term investors that want to have exposure to fintech companies that are already profitable and have a recurring business model.

For further details see:

Fiserv: An Undervalued Growth Play