WHITF - Fishtown Capital Q3 Holdings Update

Summary

- I remain bullish energy and bearish on tech companies. Even after the latest downturn, technology companies still are not cheap.

- Considering the outlook for interest rates, with some predictions having them top 5%, the broader market also does not look cheap.

- Cash is much less painful to hold now that it earns 4%.

- I continue to search for value in small caps and other investments.

I entered 2022 bullish energy and cautious technology while maintaining an overall defensive posture with a lot of cash, and wow does that call look good right now. Even after the absolute wrecking that many technology companies have taken, I still do not find the sector appealing.

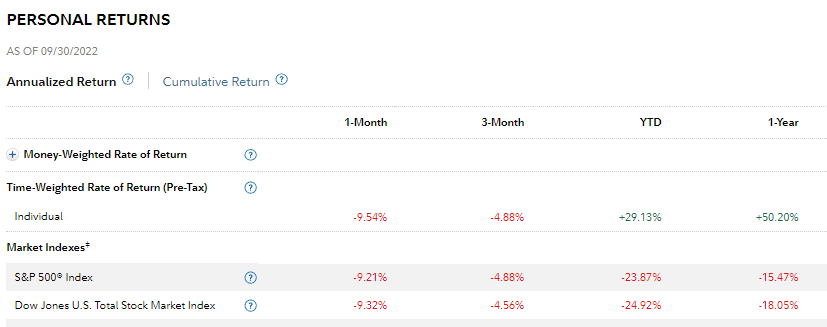

YTD Performance and 2022/2023 Outlook

Through September 30th, I am +29.1% versus -23.9% for the S&P 500 ( SPY ) primarily driven by strength in Cenovus ( CVE ), Energy Transfer ( ET ), and H&R Block ( HRB ).

{kind=link}

I'm still cautious right now with cash near 30%, but after a drawdown of 20%, the risk/reward has skewed a little more favorably. I added my first major new position in Dole ( DOLE ) in the last month at a cost basis of $7.65.

There are still things to like: the labor market is extremely strong, housing is still hanging in there after interest rates hikes, and the consumer is still robust. GDP was positive in the 3rd quarter. I also believe the supply chain situation will sort itself out quickly, which was on the reasons I bought into Dole. That said, I believe we are in uncharted territory raising rates this quickly after a decade of low interest rates, and we have not seen the real impacts yet.

New Positions

Dole ( 7% position ) Opened at $7.65

Investment case described recently in Dole: Poised for a Major Rebound.

I think Dole can double in 12-18 months.

Closed Positions

Bank of NY Mellon ( BK ) (3% position)

Closed at $45 for a 12% loss after opening at $51. Nothing company specific other than a lack of catalysts. I just decided I was more comfortable in cash for now. It's starting to look interesting again to me.

Whitehaven Coal ( OTCPK:WHITF ) (3% position)

Purchased 8/15 for $4.63, sold on 10/7 at $6.90.

Australian Thermal Coal producer trading at a very low valuation. Key risk is Newcastle coal prices. Leading up to me selling, Newcastle Coal prices have weakened significantly while Whitehaven has gone up 20%. That was enough for me to book the win.

We're in shoulder season for coal and bullish sentiment towards energy in general seems to have dissipated in the last month. But winter is coming, and if WHITF declines further and/or Newcastle Coal prices rebound, I would re-enter.

Existing Positions

Cash (30%)

Less painful to hold yielding 3-4% right now. I do not buy into the idea that in an inflationary environment like this one, I need to hold assets otherwise I'll lose to inflation. Why? Because inflation doesn't look the same to everyone, and because the optionality of the cash is important to me.

Cenovus Energy (25%)

My top position, Cenovus was established at an average price of $9. I did trim some of this around $21 because it had just become too large of a position. My risk management was out the window at $16. At $21, it was just too extreme and I took a bit of profits in my non-taxable account.

I'm still very bullish on this name, especially in light of the recent OPEC moves. Cenovus likely hits their debt targets sometime in Q1 of next year, and then begins returning all of their free cash flow to investors. If oil prices and crack spreads stay strong, I could see Cenovus hitting $30 sometime next year.

Berkshire Hathaway (10%)

Berkshire Hathaway ( BRK.A ) ( BRK.B ) is an anchor in my portfolio and I consider it to be an extremely safe stock, even if it isn't nearly as cheap as last year. It continues to outperform the S&P500 and it is a much better choice in an inflationary environment as I described recently in Berkshire Hathaway Performing Well In this Down Market.

H&R Block (10%)

A big winner in 2021 and now a big winner in 2022. I have finally trimmed a small amount of H&R Block ( HRB ) shares and have sold January $40 and $42 calls against my existing position.

I still like the shares, but there's been a lot of appreciation fast in a tough market. I sold the calls because I questioned how much more upside it had.

At $41, it has a forward P/E of ~10 while returning nearly all of its cash flow to shareholders. It is as good of a recession proof business as I can think of.

One of H&R Block's competitors, NextPoint Financial ( OTCPK:NACQF ) (the parent company for Liberty Tax) recently reorganized and their shares stopped trading. Liberty Tax is still operating, but the future of that business looks shaky.

I still like the shares and would be happy to have the calls expire worthless.

Energy Transfer (15%) - Added another 20% in units to my position at $11.70 and purchased January 2024 $12 calls for $1.07 when the stock dropped back to $10.

I updated my thoughts on Energy Transfer ( ET ) calling it the last energy bargain in June when shares were in the low $11 range. Considering that most energy is still well off their June highs, this call has held up well.

I reallocated some of portfolio from CVE into ET. I really like both, but think ET is a bit safer, albeit with less upside if crude prices stay strong. I've been meaning to update my thoughts on this name, but Ray Merola keeps stealing my thunder and writing up everything I want to stay .

ET has been strong this year and I believe is on the verge of re-rating. In the next 4 months, I believe we see the distribution restored back to $1.22, another 2 blockbuster quarters, with news that they hit their debt leverage targets. At $12.70, a $1.22 distribution ET would yield nearly 10% with significant excess DCF to continue deleveraging or repurchasing units. I think a $15 unit price by early next year is probable.

Banks: JPMorgan (3%)

In my last update, I said

This concern and the Russian conflict made me sour on banks, so I sold Citigroup. My cost basis on JP Morgan is $80, which is why I held. Every single time I hold something because I don't want to pay taxes on it, I regret it.

Well, right on cue, JPMorgan ( JPM ) dropped from $135 to $106 but has rebounded recently. I think it's a buy here and banks in general may be a good value going forward.

Conclusion

I still believe we're in a time where protecting capital is job #1, especially since cash now yields something. I still think that now is, at best, a mediocre time to buy stocks. My opinion would change if stocks fell significantly from here, all other things being equal.

I also believe it's unlikely that the S&P500 outperforms other asset classes over the next few years like it's done so consistently in the past, so I'm looking hard at other asset classes - namely preferred shares and corporate bonds - for the first time in a while. Both will do well if the Fed gets inflation under control, but bonds will likely do better if the "soft landing" doesn't happen.

Stay safe out there!

For further details see:

Fishtown Capital Q3 Holdings Update