FTLF - FitLife Brands: At An Inflection Point With Catalysts For Re-Rating

2023-06-23 12:41:56 ET

Summary

- FitLife is at an inflection point as it shifts to an online sales strategy and integrates its acquisition of Mimi's Rock Corp.

- If these initiatives are successful, I estimate the stock to be trading at 9x 2024 earnings. This looks cheap due to its history of 25%+ ROIC and earnings growth.

- Risks include the illiquid nature of the stock and the uncertainty of successfully integrating Mimi's Rock Corp.

- Applying to be listed on the Nasdaq exchange is a potential catalyst. If successful, the share repurchase program would be more effective and the earnings multiple could expand.

I think FitLife Brands, Inc. ( FTLF ) is at an inflection point. This is despite seemingly always being at an upward inflection point given the stock’s rise over the past five years.

The stock has been relatively flat since the end of last year as they have been shifting to more of an online sales strategy and as they have been integrating their recent acquisition, Mimi’s Rock Corp (“MRC”). Earnings have been lumpy because of these factors, and investors are waiting to see how these business changes play out.

I think the results of these changes will come soon, and I think they will be very good for the business. A larger percentage of revenue coming from online sales will lead to higher margins and smoother earnings over time. The successful integration of MRC will also lead to a large increase in earnings per share, as the acquisition was not paid for with FitLife shares, but was funded by cash and some debt. I think this debt will be paid off quickly as the business is capital light and converts earnings to free cash flow efficiently.

The supplement market in North America has also grown substantially and is forecasted to grow substantially into the future. This will provide tailwinds for FitLife as the current business story plays out. I personally am not a believer in the efficacy of most supplements, but this trend can't be ignored.

North American Supplement Market Growth (Fortune Business Insights)

{kind=link}

On top of this, the company recently applied for uplisting to the Nasdaq exchange. I will go into more detail below, but this will likely be a catalyst if the above initiatives are successful. If they are, I estimate the stock to be trading at 9x 2024 earnings, which is cheap considering its history of high ROIC and earnings growth.

Online Sales

The first initiative that FitLife has been focusing on for some time is having a larger portion of its revenue come from online sales. Full year 2022 online sales were 28% of revenue compared to 24% in the prior year, but the trend has been accelerating. Online sales grew by 25% year over year in Q1 2023 while wholesale revenue grew 6% year over year. The main benefit of more online sales is smoother revenue and earnings, as wholesale revenue can be lumpy depending on timing of customers restocking inventory and timing of delivery of inventory.

This lumpiness most clear from Q4 2022 earnings results as total revenue declined 25% year-over-year due to wholesale revenue declining 39% year over year. Management encourages looking at sales of its products to consumers as a better indicator of the company’s wholesale revenue. In that quarter, sales to consumers only declined by a low single digit percentage.

Having smoother earnings doesn’t necessarily change the economics of the business over the long term, but it does make it easier for analysts to forecast earnings. Funds that wish to avoid volatility in earnings and in the stock, price may be more likely to buy the stock if earnings are more predictable.

Also, for FitLife specifically, more online sales diversifies revenue away from GNC. GNC accounted for 71% of revenue in 2021, and 67% in 2022. I don’t think this is a huge risk as GNC is a well-known brand that has been around for a long time, but if GNC sales were to decline materially, it will affect FitLife.

Valuation and Integration of MRC

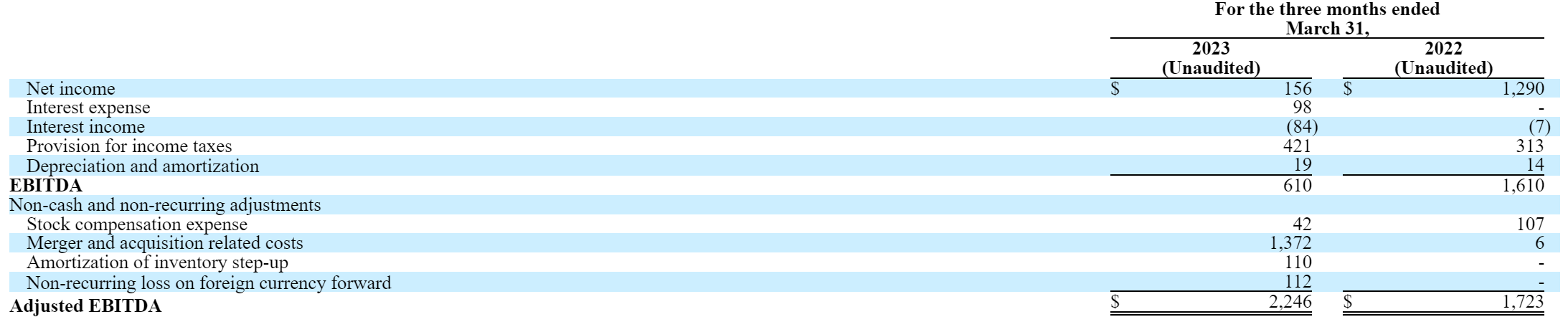

FitLife’s acquisition of MRC was consummated on February 28 and contributed $2.6m in revenue in the first quarter. Total revenue for the quarter increased 47% year over year because of this. Despite this increase in sales, earnings declined over 50% due to, according to management, non-recurring expenses from the acquisition. Adjusted EBITDA for the quarter, which excludes these expenses, increased 30% year over year to $2.2m.

Fitlife Q1 2023 Adjusted EBITDA (Fitlife Q1 10-Q)

{kind=link}

Of this increase in adjusted EBITDA, $0.4m came from MRC, which only contributed to the business for a little less than half of the quarter. For a full quarter, I would assume about $0.8m in adjusted EBITDA would come from MRC. This would have meant $2.6m in adjusted EBITDA for the quarter. Adding back net interest expense, tax expense, and depreciation and amortization would lead to $2.1m of net income, and a net income margin of 19.6%. Annualized, net income would be $8.4m.

FitLife’s fully diluted market cap is $81m, meaning the stock is currently a little under 10 times a rough estimate of 2023 earnings. Given the history of organic growth, the rapid increase in online sales, and the growth of the supplement market in North America, I would estimate FitLife revenue grows 10% in 2024 to $47m. Using my estimated 19.6% net income margin from Q1, net income for the full year would be $9.2m. With 4.9 m fully diluted shares as of Q1 2023, my estimate of 2024 EPS is $1.86 which leaves the stock trading at 9x forward EPS.

This seems cheap given the history of 25%+ ROIC, the history of earnings growth, and management that is competent, aligned and returning capital to shareholders. If these factors remain stable into the future, the stock looks very cheap and should provide great returns for shareholders.

Catalysts

The estimate above assumes the integration of MRC goes to plan, which is not a guarantee. However, the management team has a history of exceptional business performance and the CEO is clearly competent given the fact that he presided over FitLife’s turnaround, which led to the stock’s meteoric rise. It’s difficult to know the details of this integration, so at a certain point, those that own shares must trust that the management team will be successful. If investors don’t have this trust, then it would be best to sell their shares.

At the very least, it seems that the management team believe they will be successful. Recently, the CFO made an open market purchase of 1000 shares at a price of $17 per share. This is not a huge amount, but it increased his ownership by about 40%. Along with this, the company recently applied to be listed on the Nasdaq exchange, which would increase the stock's liquidity. I believe the company has been postponed repurchasing shares for this, as being listed on the Nasdaq exchange would make it easier to do so without affecting the share price.

I think this would lead to multiple expansion as more funds would be able to own the stock, and a premium would be applied due to the company actively repurchasing shares. Additionally, the reduction in shares would raise EPS, which would also help the stock.

Risks

FitLife is an illiquid stock that trades about $30 thousand worth of shares per day on average. The stock is illiquid because of its small market cap, the fact that it trades over the counter and because of its low float due to the CEO Dayton Judd owning the bulk of the equity through direct ownership and through Sudbury Capital Management, the hedge fund in which he is managing partner.

The company did apply to be listed on the Nasdaq exchange, which would increase liquidity. While there is no guarantee the application will be accepted, FitLife does meet the requirements to be listed on the exchange.

Nasdaq Exchange Listing Requirements (Nasdaq)

FitLife’s aggregate earnings over the past 3 years easily topped $11m, and the bid price is well over $4. Being listed on this exchange would increase liquidity, but it would still be a relatively illiquid stock given the market cap. This makes it difficult to sell shares quickly without bringing the stock price down if an investor has a sudden need for cash. The best way to control for this risk is to keep the position size small or not invest at all unless you have a very long-term holding period in mind.

The risk of not integrating MRC successfully remains. It is difficult to know if this is going well unless you have an inside look at the business, which outside shareholders will not. Investors must understand the management team and their history to determine the chances of success.

Final Thoughts

I am estimating that FitLife’s stock is trading at 9x 2024 earnings, assuming the successful integration of Mimi’s Rock Corp. Obviously, if the non-recurring expenses end up being a bit more recurring, the stock is not as cheap. Given current management’s history of success with the business, and their confidence as gauged from recent CFO open market purchases and the extension of the share repurchase program, I am personally betting that this will be successful.

Along with the earnings growth that I believe will come from this acquisition, the returns for shareholders may be juiced if the application to be listed on the Nasdaq exchange is accepted. With this, the company will be able to repurchase shares more effectively and the stock may see multiple expansion as funds that might not be able to stocks that trade over the counter will be able to invest.

These next 6–12 months will be pivotal for FitLife as many changes to the business become settled. While there are uncertainties, I am betting that these changes will lead to higher earnings per share and greater investor interest in the stock.

For further details see:

FitLife Brands: At An Inflection Point With Catalysts For Re-Rating