FIVE - Five Below: An Apparent Struggle To Meet Double-Double Goal

2023-10-19 13:56:16 ET

Summary

- Five Below, Inc. has held up better than its peers in the retail sector, bouncing sharply off its lows and seeing much less relative downside in Q3 than names like Dollar General and Dollar Tree.

- However, Five Below isn't immune from shrink issues which will affect its Q3/FY23 earnings, and although its growth has been impressive, its FY25 targets are proving elusive.

- In this update, we'll look at how Five Below is progressing vs. its FY2025 targets, its recent results, and whether Five Below offers a margin of safety after its sharp correction.

It's been a volatile past quarter for the Retail Sector ( XRT ). While off-price names like TJX Companies ( TJX ) have held up well, we've seen bifurcated results among discount stores, with Dollar General ( DG ) seeing its share price more than halved and Dollar Tree ( DLTR ) taking a beating as well.

Fortunately, Five Below, Inc. ( FIVE ) has been one name that's held up better than its peer group, down ~18% in Q3 vs. a ~37% decline for DG and a ~26% decline for DLTR. However, it has become clear that shrink isn't just an issue at Target ( TGT ) and some other brands, and while the company has maintained its sales guidance and has a strong H2 on deck from a unit growth standpoint, it will need flawless execution to hit its 2025 Triple-Double targets. Let's dig into the recent results and FY2023 outlook below:

{kind=link}

Recent Results & Updated FY2023 Outlook

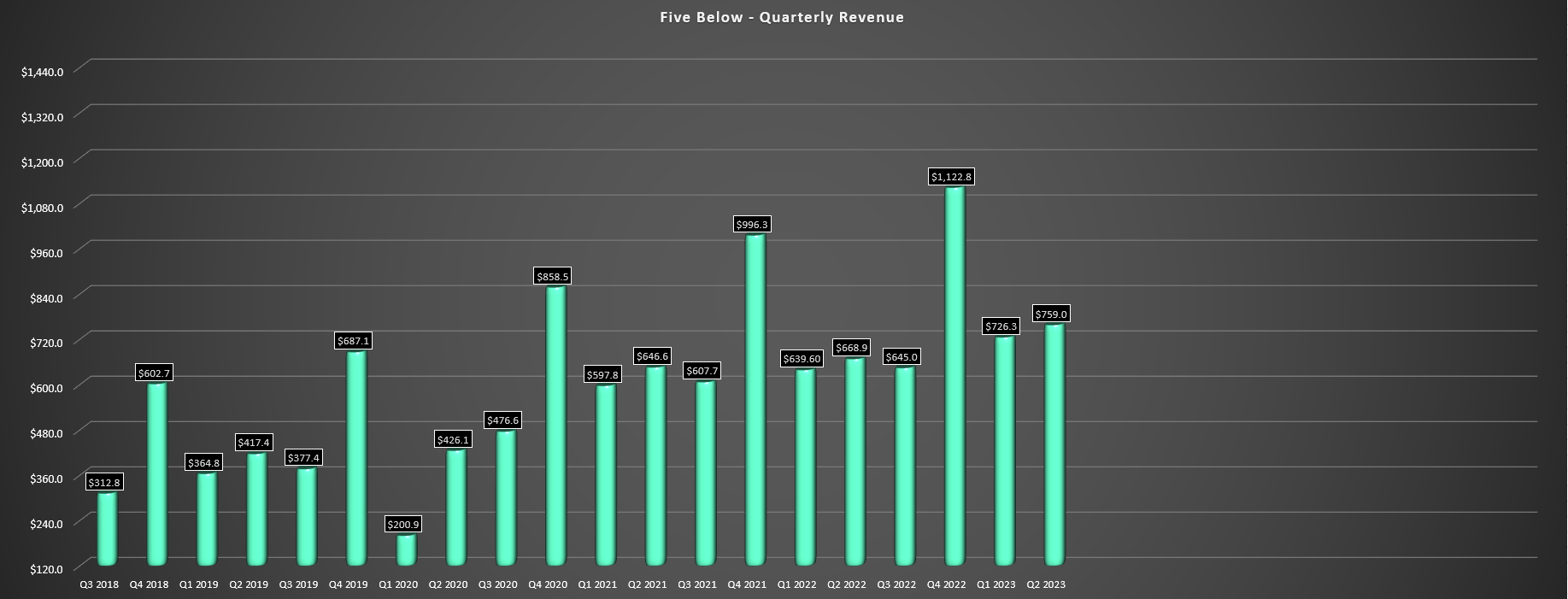

Five Below released its fiscal Q2 results in late August, reporting quarterly revenue of $759.0 million, translating to 14% growth year-over-year. The solid performance was driven by industry-leading unit growth of 12% (40 new stores opened in the quarter, ending the quarter with 1407 stores), and 2.7% comp sales growth. The company noted that its comp sales growth can be attributed to 4.5% growth in comparable transactions, and shared that backpack season was strong for back-to-school, and that it also had success chasing sales with Barbie, with other stand-out performers including Squish, Hello Kitty, and consumables (candy, snacks and beverages).

Five Below Quarterly Revenue - Company Filings, Author's Chart

{kind=link}

Meanwhile, Five Below shared that H2 2023 would be a busy period for store openings, with the company expecting to open upwards of 130 stores (67 year-to-date) to achieve its goal of opening 200+ stores for the year. And the company also shared that gross improved by 70 basis year-over-year with the benefit of lower inbound freight costs, and it confirmed that its remodels are going well, with ~600 total remodels to date with these remodels providing a nice lift to average unit volumes and paying dividends. This is important because Five Below will head into the busy holiday season (Halloween, Christmas) in its strongest position to date with a significant portion of its fleet in its new Five Beyond format. Finally, quarterly earnings per share were up 14% year-over-year to $0.84, and the company shared that labor availability is not an issue, supporting its aggressive growth targets.

Unfortunately, these solid results were overshadowed by negative commentary related to shrink, with Five Below noting that it expects higher shrink levels for the year consistent with what some other retailers have called out, with Philadelphia being one of its worst performers from a shrink standpoint. Given this development, the company elected to increase its shrink reserve for the balance of the year, with this expected to affect its annual EPS this year (lowered to $5.27 - $5.55). The company did note that it's looking to combat this with enhanced technology, merchandise presentation, selective price increases, register formats and policies/procedures, but given how prevalent this is across the space, it's not clear how much impact these initiatives will have, and whether this may have to lead to some store closures for the worst impacted stores if things to worsen substantially.

Earnings Trend & Progress Against Triple-Double

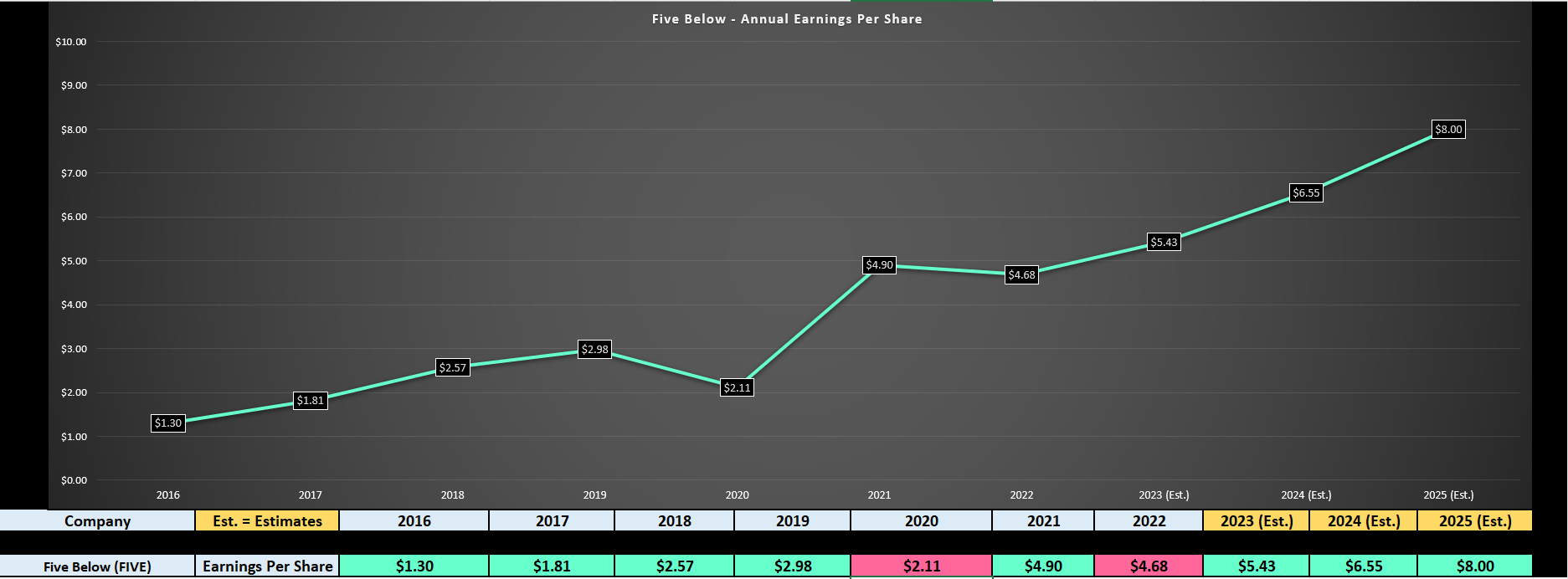

Looking at Five Below's earnings trend below, the company has done a phenomenal job over the past few years, and just as impressive of a job since going public. For starters, the company has reported a market-leading 10-year median return on invested capital of ~25%. Second, it's grown annual earnings per share [EPS] at an incredible rate of ~24% since FY2016, and is on pace to maintain a ~22% compound annual EPS growth rate out to FY2025 based on estimates of $8.00.

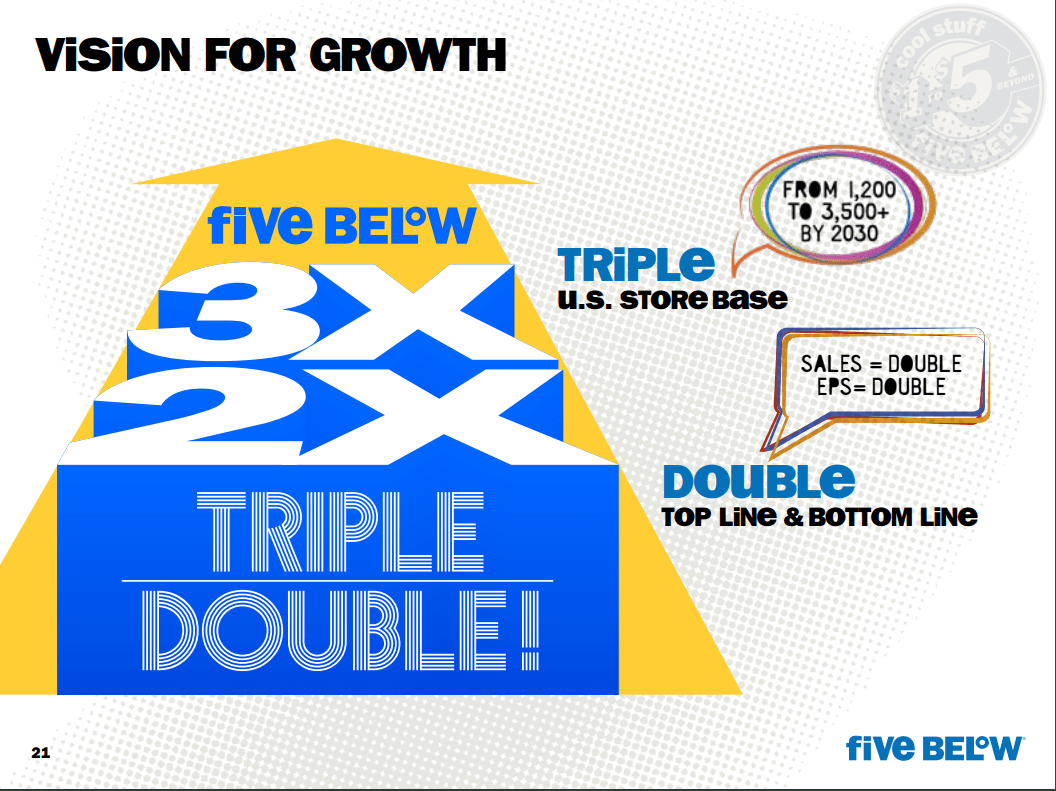

That said, while these are incredible figures and the company continues to be one of the better growth stories in the Retail Sector ((XRT)), the company's Triple-Double targets through 2025 are looking like they might have been too ambitious, with them including the following:

1. A doubling of sales to ~$5,696 million (FY2021: ~$2,248 million).

2. A doubling of earnings to $9.80 (FY2021: $4.90).

3. 1,000 new stores over the period (925 at low end) with the store count sitting at 1,190 at the time.

Five Below - Earnings Trend & Forward Estimates - TIKR.com, Author's Chart

{kind=link}

If we check in on these targets, Five Below will finish FY2023 with annual sales of ~$3.57 billion, assuming it meets the high end of guidance. This means that it would need to grow sales by ~60% from FY2023 to FY2025 to meet its targets. And while meeting these goals is certainly helped by an industry-leading unit growth rate, delivering that level of comp sales growth won't be easy in the current environment. As for earnings, FY2025 annual EPS estimates are currently sitting at $8.00 and even if we assume blowout earnings of $8.25 with above-planned store growth and margin expansion, it will still come up ~17% shy of its target. Finally, on unit growth, the company would need to finish 2025 with 2,115 stores to meet the low end of its target, and assuming it finishes 2023 with 1,540 stores, this would mean it will need to open 287 stores per year just to meet the low end, also a big ask.

Triple Double Plan - FIVE Investor Day March 2022

{kind=link}

In fairness, the store count goal looks achievable if it can continue to execute as it has with a track record of over-delivering, so I wouldn't count that out just yet. And to be fair, the company could not have predicted that interest rates would soar to their highest levels in two decades at the time of the Investor Day, though some conservatism could have been baked in given the high inflation, the potential for multiple hikes, and that interest rates were already at generational lows. Finally, the company couldn't have predicted the shrink issue, which certainly hasn't helped. So, while I don't think the company should be heavily penalized for swinging for the fences and coming up short given the negative developments from a bigger picture standpoint (weaker consumer, higher theft, development/permitting delays), it is disappointing that FIVE will need a miracle to deliver on these three targets.

Given that these goals are looking much less achievable with just nine quarters to go and some of the company's ultra-high multiple might have been tied to delivering near these goals, I think it's better to use a more conservative multiple to value the stock vs. its 10-year average earnings multiple of ~36.2x during an ultra-low interest rate environment with ambitious goals. That said, Five Below continues to execute well given the challenging environment and whether the company meets its revenue goal in FY2026 and its annual EPS goal in FY2027, it will still be one of the higher-growth names in the sector with a unique more recession-resistant positioning. Hence, I think a premium multiple is still warranted, but I think a more conservative multiple is ~29x earnings, a 15% discount to its 10-year average.

Valuation & Technical Picture

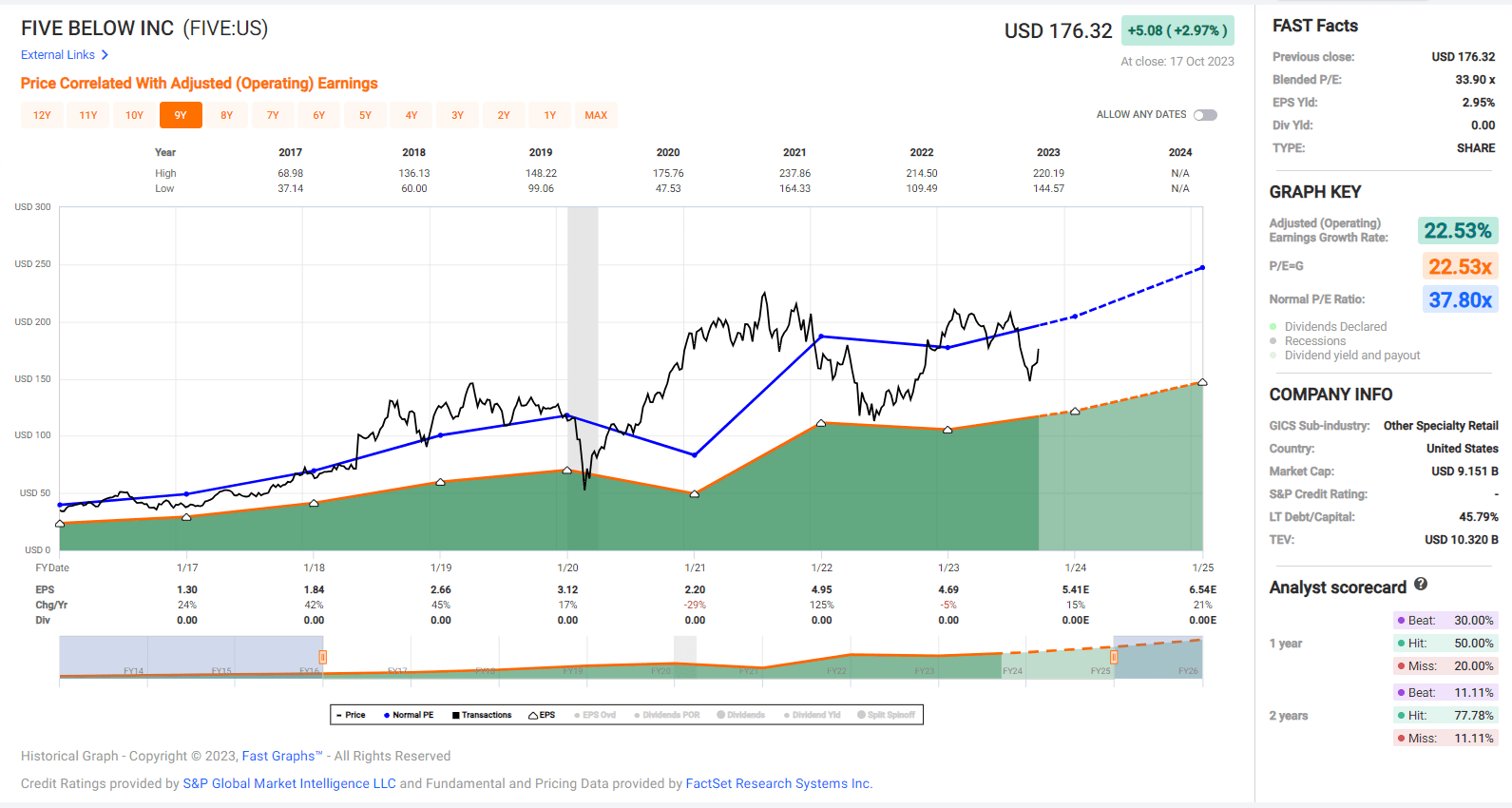

Based on ~56 million shares and a share price of $176.00, Five Below trades at a market cap of ~$9.86 billion and an enterprise value of ~$11.0 billion, making it one of the higher capitalization names in the market, with a similar market cap to names like Casey's ( CASY ) and Burlington Stores ( BURL ). However, with industry-leading unit growth rates and an incredible earnings CAGR, the company continues to command a premium multiple as highlighted previously, with its 10-year average earnings multiple coming in at ~36.2. However, while this multiple might have been appropriate in a near-zero interest rate environment in the company's higher growth years, I think a more conservative multiple today is ~29.0x, which would place a fair value on the stock of $190.00 using FY2024 annual EPS estimates of $6.45.

Five Below - Historical Earnings Multiple - FASTGraph.com

{kind=link}

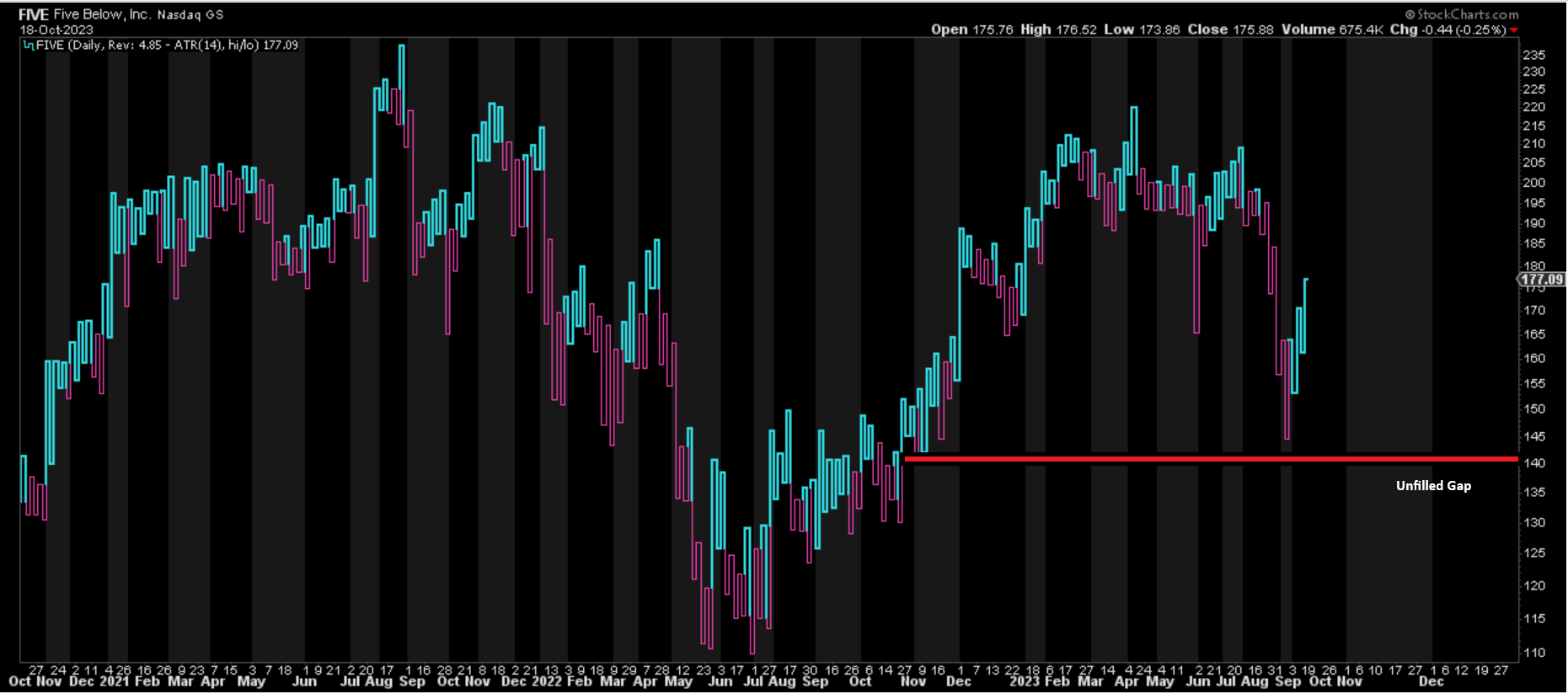

Although this points to an 8% upside from current levels, I am looking for a minimum 25% discount to fair value for mid-cap stocks to ensure a margin of safety, and preferably closer to 30% in the more difficult macro environment. And, if we apply this discount to Five Below, the stock's ideal buy zone comes in at $142.50 or lower, suggesting the stock is nowhere near a low-risk buy zone currently. And while the stock could continue to rally and outperform its peers off its recent lows, the stock's recent correction stopped short of filling in an important gap on the chart from October 2022 at $139.60, with Five Below having a propensity to fill its upside gaps in the past (June 2018, September 2018, January 2019, August 2019) in the past. So, while the stock may get away with not filling this gap this time, I don't see any reason to chase the stock above $176.00 with an unfilled gap below and the stock trading at a rich multiple even when factoring in its exceptional growth rates.

Five Below - 3-Year Chart - StockCharts.com

{kind=link}

Summary

Five Below had a solid Q2 from a financial standpoint, but its Q3 results will likely be much softer because of the impact of a true-up in its shrink reserve, and this will also affect its annual EPS which is now expected to grow just 16% year-over-year despite ~15% unit growth and the benefit of a 53rd week. Meanwhile, although the company is working on initiatives to reduce shrink, this is certainly a negative development investment thesis and a minor margin detractor that wasn't present previously.

Assuming Five Below were trading at less than 22x forward earnings, I would argue that the lower than anticipated growth was becoming priced in, and it might suggest the stock was worthy of investment. However, with Five Below, Inc. at ~27x next year's earnings estimates, I don't see enough margin of safety here. So, if I were looking to put capital to work, I think there are more attractive bets elsewhere like Aritzia ( ATZ:CA ) at just ~13.8x 2024 earnings estimates.

For further details see:

Five Below: An Apparent Struggle To Meet Double-Double Goal