DG - Five Below: Shares Still Aren't A Buy After Tanking

2023-08-31 06:04:46 ET

Summary

- Five Below's Q2 revenue of $759 million missed analysts' expectations by $1.1 million but increased 13.5% YoY.

- Earnings per share came in at $0.84, beating analysts' expectations by $0.01.

- Management revised profit guidance for the year, forecasting net profits of $295 million to $311 million, down from $297 million to $319 million.

- This lowered guidance caused shares to sink, but the firm's long-term outlook is positive.

- Despite this, FIVE stock doesn't look attractive enough to buy just yet.

After the market closed on August 30th, the management team at discount retailer Five Below ( FIVE ) announced financial results covering the second quarter of the company's 2023 fiscal year. Even though management exceeded expectations on the bottom line, a combination of missing expectations on the top line and, more importantly, management's decision to reduce profit guidance for the year, resulted in shares of the company tanking about 7.7% in after-hours trading. In the grand scheme of things, the results reported by management were still solid and the long-term outlook for the company remains positive. But this does go to illustrate the risks associated with buying companies that are very expensive. Even after adjusting for this aftermarket drop, shares of the retailer don't look particularly appealing. However, if they drop more than this, they could be worth consideration.

A mixed quarter

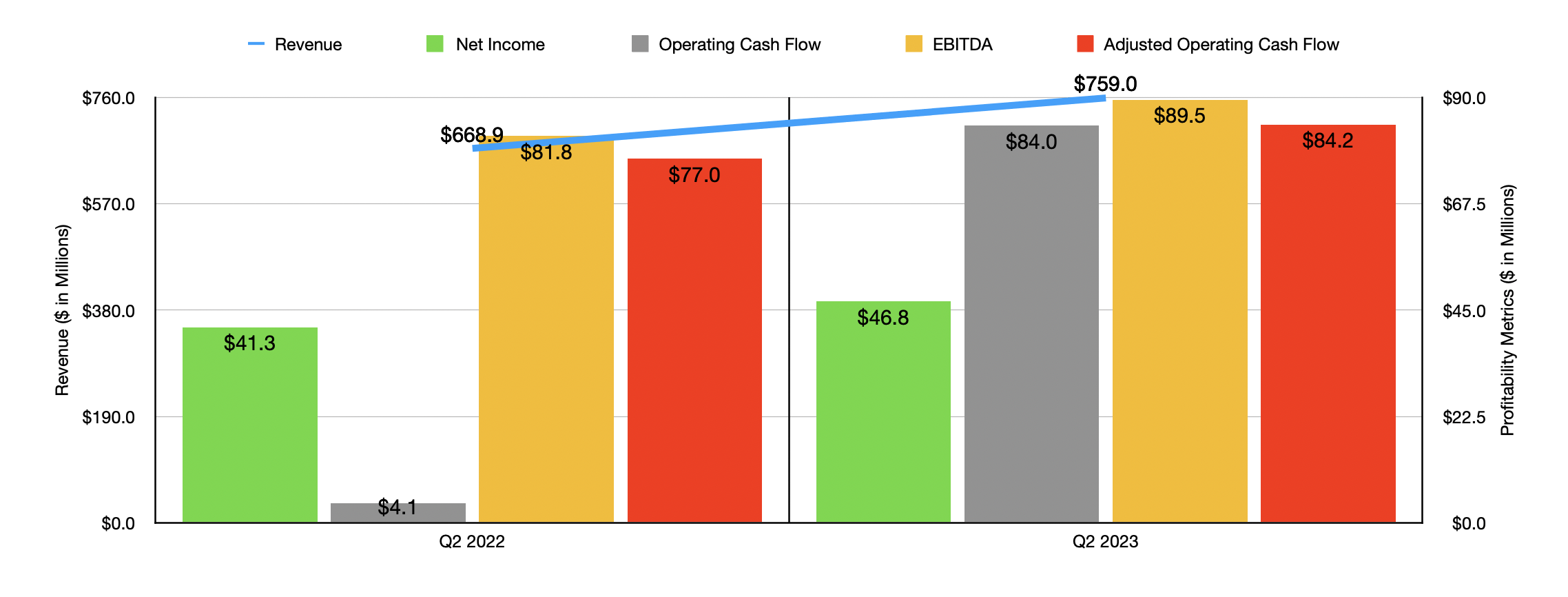

During the second quarter of its 2023 fiscal year, Five Below reported revenue of $759 million. That represents an increase of 13.5% over the $668.9 million management reported at the same time last year. Although this is a nice year over year increase, it did miss analysts' expectations by a modest $1.1 million. Frankly, I don't see this as a material miss, but the market can be fickle with these things. Based on the data provided, the primary driver of the sales increase was a continued rise in store count. By the end of the quarter, the company had 1,407 stores in operation. This is 155 greater than the 1,252 stores that the company had at the end of the second quarter of last year. During the second quarter on its own, management succeeded in opening 40 new stores. Another, though less significant, driver of the increase involved comparable store sales. These grew by 2.7% year over year.

{kind=link}

On the bottom line, the picture for the firm was a bit better. Earnings per share came in at $0.84. This is a nice increase over the $0.74 per share reported in the second quarter of 2022. It also happens to be $0.01 per share higher than what analysts were expecting. This translated to net profits of $46.8 million compared to the $41.3 million the company generated at the same time last year. We should also pay attention to other profitability metrics. Operating cash flow, for instance, skyrocketed from $4.1 million to $84 million. But if we adjust for changes in working capital, we would get an increase from $77 million to $84.2 million. Meanwhile, EBITDA for the company grew from $81.8 million to $89.5 million.

{kind=link}

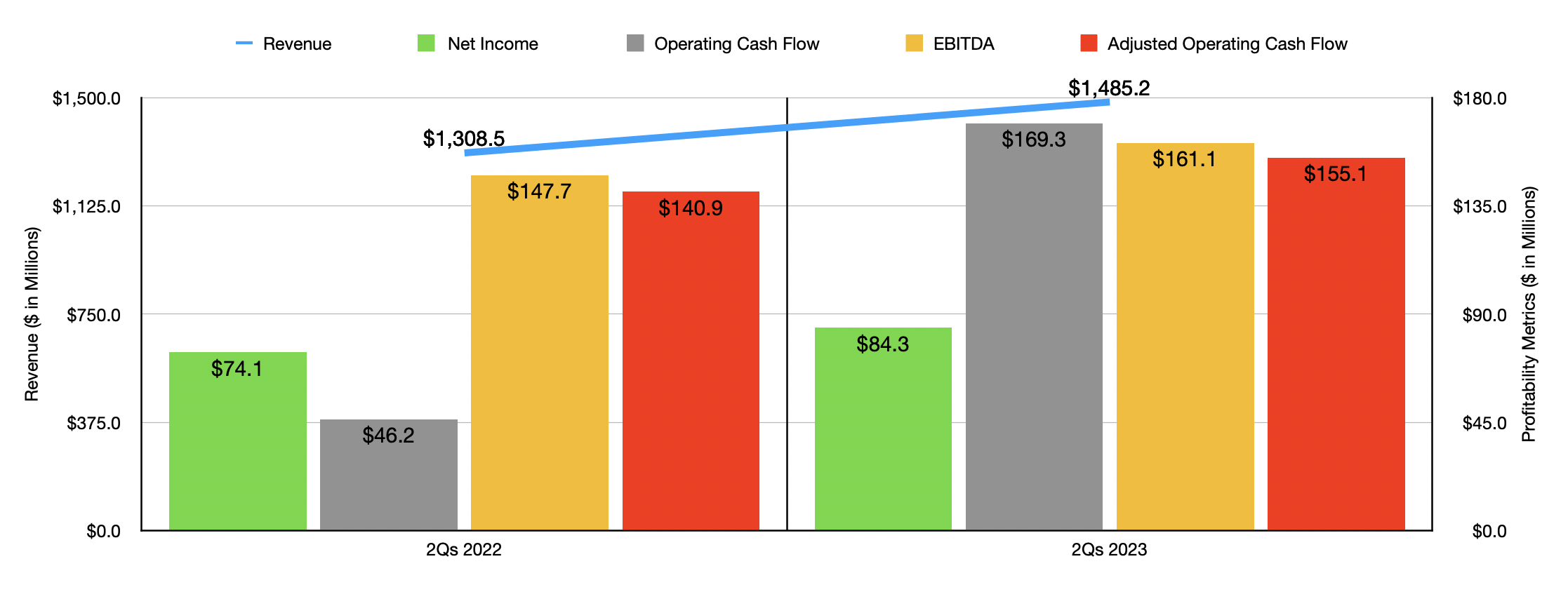

In addition to showing financial results for the most recent quarter, I also decided to provide, for context, results for the first half of 2023 relative to the same time of 2022. These results can be seen in the chart above. The overall trend, as you can see, has been positive for the company this year. However, management has had to revise guidance to some extent. For the year as a whole, they are still forecasting revenue of between $3.50 billion and $3.57 billion. This is unchanged from prior guidance. This increase should be driven by 200 new stores that will be opened during the year, and by comparable store sales climbing by between 1% and 3%. Once again, all of this is unchanged from what the company achieved last year. What has changed, however, is it management is now forecasting net profits of between $295 million and $311 million. Prior guidance called for this to be between $297 million and $319 million. At the midpoint, this would result in net profits coming in at about $303 million. That's down from the $308 million previously forecasted.

When valuing the company, I do think it is worth mentioning that we should adjust for the fact that this year has an extra week included in it. That will add about $40 million in sales to the company and $4.5 million in net profits. So to be comparable with more typical years, we should subtract these from guidance provided by management. Following this approach, we should end up with net profits, on an adjusted basis, of $298.5 million. Adjusted operating cash flow should be around $475.5 million, while EBITDA should come in at around $517.5 million.

{kind=link}

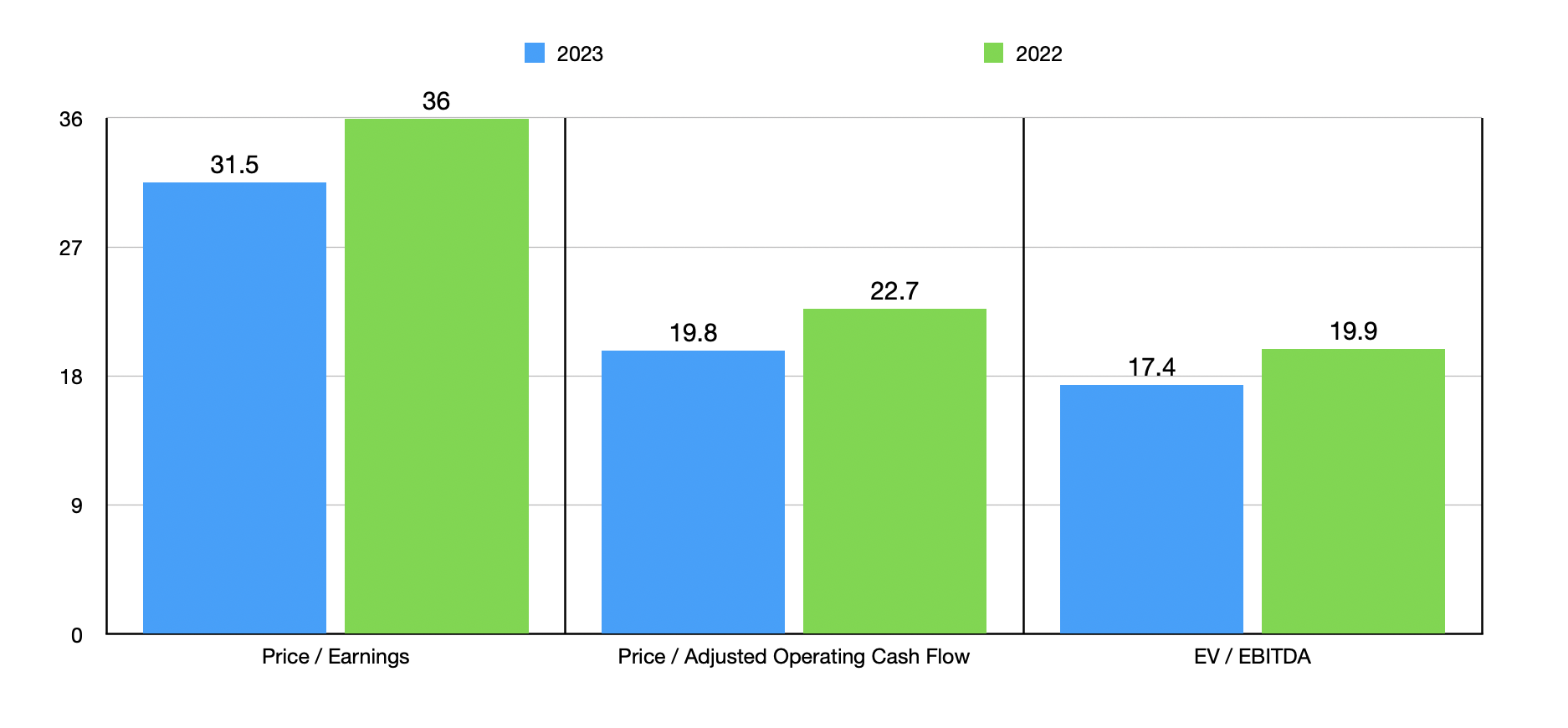

Taking these figures, we can easily value the company as shown in the chart above. The data there also covers what the company looks like if we value it using results from 2022. These results do assume a 7.7% drop in share price in response to this earnings news. The stock does look cheaper, but it's not cheap enough to pique my interest. In the table below, meanwhile, I decided to compare Five Below to two other discount retailers. Using both the price to earnings approach and the EV to EBITDA approach, I found that it was the most expensive of the group. However, it does fall in between the two players if we use the price to operating cash flow approach.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Five Below |

| 31.5 |

| 19.8 |

| 17.4 |

| Dollar General ( DG ) |

| 14.9 |

| 20.5 |

| 10.1 |

| Dollar Tree ( DLTR ) |

| 22.6 |

| 13.7 |

| 12.0 |

In my opinion, it is vital to factor in future growth planned by management. You see, the firm does currently expect to grow the number of locations that it has in operation to roughly 3,500. That would be, according to management, the point of market saturation. In the table below, you can see a few different metrics ranging from 2018 through 2022. First, you can see the number of new stores opened each year. Second, you can see the number of stores that the company had in operation at the end of each fiscal year. And finally, you can see the average revenue per store that the business has generated in each of those years.

{kind=link}

The last of these metrics is a bit tricky sense the timing of store openings will impact revenue for any given year. However, the numbers over that five-year window are close enough to be valuable for analyzing the company moving forward. It is worth noting that the revenue per store implied for 2023 is $2.295 million. So that is right in the ballpark of what we've seen over the past five years.

{kind=link}

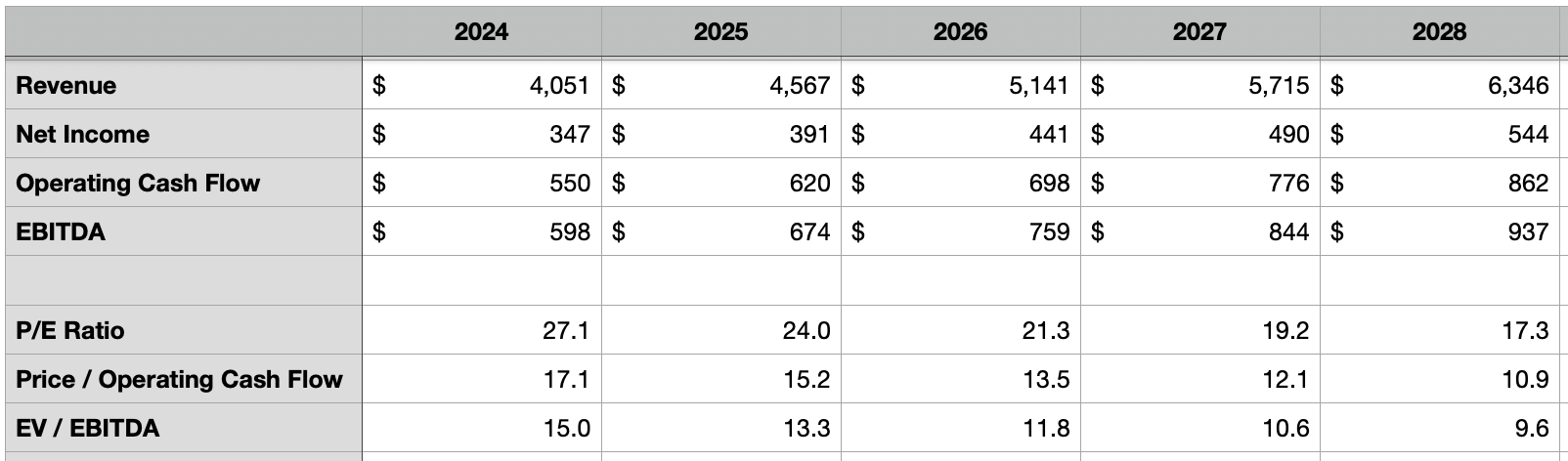

In the table above, I then forecasted out how many stores the company might have in any given year between 2024 and 2028. Even though the number of new stores added each year did bounce around a bit, the overall trend from 2018 through 2023 is for increases as the company grows. So the numbers shown in that chart or what I believe to be reasonable assumptions, and they are not based on any data provided by management. You can also see the total store count included in that. In the table below, meanwhile, you can see what the revenue would be for the company in these instances. Included in that would also be through the three different profitability metrics that I analyzed the company with, followed by the trading multiples of the firm for each of those years given current pricing. What this shows is that, to me at least, the stock won't become priced at an attractive level until sometime in 2025. So that implies that, absent something else changing like the firm's share price, investors might achieve only subpar returns between now and then.

{kind=link}

Takeaway

All things considered, I am a huge fan of Five Below from a business perspective. I think they have an excellent brand and management has done a great job growing the enterprise. Recent financial performance might not be pleasing investors at this time. However, I would argue that the company is likely to continue to grow and will almost certainly create additional shareholder value over time. But given how pricey the stock is, I do not think that it is any better than a 'hold' candidate at this time.

For further details see:

Five Below: Shares Still Aren't A Buy After Tanking