UMH - Flagship Communities REIT: Manufacturing Value Through The Cycle

2023-09-27 13:54:32 ET

Summary

- Flagship Communities REIT presents a unique opportunity for Canadian investors as the sole pure-play U.S.-based manufactured housing communities portfolio on the TSX.

- The U.S. manufactured housing sector has shown resiliency and generated positive growth, making it a defensive asset class.

- Flagship has the potential for organic growth through increasing average monthly lot rent and improving occupancy rates, as well as inorganic growth through acquisitions.

I am initiating coverage of Flagship Communities REIT (MHC.UN:CA) with a Buy rating and US$21 target. As the sole pure-play U.S.-based manufactured housing communities (“MHC”) portfolio on the TSX, Flagship presents a unique opportunity for Canadian investors. Favourable industry fundamentals and an experienced management team should enable Flagship to continue delivering outsized organic growth. Additionally, the resiliency of the U.S. manufactured housing sector , and Flagship’s strong debt profile position it favourably to weather potential economic headwinds.

Generally, MHC owners operate a land-lease business, renting lots inside their communities to residents who own or rent a manufactured home located on-site. Residents are responsible for all maintenance and repairs, and monthly utilities. The industry is supported by several key characteristics:

Affordability

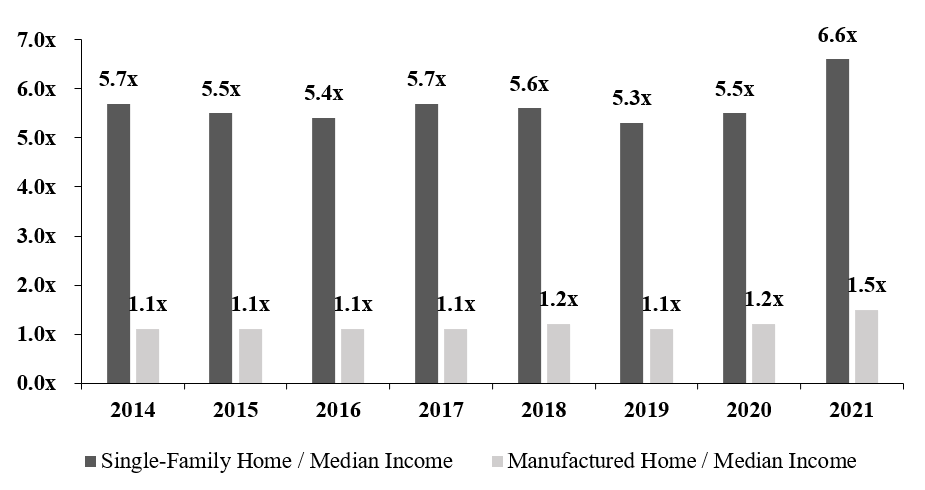

MHCs are one of the most affordable options for housing compared to apartment rentals and traditional single-family homes. This is an important factor in the context of the current inflationary environment and the shortage of U.S. housing supply. Better affordability should continue to support strong demand from low- and middle-income segments of the population, Flagship’s primary residents, that have been particularly pressured by the decreasing affordability of housing.

St. Louis Fed, U.S. Census Bureau

{kind=link}

Defensive Asset Class

Since 2000, the U.S. manufactured housing sector has generated positive same-property net operating income (“SPNOI”) growth in every year (including the GFC). Between 2002-2022, I estimate publicly traded U.S. manufactured housing players delivered ~5% average annual SPNOI growth (n.b., including Equity LifeStyle Properties (ELS), Sun Communities (SUI), and UMH Properties (UMH)).

Favorable Supply/Demand Imbalance

Supply is constrained by restrictive zoning policies, competing land uses, and tax considerations in Flagship’s markets. The zoning process for new MHCs is cumbersome and time intensive. Local governments are generally less familiar with MHCs and prefer multi-family and single-family developments. Furthermore, MHCs suffer from poor public perceptions about MHCs.

Most manufactured homes in the U.S. are titled as personal property and, therefore, generate lower tax revenues for governments compared to single or multi-family developments. Flagship claims no new communities have been developed within its markets in the past 15 years.

Roll-Up Opportunity

The MHC industry is highly fragmented. Despite attracting increasing attention from institutional players in recent years, the Manufactured Housing Institute estimates that the largest 50 operators account for only ~15% of the total market by lot count. Management’s industry expertise, coupled with Flagship’s operating platform will serve as an advantage in its consolidation strategy as vendors are often less sophisticated operators. This results in greater potential for Flagship to drive margin expansion and revenue in undermanaged communities following acquisition.

Strong Earnings Growth

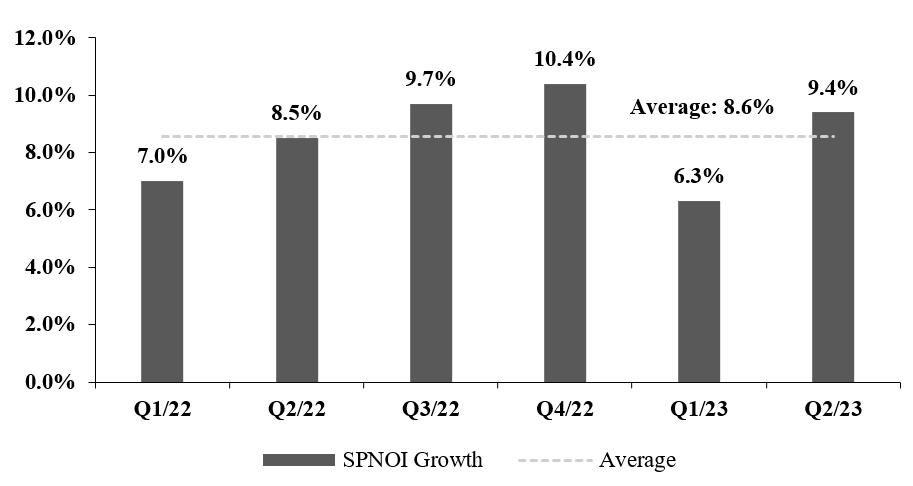

Since IPO, Flagship has generated positive SPNOI growth every quarter, with 2022 SPNOI growth of +8.6%, and YTD 2023 SPNOI growth of +7.8%. I believe the REIT can deliver high-single-digit SPNOI growth into 2024E on the back of continued lot rent growth (n.b., I anticipate a 4-5% increase in 2024E), occupancy upside, and a home ownership model which drives resident retention.

{kind=link}

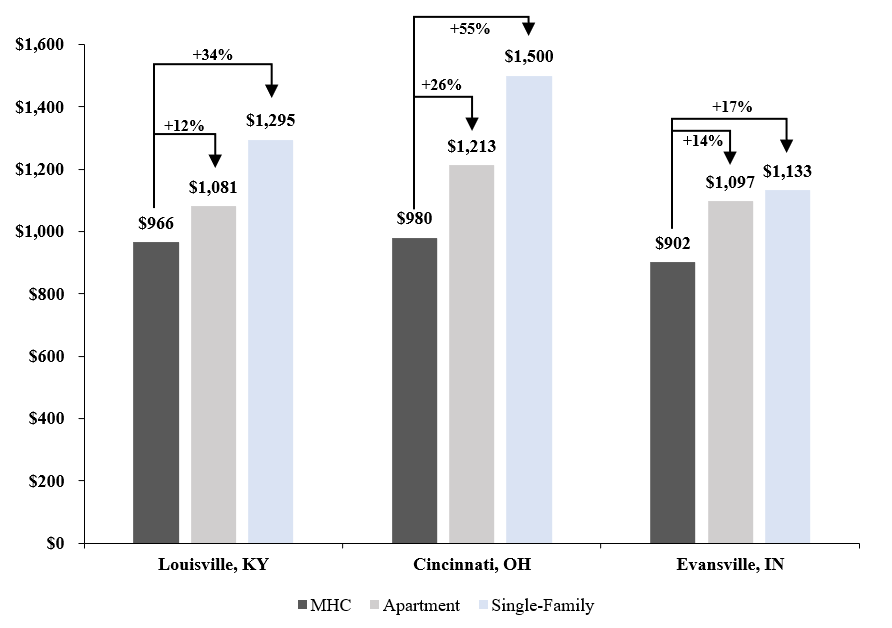

Lot rent growth is supported by the absence of rent control in any of its markets, and the affordability of its product. Competition for residents at Flagship’s communities is primarily from apartments and single-family rentals in the same geographic area, as these are the next most affordable options. Based on online rental listings, I believe the affordability gap is ~$200-$350 per month in favour of Flagship’s MHCs across its three largest markets (n.b., ~65% of total lots) compared to comparable apartments and single-family rentals.

Company reports, Apartments.com, Zillow

{kind=link}

My projections result in 2023E/24E/25E FFOPU of $1.20/$1.30/$1.39, which equates to a 2022-24E CAGR of ~10%, significantly higher than the Canadian REIT sector average of +4%, and U.S. MHC peers at +4%. With a conservative 2023E AFFO payout ratio of ~54%, I see opportunity for continued distribution increases, and I incorporate a 5% distribution increase by the end of 2023E, with another 5% bump in 2024E.

Finally, I believe management’s alignment (n.b., estimated ~14% ownership, ~26% control) and track-record, as well as Flagship’s attractive debt profile support the investment thesis. With no debt maturities until 2027, and no exposure to floating rates, the REIT is protected from the current interest rate environment. Furthermore, credit availability remains healthy for MHC industry in general, with a strong appetite from Fannie Mae/Freddie Mac and life insurance companies.

Company filings, author's estimates

{kind=link}

Company filings, author's estimates

{kind=link}

Portfolio & Growth Drivers

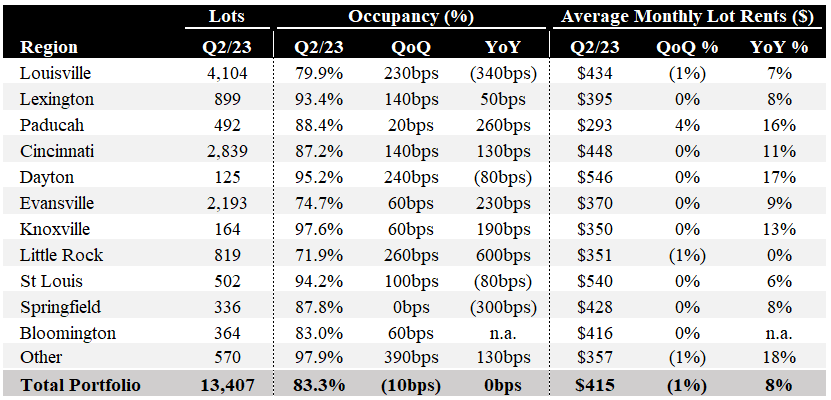

Since IPO, Flagship has continued expanding its footprint, executing on +$270MM of acquisitions. After acquiring three communities in Indiana, Arkansas, and Tennessee in May 2023 for $21MM, its portfolio contains 73 communities and 13,407 lots (n.b., +62% since IPO).

Flagship is one of the largest owners of MHCs in the U.S. Midwest, with its portfolio spanning seven states, with a significant presence Kentucky, Indiana, and Ohio. By MSA, Louisville (4,104 lots), Cincinnati (2,839 lots), and Evansville (2,193 lots) collectively account for ~65% of the portfolio. Within Flagship’s portfolio is one age-restricted community (55+), and two RV resort communities. Average monthly lot rent across the portfolio is $415.

Flagship’s resident base is roughly equally split between families, seniors, and empty nesters. Across its markets, employment is supported by manufacturing, transportation/logistics, and retail.

{kind=link}

Organic Growth Opportunity

Flagship has multiple levers for organic growth in the short and medium term. Continued growth in average monthly lot rent (“AMR”) in the REIT’s targeted range of 4-5% per year are realistic, given none of the REIT’s markets are rent controlled. With an in-place AMR of $415 as of Q2 2023, a 4.5% increase equates to about $15-$20/month in incremental cost for residents. This is reasonable, considering the REIT estimates ~70% of its residents own their home outright, without no mortgage (n.b., amortization periods on chattel financing for a manufactured home generally range from 12-15 years). Furthermore, the cost to transport a manufactured home to another community is prohibitively costly at $5,000-$10,000. For ~35-45% of Flagship residents on fixed incomes (e.g., social security, disability, etc.), the 2023 COLA for social security benefits was 8.7% (vs. 5.9% for 2022).

Company filings

Occupancy currently sits at ~83%, providing amble room for lease-up. MHC occupancy is considered stabilized at >90%. Flagship is also increasing resident retention via its home sales strategy, aimed at driving high levels of home ownership across its communities. It estimates its portfolio-wide turnover rate at ~15% annually. Owner-occupied units have turnover rates closer to ~5%. Owned units also have the benefits of smoothing NOI, as these turnovers mean a unit is sold resident to resident, with no interruption in rent or costs to the REIT. Conversely, turnover in rental units incur re-leasing costs and vacancy. At Q2 2023, Flagship had ~1,300 rental units (n.b., ~10% of total lots). I estimate every 100bps increase in occupancy would equate to incremental FFOPU of ~$0.02 (+1.5% vs. base 2024E outlook of $1.30).

Inorganic Growth Opportunity

Given the fragmented nature of the industry and pressure on small operators from higher rates, Flagship has a large opportunity to continue its strategy of acquiring communities to scale its platform. While M&A is an important factor in scaling the business, it will require disciplined capital allocation to preserve and create value given the current cost of equity (i.e., discount to NAV). Management has developed deep relationships with local operators, brokers, and other industry participants, which should improve pipeline visibility. Historically, many of Flagship’s acquisitions have been generated from bilateral relationships and contacts vs. competitive auctions.

With decades of experience, Flagship’s management team is sophisticated in a generally unsophisticated industry. This is a differentiating factor with respect to its M&A strategy. Flagship has been successful in achieving NOI margin expansion in acquired communities through labor efficiencies, submetering of utilities, and an emphasis on higher margin residents through its home sales strategy. It is notable that portfolio-wide NOI margins float around ~65%, while acquired communities often come with margins in the ~40-55% range.

Forecast

My 2023E-25E FFOPU estimates for Flagship are ~$1.2, ~$1.3, and ~$1.4, respectively, with AFFOPU estimates of ~$1.1, ~$1.2, and ~$1.2. This represents a 2022-24E FFOPU CAGR of 10% (n.b., manufactured housing peers average of +4%). My estimates are based on the following assumptions:

- AMR growth of ~4.5% in 2024E (n.b., 2023 increase of ~8%). Growth should be slightly lower than 2023 given the abatement of inflationary pressures.

- G&A expenses of ~$9MM p.a. (~12% of rental revenue). As the REIT scales, should be able to benefit from operating leverage.

- Interest expense of ~$14MM in 2023E, and ~$15MM in 2024E/25E. All of Flagship’s mortgages are at fixed rates, with no maturities until 2027. Interest expense should be comparable year-to-year in the absence of debt-financed M&A or material prepayments.

- No M&A is forecast.

- AFFO estimates account for normalized maintenance capex of ~$60/lot p.a. and ~$1,000/rental home per year, in-line with Flagship’s methodology (n.b., ~5% of NOI).

- 5% distribution increase in November 2022 to an annualized rate of $0.56 per unit, and further 5% increases in 2023E and 2024E. At current prices, the distribution implies an annual cash outflow of ~$12MM and a ~3.5% yield.

Net Asset Value

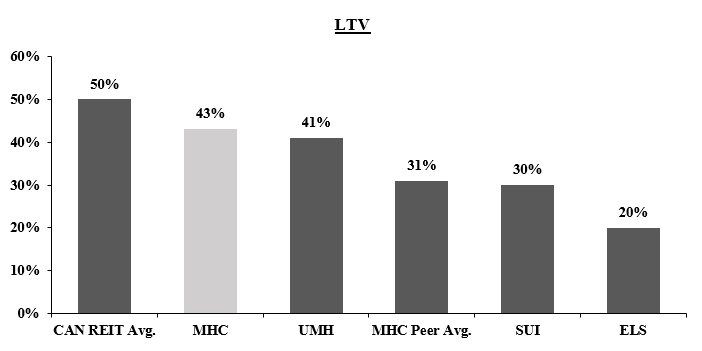

My NAV per unit is based upon a ~6% cap rate applied to NTM NOI, based on broker surveys. The NAV implies a total property value of ~$815MM (n.b., ~$59k/lot). Adjustments for other net assets and net debt ($349 million) result in a NAV of ~$470MM, or ~$22.3 per unit (n.b., including Class B units). This implies a ~28% discount to NAV, and a market-implied cap rate of ~7.2% (n.b., $50k/lot). Based on My NAV, LTV sits at ~43%. My year forward NAVPU estimate implies growth of 8% vs. +7% growth across the Canadian REIT universe.

Price Target

My price target of US$21 is based on a 15% discount to NAVPU. Over time, the discount to NAV should narrow as macro visibility improves, rates stabilize, and Flagship proves it can continue delivering above-average FFOPU growth. The main risks to this thesis are the REIT’s small market cap, limited float, and low trading liquidity.

Risks

Beyond the generic risks that apply to all REITs (e.g., competition for tenants, new supply, illiquidity, and economic and interest rate exposure), I believe there are the following risks specific to Flagship:

- Geographic concentration: Flagship’s assets are concentrated in a handful of U.S. states, predominantly Kentucky, Ohio, and Indiana. Its top three MSAs are Louisville, Cincinnati, and Evansville, which account for a combined ~65% of the REIT’s total lots. Local economic, regulatory, and political changes also present material risks to Flagship.

- Regulatory changes : As none of Flagship’s markets are currently rent-controlled, any movement by local governments to adopt rent control mechanisms for MHCs would be a significant risk. Additionally, changes in property tax treatment for MHCs, or environmental and zoning laws could impact the REIT’s occupancy, margins, and local supply/demand dynamics.

- Trading liquidity : Flagship’s trading volume is limited, and its market cap is quite small. This will preclude some institutional investors from holding Flagship’s units and may limit the units’ ability to close the value gap, and/or extend the time horizon required to reach the target price.

- Capital markets risk: As M&A is a cornerstone of Flagship’s strategy, it will require access to debt and equity capital markets. The higher current cost of debt and depressed unit price (discount to NAV) may make this more difficult.

- Generic M&A risk: The ability to improve operating performance (i.e., lease-up, cost reduction, etc.) is a key factor that allows Flagship to bid competitively on deals and meet return hurdles. As with any roll-up strategy, there are risks inherent to this value-add approach that may affect the success of integrating acquired assets.

- Natural disasters: Some of Flagship’s key markets are subject to the risk of natural disasters (e.g., tornadoes). This risk is mitigated by the fact that Flagship carries general liability insurance, property insurance, and loss of revenue insurance.

My main sell criteria would be any large, value-destructive unit issuance or a large acquisition financed with high-cost debt that significantly impairs the REIT's pristine debt metrics. I would also be concerned by any material management departures, though this may not be an automatic sell criterion.

Conclusion

Flagship remains a hidden gem in the TSX, being the sole pure-play U.S.-based MHC portfolio. Robust industry fundamentals and its seasoned management team provide a strong setup for exceptional organic growth with M&A upside. The inherent resilience of the U.S. MHC sector and Flagship's conservative balance sheet equip it to confront and thrive amidst potential economic challenges.

I personally believe that REITs like Flagship, with strong AFFO and FFO per unit growth and clean balance sheets, will be the first to catch bids once the market gains some certainty around the future path of interest rates. The defensiveness of the REIT and discount to NAV warrant my Buy rating, but I will be saving some bullets in case of further market volatility.

For further details see:

Flagship Communities REIT: Manufacturing Value Through The Cycle