AFMC - Flash PMI Data Signal Accelerating Developed World Economic Growth In March

2023-03-29 02:20:00 ET

Summary

- Economic growth accelerated across the four largest developed economies on average in March.

- However, growth is skewed heavily towards the service sector, with manufacturing continuing to suffer falling orders.

- The resilience of growth and elevated inflation rates suggests central banks will lean towards further policy tightening in the coming months.

Economic growth accelerated across the four largest developed economies on average in March, pointing to a surprising resilience of growth amid headwinds of higher interest rates, the cost-of-living crisis and recent stress in the banking sector.

However, growth is skewed heavily towards the service sector, with manufacturing continuing to suffer falling orders. While this weakness in demand has helped further drive down inflation in the manufacturing sector, March saw signs of stubbornly elevated service sector selling price inflation, and in some cases even accelerating inflation.

The resilience of growth and elevated inflation rates suggests central banks will lean towards further policy tightening in the coming months. But it remains to be seen whether growth resilience can persist as we await the lagged impact of prior rate hikes, including those seen in March, in an environment of squeezed incomes and increasing financial market uncertainty.

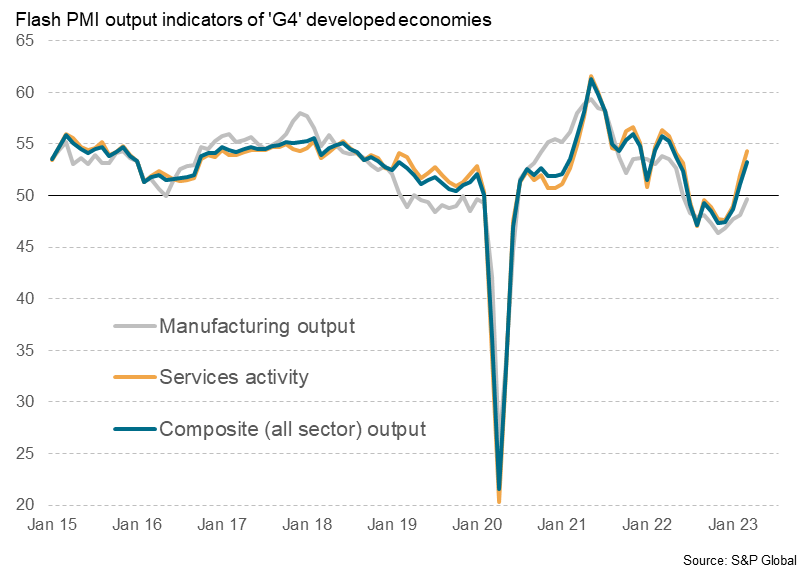

Economic growth revival driven by services

Business activity rose across the four largest developed world economies (the "G4") for a second successive month in March, according to provisional 'flash' PMI data, the rate of growth accelerating to the fastest since last May. The sustained upturn adds to signs that global recession risks have abated, for the near term at least, contrasting markedly with the gloomy picture presented by the surveys heading into last winter.

Moreover, growth was recorded in all four economies for a second month running, indicating a broad-based geographical improvement. Growth hit ten-month highs in both the US and the Eurozone, while a nine-month high was recorded in Japan. Although growth slowed slightly in the UK, it was nevertheless the second-best seen over the past nine months.

It was a different story by sector, however, with growth largely limited to the services economy. Measured across the G4, service sector business activity grew at its sharpest pace since last April, building on the return to growth seen in January. Accelerating services growth was seen in all four economies bar the UK, where growth was also recorded but at a reduced rate compared to February, linked at least in part to labour shortages.

Manufacturing, on the other hand, saw output fall for a ninth successive month in March, dropping in all four economies bar the US, where a modest gain was reported. While the rate of decline moderated, this was in part due to improved supply availability rather than an upturn in demand for goods, with new orders falling in manufacturing for a tenth straight month, contrasting with improved demand growth for services.

Flash PMI output indices

{kind=link}

{kind=link}

{kind=link}

Source: S&P Global, au Jibun Bank, CIPS

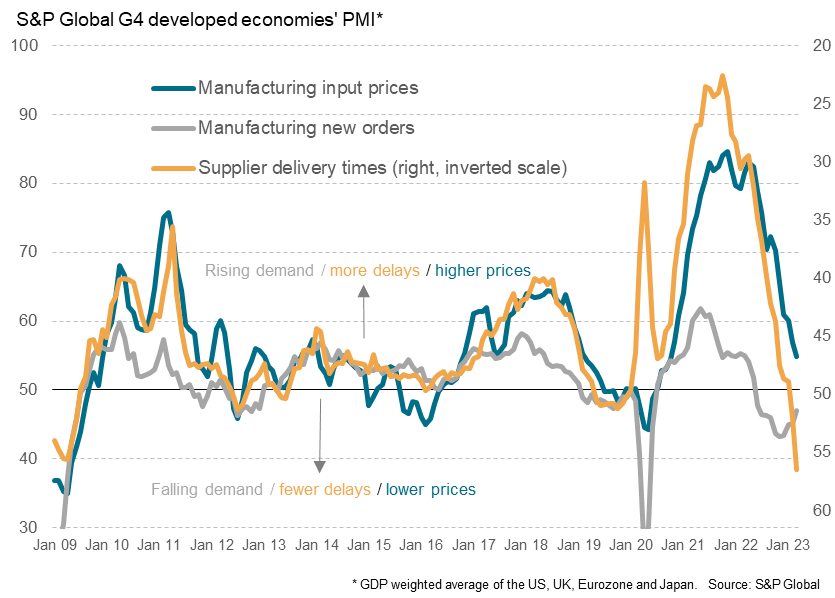

Unprecedented improvement in supply conditions

The improvement in supply conditions during the month was especially notable, as average supplier delivery times shortened to the greatest extent seen since comparable survey data were first available in 2007.

Faster deliveries reflecting an alleviation of pandemic-related logistical issues such as container shortages and port congestion, as well as the reopening of the Chinese mainland economy.

However, suppliers were also less busy simply because of reduced demand for inputs from manufacturers around the world, in turn exacerbated by an ongoing trend towards inventory reduction. Stocks of inputs and other raw materials fell in March across the G4 for a fifth month in a row.

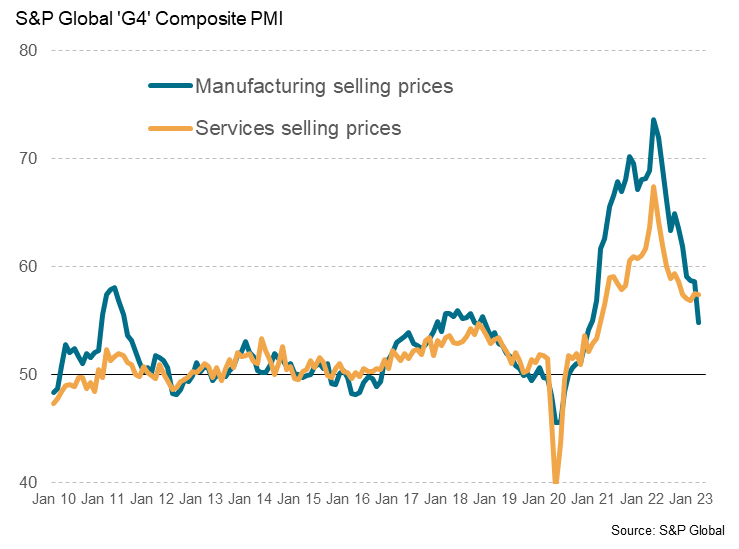

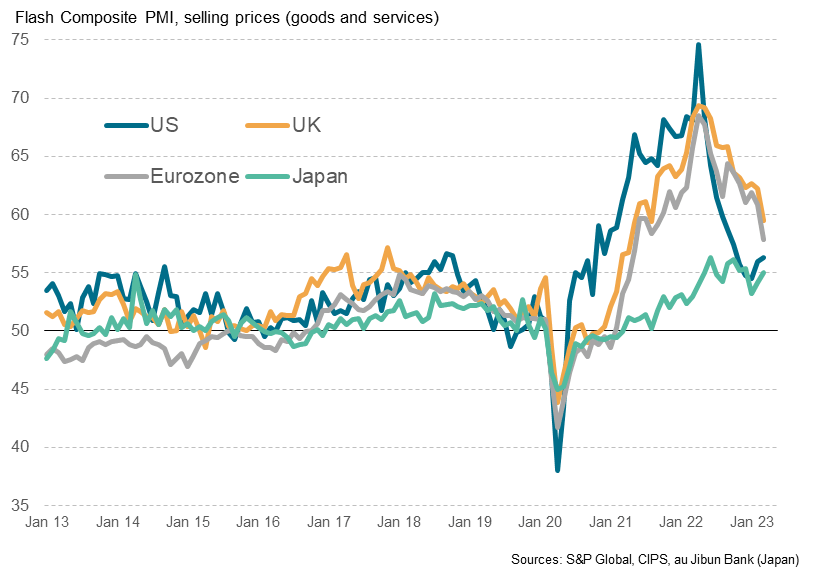

Price pressures driven by services

A corollary of more plentiful supply and falling demand was a further reduction in price pressures in the manufacturing economy. Input prices rose on average across the G4 at the slowest rate since October 2020. Factory input prices even fell in the eurozone, where lower gas prices have helped further alleviate cost pressures in recent months.

G4 flash PMI factory input costs and supply chains

{kind=link}

The reduced upward pressure on raw material prices helped drive a slower rate of inflation for goods leaving the factory gate on average across the G4, with manufacturing output prices rising at the slowest rate since December 2020.

However, while the G4 service sector as a whole also saw cost growth moderate further on average, prices charged for services rose at a slightly increased rate for a second month running in March.

Higher rates of inflation were evident in the US and Japan and, although rates slowed in Europe (in part reflecting the gas price cooling), all four economies continued to see elevated rates of service sector selling price inflation.

Moreover, combined gauges of goods and services selling price inflation also consequently rose in both the US and Japan in March, and remained especially elevated in the Eurozone and UK, albeit down sharply from the peaks seen in the immediate aftermath of the invasion of Ukraine.

Selling prices

{kind=link}

{kind=link}

Outlook

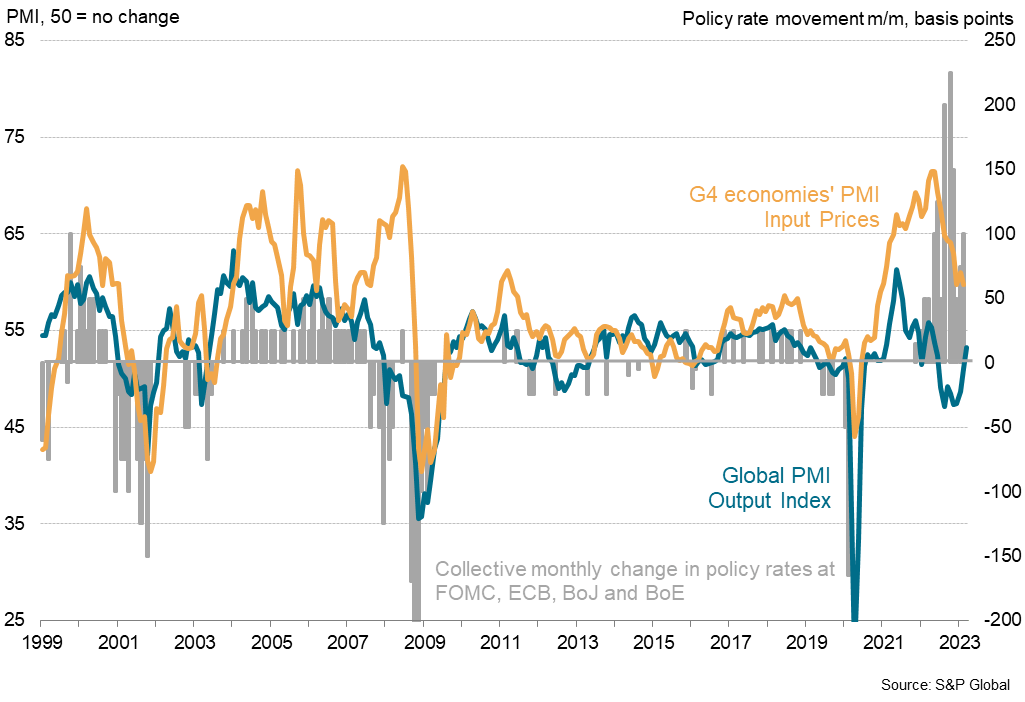

The March flash PMI data therefore point to encouraging resilience of economic growth across the four major developed economies, with output growth accelerating in the first quarter despite uncertainty caused by recent banking sector stress (the latest survey data were collected after 10th March) and despite the further tightening of monetary policy.

However, while the hiking of interest rates appears to have further helped cool inflationary pressures, aided by lower energy prices, a further 100 basis points of tightening in March by the combined major central banks of Europe and the US looks set to pose additional headwinds to demand in the months ahead.

The stubbornly elevated price gauges also imply a strong possibility of further rate hikes in the coming months, especially when viewed in light of the resilient current growth picture.

Thus, while recession appears to have been averted for now, there remains a strong possibility of substantially weaker economic growth later in the year as the lagged impact of higher interest rates feeds through to the economy, at the same time that the cost-of-living crisis has eroded real incomes and uncertainty surrounding the banking sector haunts markets.

The latter poses an especially important downside risk to growth, and will inevitably play a key role in determining the future path of demand as well as future policy decisions.

PMI data vs. central bank policymaking

{kind=link}

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Flash PMI Data Signal Accelerating Developed World Economic Growth In March