FNNTF - flatexDEGIRO: Q2 Will Likely Show A Further Slow Down

2023-07-06 14:26:44 ET

Summary

- Q2 earnings will likely show a further reduction in commission income.

- Driven by the ECB rate increases, interest income should go up and partly compensate for the reduced commission income.

- There are no signs of a deposit outflow even though flatexDEGIRO pays zero interest on deposits.

- The proposed EU ban for payment for order flow will be beneficial to flatexDEGIRO in the mid- to long-term as it will affect the business models of some competitors.

- flatexDEGIRO seems valued fairly, and as there is no immediate growth catalyst in sight, there is no compelling reason to buy the shares.

(Note: all amounts in the article are in EUR. At the current exchange rate 1 EUR is around 1.09 USD.)

Investment thesis

flatexDEGIRO (FNNTF) Q2 2023 earnings will likely show a further reduction in commission income, based on the monthly KPIs the online broker has been publishing.

The total number of customer transactions - the most important driver of revenue for flatexDEGIRO - has been 22.6% lower in H1 2023 than in H1 2022 (which was itself already significantly lower than 2021). This will be partly, but not fully compensated for by higher interest income due to the ECB interest rate increases.

The online broker assumes commission income of 265mn euros and interest income of 100mn euros for 2023. In total it looks like flatexDEGIRO will achieve Q2 2023 earnings in line with this guidance.

With a P/E ratio of around 9x shares do not look expensive. But the lack of growth and the clearly cyclical nature of the online brokerage business do not give enough reason to buy. Therefore, the Hold rating is confirmed.

Quick recap of my previous coverage

I have covered flatexDEGIRO first in December last year, flatexDEGIRO: Don't Buy The Long-Term Growth Story , and then with an update in February and April . Back in December the shares had fallen significantly because of repeated downside earnings revisions and a disastrous regulatory audit. I argued that, although shares might look cheap, investors should be careful if they wanted to buy the dip.

flatexDEGIRO positioned itself as a growth company and its so called Vision for 2026 was to have 7-8mn customer accounts and 250-300mn annual customer transaction by the year 2026. I questioned whether this was achievable as it would require the growth rates of the pandemic years 2020 and 2021 to continue for at least five more years. My view was that those were exceptional years which flatexDEGIRO cannot repeat easily.

Given where we are now with customer accounts growing only in the single digits and customer transactions actually decreasing over the last quarters, I think it is fair to say that my view has so far been validated.

Performance on KPIs in Q2

As not everybody agreed with me though, I keep checking back and I also wanted to examine the recent Q2 performance numbers to see whether things have changed.

Since the beginning of this year flatexDEGIRO has been publishing quite detailed monthly performance numbers on its KPIs. This is very useful as we do not have to wait for the quarterly numbers to understand the trajectory of the business and can try to predict quarterly earnings before they are announced.

Customer account growth

QoQ customer account growth slowed down somewhat to 60,000 in Q2, but this is still in line with a stable, but slow growth over the recent quarters:

flatexDEGIRO - QoQ customer account growth (Source: Bellasooa Research based on company data)

Unfortunately, the growth in customer accounts does not result in more transactions which drive flatexDEGIRO revenue and income.

Customer transactions

The number of transactions was only 13.6mn, 18.5% less than in Q2 last year, and also clearly below the quarterly average.

flatexDEGIRO - QoQ transactions (Source: Bellasooa Research based on company data)

The average number of transactions per quarter in 2022 was 16.75mn, the average in 2023 so far is just 14.75, so 11.9% lower. We have to go back to 2019 to see quarterly transaction numbers in that low area.

flatexDEGIRO - Average quarterly transactions (Source: Bellasooa Research based on company data)

It is quite unlikely that the online broker can make up for this in the second half of the year, so the decrease in customer transactions will probably continue for a second year.

Interest income

Due to its EU banking license (in Germany), flatexDEGIRO can put costumer deposits to use and create additional interest income. The increased interest rate environment makes this part of the business more and more lucrative for the online broker.

Of the 100mn interest income that are forecasted for 2023, 36mn should come from margin loans. The margin here is assumed to be 4%, on a loan volume of 900mn euros. In the first half of the year the total was around about 900mn in every quarter. So this is positive as it meets the guidance.

It is possible that flatexDEGIRO could make more margin loans, but is restricted by capital requirements to do so. The company uses the rest of the available customer cash (which it calls Treasury portfolio) for deposits at the European Central Bank, and accrues interest for that.

The business model here is remarkably simple. flatexDEGIRO takes the customer cash and deposits it at the ECB which pays an overnight interest rate. This is in essence what Matt Levine from Bloomberg refers to as narrow banking - take deposits, but do not use them to make loans to customers; just give the money back to the central bank which pays interest.

In its financial guidance for 2023 flatexDEGIRO assumed a Treasury portfolio of 2.5bn with an average yield of 2.5%.

Every time the ECB increases the overnight deposit rate by 25 basis points, flatexDEGIRO has about 6.25mn euros increased interest income (on an annualized basis). After the rate hike on June 21 the yield is already now 3.5% (flatexDEGIRO pays no interest to the customer), 100bps above the target. With 2.6bn the portfolio size was marginally larger at the end of Q2, so - if things stay this way - on an annualized basis the interest income should be around 25mn euros higher than planned.

Investors should be aware though that these gains may be temporary, and they will move the other way once interest rates go down.

I do see the stable or slightly increasing customer deposits as a positive. There is significant competition for customer deposits across Europe - from banks, but also other brokers. flatexDEGIRO still does not pay interest on customer deposits, so I would not have been surprised if deposits would have gone down over the quarter. But this has not happened (yet).

Positive regulatory developments

The online broker seems to be making progress with the remediation of its regulatory issues.

On June 16 flatexDEGIRO reported that the BaFin, the German financial services regulator, has reduced the SREP (Supervisory Review and Evaluation Process) capital requirements for flatexDEGIRO Group by 75 basis points from 5% to 4.25%. BaFin had increased the capital requirements after a quite negative process audit in 2022.

Another positive development for flatexDEGIRO is that the EU agreed on a ban for payment for order flow . This is a practice through which brokers receive commission payments for forwarding customer orders to specific trading platforms. The practice is widely used by neo-brokers like Trade Republic (often in conjunction with a nominal zero-fee policy), but flatexDEGIRO has only very little revenue tied to it. In November 2021 flatexDEGIRO had issued a statement saying that only 3% of revenue came from the practice, and I do not think that this has changed.

In that statement flatexDEGIRO said it expects to profit from a decision to ban payment for order flow:

flatexDEGIRO would rather expect such a decision to have a substantially positive effect on its business development, driven by presumably necessary price adjustments of peer companies that mainly or solely rely on payment for order flows in order to offer allegedly low trading fees.

There will no immediate benefit though. The deal, which still needs formal approvement from the EU parliament and individual EU countries, says that member states which currently allow the practice can continue doing so until June 2026.

Valuation

flatexDEGIRO trades with a forward-looking P/E ratio of around 9x at the moment. After the predictable bounce-back from the lows of around 6 euros in December, shares have been moving in a range of 7 to 10 euros since.

A P/E ratio of 9x might seem low if you see flatexDEGIRO as a profitable and fast growing fintech. But I do not think this is what flatexDEGIRO is. It is a specialty financial services company with a cyclical business and a steady, but low growth.

Both its income streams are cyclical. Commission income depends on the trading activities of private customers, and it is at a cyclical low at the moment. Interest income depends directly on central bank interest rates and is at a cyclical high.

Additionally, due its regulatory issues and the current undercapitalization, the online broker needs to retain profit and is not able to pay a dividend or buy back shares. This situation will not change until at least next year.

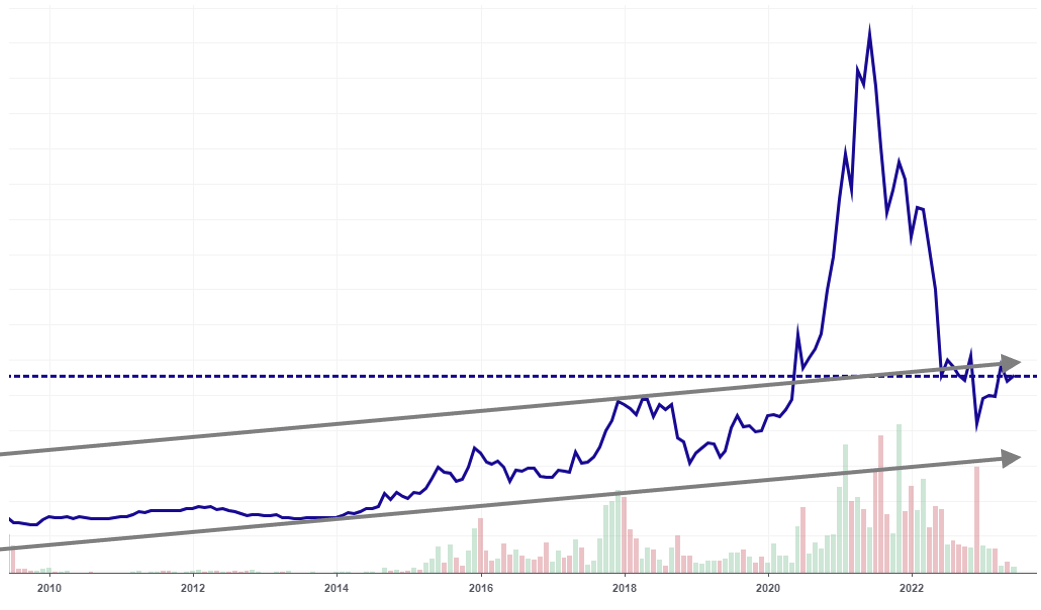

Long-term upwards trend seems intact

That being said, if you step back and look at the bigger picture of the share price, you will notice that a long term upwards trend is still intact. You just need to discard the exceptional development during the pandemic.

{kind=link}

With this long-term view, I think the Hold rating is appropriate.

Risks

I have already mentioned the regulatory issues. flatexDEGIRO had a disastrous BaFin audit last year and as a result had to pay a fine of 1mn euros and, which hurt more, capital requirements were increased significantly.

I think the audit is a temporary issue, and the online broker is working through it. As mentioned above, this is being recognized by the regulator who reduced the capital requirements again (they are still higher though than before the audit). So, this should not come back.

On the income side, I do not see significant downward risk. Customer transactions are already at a cyclical low. Unless flatexDEGIRO loses customers, which has not happened before, they should not go down much further. The EU ban of payment for order flow is favorable in the long-term to flatexDEGIRO as it negatively affects the business models of key competitors like Trade Republic, who have shown stronger customer growth based on a zero-fee model.

Interest income is fairly predictable and will continue to go up at least for a while in line with increasing rates. A key risk here are deposit outflows. flatexDEGIRO does not pay interest on customer deposits and with interest rates of up to 3% on savings accounts across Europe, deposit outflows are possible. This would reduce interest income. So far it has not happened, my explanation would be that the deposits, while in total 3.5bn euros, are maybe small as an average across accounts. Therefore the incentive for an individual customer to move the money out of the account is relatively small.

Conclusion

I expect Q2 earnings to be mostly in line with previous guidance. Reduced commission income should be partly compensated by higher interest income.

Although shares are not expensive, flatexDEGIRO seems fairly valued given the cyclical nature of the brokerage business. A return to higher growth rates is not visible and, despite the positive regulatory developments, I still do not see a compelling reason to buy.

For further details see:

flatexDEGIRO: Q2 Will Likely Show A Further Slow Down