FNNTF - flatexDEGIRO: Regulatory Matters Don't Justify Depressed Valuation

Summary

- flatexDEGIRO reported a good financial performance in 2022, despite a challenging operating environment.

- Its strong customer growth in the recent past bode well for its growth prospects.

- Regulatory shortcomings don’t seem to be a major issue and have created a mispricing situation, given that flatexDEGIRO trades at only 8.4x earnings.

flatexDEGIRO ( OTCPK:FNNTF ) is currently trading at a very depressed valuation, largely driven by regulatory issues, while its operating performance has remained strong. For long-term investors, it remains a compelling growth play in the European financial sector.

As I’ve covered in a recent article , flatexDEGIRO is an interesting growth play in the European financial sector, due to a good competitive position in the European brokerage industry and an attractive valuation. However, its share price performance has been negative since then, mainly due to some regulatory issues raised by the German financial watchdog, which spooked investors.

As the company has recently presented its 2022 financial results and addressed its regulatory issues, in this article I do an update on flatexDEGIRO’s investment case taking into account the recent developments.

Recent Earnings & Regulatory Issues

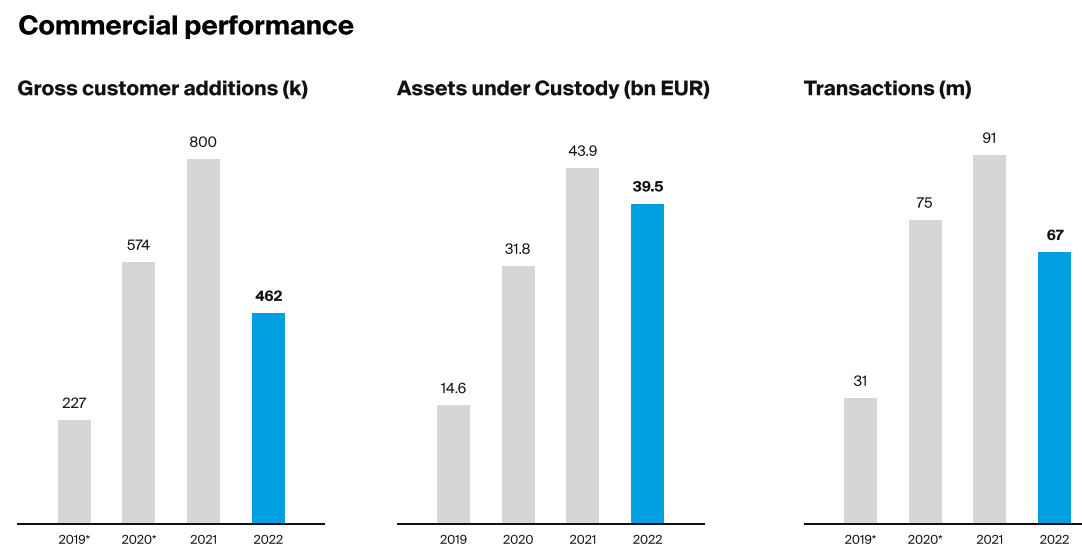

flatexDEGIRO is the largest pan-European online brokerage company, being present in about 16 European countries, after recently decided to exit Norway and Hungary. At the end of 2022, the company had more than €39 billion of assets under custody, and about 2.4 million customers.

During the past year, flatexDEGIRO’s operating momentum was negatively affected by weaker equity markets, which led to lower customer activity and therefore decreasing fee income. This was a trend that affected the whole industry, and flatexDEGIRO was as expected not immune to it.

{kind=link}

Trading activity (flatexDEGIRO)

This lower activity background led to lower transactions settled compared to the previous year, while the company raised transaction fees to offset to some extent lower volumes. Indeed, its average commission per transaction was €4.06 in 2022, compared to €3.73 in 2021, which represents an increase of almost 9% YoY. Despite lower customer interest in the equity market and higher fees, flatexDEGIRO’s churn rate was only 2.2% in 2022, and the company was able to increase its net customer count by some 400,000 in the year. This is still quite good considering the challenging market environment, and more than what its closest four European competitors were able to gain together during 2022. Moreover, its net cash inflows amounted to €5.9 billion in 2022, a very good achievement in a tough year.

{kind=link}

Key metrics (flatexDEGIRO)

On the other hand, rising interest rates were a tailwind for total revenue, generating some €72 million in interest income during the year (vs. virtually zero in the previous year), being an important factor for flatexDEGIRO to report a decrease of 3% YoY on annual revenue, to €407 million in the past year.

Nevertheless, due to higher costs its adjusted EBITDA was €145 million in 2022, representing a decline of 18% YoY. A significant part of higher costs was the company’s marketing campaigns at the end of 2021 and in the first two quarters of 2022 related to its documentary ‘True Stories of Investing’, while in the past two quarters its quarterly marketing expenses returned to more ‘normal’ levels.

{kind=link}

Marketing costs (flatexDEGIRO)

Not surprisingly, flatexDEGIRO’s adjusted net income decreased to €79 million in 2022 (-18.5% YoY), while its reported net income was €106 million. This difference is justified by the release of provisions related long-term employee incentive plans, thus the best metric to analyze the company’s underlying performance is adjusted net income.

Net income (flatexDEGIRO)

Regarding its guidance for 2023, flatexDEGIRO does not aim to increase fees during the year and expect an average commission from trade of €4.10, and is being conservative on volumes expecting to settle about 65 million transactions in the year. This leads to about €265 million in commission income, a decline of 2.5% YoY, while interest income should be around €100 million (+38% YoY) due to higher margin loans and treasury income. Its total revenue is expected to be around €380 million (-6.6% YoY), which seems to be conservative as customer activity has recovered in the first two months of 2023, and is below current consensus of around €398 million.

Nevertheless, its EBITDA margin is expected to be about 40% (vs. 36% in 2022), as the company is likely to maintain strong cost control, while its net income should be around €85 million (+7.6% YoY).

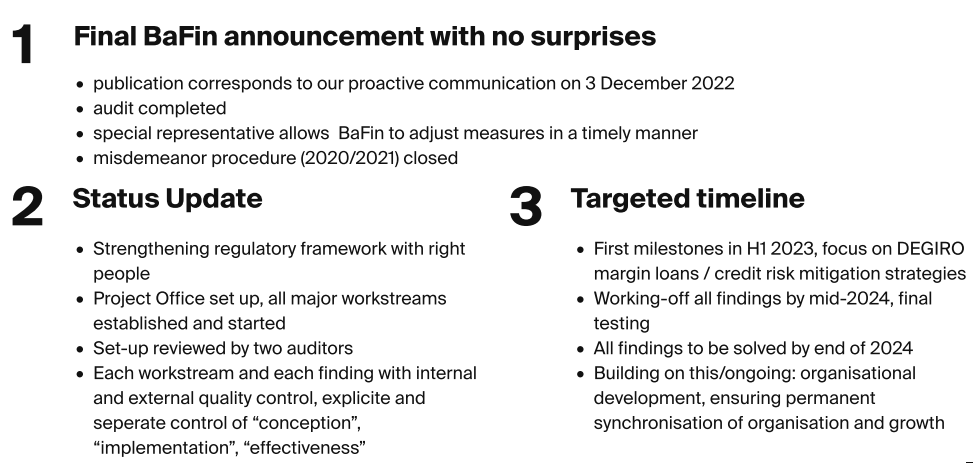

Regarding its regulatory issues, flatexDEGIRO announced back in December that it was working to address some shortcomings raised in an audit by the German regulator. This was related to the risk mitigation processes regarding margin loans issued by DEGIRO and the audit is now completed, resulting in the company being fined by more than €1 million due to infringements in 2020/2021.

flatexDEGIRO is working to address the deficiencies identified over the coming months, and a new follow up audit is expected after 12-24 months, thus this is a risk that investors should be aware of, even though the financial impact is likely to be rather low. Investors should note that when flatexDEGIRO reported this issue in December its shares declined by 37% on that day to €6.78 per share, which was clearly an overreaction, and have since then recovered to more than €8 per share, but still trades below its share price when this issue was announced.

{kind=link}

Regulatory issue update (flatexDEGIRO)

Going forward, flatexDEGIRO’s growth strategy is expected to remain focused on organic growth by gaining market share to incumbent brokerages, while prioritizing profitability at the same time by reducing expenses and improving business efficiency. While the current operating momentum remains highly uncertain, as customer activity is difficult to forecast and is highly dependent on investor sentiment, the company’s long-term growth prospects remain good considering its strong track record of sustainable customer growth.

Conclusion

flatexDEGIRO reported a resilient performance in 2022 despite the challenging market environment, with its strong customer growth being a very good sign about the company’s strong position in the brokerage industry in Europe.

Due to regulatory issues, its shares are currently trading at only 8.4x its earnings, at a significant discount to its peers that trade on average at about 20x earnings. Additionally, its own historical average over the past five years is close to 16x earnings, showing that flatexDEGIRO is clearly undervalued and a good growth play for long-term investors within the European financial sector right now.

For further details see:

flatexDEGIRO: Regulatory Matters Don't Justify Depressed Valuation