FNNTF - flatexDEGIRO: Up Over 30% Since My Last Coverage

2024-01-13 02:03:18 ET

Summary

- I've invested in growth stock flatexDEGIRO and expect market-beating returns in the long term.

- flatexDEGIRO is a player in the fragmented European investment market and has the potential to expand and dominate.

- The company has shown strong financial performance, with record-level numbers in EBITDA and net inflows of almost €4B.

Dear readers,

You may, if you follow my work, be aware of my reticence when it comes to investing in growth stocks. I rarely do this. However, when I do, I do so with a very long-term sort of timeframe, allowing the company to really grow beyond what the market expects it to, and provide some market-beating returns.

Such is the case with my investment in flatexDEGIRO (FNNTF). If you call, I wrote on this company all the way back in July of last year, and I did so with a "BUY" rating. I also went ahead and bought company shares - quite a few of them over the following weeks, until where I had a respectable 0.5% position in this European broker.

When I invest in growth stocks, I prefer smaller companies in excellent positions, like Seafire AB, a Swedish company in which I made a 400% return on investment. This company has not yet provided that return - but it has provided over 30% RoR in less than 6-7 months, which is an impressive annualized rate of return.

This is an update article, and you can find the company's initial coverage in this article - let's look here for the latest update, and what you can expect from flatexDEGIRO in this year.

Updating on one of my very few growth stock investments - flatexDEGIRO

So, this is one of the extremely few growth businesses you'll currently find me investing in. A stock that does not pay a dividend, or the appeal hinging entirely on capital appreciation is not an investment I make lightly, often or without having a clear goal for the position or the company.

As I specified in my last article on the company, flatexDEGIRO is a player in a very fragmented investment market, namely the European investment market, which has few large players. The players that exist and are large are typically local , such as the ones I use with Nordnet and Avanza - but we really don't have any "Schwabs" here that have large market positions with pan-European coverages, and above all, dominance.

The closest you'd come to that, I'd say, is Interactive Brokers (IBKR).

I like investing in brokers and in stock market operators, as evidenced by my coverage of Deutsche Borse (DBOEY) and similar companies. Investing in brokers is, in my view, or in stock market companies, a good idea, because much of Europe is still a largely untapped market with plenty of upward potential with new customers and new investments.

It's this market that the company intends to address. Flatex purchased DEGIRO not that long ago, meaning we have a situation where this company that has less than $1,000M in market cap does over 90M transactions on a yearly basis, or over 375x its market cap in transaction volume, and I believe the company likely to expand from this.

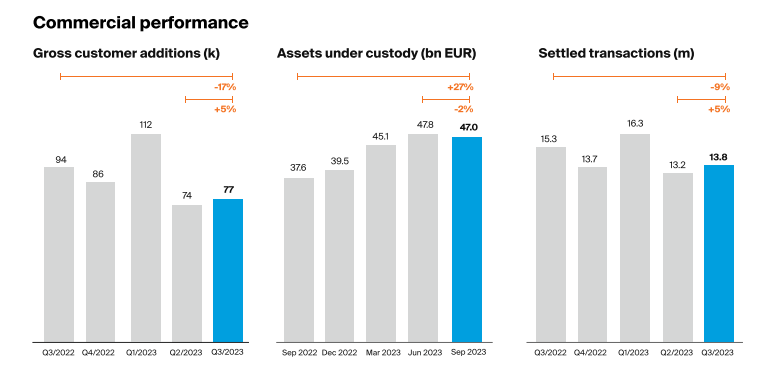

The latest set of results we have to look at are the 3Q23 results, which continued to see over €100M+ in quarterly trading revenues despite quite an anemic overall market. It also saw the company delivering record-level numbers in EBITDA since meme-stock mania back in 2021, and a strong overall benefit from higher interest rates. Remember, financial companies, by and large, earn both in low-interest as well as high-interest environments. The company also managed to grow its customer core, despite all that's ongoing.

Here is the commercial performance that the company managed in the last quarter.

flatexDEGIRO IR (flatexDEGIRO IR)

{kind=link}

Not bad, given the overall macro we're looking at here, I'd say. And there seems to be plenty of more upside as well to be had. The company recorded net inflows of almost €4B, which the company has invested in its entirety already.

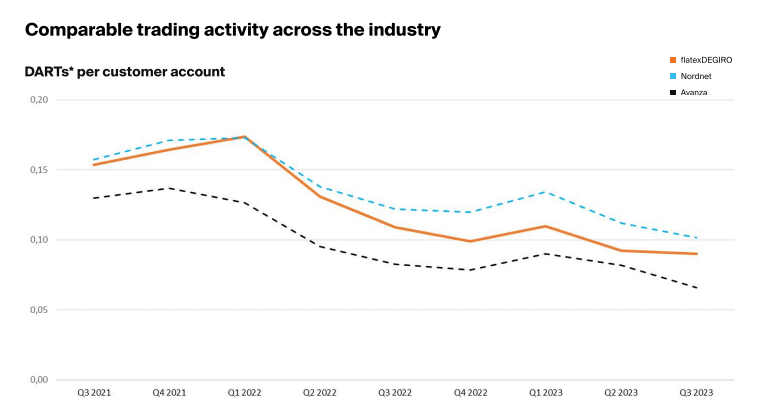

An important KPI to keep a look at here is the so-called DART's, or basically daily activity in terms of trades on a per-user basis. While Nordnet still has a leading market position, Degiro has caught up and Avanza keeps dropping on a comparable basis.

flatexDEGIRO IR (flatexDEGIRO IR)

{kind=link}

There are no real worrying signs in terms of commission income patterns, in terms of adjusted revenues, in terms of interest income (which is growing significantly). On a per-trade or transaction basis, the commission is up, meaning either the company is managing to charge more, or the users are trading in a more favorable pattern. At a growth from around €4/trade to €4.25/trade, this is not a small change either. EBITDA is also in a growth trajectory at this time, with relevant adjustment only for stock appreciation rights, or SARSs, and those, unlike many stocks with a lot of stock-based comps, are actually mostly executed as of 9M23.

That's another reason I like the company. Not as much of that as we see in other growth-based companies.

Overall, there are very few worrying signs in flatexDEGIRO at this time., to a degree where I would argue that the overall upside to my thesis that I spoke of in my last bullish article is still very much there.

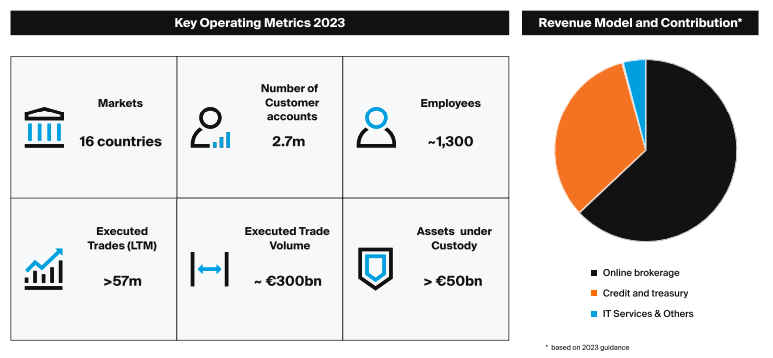

The company operates one of the leading - and growing - online brokerage platforms in Europe. While I love IBKR for its breadth of service and wide flexibility, I also believe this platform to be far more user-friendly. The company, at this time, is executing over 57M paperless security transactions in Europe in 2023 to date with over 2.7M customer accounts. If you take even a quick, cursory look at where the population numbers put the TAM here, you'll realize that the company has the potential to grow far, far, more than that.

flatexDEGIRO IR (flatexDEGIRO IR)

{kind=link}

Its M&A of DEGIRO in 2020 means that it's now the largest retail online brokerage in Europe, and this is certainly part of the current "trend", with ongoing consolidation of banking and finance, which makes it well-positioned for further growth.

The company has one of the best product offerings of any competing broker in the area here, fully integrated with investment banks, ETF providers, Fund managers, and operations for digital wealth management and the like. The company's core markets of Germany and Austria are only the beginning, and I remain in a positive position about the potential of being part of this company's growth.

Let's look at what sort of Risks and upsides we have for the company here.

Risks & upside to flatexDEGIRO

The primary risk to flatexDEGIRO that I currently see is the operational risk that the company does not grow according to its projections. Unlike most of the other growth companies out there, and this should not surprise you if you follow my work , I do not invest in overvalued growth.

flatexDEGIRO is not an overvalued growth stock. The company trades at a conservative multiple (more on that later). Because of that, most of the risk is found in whether the company actually manages to grow as it expects - which in turn is tied to quite a bit of macro and consumer behavior, which can certainly change.

The fact that the company also doesn't pay any sort of dividend is a secondary risk here, and not necessarily a small one, because your entire upside is the capital appreciation of the company. I do not view it likely in the least that this company is going to start paying dividends.

Long-term investors in the company have done well. Those who bought it during meme-mania have not, having lost more than 60% of their invested capital since the peak back in -21.

I did not buy at that time.

The upside is if the company meets its growth trajectory, at which point I believe a 13-15x P/E is not a "strange" thing for a company such as this. And valuation, as I see it, dictates that this company actually has an upside still, despite going up 30%+.

flatexDEGIRO valuation - There remains a market-beating upside potential here

Betting against his company has been a bad idea. This is shown by the RoR since my last article.

Seeking Alpha flatexDEGIRO RoR (Seeking Alpha)

The question becomes, what upside remains here?

I say "quite a bit".

If we assume that flatexDEGIRO manages its growth estimates, which include double-digit growth for 2024-2025, and actual decline for -26E, then there is a market-beating upside even on a conservative 15x P/E of over 15% annually.

And this is well below its average, which has the company trading closer to 20x P/E. That sort of upside would have this company being a triple-digit RoR potential, which is of course nice, but I don't view that as all that likely - 20x P/E for this company is possible, but it's below where the company has been for some time, and I believe the ease of gaining further market share is mostly over. Capturing more market share will likely take CapEx, and will be slower going forward - but this is only in comparison because the company has been on a significant growth trajectory for some time.

Still, I do not view the growth story as over for the company. I am not necessarily selling or rotating my stake in flatexDEGIRO here. My previous target was €16/share. The company has not reached this target yet, and I am not changing my target. €16/share is in fact lower than a 15x 2026E target, and I believe the company could easily manage this over time.

S&P Global analysts go lower than my target. 11 analysts give the company a range from €9/share to €17/share, with an average PT of around €12 - but I believe the analysts might be underestimating this company here.

For the time being, I'm sticking to my target and not lowering it. I'm curious to see full-year results and will provide an update on those as well, but for the time being, I say that my investment and conviction in this company have paid off, and I expect that this will continue.

Here is my initial 2024 thesis for flatexDEGIRO.

Thesis

- flatexDEGIRO continues to be a very rare breed - it's a growth company that I consider investable based on solid earnings, a fundamentally sound and profitable business model, good prospective results for 2023-2025E, and good management with a vision of turning this into a leading broker in Europe.

- I'm "on board" with this vision and strategy. And that's where I give the company my rating of "BUY", going in with a PT of €16 and having bought a stake representing 0.5% of my investment portfolio on the private side, now up a significant 30% over a short period of time.

- I expect to own flatexDEGIRO for several years and eventually see triple-digit returns for this investment. This is how I invest in growth stocks - choosing profitable and well-managed companies with what I see as a clear future in a market that's not going anywhere.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The only scenario where I am "okay" with buying a growth company is when the company is qualitative, safe, cheap, and with a realistic upside. flatexDEGIRO has this, and for those reasons, it's a "BUY".

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

flatexDEGIRO: Up Over 30% Since My Last Coverage