FLBR - FLBR: Time To Look At Brazil Again Ahead Of A Likely Monetary Policy Pivot

2023-07-11 11:37:59 ET

Summary

- Brazil's key economic indicators are now moving in the right direction.

- A sooner-than-expected policy pivot may be on the horizon.

- The heavily discounted Franklin FTSE Brazil ETF is poised to benefit.

- Investors get a hefty yield in the meantime.

Having endured a difficult start to the year, Brazil's economy appears to finally be turning the corner. Inflation has decelerated well below trend, while downward revisions to earnings and GDP growth forecasts may finally be nearing an end. And though the past earnings season saw more downward earnings revisions, the improving consumer and business confidence indicators, likely a result of the declining inflation, warrant a relook at my previously cautious stance on Brazilian equities. Political concerns have also been somewhat allayed by recent developments at the Lower House, indicating checks and balances to President Lula's populist reversal of past business-friendly reforms.

Given the widening delta between rates and inflation (13.75% SELIC rate vs. ~5% expected inflation by year-end), a monetary policy reversal is likely a matter of when not if. Not all of the Franklin FTSE Brazil ETF's ( FLBR ) portfolio will benefit from rate cuts (note financials is the largest sector exposure at 24.5%) but at a rather undemanding ~8x fwd P/E valuation (well below pre-hike levels), FLBR presents compelling re-rating potential ahead of a likely pivot. Investors get paid a hefty low-teens percentage yield to wait in the meantime.

Fund Overview – Still the Most Competitively Priced Brazilian Investment Vehicle

The NYSE-listed Franklin FTSE Brazil ETF, which tracks Brazilian large and mid-cap equities via the market cap-weighted FTSE Brazil Capped Index (subject to single-stock concentration limits), held $121m of net assets at the time of writing, well below the prior $266m amid heavy investor outflows in recent months. The 0.19% expense ratio (gross and net) is maintained, though, making the fund the most cost-effective option available for US investors looking to access Brazilian equities – by comparison, the $5.2bn iShares MSCI Brazil ETF ( EWZ ) charges ~0.6%.

{kind=link}

Franklin FTSE Brazil ETF

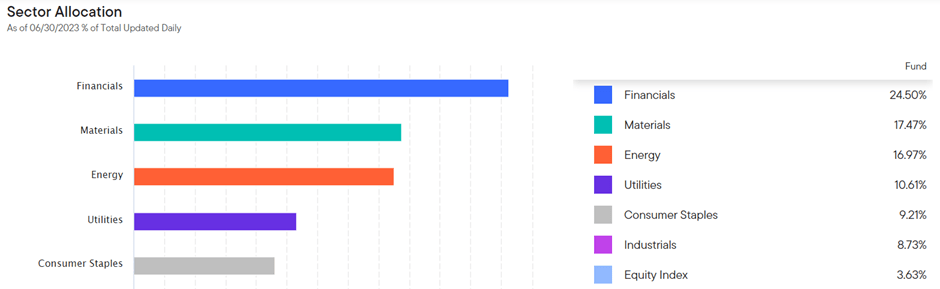

The fund's sector allocation is largely consistent with prior reporting, with Financials still the top exposure at 24.5% (unchanged). Materials (the largest sector allocation at the beginning of the year) has ceded further share and now contributes 17.5% (down from ~21% prior), while energy at 17.0% is unchanged. The other notable change in the top-five list is the addition of Consumer Staples (9.2%) over Industrials (8.7%). Broadly speaking, the FLBR composition is largely in line with comparable Brazil large-cap funds like EWZ, which tracks the MSCI Brazil 25/50 Index.

{kind=link}

Franklin FTSE Brazil ETF

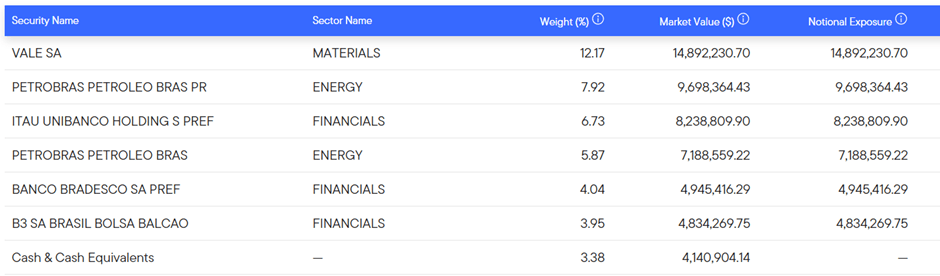

From a single-stock perspective, the FLBR portfolio is also unchanged, with metals and mining leader Vale S.A. ( VALE ) still the largest holding at 12.2% (albeit down from ~15% prior). The combined allocation to state-owned petroleum multinational Petrobras' ( PBR ) preferred and common stock also remains sizeable. The rest of the top five are financial holdings, led by Itau Unibanco ( ITUB ) at 6.7% (unchanged), Bradesco ( BBD ) at 4.0%, and B3 S.A. ( OTCPK:BOLSY ) at 4.0% (unchanged). Outside of the top five, the increased 3.4% cash holding is notable; outside of this, the fund is fully invested in domestic equities. Also positive is the reduced concentration risk, with the top-five holdings contributing a lower ~37% of the portfolio.

{kind=link}

Franklin FTSE Brazil ETF

Fund Performance – Disappointing Shareholder Return; Distribution Sustained

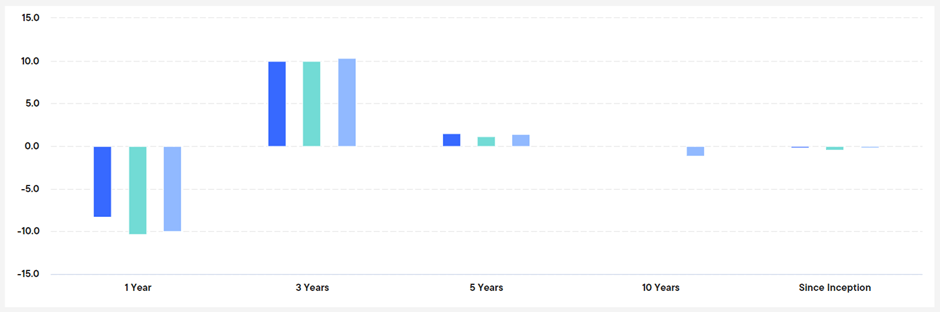

With FLBR up 18.7% in 2023, the fund has outperformed not only its historical trend but also most other emerging market ETFs this year. Zooming out, however, the fund has steadily declined in value since its inception in 2017, losing investors -0.2% on an annualized basis. Over a five-year timeline, FLBR's total return has been similarly underwhelming at +1.5% (+1.2% in NAV terms). And while the three-year return seems strong at +10.0%, this was largely due to the rebound in equity prices off a COVID-impacted base. By comparison, key comparable EWZ has returned +13.1% and +6.0% over its three and five-year timelines. The only consistent positive has been the tracking error relative to the underlying FTSE Brazil Capped Index – after expenses, the minimal delta has impressively sustained through the cycles.

{kind=link}

Franklin FTSE Brazil ETF

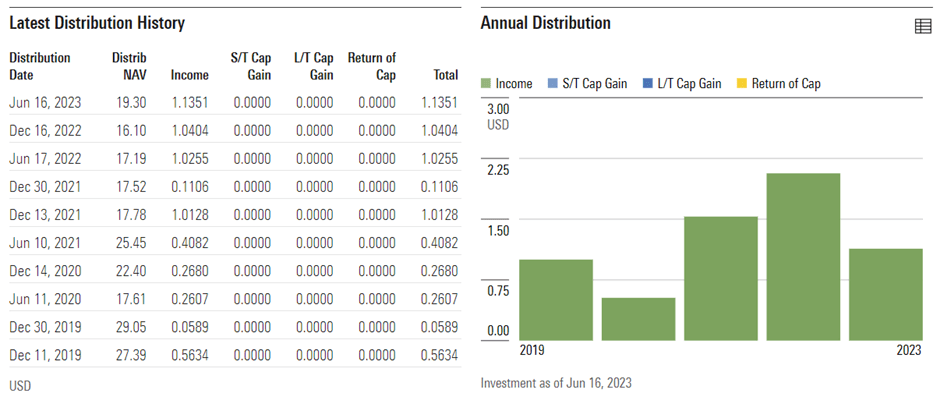

The fund has started off this year's distribution cycle well, returning $1.14/share in H1 2023 (above the $1.04/share in H1 2022). Assuming this trend continues into H2, there could even be upside to the $2.07/share distribution last year (implied ~11% yield). There will inevitably be some cyclicality in the yield (primarily income payouts on a semi-annual basis) due to the fund's exposure to commodity/energy price swings. But the resilience of FLBR's portfolio holdings thus far means we may well be on track for another year of double-digit percentage yields. Should the recent payouts prove sustainable beyond this year as well, FLBR could re-rate accordingly.

{kind=link}

Morningstar

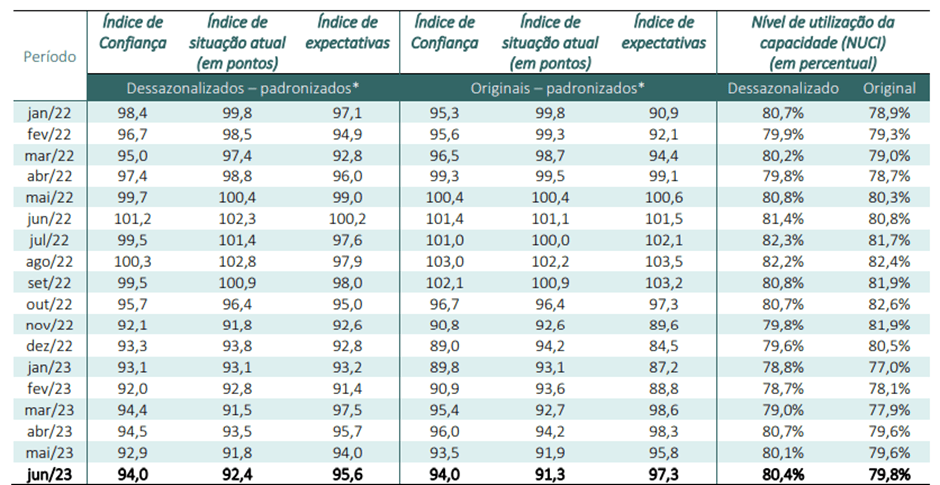

Copom Patient but a Policy Pivot is at Hand

Brazilian economic activity has been markedly improving of late. The FGV industry confidence index rose at a surprisingly rapid pace in June to 94 – while still below the 100pt optimism threshold, the rise of the expectations component to 95.6 (vs. 92.4 for the 'current situation index') indicates a brightening outlook. Consumer sentiment has been similarly improving , reaching ~92pts in June on the back of an upturn in the expectations component (up to 104.0). So while Brazil's large-cap earnings have suffered heavy downward revisions in recent months, there might still be light at the end of the tunnel.

{kind=link}

FGV

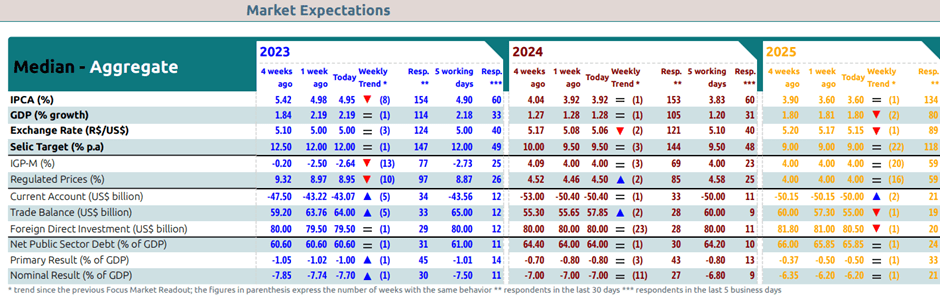

Also driving the optimism on Brazilian equities are decelerating inflation expectations – core inflation most recently printed at +6.2% YoY (vs. ~9% in 2022), driving consensus forecasts of +5.1% by year-end and a reversion to +4% by 2024. While still above the central bank's +3.25% consumer inflation target, the extent to which wholesale inflation has eased and the BRL has strengthened this year means the Copom (i.e., the Monetary Policy Committee of the central bank) finally has room to consider a policy pivot. The June policy meeting statement only amplified hopes for a pivot, with the central bank adding data dependency as a precondition to altering its neutral stance. Whether Copom ultimately cuts the overly restrictive 13.75% Selic rate at the August or September meetings, the tailwind from a lower cost of capital presents massive upside to currently depressed equity valuations in Brazil.

{kind=link}

BCB

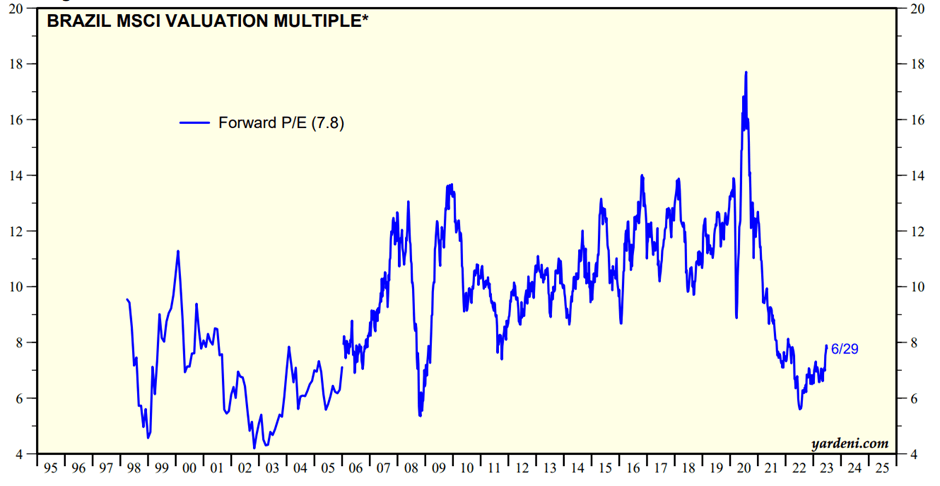

Time for a Relook at Brazil Ahead of a Likely Monetary Policy Pivot

FLBR has outperformed YTD, as inflation-driven optimism about potential rate cuts outweighed the wave of negative earnings revisions in recent months. Alongside markedly improved consumer and business confidence, declining inflation is the tide that appears to be lifting all boats. With all signs pointing to inflationary pressures easing further through year-end (~5% per consensus expectations), earnings and GDP growth may be poised for an inflection as well. While FLBR's rally this year has come mostly out of valuations, there's still plenty of room for further multiple expansion to pre-tightening levels. The key risk remains on the political side - President Lula's platform has favored populism over business-friendly policies, though checks and balances at the Lower House mitigate this risk somewhat. And at a historically discounted ~8x fwd P/E valuation (plus another year of low-teens distribution yield), investors get a compelling safety margin here.

{kind=link}

Yardeni

For further details see:

FLBR: Time To Look At Brazil Again Ahead Of A Likely Monetary Policy Pivot