FLC - FLC: Higher Rates Continue To Pressure Preferreds But Discount Offers Potential

2023-10-19 12:37:35 ET

Summary

- Flaherty & Crumrine Total Return Fund has continued to face significant pressure from rising rates.

- FLC's share price has also been significantly impacted due to the fund's discount widening dramatically.

- Despite facing rate pressures, FLC presents a potential opportunity for long-term investors, particularly if one believes we are at or near peak rates.

Written by Nick Ackerman, co-produced by Stanford Chemist.

To say that my prior coverage of Flaherty & Crumrine Total Return Fund ( FLC ) fund was incredibly poor timing would be an understatement.

FLC Performance Since Prior Update (Seeking Alpha)

The article was posted in early February, right before we had regional banks collapsing. This saw FLC see some of their holdings go to zero overnight. We discussed the regional bank crisis and interest rate pressures on preferreds shortly after that event.

That accounted for a sizeable portion of the drop. However, a meaningful portion of the drop in terms of the share price was from the widening of the discount as well. While NAV has recovered a bit on a total return basis, investors really haven't felt it since FLC's discount was around 5% and has now expanded to discount levels not seen since the global financial crisis in 2007/08.

This is where the potential opportunity is for the fund even as it continues to face rate pressures as risk-free Treasuries go to levels not seen since 2007. This would be a particularly attractive time to consider the fund if an investor assumes that we are at or near peak rates for this cycle.

The Basics

- 1-Year Z-score: -2.23.

- Discount: -16.56%.

- Distribution Yield: 7.83%.

- Expense Ratio: 1.30%.

- Leverage: 42%.

- Managed Assets: $282.25 million.

- Structure: Perpetual.

FLC's objective is quite simple , "provide its common shareholders with high current income." They also have a secondary investment objective of "capital appreciation," though preferreds and preferred funds typically fall short of this secondary goal.

To achieve the fund's objective, they will "normally invest at least 80% of its total assets in a diversified portfolio of preferred securities and other income-producing securities, consisting of various debt securities." They continue with, "normally invest at least 50% of its total assets in preferred securities."

Leverage And Rate Pressures

The main headwind for preferreds remains interest rates rising. As Treasury Rates surged recently, that put additional pressure on all fixed-income or income-oriented investments. The 10-year Treasury Rate is right near 5% with the latest surge.

As rates rise, other yields need to rise to be more competitive. FLC's effective duration comes to 3 years. That means that for every 1% change in interest rates, FLC's portfolio should move about 3%.

However, it isn't just the fact that higher rates make risk-free yields look more attractive, and therefore, prices of preferred need to go down. For FLC, they are also dealing with a sizeable amount of leverage that they run in their portfolio. This leverage comes with a cost, and that cost has increased substantially. Since they borrow short, they see those yields climb immediately as it is based on SOFR plus 0.90%.

With SOFR at 5.32% today , that would put borrowing costs at about 6.22%. That has caused the fund's total expense ratio to go from 1.64% last year to 3.05% as of the last semi-annual report. That report is from May 31, 2023, so it has since increased even further.

Given the average coupon on their underlying portfolio comes to 6.87%, we can start to see why there has been so much pressure. Not only are they borrowing at around 6.22%, but then the operating expenses go on top of that, and we are given a negative spread between what most of their portfolio can earn and what their expenses are.

Now, there are lower-quality holdings in terms of credit quality that they are likely carrying that do out-earn those expenses. After all, the 6.87% is only the average coupon of the underlying portfolio.

Still, this has been the significant headwind their portfolio has faced, and it is what has caused their distribution rate to be cut every quarter for the last year and a half now. With potentially one more rate increase to go, it probably hasn't stabilized yet, either.

FLC Distribution History (CEFConnect)

{kind=link}

One could suggest that deleveraging their portfolio would make sense. If they aren't earning a very widespread, then that argument can make sense. There is no reason to carry leverage unless the portfolio can out-yield the expenses.

That said, that isn't necessarily taking into account the fact that no one knows when a recovery will take place either. If rates are cut, that could lead to a sizeable rebound in a lot of these underlying holdings. If they deleverage now, it would essentially be increasing the chance to lock in permanent damage to the fund.

Additionally, if rates stay higher for longer, the preferred that they can invest in should start to see their yields tick higher. A large 85% portion of their portfolio is fixed-to-float securities that start floating anywhere between now and 2030. A good portion of these could be redeemed as they start floating, as we've seen . However, if yields remain elevated and the banks need to issue new preferred, they'll be done at higher rates.

Banks often use preferred as one of their tools to stay within regulatory compliance because they can issue non-cumulative perpetual preferred that counts toward Tier 1 Capital. That's why 56.2% of the portfolio is in the bank sector. Insurance companies are another large exposure for the fund at 22.2%. So clearly, the fund has a significant financial sector weighting.

What makes FLC attractive to consider for a longer-term investor is to see a recovery in the preferred space or higher income longer term when rates stabilize or are cut. What makes it even more particularly attractive at this time is the fund's significant discount to NAV per share. That could also serve to potentially boost returns when a recovery takes place. The fund is currently trading at the widest discount since the GFC.

Since that initial drop due to the banking crisis, from the end of March to today, preferred had started to recover. FLC reflects this with a positive total NAV return. However, a lot of the recovery had been given up due to the latest Treasury rate surge. Still, even while FLC remained mostly flat at this point on a total NAV return basis, it is the fund's total share price basis that wouldn't reflect this, as the discount widened substantially during this time.

YCharts

FLC's Portfolio

The main risk, of course, would be that rates continue to march higher and continue to pressure FLC going forward. Further bank collapses would also be expected to lead to further losses.

Yes, when SVB collapsed, it was rated investment-grade. However, generally speaking, companies with investment grades don't collapse regularly or as regularly as their non-investment grade counterparts. So, a fairly substantial portion of FLC's portfolio being dedicated to investment-grade exposure could be some comfort.

FLC Portfolio Credit Quality (Flaherty & Crumrine)

{kind=link}

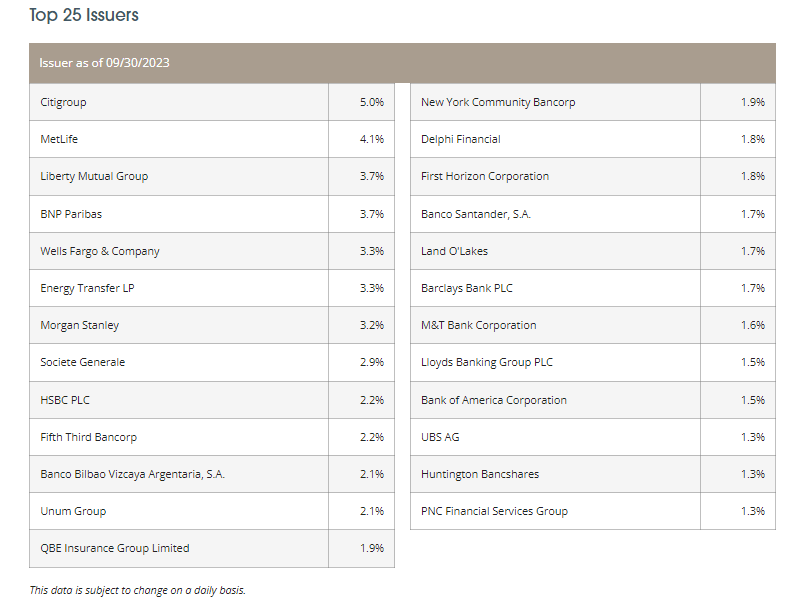

The fund is also significantly diversified, as they list 207 holdings. In their top positions, they hold some fairly significant weightings, but these are generally larger financial institutions. That includes a number of G-SIbs , which are those that aren't allowed to fail, or the government will step in to backstop it.

That doesn't necessarily mean that equity or preferred holdings aren't wiped out, but they are also the more highly regulated entities. With regulations meant to create a situation where the government doesn't need to step in the first place.

FLC Top Holdings (Flaherty & Crumrine)

{kind=link}

Conclusion

Preferreds have been beaten, and FLC has been beaten even further with a significantly expanding discount. That can create a tempting situation for the long-term investor. Stabilizing interest rates would help out the fund, and interest rate cuts could be even better for the fund, assuming it doesn't come from a significantly weakening economy. Higher rates continue to be the key risk here, which could cause further depreciation and pressures on their leverage costs.

For further details see:

FLC: Higher Rates Continue To Pressure Preferreds But Discount Offers Potential