FLNG - FLEX LNG: 9% Yield More Growth In 2023 Long Term-Tailwinds

Summary

- FLNG yields 8.6%, plus additional percent from its special dividends.

- 2022 net income and EPS rose more than 15%.

- FLNG has one of the youngest LNG fleets, ~3 years old, with a contract backlog of ~60 years - the majority of its fleet is booked into 2026.

- Its next debt maturity isn't until 2028.

LNG was a hot commodity in 2022, with Europe switching its supplies from Russia to other providers. This ramped up demand for LNG vessels, and greatly benefited vessel owners, which enjoyed high spot rates.

Moreover, it enabled some of them, like FLEX LNG Ltd.( FLNG ), to lock in high long-term charter rates.

Company Profile:

FLEX LNG Ltd., through its subsidiaries, engages in the seaborne transportation of liquefied natural gas worldwide. As of February 16, 2022, it owned and operated nine M-type electronically controlled gas injection LNG carriers; and four vessels with generation X dual fuel propulsion systems. It also provides chartering and management services. FLEX LNG Ltd. was incorporated in 2006 and is based in Hamilton, Bermuda. (FLNG site)

FLNG has one of the youngest fleets in the LNG shipping sub-industry - ranging in newbuild dates from 2018 to 2021, with an average age of ~3 years. The contract backlog for FLNG's time charters is over 49 years.

Tailwinds:

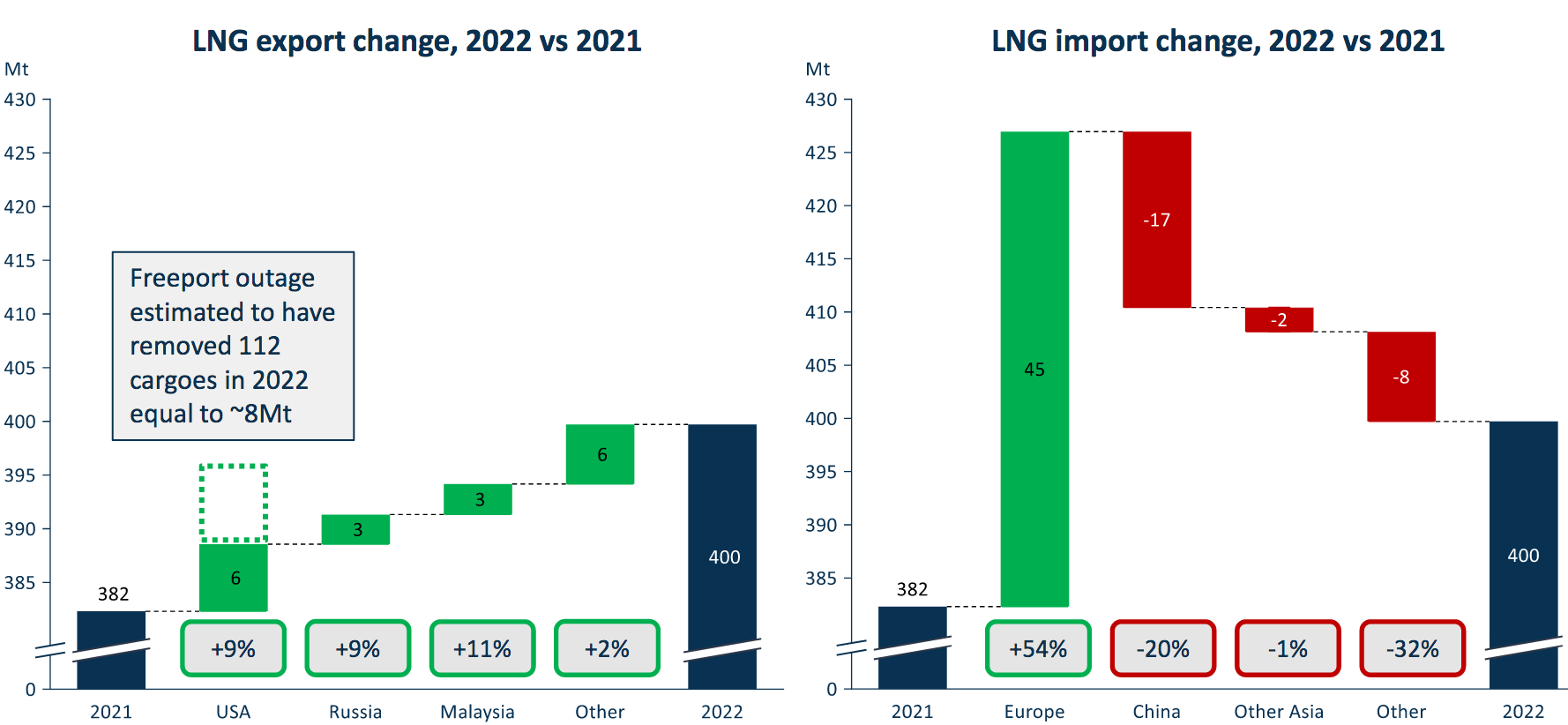

US LNG exports rose 9%, to 6 metric tons in 2022, even with the Freeport, Texas, LNG terminal fire removing ~8 metric tons. Europe's LNG imports rose 54% - the top six countries for growth in LNG imports were all European. Pipeline flows from Russia were down by ~90% vs. 2021, so Europe tapped the LNG spot market to replace Russian pipeline flows.

{kind=link}

FLNG site

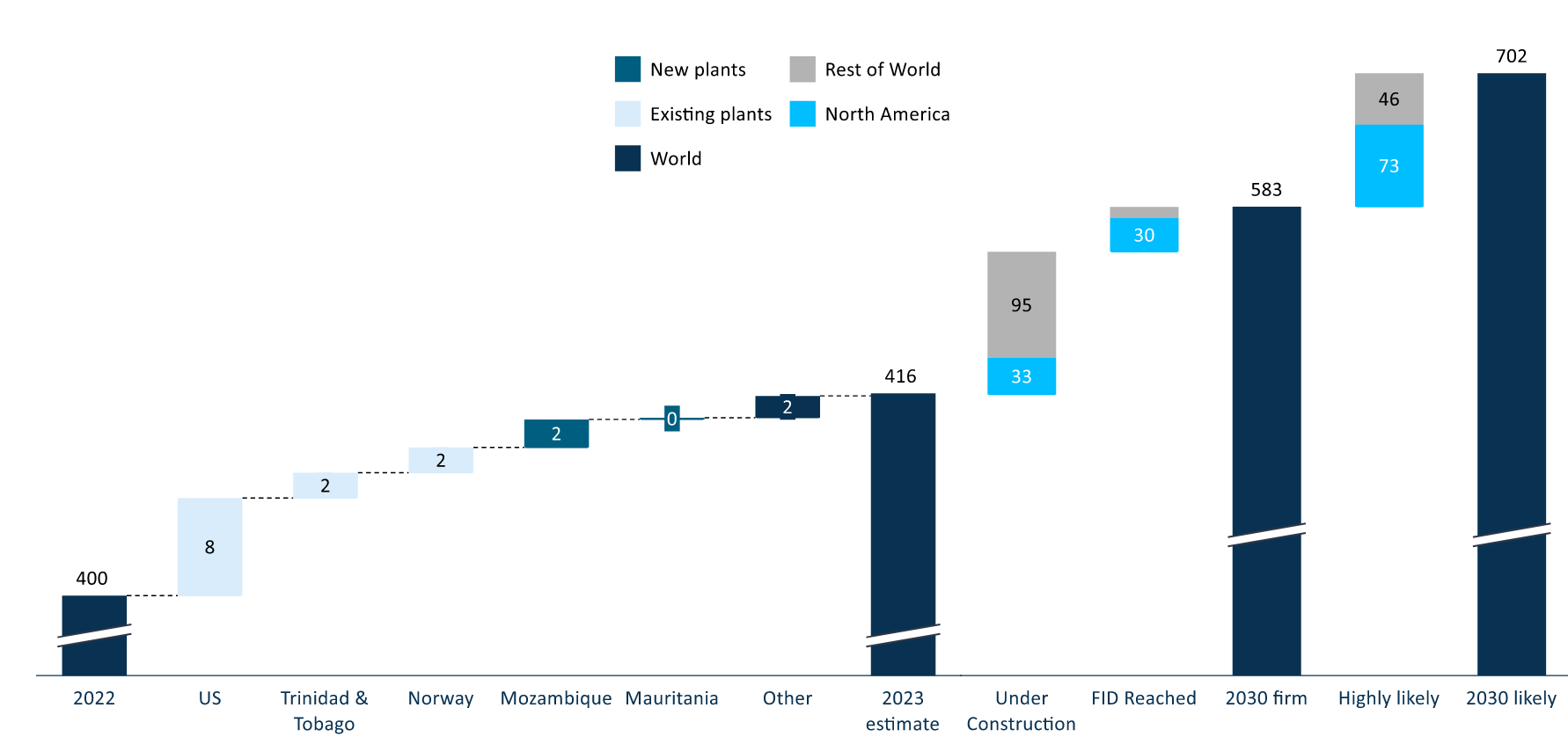

Looking forward, it's estimated that production will expand to 700M tons by 2030m 73 million tons more in the U.S., and 46 in the rest of the world, which will create more demand for LNG shipping.

{kind=link}

FLNG site

Fleet:

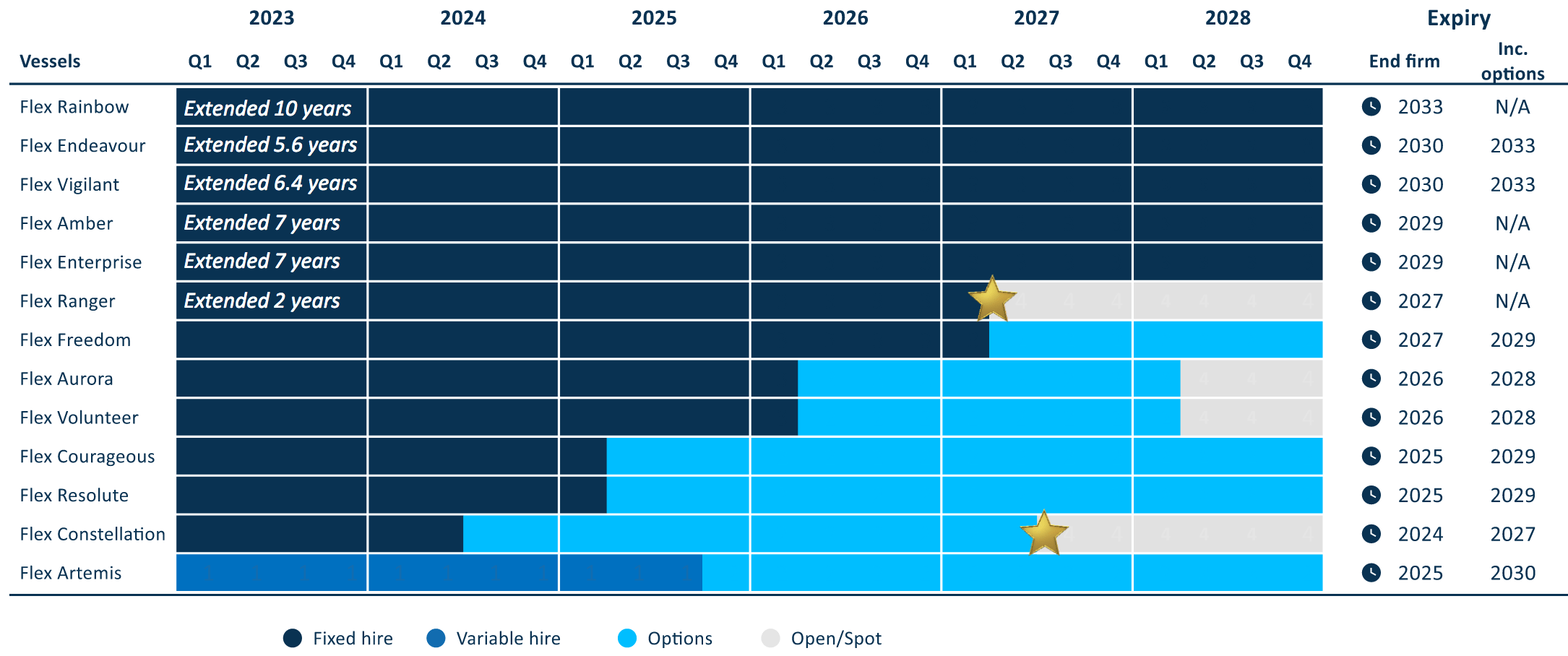

Management extended three ships' charters in November, with Cheniere: The Flex Endeavour, which was extended until end of 2030, adding 5.6 years. Flex Vigilant added 6.4 years, also bringing that to 2030. Those two ships have options to 2033. The Flex Ranger was extended for another two option years, bringing that ship until early 2027.

These longer-term charters will serve to support FLNG's dividends in the coming years.

{kind=link}

FLNG site

Earnings:

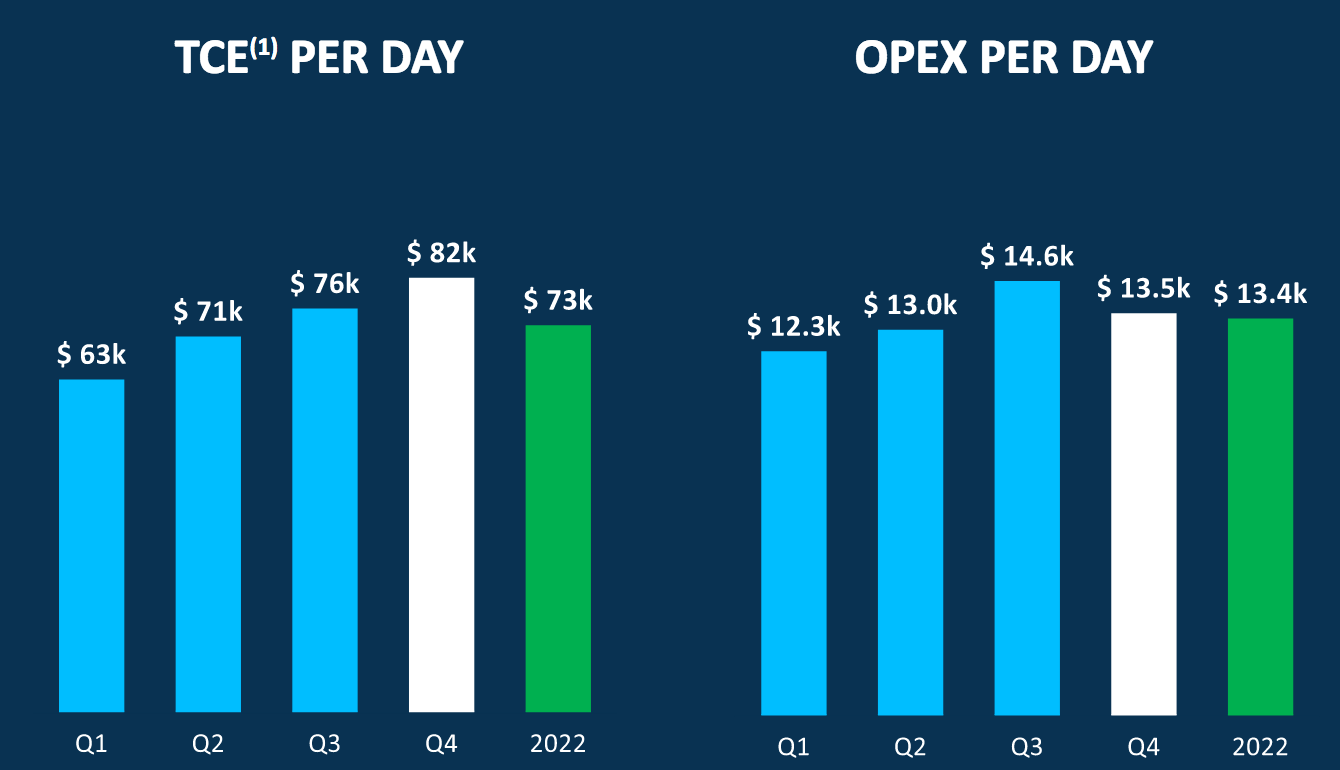

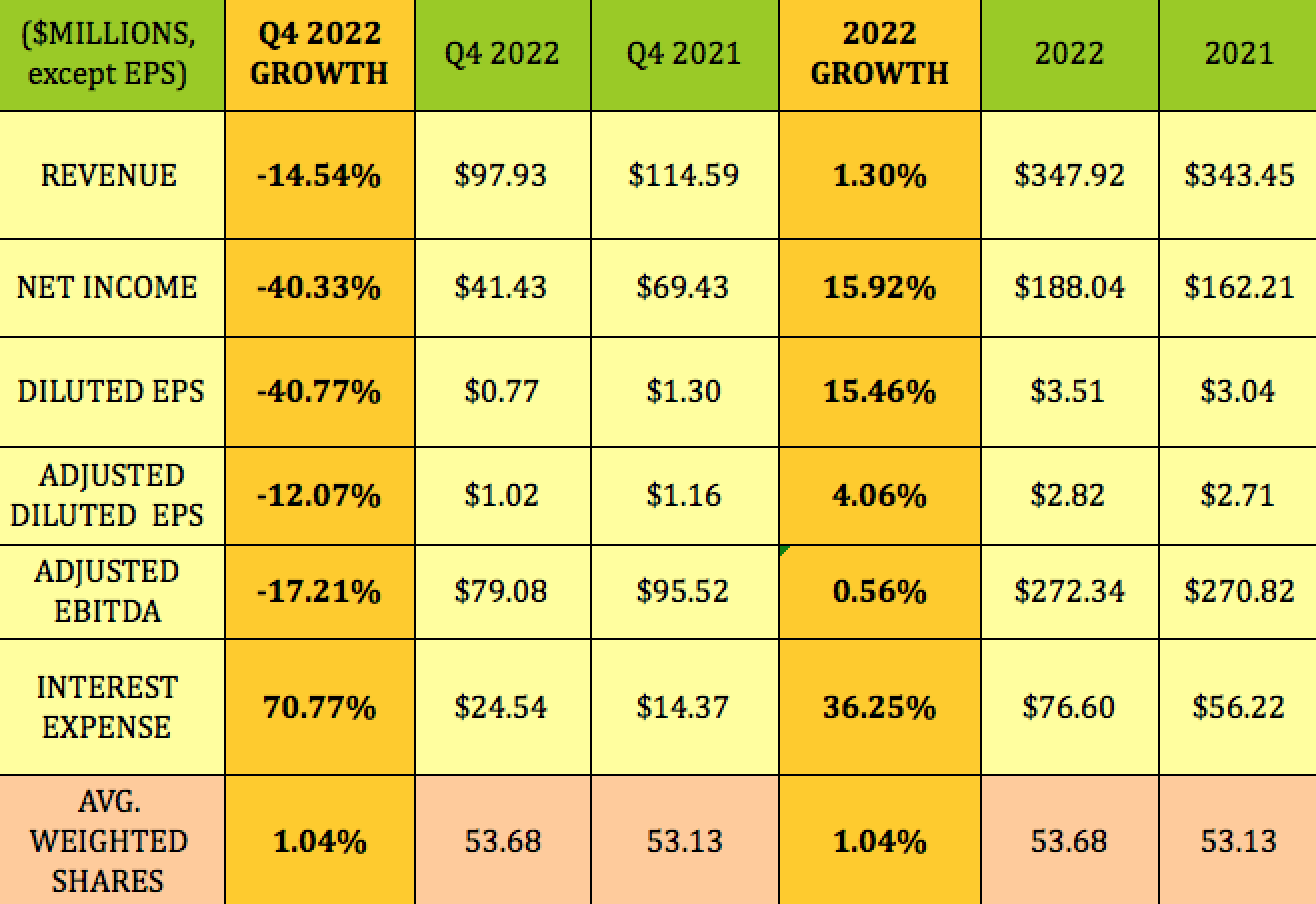

Time Charter Equivalent, TCE, rates were $82K in Q4 '22, up from $76K in Q3 '22, and averaged $73K in 2022. However, TCE rates averaged ~$96K in Q4 '21, 17% higher, hence the lower earnings in Q4 '22 vs. Q4 '21.

Operating expenses averaged $13.5K in Q4 '22, similar to the full-year 2022 average:

{kind=link}

FLNG site

In addition to the ~$14.5M drop in revenue, there was also a ~$10M rise in Interest expense, and ~$2.5M less in derivative gains in Q4 '22, all of which comprised the ~$27M drop in net income for the quarter.

For full-year 2022, although revenue was flattish, net income rose nearly 16%, and EPS was up 15.46%, even with the 36% rise in interest expense:

{kind=link}

Hidden Dividend Stocks Plus

2023 Guidance:

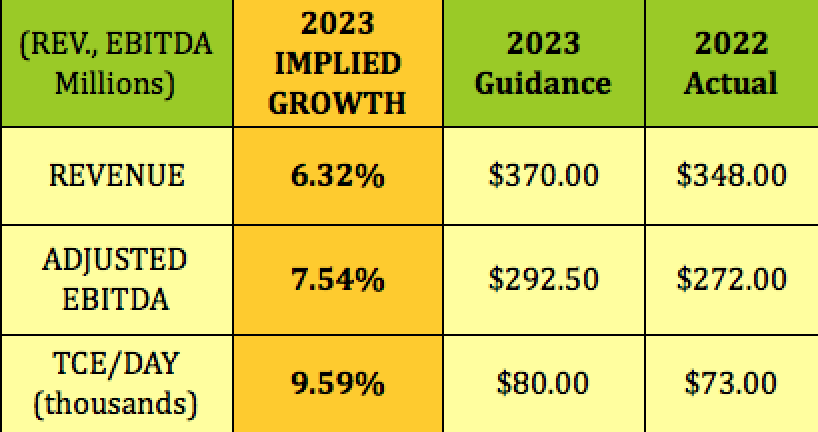

However, with the new charters locked in, management sees ~6.3% growth in revenue for 2023, and 7.5% growth for midpoint Adjusted EBITDA, with TCE/Day expected to be at $80K, up ~9.6%. This growth is inclusive of the dry-docking of four ships in 2023, with dry-docking expenses of ~$18 to $20M in total.

{kind=link}

Hidden Dividend Stocks Plus

Dividends:

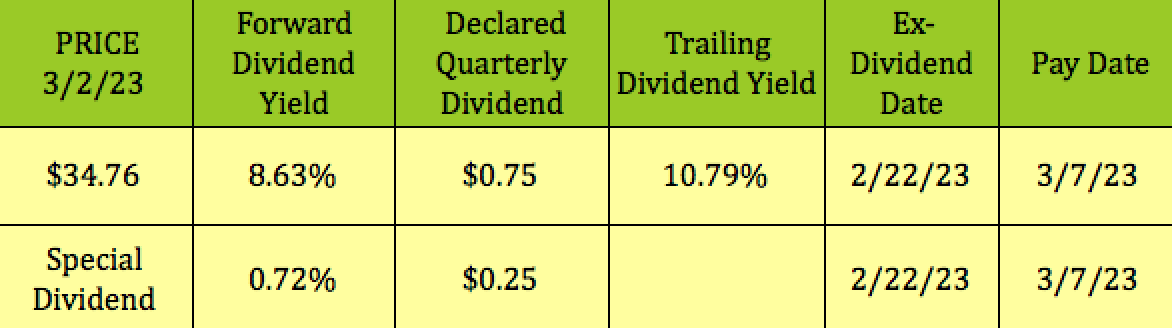

Management declared another $.75 quarterly dividend, plus a $.25 special dividend which went ex-dividend on 2/22/23. If they maintain the $.75 quarterly dividend, the forward yield would be ~8.6%, at the 3/2/23 $34.76 price level. Its next dividend should be declared in early May.

{kind=link}

Hidden Dividend Stocks Plus

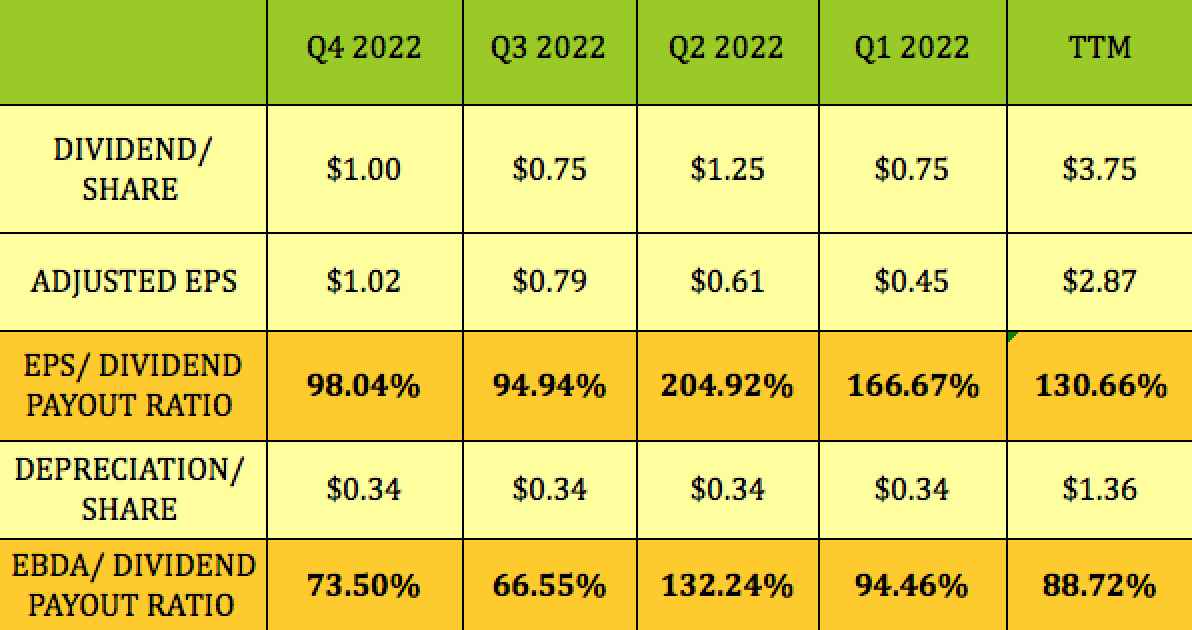

FLNG's Adjusted EPS Dividend Payout ratio was 98% for the latest $1.00 in dividends attributed to Q4 '22, down significantly from over 200% in Q2 '22 and 167% in Q1 '22.

However, EPS includes a great deal of non-cash depreciation & amortization. After adding the D&A amounts back to EPS, the trailing EBDA dividend payout ratio is a more reasonable, at 73.50% in Q4 '22, and averaging 88.72% in 2022:

{kind=link}

Hidden Dividend Stocks Plus

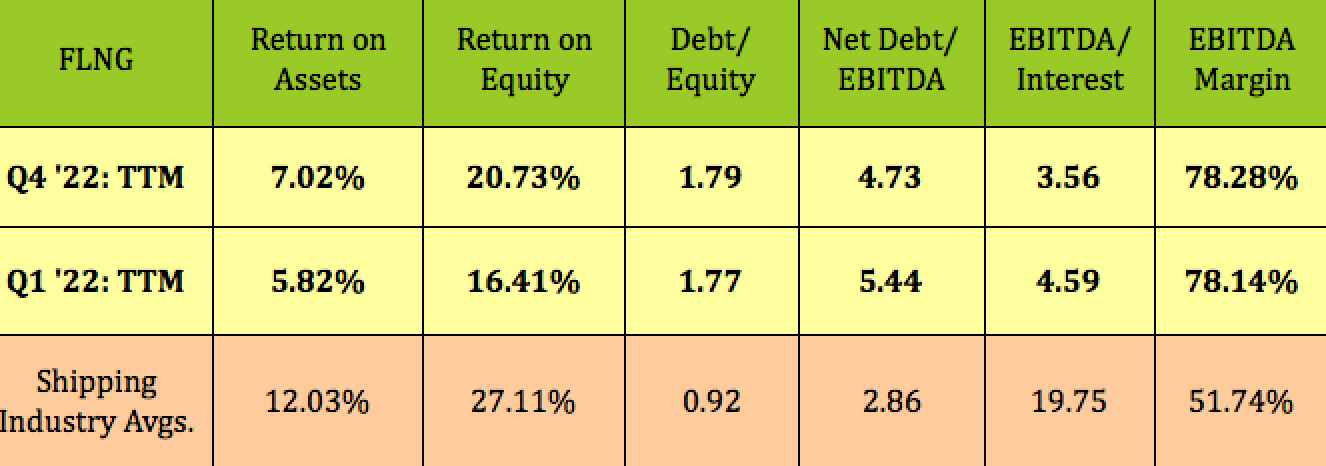

Profitability & Leverage:

FLNG's ROA and ROE both improved in 2022, as did its net Debt/EBITDA, which fell to 4.73X, as of 12/31/22, vs. 5.44X, as of 3/31/22.

{kind=link}

Hidden Dividend Stocks Plus

Debt and Liquidity:

Management completed several sale and leasebacks, which improved its cash position in 2022, releasing $387M in cash. It now has a mix of leasebacks and bank financings for its vessels.

{kind=link}

FLNG site

FLNG has no debt maturities before 2028, when its $123M financing for the Aurora vessel comes due. There will be three bank vessel financings maturing in 2029. These are at SOFR + rates, but management has an interest rate hedging program in place

{kind=link}

FLNG site

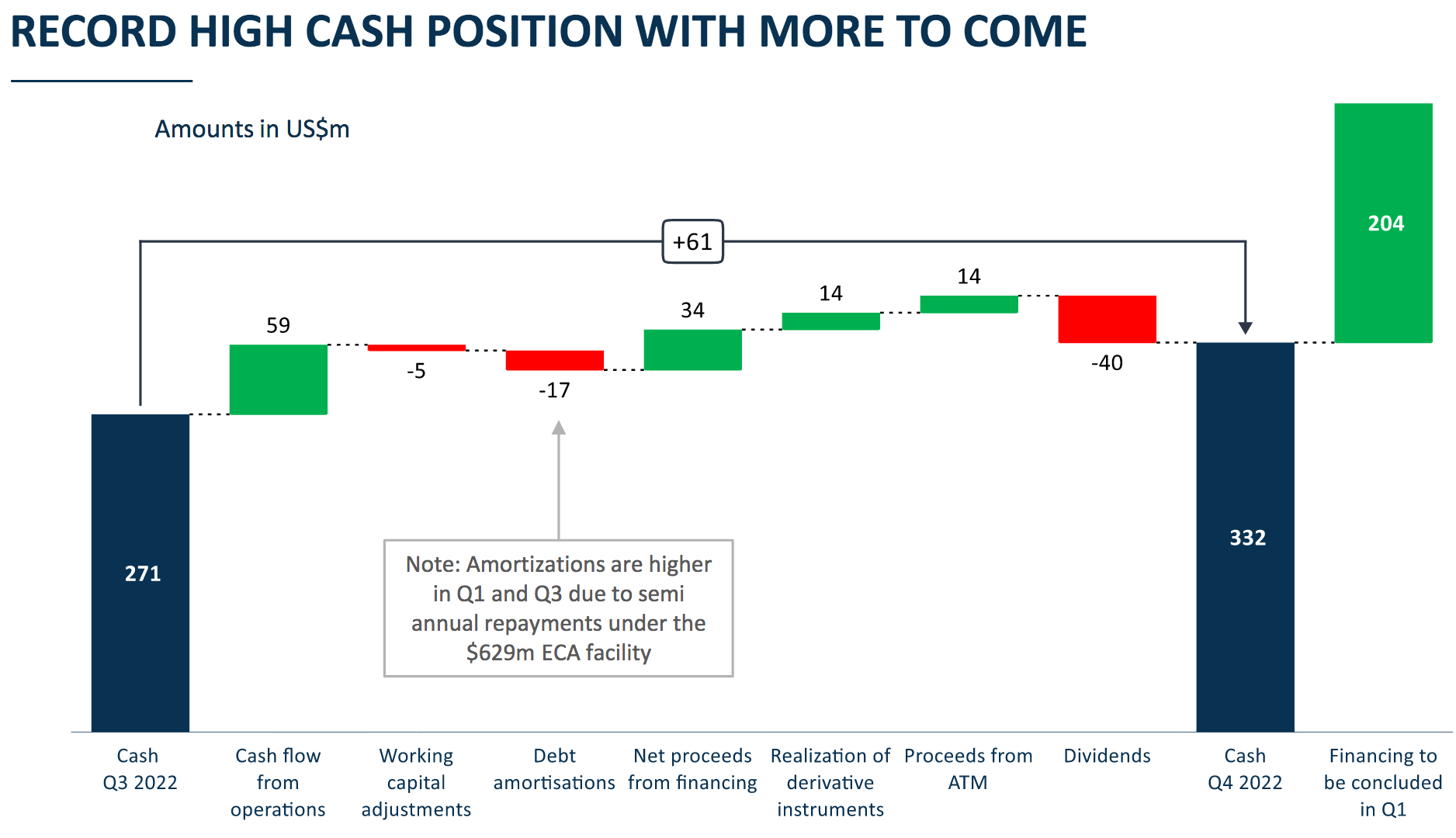

FLNG had a cash position of $332M, as of 12/31/22, which will improve by an additional $204M when its financing program concludes in Q1 '23:

{kind=link}

FLNG site

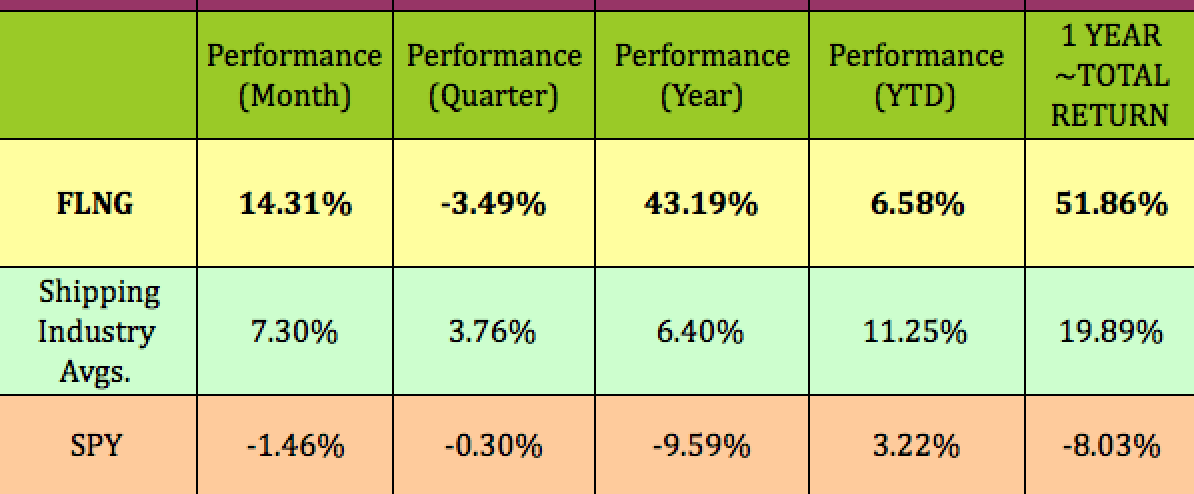

Performance:

FLNG has outperformed the S&P 500 over the past month, year, and year to date on a price basis, and has also outperformed it over the past year by a very wide margin on a total return basis. FLNG lags the shipping industry so far in 2022, but has outperformed it over the past month, and year, in addition to outperforming it on a total return basis over the past year:

{kind=link}

Hidden Dividend Stocks Plus

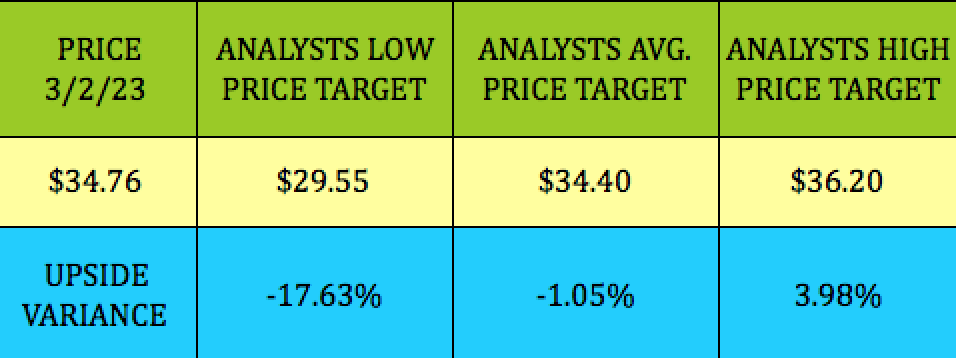

Analysts' Targets:

At its 3/2/23 intraday price of $34.76, FLNG was 1% above analysts' average price target of $34.40, and 4% below the $36.20 highest price target.

{kind=link}

Hidden Dividend Stocks Plus

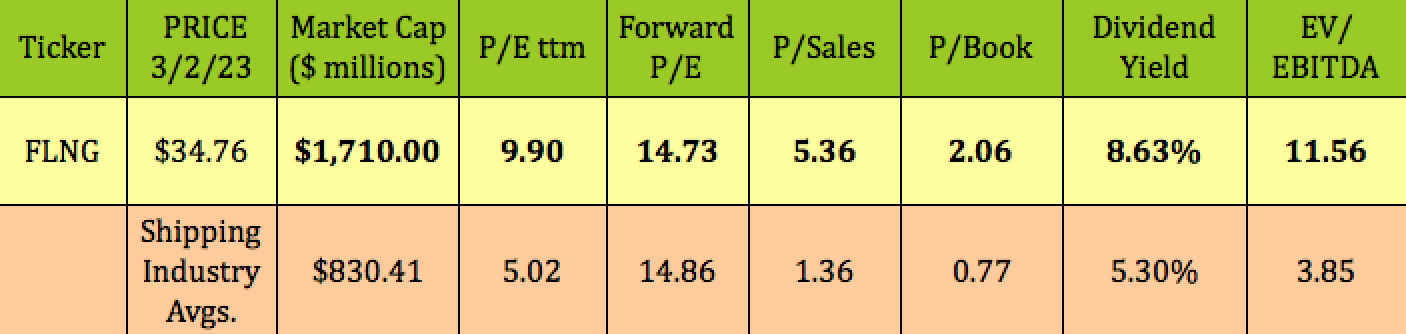

Valuations:

FLNG's 40%-plus rise outdistanced its EPS over the past four quarters, leading to a higher than average P/E valuation, whereas its 2023 forward P/E valuation is slightly lower than average for its industry. It's also getting premium valuations for P/Book, P/Sales, and EV/EBITDA. Its Dividend Yield is much higher than shipping industry averages.

{kind=link}

Hidden Dividend Stocks Plus

Parting Thoughts:

FLNG paid out $186M in dividends in 2022, with EBDA of ~$196M, for a ~1.05X coverage factor. If it achieves the midpoint EBITDA of $292.50, less ~$72M in depreciation, that would equal EBDA of ~$220M, which implies 1.18X dividend coverage in 2023. It looks like FLNG's dividends should have plenty of support in 2023.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.

For further details see:

FLEX LNG: 9% Yield, More Growth In 2023, Long Term-Tailwinds