FLNG - FLEX LNG: Consistency Is Key

2023-12-12 10:59:23 ET

Summary

- FLNG's Q3 results once again showed the consistent nature of this LNG shipper.

- Given its contract structure, FLNG is set to provide steady results over the next several years.

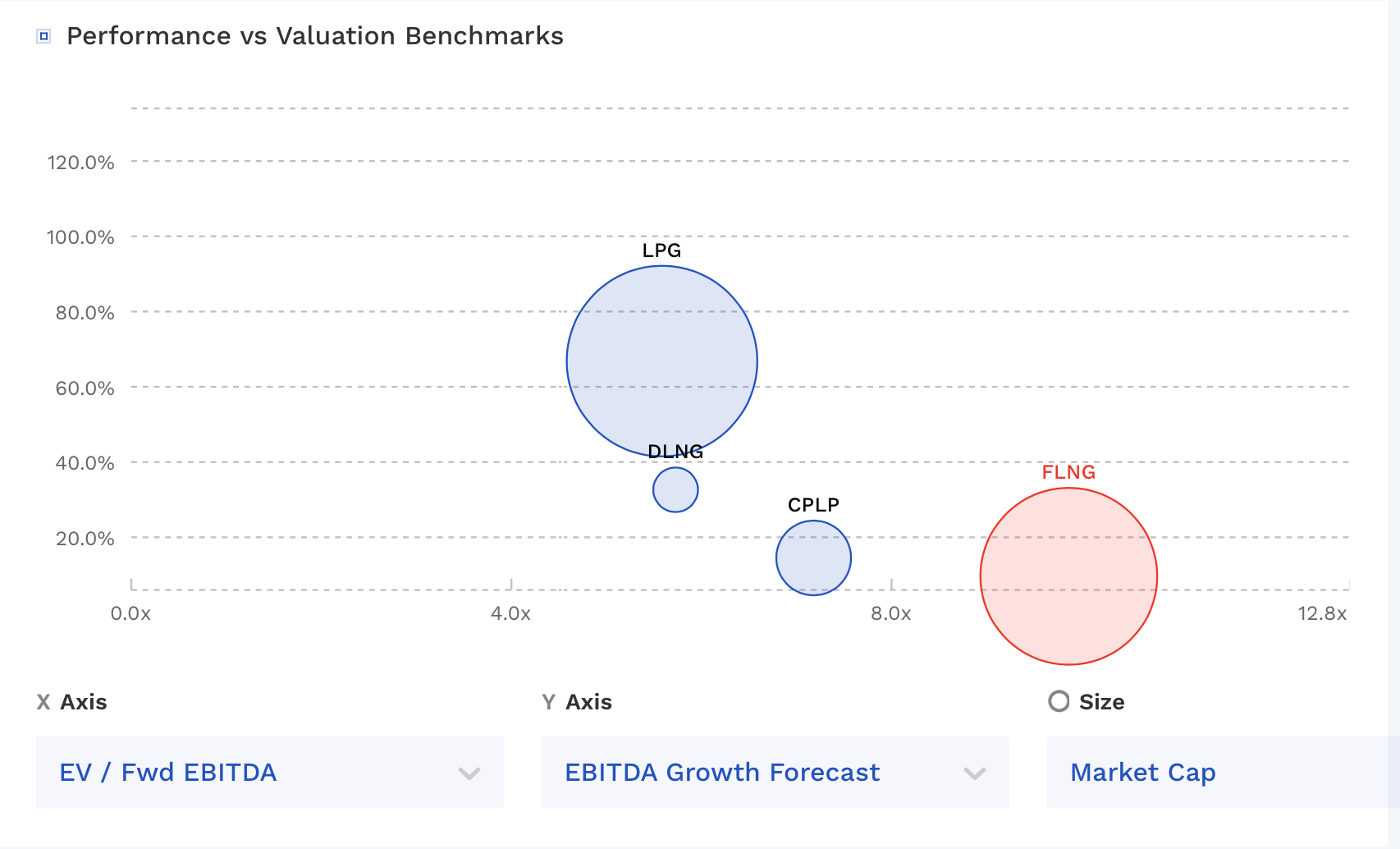

- FLNG trades at a discount to what it would cost to replicate its young fleet, leaving some potential upside to the stock to go along with an over 10% yield.

I upgraded FLEX LNG Ltd. (FLNG) back in September, noting that vessel values had increased and that it had solid visibility into earnings and cash flow given its contracts. With the company reporting its Q3 results last month, let's catch up on the name.

Company Profile

As a reminder, FLNG owns and operates a fleet of 13 LNG carriers, all of which were built between 2018-2021. These newer vessels all are equipped with XDF or MEGI propulsion engines.

As of early November, it had only four vessels with time charters expiring before 2026, with the earliest in Q2 2024, if its customer doesn't exercise its option to extend the charter.

Solid Q3 Results

For its most-recent quarter, FLNG recorded vessel operating revenue of $94.6 million, up 9% from $86.7 million a year ago and up 9% sequentially, as the company had three ships off-hire in Q3 for their scheduled 5-year special survey in drydock.

The company realized time charter equivalent (TCE) rates were $79,207 a day in the quarter, up 4% from $75,941 last year. TCE rates rose nearly 3% sequentially from $77,218 in Q3. As a reminder, the company has one vessel who rates are tied to the spot market. Strong spot rates for that vessel helped push up its overall TCE.

Opex per day fell to $14,161 from $14,625 a year ago and $14,618 in Q2.

Net income came in at $45.1 million, or 84 cents per share, versus $46.6 million, or 87 cents a share, a year ago. It was up sequentially from $39.0 million, or 72 cents per share, in Q3. The year-over-year results were hurt by $6 million in additional interest expense as a result of higher interest rates. Adjusted net income was $36.1 million, or 52 cents, versus $42.2 million, or 79 cents a share, a year ago, and $28.2 million, or 52 cents per share, in Q2.

Adjusted EBITDA came in at $74.7 million, an increase of 5% from $70.9 million a year ago, and up 13% from $66.2 million in Q2.

The company declared a dividend of 87.5 cents for the quarter, which included a regular dividend of 75 cents and a special dividend of 12.5 cents.

Turning to its balance sheet, FLNG ended the quarter with debt of $1.84 billion. It had cash and equivalents of $429.5 million. The company has no debt maturities before 2028.

Most of its rates are floating, but the company did enter swap transactions to create a fixed rate on $720 million of its debt. These hedges produced at gain of $15.6 million in the quarter.

Looking ahead, the company expects to generate revenue of $97-99 million in Q4 at the high end of its prior outlook of between $90-100. It continues to forecast revenue of $370 million for the full year and adjusted EBITDA of between $290-295 million.

The company noted that spot rates peaked at $240,000 a day in late September, before stabilize at around $200,000 a day. It said the outlook for 2024 is currently $100,000 a day given an influx of newbuilds versus minimal LNG export volume growth. It also noted that 5-year rates are currently at $115,000 a day.

The company will have 7.7% of its available days exposed to the spot market in 2023 and 12.7% in 2024, as its one vessel will have an open period between whether the charterer exercises its option to extend the contract.

Discussing the outlook for the LNG shipping market, CEO Oystein Kalleklev said:

"The overall freight and product market today ahead of the peak winter season is fairly balanced. The LNG product market is well supplied as supply curtailments have recently been limited despite the noise. That said, spot LNG prices remain at about $15/mmbtu which still reflects a tight market with LNG being priced at premium to crude oil which is somewhat unusual in historical context. As LNG export growth will continue to be fairly muted the next two years, we do expect the LNG product market to stay tight as European buyers will continue to be buyers both of first and last resort. Active buying by Europeans also means Atlantic cargoes will continue to be pulled towards Europe instead of Asia which will put a dent on sailing distances in the near term. The spot freight market will therefore continue to experience a very high level of volatility depending on season. From the end of 2025 we do however see a wave of new LNG coming onstream, and we expect these volumes to gradually alleviate market tightness and make LNG affordable to consumers with shallower pockets. Consequently, with newbuilding deliveries peaking at end of 2025, we do see incrementally tighter shipping market from 2026 onwards. We therefore think our two fully open ships in 2027 and two fully open ships in 2028 are attractively positioned for re-contracting opportunities. This is particularly the case given the elevated newbuilding prices which have pushed up term rates to very attractive levels for owners of modern fuel-efficient tonnage."

Q3 once again showed the steady results one should expect from FLNG given its long-term contracts, while seeing some benefits from increased spot rates given its Artemis vessels rates are tied to the spot market. Now the company did leave a lot of money on the table from these contracts, given the huge surge seen in spot rates, but the LNG shipping market will start to loosen up next year and into 2025 as newbuilds come into the market, so it can work both ways. FLNG also positively kept Opex per day down in the quarter, which was nice to see as it had been creeping up.

Looking ahead, the company should benefit from less drydocking days next year, and possibly lower interest rates, which would lower the interest expense on its floating debt. However, it will likely see less of a benefit from the spot market with Artemis.

Valuation

FLNG trades at 9.9x the 2023 EBITDA of $292 million and 9.8x the 2024 EBITDA consensus of $294.8 million.

On a P/E basis, it trades at 11.4x EPS estimates of $2.51. Based on the 2024 consensus for EPS of $2.52, it trades at 11.3x.

FLNG trades at a premium to other LNG and LPG shipping operators such as Dorian (LPG) and Dynagas (DLNG), although it has a younger, more modern fleet.

{kind=link}

It would cost about $3.4 billion to replicate FLNG's fleet based on the prices FLNG has said where the newbuild market has settled at. However, Capital Products just purchased 11 vessels last month for $3.13 billion, valuing them even higher at around $285 million per vessel, which would bring the value of 13 ships to $3.7 billion. You can put a -15% discount to that and get $3.15 billion. I believe that would put the stock price at between $34- $44. As such, I think my prior $38 target still looks reasonable.

Conclusion

Given its contract structure, FLNG is a solid option for income-oriented investors. It has a 10.5% yield based on its well-covered base dividend, but it will also occasionally pay out a special dividend like it did for Q3 as well.

Next year should be pretty similar to this 2023 from an operational standpoint, with spot rates having a moderate impact on its results. As such, I expect a similar base dividend to be paid, and if spot rates are strong or interest rates go down investors could perhaps see a special dividend or two as well.

All in all, I view the stock as a "Buy" for income-oriented investors. The biggest risk to the name would be if spot market rates crash and the value of vessels decrease. While the market should loosen up in the medium term, there are still a lot of LNG projects set for outer years that will increase the need from more LNG vessels and transport. A look at Cheniere ( LNG ) and its projects is just one example of the projects coming online to fill growing LNG demand.

For further details see:

FLEX LNG: Consistency Is Key