FLNG - FLEX LNG Positioned To Benefit From Positive LNG Outlook

Summary

- FLNG operates a fleet of 13 modern LNG carriers. These vessels have a backlog of several years due to demand, with sky-high charter rates.

- FLNG operates with an EBITDA margin of 76%, with this expected to continue. Dividend yield is currently 9% but with scope to increase.

- We are very bullish on LNG, seeing it as the near-term preferred substitute to oil. With the Russian Invasion of Ukraine, the medium-term looks even more lucrative.

- FLNG is trading at a high valuation, but we believe the current profile of the business supports this.

Company description:

FLEX LNG ( FLNG ) is an LNG shipping company incorporated in Bermuda and listed on the NYSE.

FLNG has a fleet of thirteen fuel efficient , 5th-generation LNG carriers. This consists of nine M-type, Electronically Controlled, Gas Injection (“MEGI”) LNG carriers and four Generation X Dual Fuel (“X-DF”) LNG carriers built between 2018 and 2021. These vessels operate at a lower cost than most and are more fuel efficient.

Prior to FLNG, we have covered other Shipping companies, including GSL , EGLE, GRIN and DAC.

Although many are aware, it may be worth illustrating how FLNG operates. The business is responsible for the transportation of LNG from a production location to an importer. For this service FLNG receive a daily charter rate, which is predetermined based on a contractual agreement. These can be long or short-term charters. For this reason, revenue can be agreed for years in advance, with a backlog build up.

FLNG has had an eventful few years, initially falling over 50% as a result of COVID-19. Demand for LNG fell substantially as the world was plunged into lockdowns. The subsequent reversal reflects the large uptick in demand that we observed following the end of lockdowns.

With such an unprecedented expansion, we are looking to assess whether FLNG remains an attractive investment. This will involve an assessment of the current profitability profile and the solvency of the business, with a view of how macro conditions will impact the business.

Bullish on LNG:

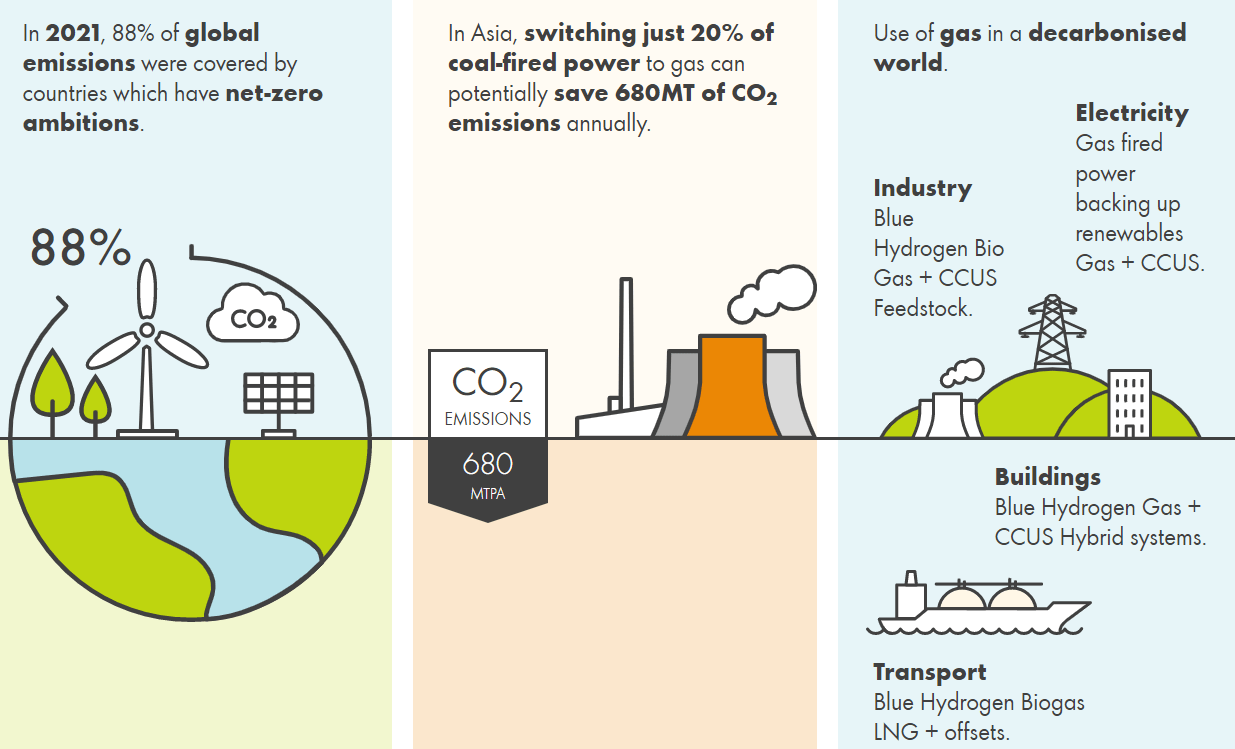

The LNG market has grown substantially in the last decade, one of the primary reasons for this is that it is the cleanest of the fossil fuels . It is 30% cleaner than oil and 40% cleaner than coal. With pressures to meet net zero and reduce carbon emissions, countries are willing to pay a premium to use LNG over substitutes.

{kind=link}

LNG infographic (1/3) (Shell)

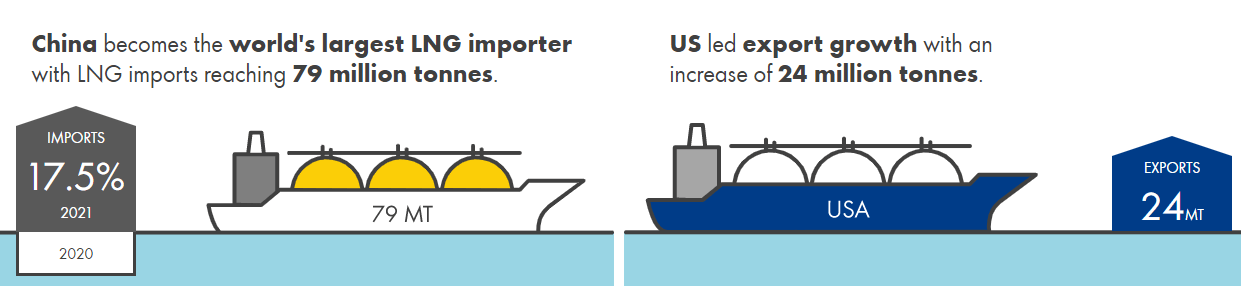

For this reason, LNG is expected to growth continuously into 2036 according to McKinsey, the only fossil fuel to do so (Source: McKinsey: "Global gas & energy outlook to 2035"). China is now the largest importer of the LNG and is expected to lead Asian demand for the commodity (Japan and S. Korea are the 2nd and 3rd largest importers), with the US expected to be the largest exporter. This is positive news for continued growth as the Asian nations are developing rapidly, with China keen to continue its growth and so a fall-off is unlikely in the medium-term.

{kind=link}

LNG Infographic (2/3) (Shell)

LNG infographic (3/3) (Shell)

Russian invasion of Ukraine:

On 24th February 2022, Russia invaded Ukraine. In the following months, countries imposed various restrictions on Russia, with the largest (and most difficult) looking to reduce the nation's ability to export O&G. As an example, Germany, who imported over 50% of its gas from Russia before the War, is looking to phase out all Russian energy by 2024 . For this reason, nations will have to look elsewhere for O&G, with many choosing LNG.

This is extremely bullish both short-term and long-term for LNG. In the short-term, demand for vessels will increase, as LNG needs to be transported as a priority to make-up for the loss in Russian imports.

Over the long-term, more LNG will need to be transported by sea, now that energy cannot be imported through Russian pipelines.

Qatar:

Qatar is one of the largest producers of LNG, only marginally behind the US . In response to the Russian invasion, Qatar has moved quickly to secure contracts and expand its exports of LNG. It has recently agreed to supply Germany with its LNG needs, agreeing strategic partnerships with various Western O&G producers such as ConocoPhillips ( COP ) in order to facilitate this. This involves 2 expansions to the North Field, the world’s biggest single non-associated natural gas field.

Again, this is extremely bullish for LNG, increasing the volume of gas exported globally. Even if this is not transported by FLNG, this contributes to the growth of energy globally.

LNG in 2023:

Our analysis of LNG so far has been focused primarily on the medium-term onwards, so how does 2023 look?

S&P Global believe an extremely volatile year is ahead for prices, the reason for this being a lack of new liquefaction facilities. This will restrict the expansion of supply, in spite of already high prices increasing further. Prices are said to be " reaching for the stars ".

S&P Global expects a large increase in European import infrastructure in 2023 that could ease the bottlenecks, with 10 new LNG import terminals proposed or constructed that could come online. This increases both Europe's capacity for LNG, and its commitment to the energy source long-term.

Macro-economic considerations:

Energy prices are generally strongly correlated with macro-economic conditions. The logic is simple, when things are good, the demand for energy is higher as more is being consumed. With the opposite also being true.

China:

China is going through a period of change. Policy is changing in the country and is driven by the vision of Xi's common prosperity speech , while COVID-19 is causing unexpected disruptions.

Xi has remained steadfast in maintaining a policy of zero-COVID. This has led to lockdowns continuing well beyond the last in Europe or other countries in Asia. The impact of this has been twofold. Firstly, growth in China has slowed , with the knock-on effect already felt across the global. Secondly, demand for energy has fallen .

Policy changes come as China looks to re-focus the country's objectives on "common prosperity". One aspect to this has been reallocating resources away from low quality growth, such as construction. The crack-down has caused many casualties in the housing market.

It is too early to say what the new China will look like, but it is not out of the question that expenditure will be more prudent. Although this is a risk for LNG, one would expect that a sustainable level of energy expenditure must remain to fuel the nation, with LNG growth coming from an increase in proportion of total energy.

GDP growth and inflation:

One of the other factors that will likely lead to volatility in prices during 2023 is weakening GDP growth. Central Bankers are failing in bringing down inflation down, without weakening growth. Should things continue as they are, we are likely to see reduced demand for energy as consumption falls. This will have minimal impact on FLNG as only 2 charters are due to expire before the end of 2024. By then, one would expect economic conditions to improve. This is the benefit of having a quality backlog, short-term volatility can be avoided, to an extent.

Overall, our view of both the LNG market in isolation, and when factored into macro-conditions is very bullish. High LNG prices are key to high charter rates and the ability to secure long contractual agreements.

We are not necessarily arguing that FLNG will be able to secure additional contracts from Qatar's supply to Germany, alternatives to Russia or the Chinese, but that these factors will all contribute to more demand for LNG. More demand means greater use of LNG vessels.

Financials:

{kind=link}

FLNG - Financial analysis ( TIKR Terminal )

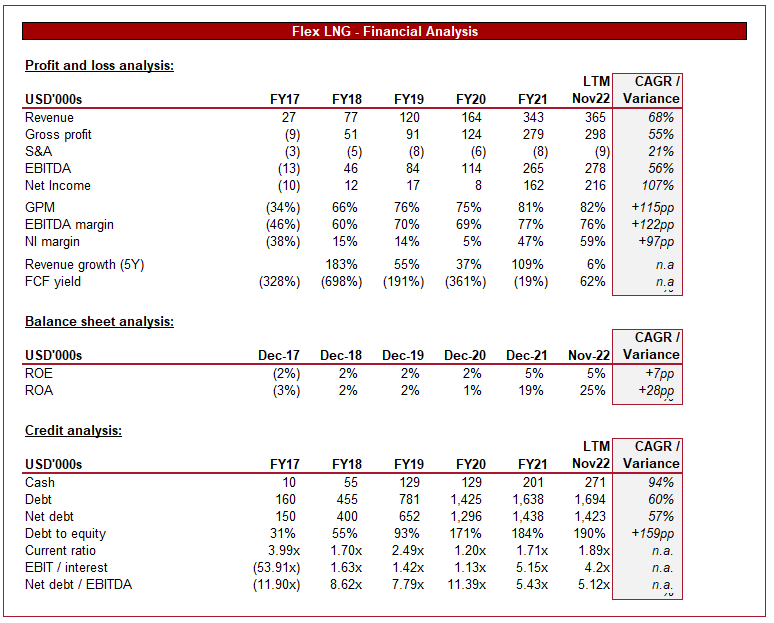

FLNG's financials are reflective of our analysis above. Revenue has grown at a CAGR of 68%, with net income exceeding that between 2018 and LTM Nov22, at a rate of 107%. Profitability will continue to increase disproportionately to costs as charter rates increase, as their cost base is relatively fixed. The largest costs above the line are vessel operating expenses, which includes personnel salaries.

Average Time Charter Equivalent ("TCE") rate of $75,941 per day for the third quarter 2022, compared to $70,707 per day for the second quarter 2022. This suggests charter rates continue to materially increase, showing no drop due to economic weakness.

FLNG utilize numerous derivatives in order to hedge the impact of interest rates on their loan book. In the 9M Sept22 period, a gain of $75M was made (exceeding interest payments of $52M). This is an important factor for investors to consider as the majority of FLNG's debt is pegged to changes in interest rates.

Free cash flow has finally turned positive, as large capex payments have ceased. This is positive news for investors, as much of their operating cash flow can now be utilized for dividends.

From a balance sheet perspective, we observe debt-to-equity increasing substantially over the historical period. FLNG has utilized various debt facilities and sale-and-leasebacks in order to finance their vessels. As the fleet size has increased, further debt has been obtained. Management have been in the process of re-financing their ships, the net impact has been cash released and reduced interest payments.

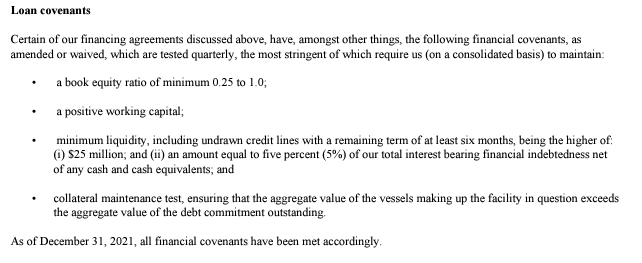

Although the net debt balance can look concerning, especially when the company is paying the levels of dividend it is, we must remember the nature of the business. With a strong backlog and contractual arrangements as far as 2027, revenue is fairly certain. Therefore, the business faces lower risks, as they can financially pay interest payments with hedging instruments. The only risks are with ensuring covenants are meant, which are listed below. Currently all requirements are healthily maintained.

{kind=link}

FLNG Covenants (FY21 Annual report)

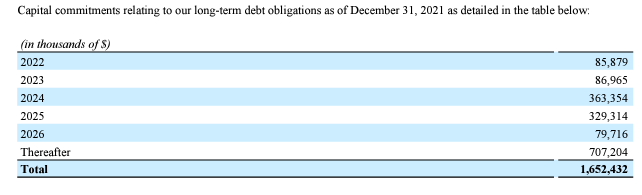

FLNG has the following capital commitments expected

{kind=link}

Capital commitments (FY21 Annual report)

FLNG has the following options outstanding:

Share options outstanding (FY21 Annual report)

These represent c.0.1% of outstanding shares.

Outlook:

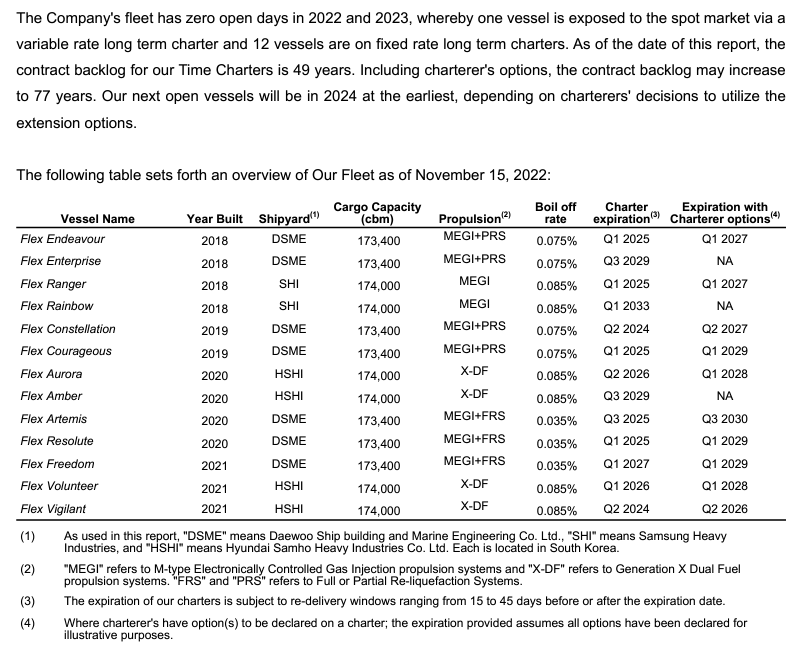

FLNG estimate that the cost of a new build ship is now $250M, with deliveries only taking place from 2027 onwards. This puts FLNG in a fantastic position to remain fully utilized until then (majority of contracts expiring around this date). For this reason, it is not out of the question that FLNG remains, at a minimum, this profitable for at least the next 5 years. This is truly a unique trait in the business world.

{kind=link}

FLNG's Fleet composition (FLNG - Q3 Investor pack)

Dividends are currently yielding 9.1%. Our view is that this is sustainable going forward, especially once all intended refinances are complete.

Overall, the profitability profile and financial position of the business is very good. Margins are high and costs have been controlled. This will ensure continued strong dividend payments to investors.

The business has hedged its debt, eliminating much of the interest rate risk on their floating exposure. This contains any liquidity risk and provides the potential for upside, as observed.

Valuation:

FLNG is currently trading at a 11.4x NTM EV/EBITDA and 10.7x NTM earnings. Between 2018-2022, NTM EV/EBITDA has averaged 10.2x. There are few comparable companies in the LNG market with a purely modern fleet and so a relative valuation is difficult to assess.

FLNG is certainly trading at a premium to the shipping industry as a whole, but our analysis above is the justification of this. Investors considering FLNG should acknowledge that they are not purchasing this stock at a discount, and to an extent are banking on a multiples expansion with capital growth.

Downside protection comes in the way of sustainable dividend payments.

With a market cap of c.1.7BN, investors should consider volatility as a great risk. Investing in stocks this size, and in the shipping industry, is not for the faint-hearted. Double-digits swings are regular occurrences with little evidence as to the reason. We are not in the business of timing the market and so cannot merely suggest waiting when we still see value on the table. The stock was up 33% in 2022, the year the S&P closed down 20%. There is no certainty of a correction coming.

Conclusion:

As much of this paper clearly reflects, we are very bullish on LNG. LNG seems to be the stop-gap energy source between oil/coal in the last few decades and a completely green future.

FLNG is positioned well to benefit from this, securing record high charter rates and operating a modern fleet. Vessel supply is sticky, which has led to a several year backlog. This will mean sustainable growth in profits, and dividends for investors. Capital appreciation may come as deleveraging occurs, or if dividend yields increase.

The price for FLNG is steep, however. A poor 2023 could bring markets down, with FLNG following. Investors must be willing to bear the risk of this, with an eye fully on fundamentals. FLNG represents one of our riskier investment proposals, which may be reduced somewhat by a dollar-cost average approach in the coming 6-12 months.

For further details see:

FLEX LNG Positioned To Benefit From Positive LNG Outlook