FLNG - FLEX LNG's Contracts Give It Strong Earnings Visibility

2023-05-03 05:42:16 ET

Summary

- FLNG has solid visibility into future earnings and cash flow given its contracts.

- It has an attractive 9% yield and the dividend is safe.

- FLNG stock is valued near the cost to replicate its fleet.

FLEX LNG ( FLNG ) provides a lot of visibility given its long-term contracts. The stock is a solid option for investors looking for a high yield.

Company Profile

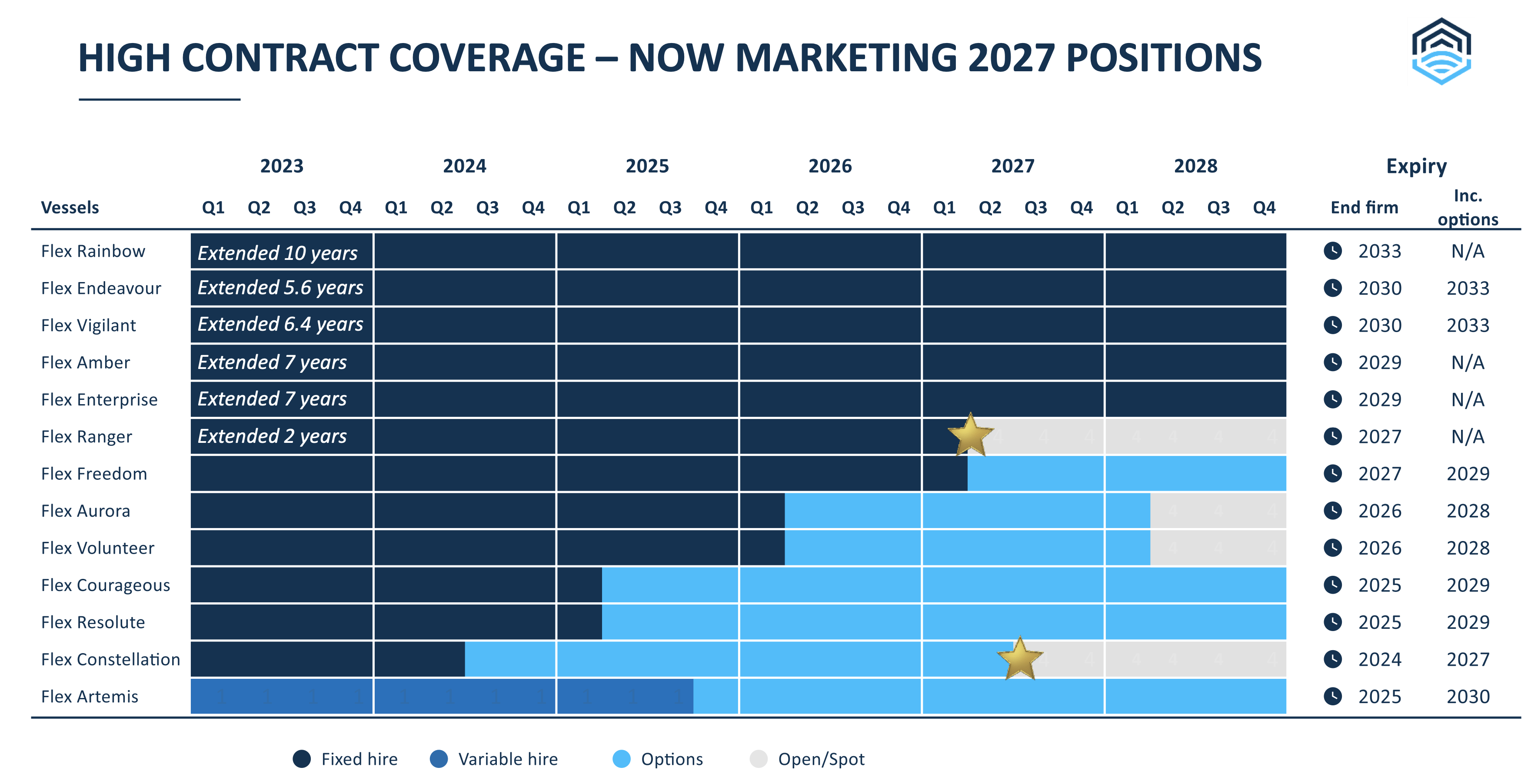

FLNG owns and operates a fleet of LNG carriers. The company has 13 vessels, all of which have with XDF or MEGI propulsion engines.

The company has a young fleet, with an average age of just over 3 years. Twelve of its vessels are on fixed-rate time charters, while one of its ships is on a variable rate contract that is indexed to the spot market. As of early March, eight of its vessels were on time charters expiring in two to five years, while 5 ships were on time charters expiring after 5 years.

FLNG's customers include LNG producers, such as oil & gas producers, as well as energy trades and industrial LNG users. The company's four largest customers represented nearly 88% of its 2022 revenue.

The company does get technical management and support services from a related party called FLEX LNG Fleet Management. It paid the related party $3.5 million for these services in 2022.

Opportunities and Risks

With 12 of its 13 ships on time charters, FLNG has strong earnings and cash flow visibility and is not as exposed to the spot market as many other shippers in various types of marine transport. When you look at LNG producers, such as Cheniere ( LNG ), which is a FLNG customer and a company I recently wrote about , contracts in the industry are generally very long-term take-or-pay contracts. As such, it makes sense for producers and users to lock-in longer-term charters to add visibility on the cost side.

That said, spot rates can still impact FLNG's earnings, as its one vessel is on a contract tied to spot rates. On that front, the company is expecting its average TCE (time charter equivalent) to increase this year from about $72,000 a day in 2022 to $80,000 a day this year. As a result, it expects revenue to grow 6% from $348 million in 2022 to $370 million in 2023. Notably, four of the company's vessels are scheduled for drydocking this year, which is why its TCE growth is higher than its overall projected revenue growth.

In the fall of 2022, there was a lot of LNG tonnes being stored in vessels due to contango in gas prices and congestion in European ports. This led to a tight LNG shipping market and thus higher spot rates. As LNG prices started to come down, so did spot rates. The spot rate for LNG shipping is pretty volatile, and the market isn't the most liquid, as many ships are on long-term charter.

Where term rates fall when FLNG renews or finds new contracts for its vessels will also play a role in its future earnings. Its Flex Constellation vessel contract ends mid-year 2024, and the charterer has the option to extend the contract exercised further out. Meanwhile, its Flex Courageous and Flex Resolute ships have contracts that end in early 2025, also with options to extend.

{kind=link}

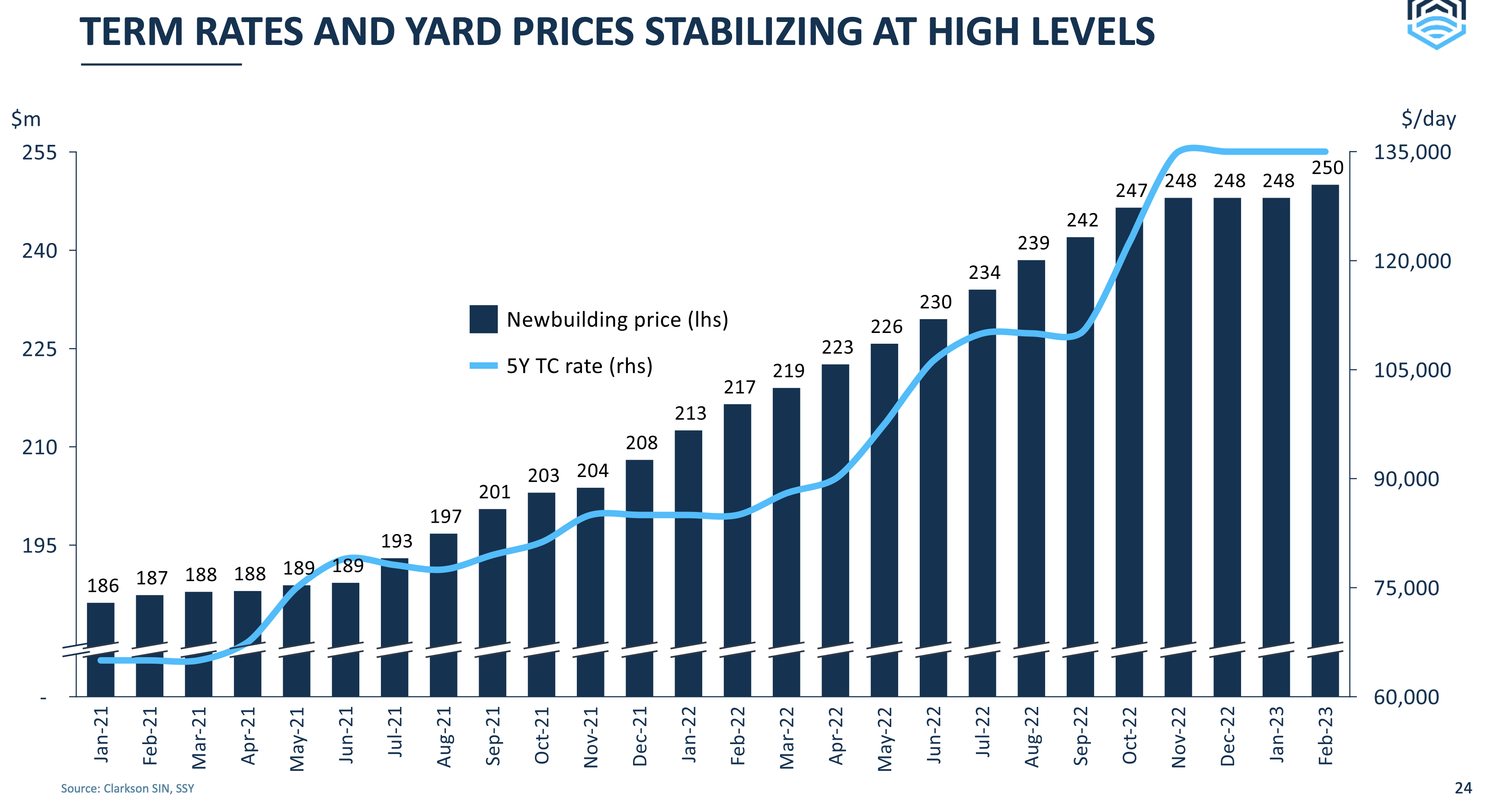

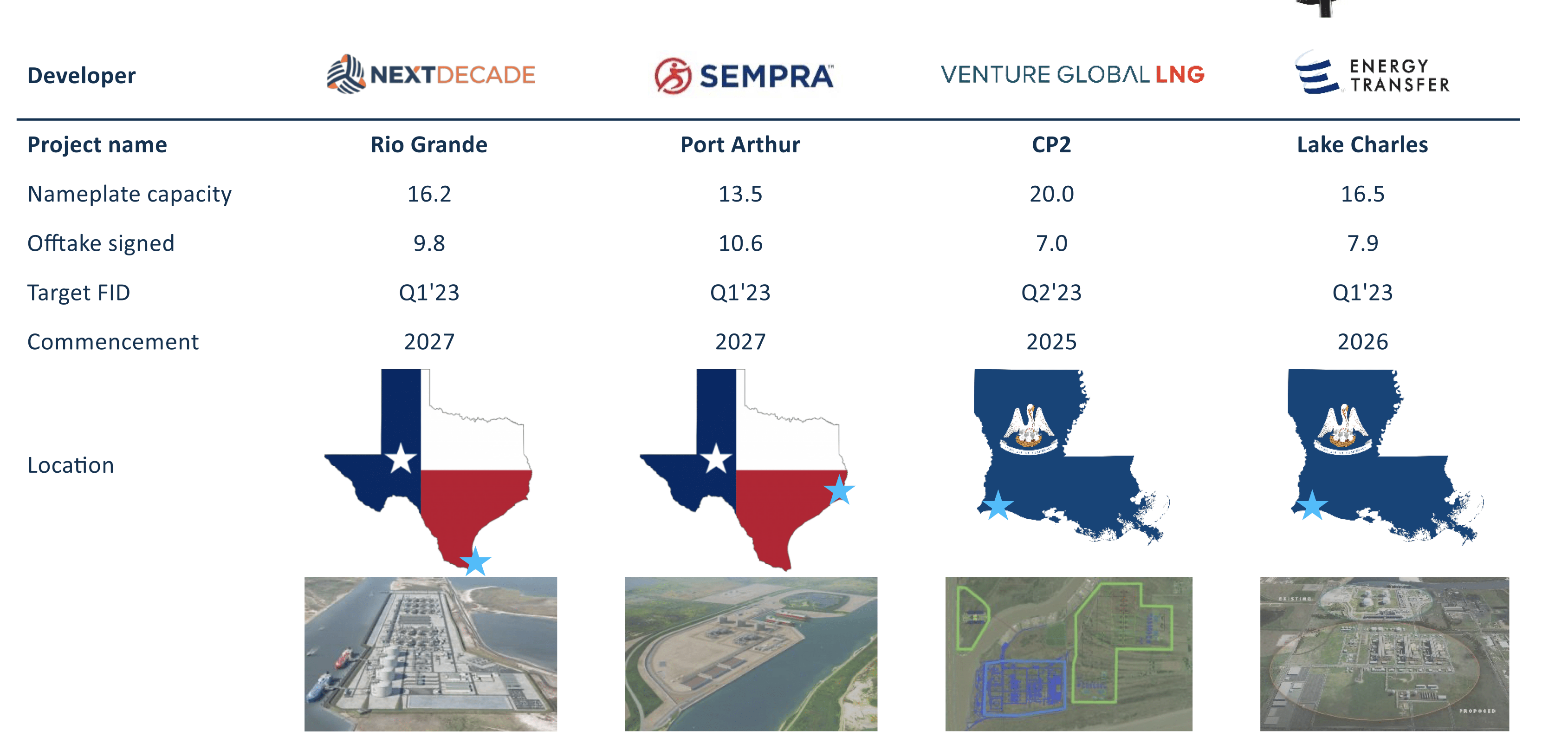

However, the company expects all these options to be exercised, and it is more looking towards 2027 as the year it will it need to find new contracts for some of its ships. This included the aforementioned Flex Constellation, as well as the Flex Ranger, which was just extended until 2027. The company feels good about having ships available at this time, because newbuild ships prices have risen to $250 million for delivery in 2027-28, which is well above the $180-185 million in paid for its vessels. The higher newbuild prices, meanwhile, is driving up term rates as a result. The company said 5-year term rates were around $135,000 a day when it held its Q4 conference call in February. Meanwhile, it sees a lot of LNG capacity coming online in the next few years.

{kind=link}

Discussing current LNG projects on its Q4 earnings call , CEO Oystein Kalleklev said:

"I'm looking forward, however, there is still plenty of new projects coming to the markets especially around '25, '26, '27 When as I mentioned we are marketing ships. We have a lot of projects under construction. As you can see here, $95 million Rest of the World, of course the Qatar is the big driver here, and then some projects in North America like Golden Pass and LNG Canada, we also have some projects being already reached FID. So, if we look at the project under construction, and those who have been given the green light to start construction, we are ending up at our volume of 583 million tonnes. However, we also expect more investment decisions to be made especially in America, as I highlighted on this arbitrage where Henry Hub prices are very low compared to international prices. So the project we see here highly likely I will come back to this 73 million tonnes more than U.S., 46 Rest of the World which can bring this market to 700 million tonnes by 2030."

One of the big opportunities for FLNG is that as its contracts roll-off in several years, it should be able to get much higher term rates. However, this won't start until 2027.

When looking at risks, these large LNG projects need to come online for LNG shipping rates to remain strong. At the end of 2022, there were 658 LNG vessels, while the orderbook was for about 285 ships. That's a massive 43% increase in the number of vessels, so there needs to be a lot of LNG production to come online in the next few years.

{kind=link}

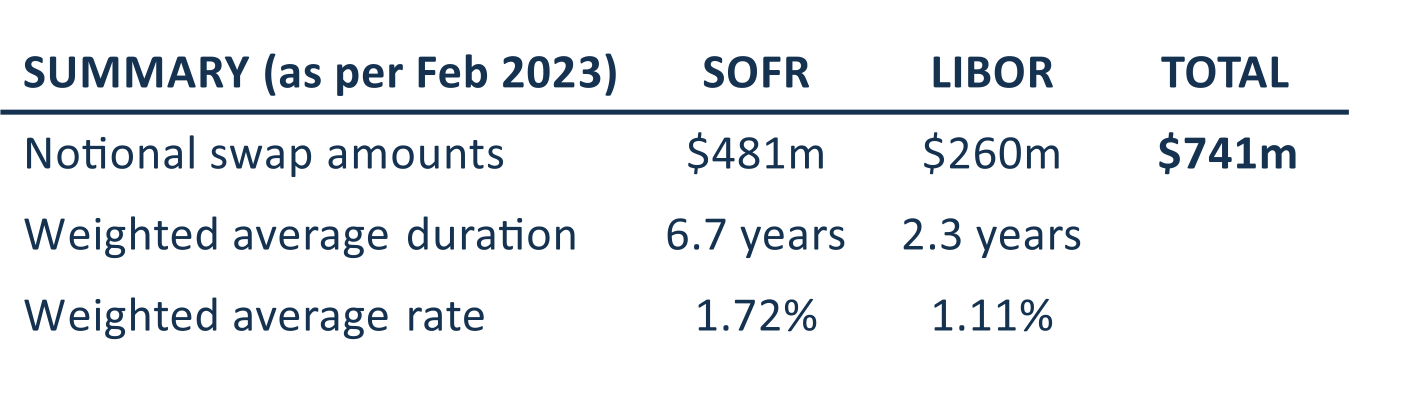

FLNG also has a lot of variable rate debt associated with its ship financing. Its debt and leasebacks are variable rate, so it faces interest rate risk. However, the company has aggressively hedged a little over half its debt through swaps to essentially turn that portion of its exposure into fixed rates.

{kind=link}

Valuation

FLNG trades at 10.5x the 2023 EBITDA of $286.6 million and 10x the 2024 EBITDA consensus of $296.6 million.

On a PE basis, it trades at 10.8x EPS estimates of $3.06. Based on the 2024 consensus for EPS of $3.13, it trades at 10.6x.

Dorian's (LPG) stock trades at a premium to other LNG shippers such as GasLog Partners ( GLOP ) and Dynagas LNG ( DLNG ), both of which have older fleets. GLOP is also in the process of merging with its parent company.

Conclusion

FLNG has a nice modern fleet of LNG vessels that are currently on contract at below market rates. This creates nice visibility into its earnings and cash flows, as well as gives upside in later years when it should be able to re-contract its fleet at more attractive rates.

Meanwhile, its 9% yield is attractive and the dividend safe. That said, I think the stock is appropriately valued at current levels. The stock is trading just below what it would cost to replicate its fleet with new LNG vessels. The simple math is $250 million per ship and 13 vessels.

As such, I think the stock is a solid "Hold" for investors looking for a nice high yield, and I'd be a buyer on any outsized dips.

For further details see:

FLEX LNG's Contracts Give It Strong Earnings Visibility