FLNG - FLEX LNG: Upgrading To 'Buy' As Vessel Values Increase

2023-09-27 17:37:45 ET

Summary

- FLEX LNG Ltd. has solid visibility into future revenue and cash flows due to its contracts.

- The company's steady performance is supported by its young, modern fleet and limited exposure to the spot market.

- FLEX LNG stock offers a solid dividend and has nice price appreciation potential.

Back in May , I said FLEX LNG Ltd. ( FLNG ) had solid visibility into earnings and cash flow given its contracts, but that the stock looked fairly valued. Let’s catch up on the name.

Company Profile

As a refresher, FLNG owns and operates a fleet of 13 LNG carriers, all of which have with XDF or MEGI propulsion engines. With an average age of just over three years for its vessels, the company has a young, modern fleet.

As of mid-August, nine of its vessels were on time charters expiring in 2026 or later. Its next open vessel is in Q2 2024, if its customer doesn’t exercise its option to extend the charter.

Solid Q2 Results

For its most-recent quarter, FLNG recorded vessel operating revenue of $86.7 million, up 3% from $84.2 million a year ago. The company had three ships off-hire in the quarter for their scheduled 5-year special survey in drydock. It has no more drydock days schedules for the year.

The company realized time charter equivalent ((TCE)) rates of $77,218 a day in the quarter, up from $70,707 last year. This was helped by the upward re-pricing of contracts that came off charter over the past year. However, that was down from $80,175 a day in Q1.

Opex per day rose to $14,618 from $12,990 a year ago and $13,424 in Q1.

Net income came in at $39.0 million, or 72 cents per share, versus $44.3 million, or 83 cents a share, a year ago. The results were hurt by $11.3 million in additional interest expense as a result of higher interest rates. Adjusted net income was $28.2 million, or 52 cents, versus $32.5 million, or 61 cents a share, a year ago.

Adjusted EBITDA came in at $66.2 million, largely unchanged from $66.1 million a year ago, and down -9% from $72.5 million in Q1.

The company declared a dividend of 75 cents for the quarter.

Turning to its balance sheet , FLNG ended the quarter with debt of $1.86 billion. It had cash and equivalents of $449.9 million. The company has no debt maturities before 2028.

Most of its rates are floating, but the company did enter swap transactions to create a fixed rate on $820 million of its debt. These hedges produced at gain of $17 million in the quarter. It also has $201 million of fixed rate leases.

Looking ahead, the company reiterated its guidance for Q3 and Q4. It expects to generate revenue of $90-95 million in Q3 and between $90-100 million in Q4. It is looking for revenue of $370 million for the full year.

The company forecast adjusted EBITDA of between $290-295 million for the year.

Management noted that it will have all 13 of its vessels on the water in the second half, and that its Flex Artemis vessel will benefit from higher spot rates. As a reminder, this vessel was chartered is the only one with a contract tied to spot rates.

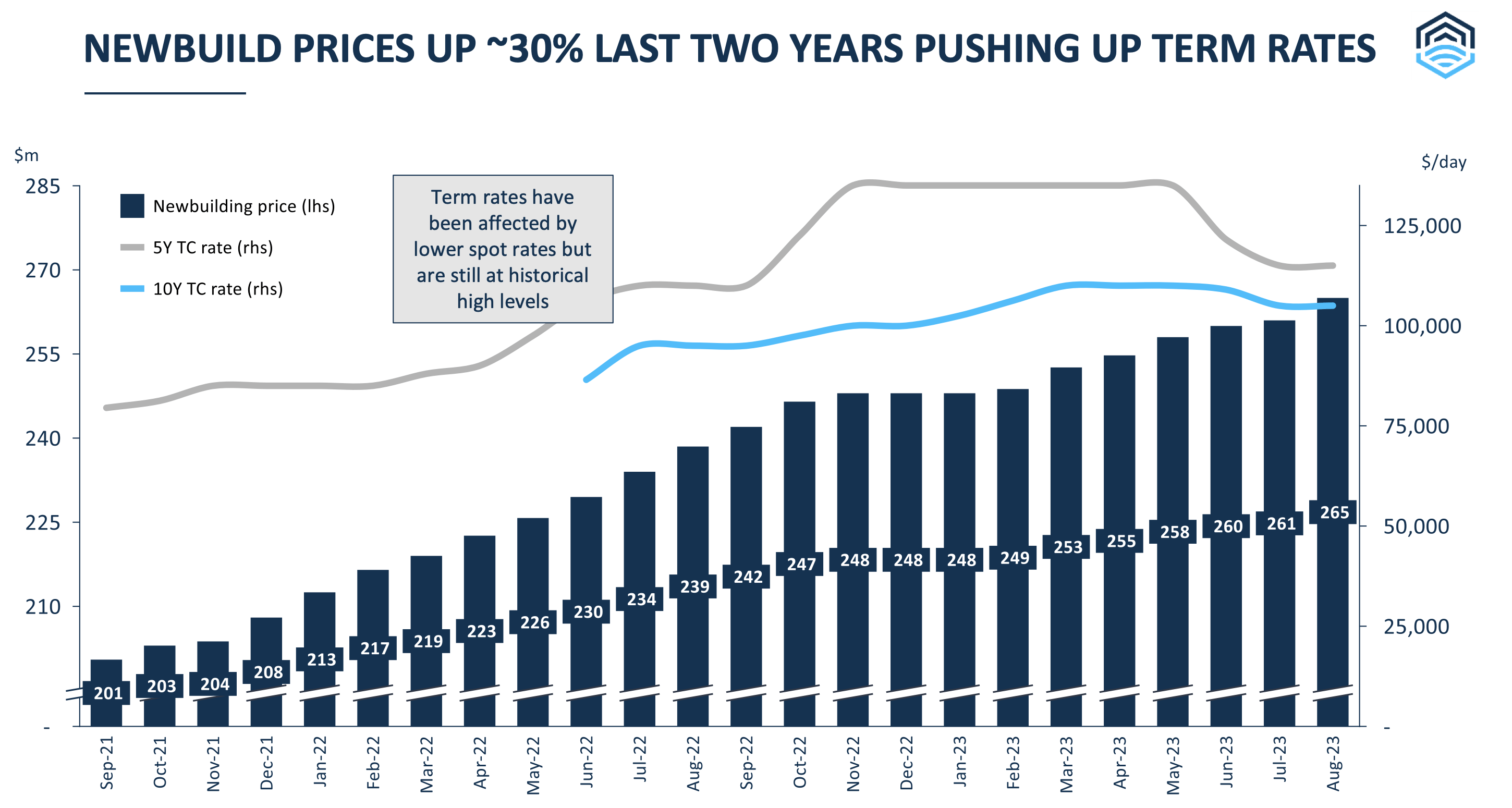

On its call, the company noted that spot rates are above $100,000 a day for modern vessels, with prices for winter above $200,000 a day. Unlike most markets, there is a healthy backlog on newbuild ships coming to the market the next few years, with 63 scheduled for 2024, 84 in 2025, 77 in 2026, and 46 in 2027, before it tapers off in 2008 to only 5. However, this also coincides with new LNG supply expected to hit the market in the next few years from projects currently under construction or where the FID has been made. Newbuild ships are currently cost around $265 million to build.

Discussing the outlook for re-contracting its ships in outer year on its Q2 earnings call , CEO Oystein Kalleklev said:

"So today the ten-year rates as you can see here in the light blue line is hovering about -- above $100,000 and then at about $150,000 for a five-year time charter rate. So this is one of the reasons why we are also very optimistic about re-contracting our ships. We have two ships open in '27, competing with these ships. And then two ships also in '28, where we do think that once we are re-contracting ships, we will be doing that at higher levels, which we have also done and evidenced in the past. Looking at the order book, we had a lot of contracting of newbuilds last year with these higher prices. We have seen fewer contracting these days. But the order book is big and it's also reflecting of the fact that we have a lot of new volumes coming to the market and it's reflecting the fact that still we have a lot of steam propulsion on water with 35% of the fleet consisting of steamships and we do see more and more of these ships leaving the shipping market and have to be replaced by more modern fuel-efficient tonnage, driven by economics, driven by regulation, and also to -- from next year, actually carbon taxation in European Union. If we look at the order book today, most of the ships are committed to long term charters. Only about 10% of the ships in order book ae uncommitted so far.”

{kind=link}

Overall, FLNG put up the steady type of results you’d expect, given that only one of its thirteen vessels is tied to the spot market. This means the biggest variables for the company are opex and interest rates. Interest rates continue to be a drag given much of its debt is floating, but it hedging out a solid portion of this debt has turned out to be a smart move. Opex continues to creep up slowly, meanwhile.

Going forward, the company should be in solid shape to hit its targets for the rest of the year. 2024, meanwhile, should be slightly better than 2023 as it will have less drydocking days.

Valuation

FLNG trades at 10.3x the 2023 EBITDA of $290.2 million and 10.0x the 2024 EBITDA consensus of $298.8 million.

On a P/E basis, it trades at 13.1x EPS estimates of $2.33. Based on the 2024 consensus for EPS of $2.57, it trades at 11.9x.

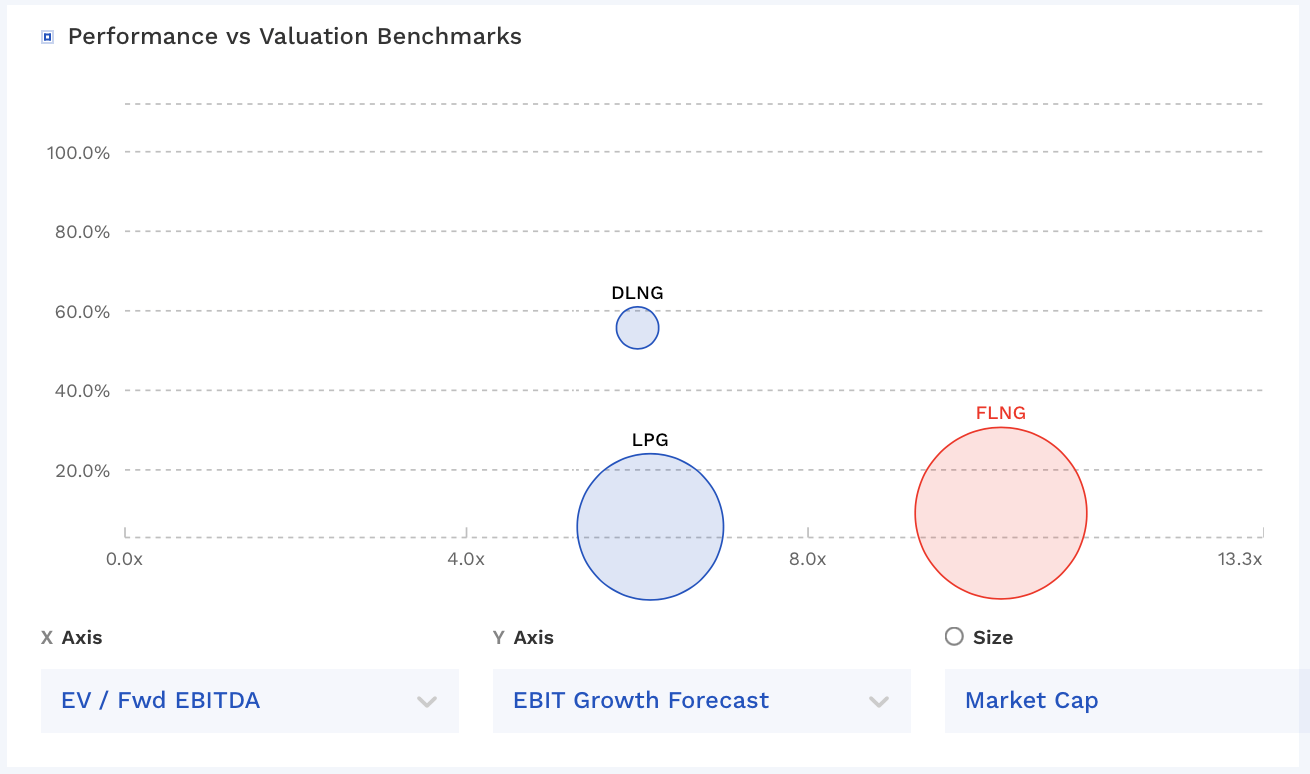

FLNG trades at a premium to other LNG and LPG shipping operators such as Dorian ( LPG ) and Dynagas ( DLNG ), although it has a younger, more modern fleet.

FLNG Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

Giving its contracts, FLEX LNG Ltd. continues to have great visibility into future revenue and cash flows. It could be earning more money on the spot market, but in exchange, investors are going to get a steady performer. The biggest negative at this time is just interest rates and FLNG’s variable debt, although hedging some of its interest rate risk has proven to be a smart move.

The price of newbuilds continues to go up, and it would now cost about $3.4 billion to replicate FLNG’s fleet. Given its young, modern fleet and the time to build new ships, I think we can use that as a way to value FLNG. That would put the stock at $38, which combined with its $3 a year dividend, would get you to about 33% return.

I think that is enough to upgrade FLEX LNG Ltd. stock to “Buy” for income oriented investors. The dividend is well covered by operating cash flow at about 1.4x.

For further details see:

FLEX LNG: Upgrading To 'Buy' As Vessel Values Increase