FLEX - Flex: Margin Expansion Is The Name Of The Game

2023-11-19 03:44:39 ET

Summary

- The EMS industry has thin profit margins due to complex supply chains, changing customer demands, and large capital investments.

- The company focuses on high-margin sectors and operational optimization initiatives to expand margins.

- Its margin expansion trajectory indicates significant value creation over the next few years.

Investment Thesis

Flex (FLEX) is a global electronics manufacturing services ((EMS)) company, that operates in a challenging and cyclical market. The EMS industry is characterized by thin profit margins due to complex supply chains, changing customer demands, and strict quality standards. To remain competitive, they have to constantly invest in new technologies, equipment, and facilities which are all cost drivers that reduce the profitability of EMS companies.

To address these challenges and improve its profitability, Flex has implemented a margin expansion strategy, focusing on three key initiatives: elevating its high-margin portfolio, optimizing operations, and boosting productivity. In this article, we will examine the company's margin expansion strategy and the impact on its valuation.

Elevating High Margin Portfolio

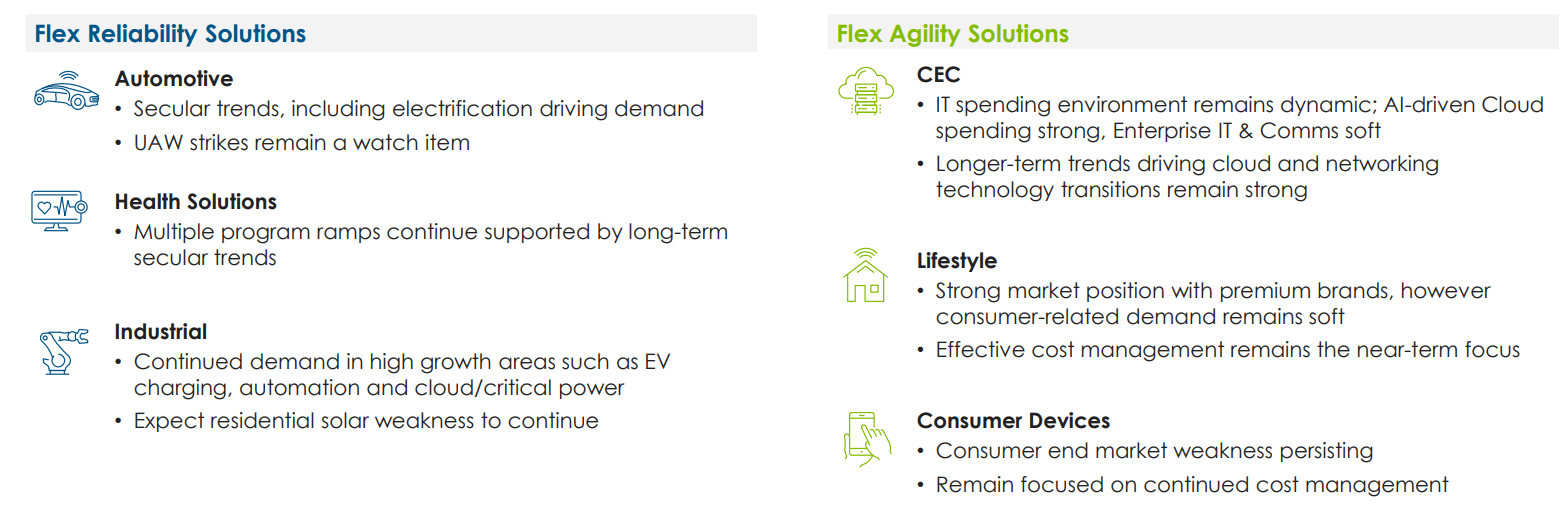

Flex strategically focuses on high-margin sectors such as digital health, automotive, and cloud solutions to grow and improve profitability. Flex operates in two business segments: Reliability and Agility. The Reliability segment, which has a faster growth rate and higher margins, includes the automotive and digital health solutions (see below)

Flex Portfolio Segments (Flex Q2 Earnings Presentation)

{kind=link}

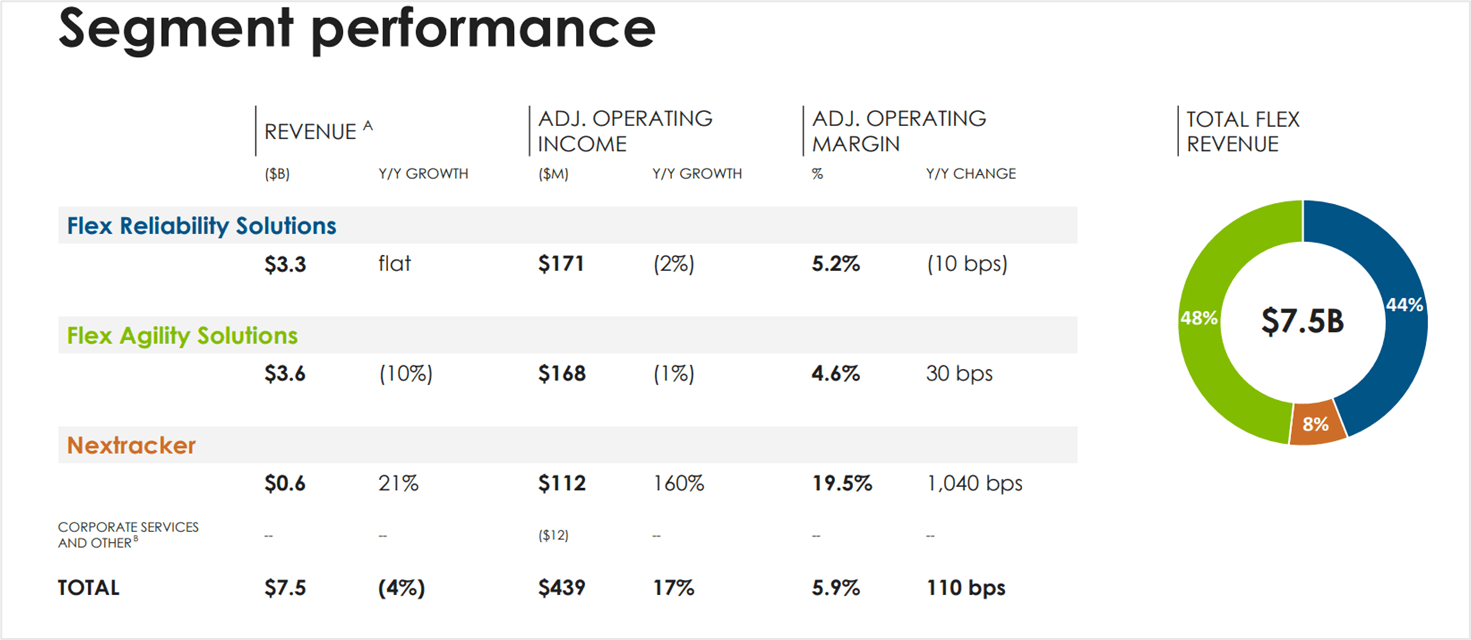

The Q2 2024 earnings report shows a 5.2% adjusted operating margin in the Reliability segment compared to Agility's segment margin of 4.6%, highlighting the success of this strategy. This concentration on digital health and automotive is leading to strong quarterly margin expansions.

Flex Segment Performance (Flex Q2 Earnings Presentation)

{kind=link}

The digital health market is growing fast, driven by technologies such as wearable devices, telemedicine, personalized medicine, medical device automation and AI healthcare. According to a report by Fortune Business Insights , the global digital health market size is projected to grow from $452 billion in 2023 to almost $2 trillion by 2030, at a CAGR of 23%. As seen from the market size numbers, digital health is a very large market that has a lot of potential for Flex. In FY 2023, the Health Solutions segment of Flex grew by 9% and we expect it to continue its strong performance in the future.

The EV market is also growing at a rapid pace, driven by various factors such as increasing environmental awareness, government zero emission policies, technological advancements, and consumer preferences. According to a report by Allied Market Research , the global EV market was valued at $163 billion in 2020, and is projected to reach $823 billion by 2030, growing at CAGR of 18% from 2021 to 2030. Flex is well positioned in this market as well. Its automotive business grew by 22% in FY2023 and we project its growth to continue at a similar pace.

Optimizing Operations

Flex invests in factory and supply chain optimization initiatives by leveraging advanced technologies such as IoT, AI, and robotics. Flex's continuous improvement culture combined with these advanced technologies is driving key optimization results such as enhancing quality control, automating inventory management, and logistics efficiencies. Notably, the company received the Manufacturing Excellence Award for its achievements in lean manufacturing. The company was recognized for its lean innovations that enable real-time operations and intelligent decision making by leveraging Industrial IoT.

Flex Sustainable Manufacturing (Flex)

{kind=link}

Another great example of Flex optimizing operations is their AI-driven contract management process. This tool has been recognized as a 2023 Value Champion Award winner by the Associate of Corporate Counsel (ACC), which is world's largest network of legal professionals. Flex is using this tool to optimize its supply chain contract review process which reduces the duration from several days to five minutes.

We think that at the core of these achievements lies Flex's high performing workforce culture which Flex enables with various employee development and training programs. This ensures that they are actively engaged in driving efficiency and innovation initiatives across the organization.

Boosting Productivity Through AI

AI is a powerful tool that can generate significant value across the entire product life cycle and supply chain. According to a McKinsey's report , AI can boost marketing productivity by up to 15%, cut customer operations costs up to 40%, save software development costs up to 45%, increase R&D productivity by 15% and more. Also Goldman Sachs Group estimates that AI can increase US companies net margins by nearly 4% over a decade.

The Economic Potential of Generative AI ((McKinsey & Company))

AI will transform all industries and enhance labor productivity. We believe that technologically advanced manufacturing companies like Flex will gain the most from this technology revolution. Flex has many use cases where AI can improve its employees' performance and efficiency. It can increase Flex's labor productivity across the organization by automating repetitive tasks, optimizing workflows, and generating insights. Our view is that by combining AI with other technologies, Flex could achieve an additional 2-3% of labor productivity growth per year, which will positively impact its margins.

Financial Performance Review

According to the 2024 Q2 earnings report, Flex reported net sales of $7.5 billion which represents a decrease of 3.8% YoY. The decline in sales was attributed to macro market weakness in the communications, enterprise and consumer sectors.

The company’s adjusted operating margin improved by 110 basis points to 5.9% from 4.8% last year. This improvement in operating margin shows Flex's commitment to operational efficiency and cost management.

Margin Trajectory

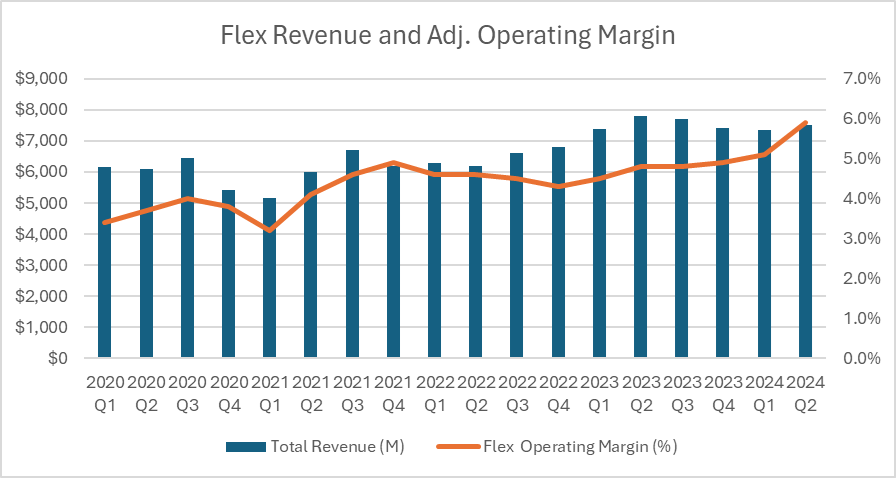

Flex has been improving its profitability over time, indicating that it is becoming more efficient each year. The graph below shows how Flex has been steadily expanding its operating margins by leveraging its core competencies in high-margin markets and managing its costs effectively.

Flex Revenue and Operating Margin (Author)

{kind=link}

Looking forward, the company expects to achieve operating income of $375 million to $425 million in Q3, which would represent an adj. operating margin of 6% (+120 bps YoY). This shows that Flex is determined to continue its margin expansion trajectory.

Valuation

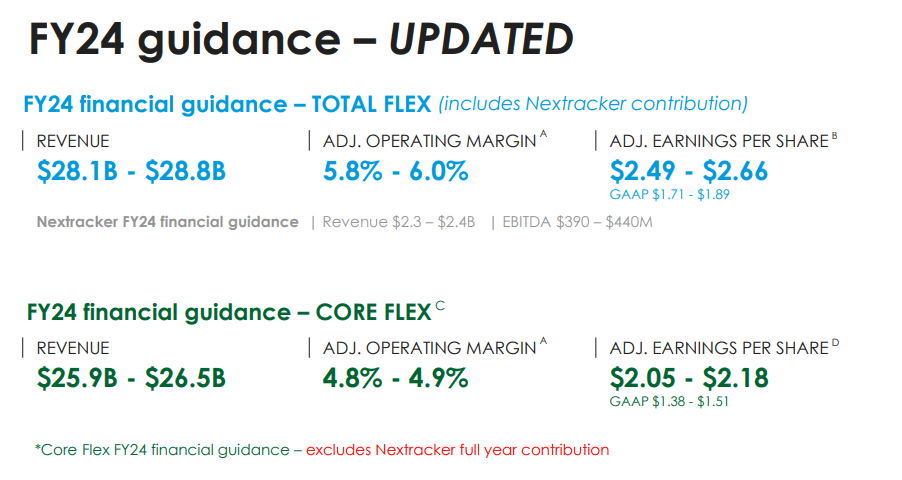

Flex will spin-off its Nextracker business in FY24, so we will not include Nextracker in our valuation. Without Nextracker, Flex's core business has an adjusted operating margin of 4.7%, and the company expects it to reach 4.9% for FY 2024 (see below chart). The company also aims to achieve an adjusted EPS target of $2.65 for FY25, which is a 26% increase from FY24.

Based on this guidance and the current margin trend, we estimate that Flex will be able to grow its operating margin at a CAGR of 20%, and reach an adjusted operating margin of 8% by fiscal year 2027. This implies that Flex can boost its EPS by at least 60% over the next three years, which would result in a price target of $41 based on its current P/E multiple.

Flex FY24 Guidance (Flex Q2 Earnings Presentation)

{kind=link}

We believe that this is a fair valuation, as we expect Flex to also benefit from improved market conditions starting from fiscal year 2025.

Risks

Risks to our valuation are as follows:

Competition : The company faces strong competition in a cyclical industry. It has to compete with leading global contract manufacturers that may impact its market share.

Macro Uncertainties : Flex is a global company and is exposed to macroeconomic uncertainties, geopolitical conflicts and supply chain disruptions that may affect its customer demand and operational efficiency.

Conclusion

Flex is a company that keeps its operational efficiency even in the face of macro uncertainties. The company’s strategic approach, which focuses on high-margin solutions and operational optimizations positions Flex for sustainable margin expansion.

With a projected 60% increase in its earnings over the next 3 years, we see substantial value in Flex and rate it as a Buy.

For further details see:

Flex: Margin Expansion Is The Name Of The Game