PSA - Flight To Quality Is A Must

2023-10-15 07:00:00 ET

Summary

- The stock market is facing multiple challenges, including sticky inflation, elevated rates, weakening economic growth, and geopolitical problems.

- The Consumer Price Index exceeded expectations in September, indicating stronger price growth.

- The possibility of a recession is increasing, as shown by declining consumer confidence and the Animal Spirits Index.

This article was co-produced with Leo Nelissen.

“It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” Warren Buffett

The stock market continues to tumble, pressured by sticky inflation, elevated rates, weakening economic growth, and new geopolitical problems.

For example, one of the biggest issues, sticky inflation, continues to remain a problem.

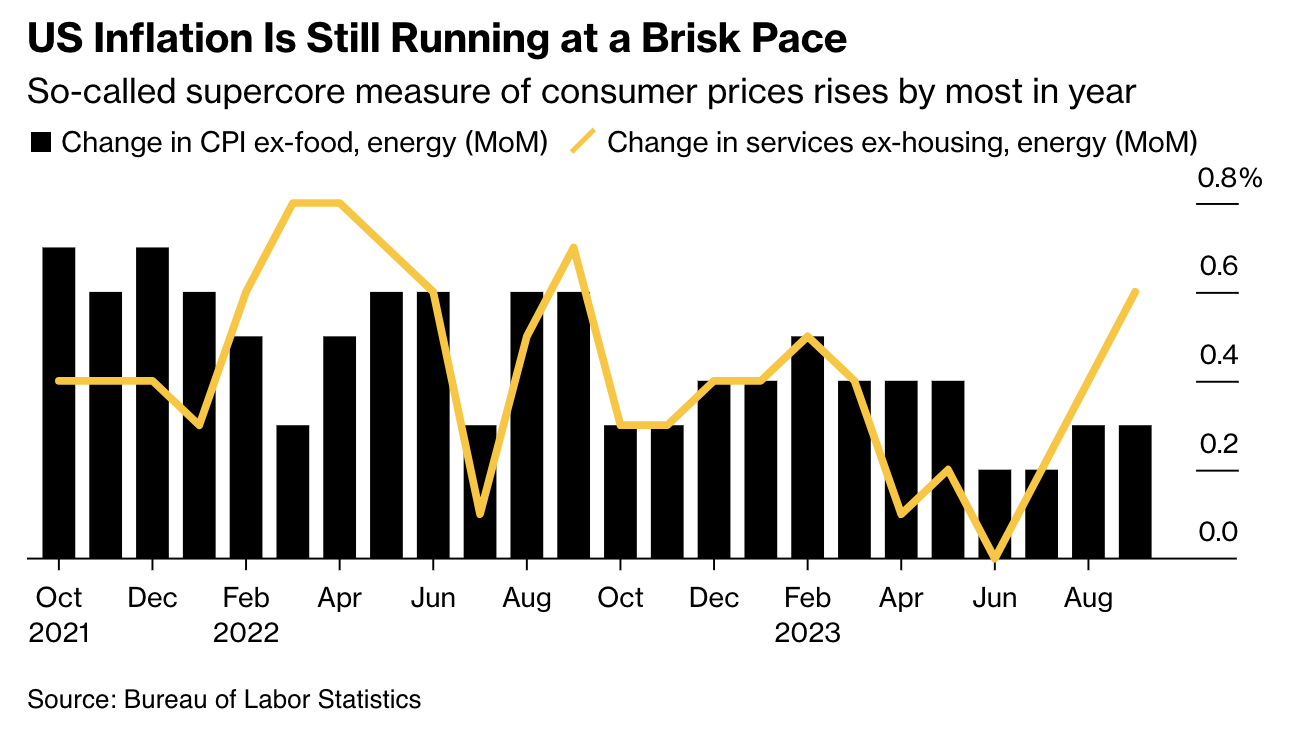

In September, the Consumer Price Index (“CPI”) exceeded expectations, indicating a stronger price growth of 0.4% compared to the anticipated 0.3% rise.

The core CPI, excluding food and energy, increased by 0.3%, aligning with projections.

{kind=link}

Although core goods prices continued to fall, core services inflation saw a monthly increase of 0.6%. This uptick was primarily attributed to a surge in owners' equivalent rent, which is not expected to be sustained, and a notable rise in the lodging away from home category.

While there has been progress in curbing inflation over the past year, achieving the target of 2% inflation sustainably remains a challenge. The recent slower pace of improvement suggests that reducing inflation will be more gradual in the coming months, which is corporate speak for “inflation will remain sticky.”

Various factors, including production disruptions and rising energy and used vehicle auction prices, could influence the trajectory of inflation.

This is what Bloomberg economists Anna Wong and Stuart Paul wrote :

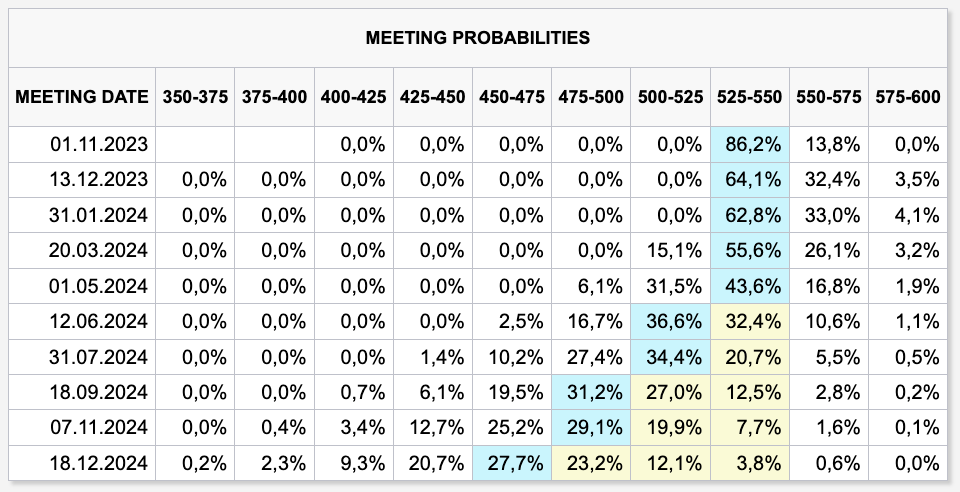

“The September CPI report won’t convince most Fed officials that interest rates are sufficiently restrictive... Our baseline is for the Fed to hold rates steady for the rest of the year, but we see non-negligible risks of another rate hike, something the market is probably underpricing.”

Looking at Fed Funds rate futures, we see that the market expects no cut until June 2024. It sees a 35%-ish probability of a hike in December.

{kind=link}

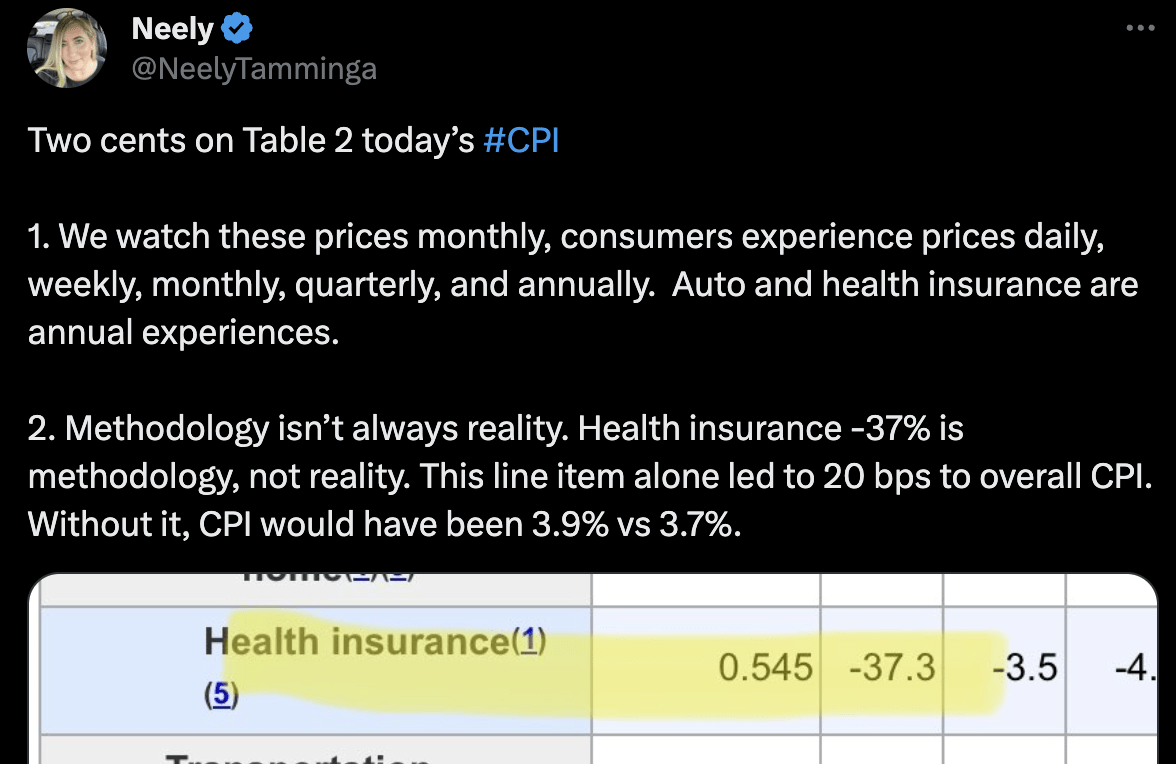

It also doesn’t help that data seems to be fudged to make inflation look lower than it really is.

This is happening all over the place.

In German data, we recently saw that energy costs are now getting a lower weight.

In the U.S., we see that a simple methodology change in health care had a 20bps impact on CPI, as calculated by Neely Tamminga .

{kind=link}

While sticky inflation is already an issue, it gets worse as general economic growth is in a bad spot.

We’re seeing increasing hints that a recession is nearing.

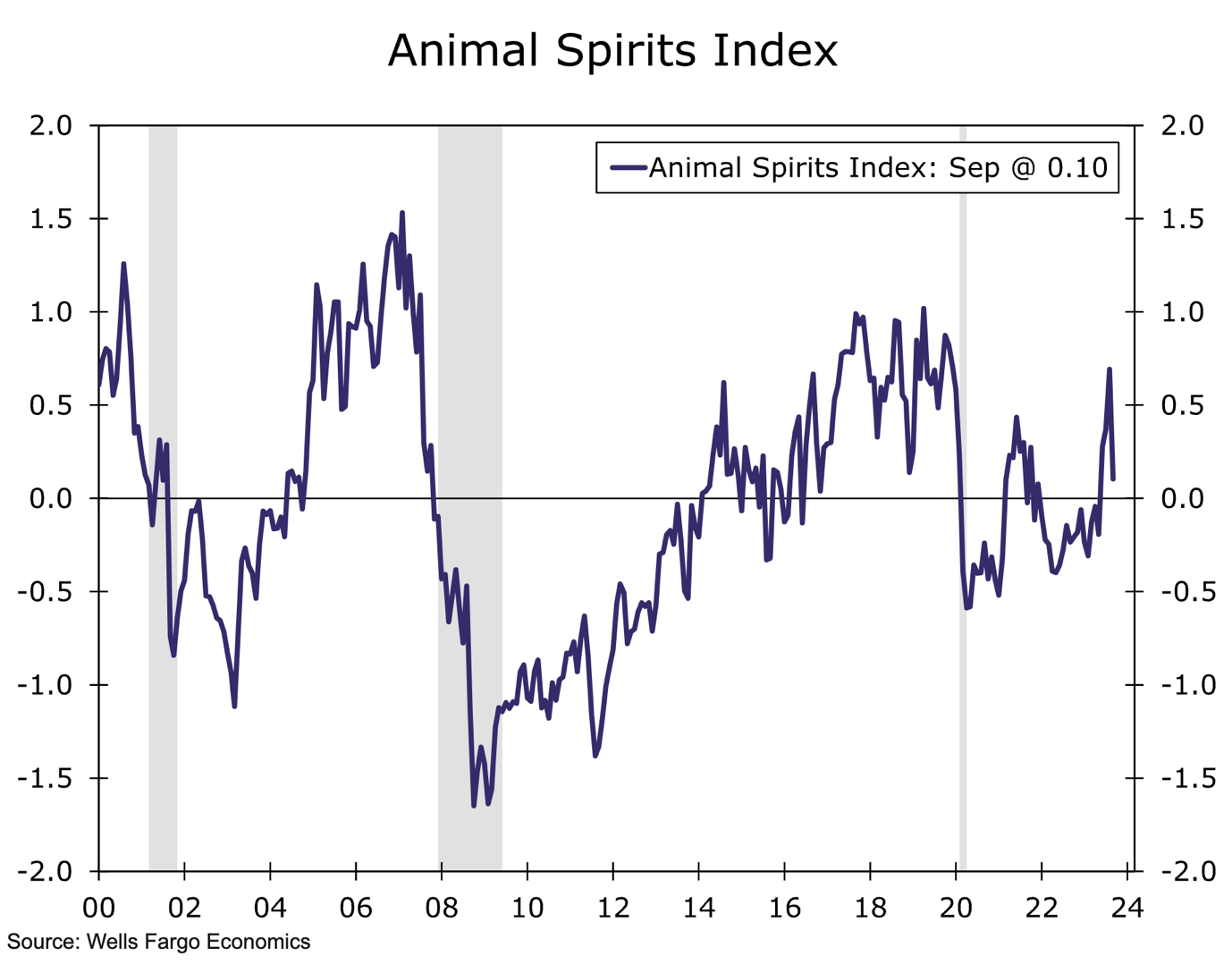

For example, the Animal Spirits Index (“ASI”) experienced a significant decline, dropping from 0.69 in August to 0.1 in September.

A value above zero indicates optimism, while a value below zero suggests pessimism. This September's slip marked the largest change in the ASI since March 2020.

{kind=link}

The ASI is composed of five indicators, including the S&P 500 Index, the Conference Board's Consumer Confidence Index, the yield curve, the VIX Index, and the Economic Policy Uncertainty Index.

According to Wells Fargo, all five components saw a decrease in September, influenced by factors such as financial market downturns and concerns about a potential government shutdown and Fed policy uncertainty.

Consumer confidence also took a hit in September. The Consumer Confidence Index saw a notable 5% decline, emphasizing increasing pessimism among consumers.

After all, inflation is a major driver of consumer confidence.

When looking at the bigger picture, we’re not that far away from a scenario where the market may have to price in stagflation.

Stagflation is very bad for consumer stocks and most REITs. After all, it would mean that limited pricing power will continue to face elevated inflation while economic contraction hurts the health of tenants.

Consumer Staples are fighting for shelf space and competing with generic brands that are often consumers’ first choice when money is tight.

Also, elevated rates make refinancing more expensive.

While the S&P 500 is less than 10% below its all-time high, the Vanguard Real Estate ETF ( VNQ ) is 35% below its high (excluding dividends). Consumer staples ( XLP ) are 18% below their high.

Seeking Alpha

The reason we're bringing up these two struggling sectors is that we just added to two of our favorite investments in these sectors.

Two stocks with high yields, great business models, and the ability to outperform their sectors.

Public Storage ( PSA ) – 4.4% Yield

This pick epitomizes SWAN (stands for sleep well at night)-style investing.

While we certainly don’t enjoy this volatile stock market and the tricky economic environment, we do enjoy the chance to buy great stocks at great valuations.

We like self-storage.

While it's way more cyclical than safer REITs like Realty Income ( O ), it comes with long-term secular growth like its ability to offer micro warehousing solutions to companies, the ever-increasing mountain of stuff we buy but don’t need, and the fact that most self-storage facilities have prime real estate close to city centers and residential areas.

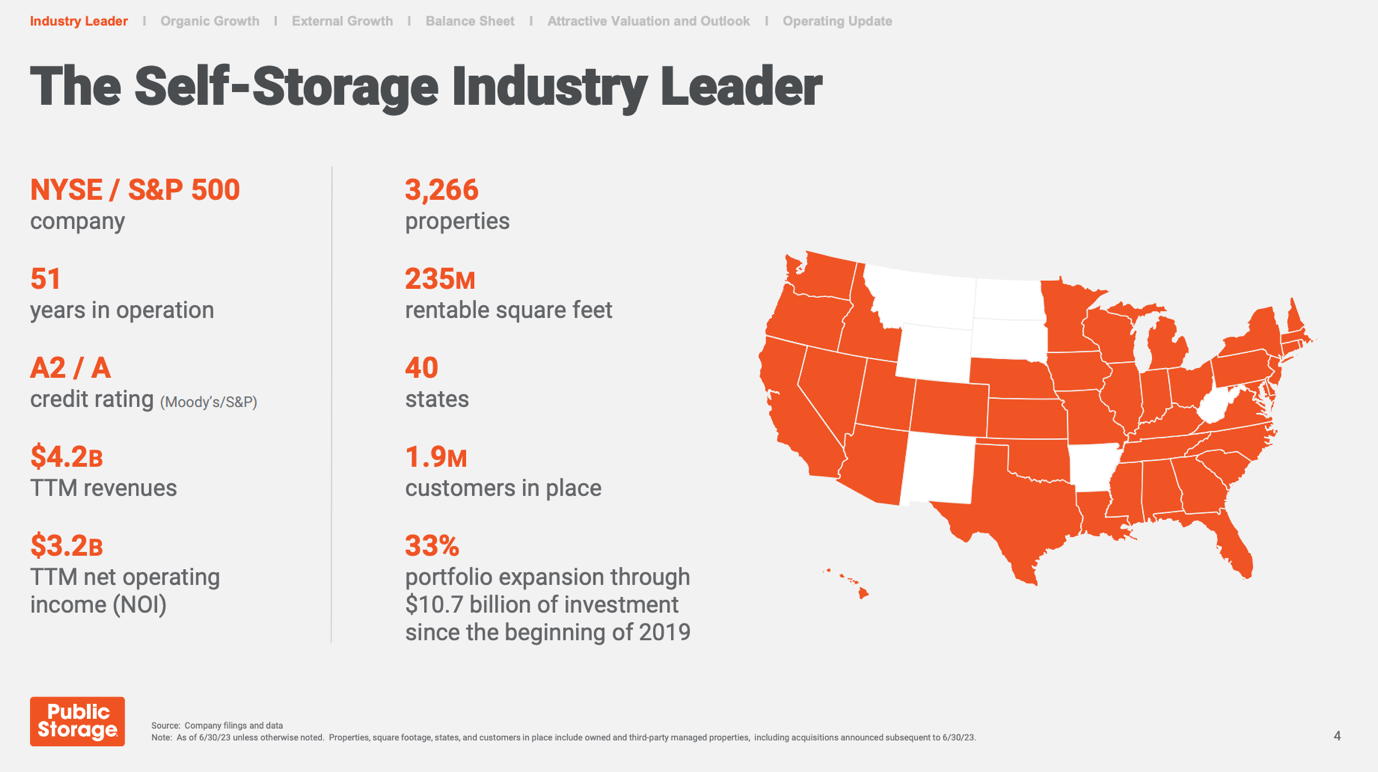

After the merger between Extra Space Storage ( EXR ) (we own it) and Life Storage, Public Storage is now the second-largest self-storage operator in the United States.

After being in business for more than 50 years, the company owns close to 3,300 properties in 40 states, servicing 1.9 million customers.

It’s also one of the few REITs that enjoys an A-rated balance sheet.

{kind=link}

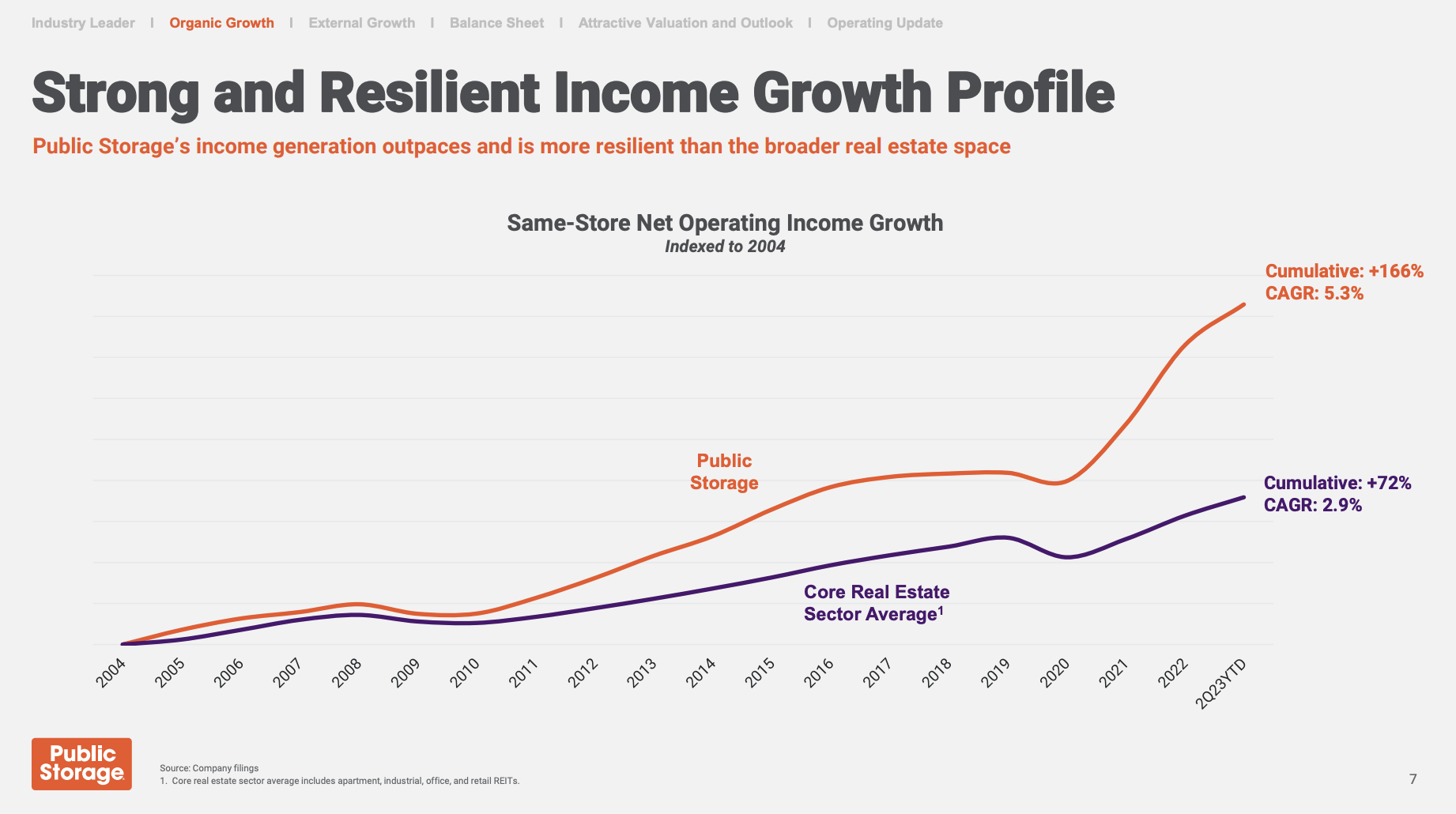

The company, which uses methods like a website and mobile applications, digital rental agreements, remote customer care, and digital property access to smoothen operations and improve customer service, has grown its same-store operating income by 5.3% per year since 2004. This beats the core real estate sector average by 240 basis points per year!

{kind=link}

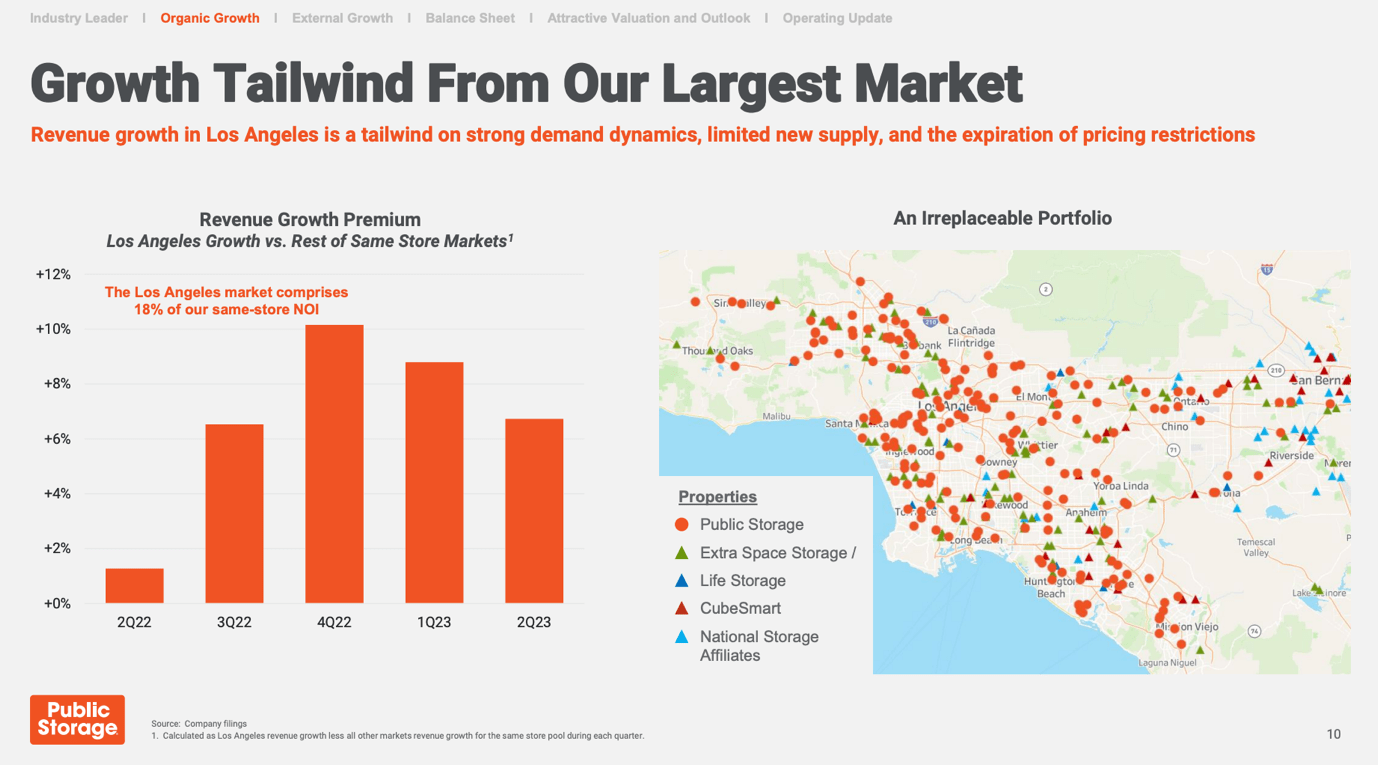

Furthermore, the company owns 440 properties in California, its home market.

That’s 15% of its total store count.

While this market is hated by some, it comes with pricing power.

After all, Californian (mainly SoCal) real estate is supply-constrained. This has geographical and political reasons causing the company to report outperforming revenue growth on a very consistent basis – even in this environment.

{kind=link}

Furthermore, the company did not cut its dividend during the Great Financial Crisis.

It also kept its dividend unchanged for multiple years before it hiked its dividend by 50% in February of this year.

The company decided to focus on growth instead of its dividend. We believe it was a smart move, as it allowed the company to significantly boost its portfolio.

Since the beginning of 2019, the company has expanded its portfolio by 33% without hurting its balance sheet. It still has a 3.9x leverage ratio, which includes $4.4 billion in preferred equity.

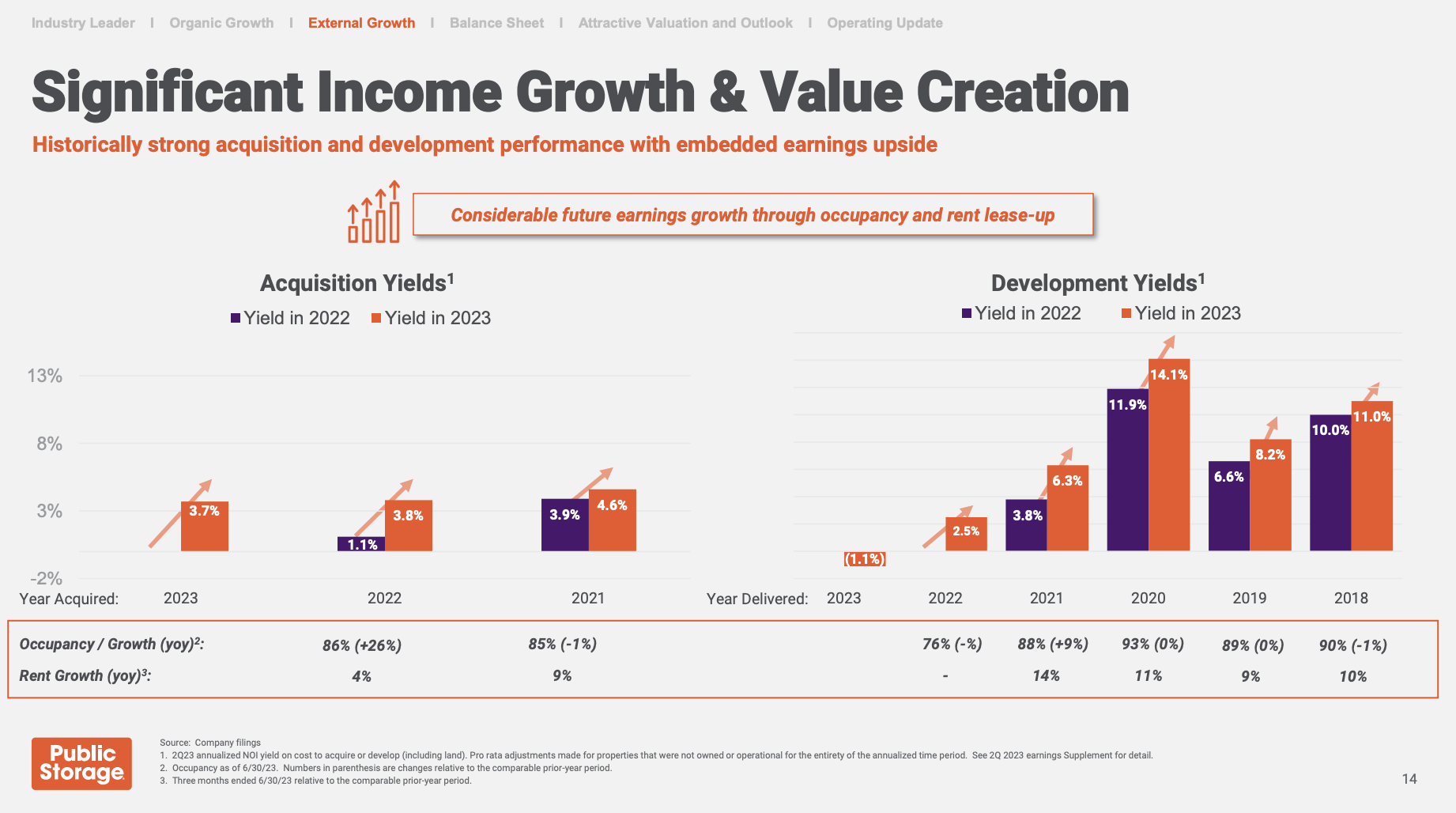

It also enjoys high yields on its newly added properties and developments.

{kind=link}

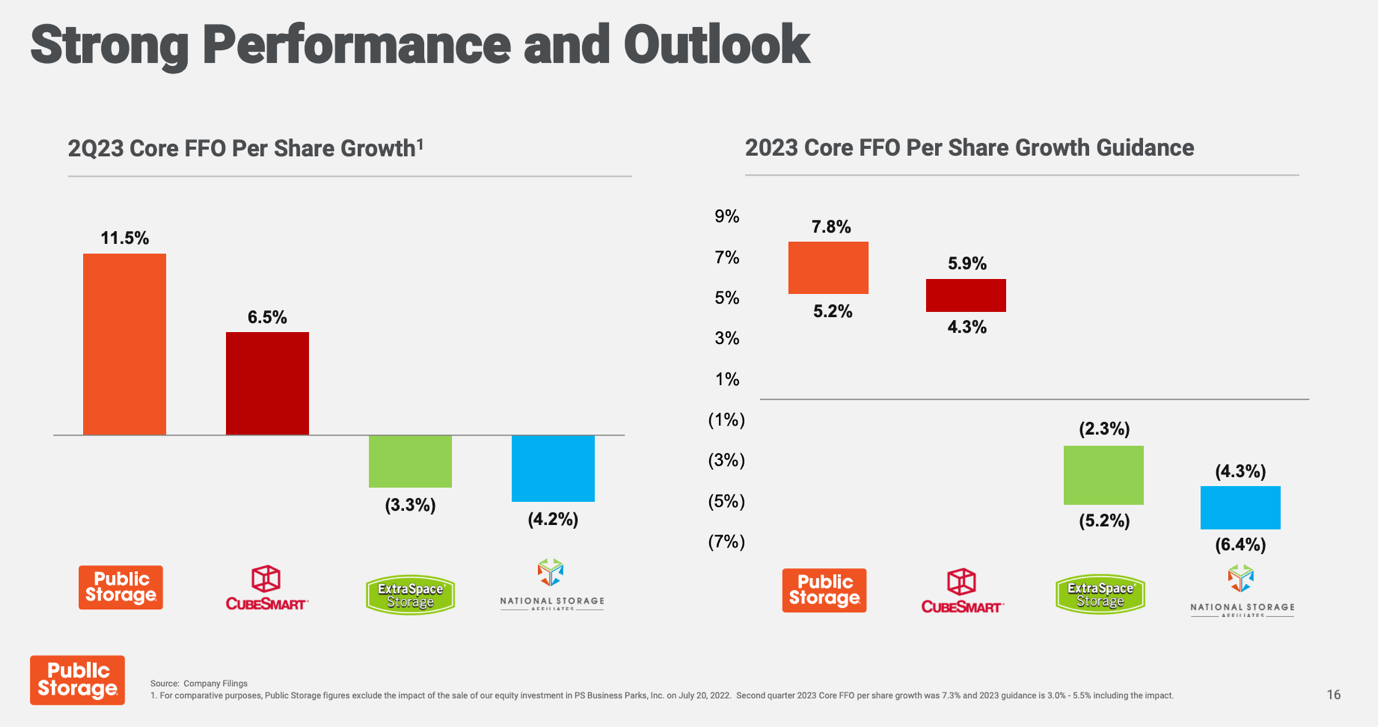

On top of that, the company turned into the strongest performer in 2Q23, beating its major peers when it comes to core FFO per share growth and core FFO per share guidance.

{kind=link}

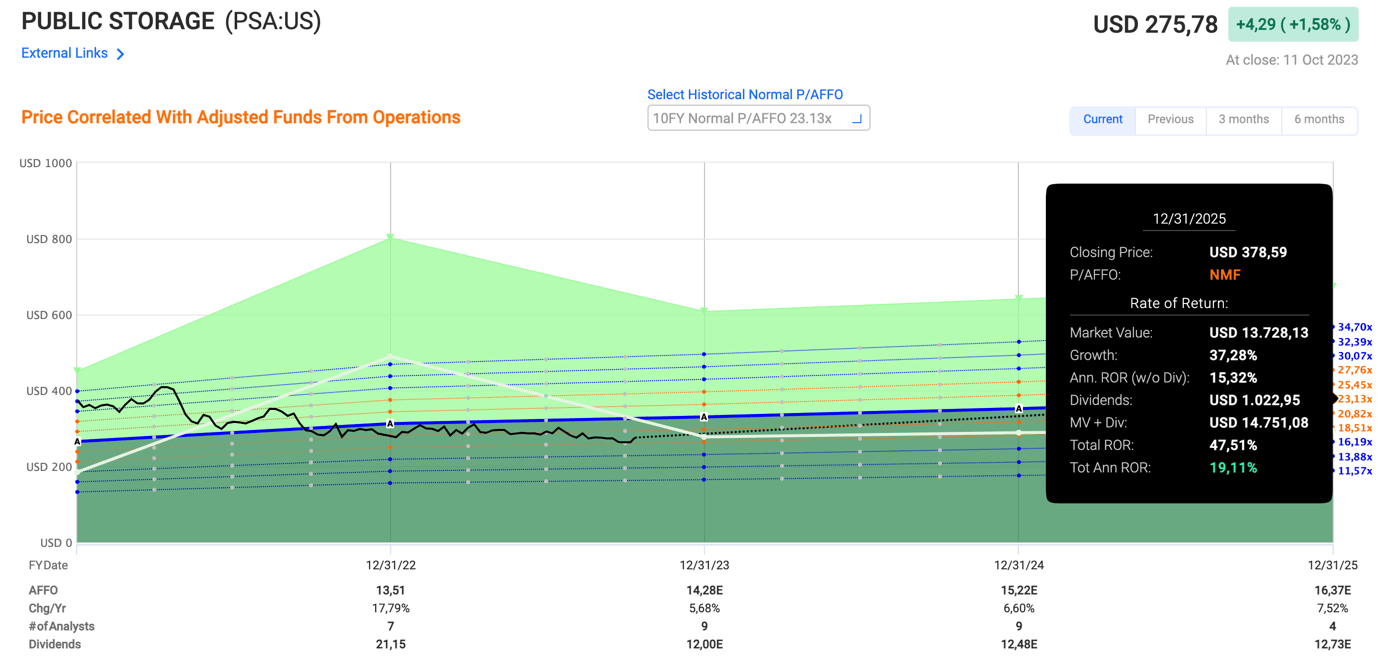

After dropping by 10.4% over the past six months, PSA now has a juicy dividend and an attractive valuation.

The company has a 4.4% dividend yield, protected by a 72% core FFO payout ratio.

Valuation-wise, PSA is trading at 19.6x adjusted FFO. The 10-year normal AFFO valuation multiple is 23.1x.

If we incorporate mid-single-digit annual AFFO growth (as seen in the overview below) and a return to its normal valuation, the stock could return 19% per year.

{kind=link}

While it waits to be seen when the stock will bottom (it is dependent on the Fed), we really like the risk/reward at these levels and have aggressively bought more in recent days.

We also expect PSA to keep outperforming the VNQ ETF on a prolonged basis.

Seeking Alpha

Stock two is similar.

It’s also an industry champion stuck in an unfavorable macroeconomic environment.

PepsiCo ( PEP ) – 3.1% Yield

The king of the snack aisle!

While generic brands are always an issue, PEP has strong pricing power, as its products have limited competition. This includes snacks and drinks.

{kind=link}

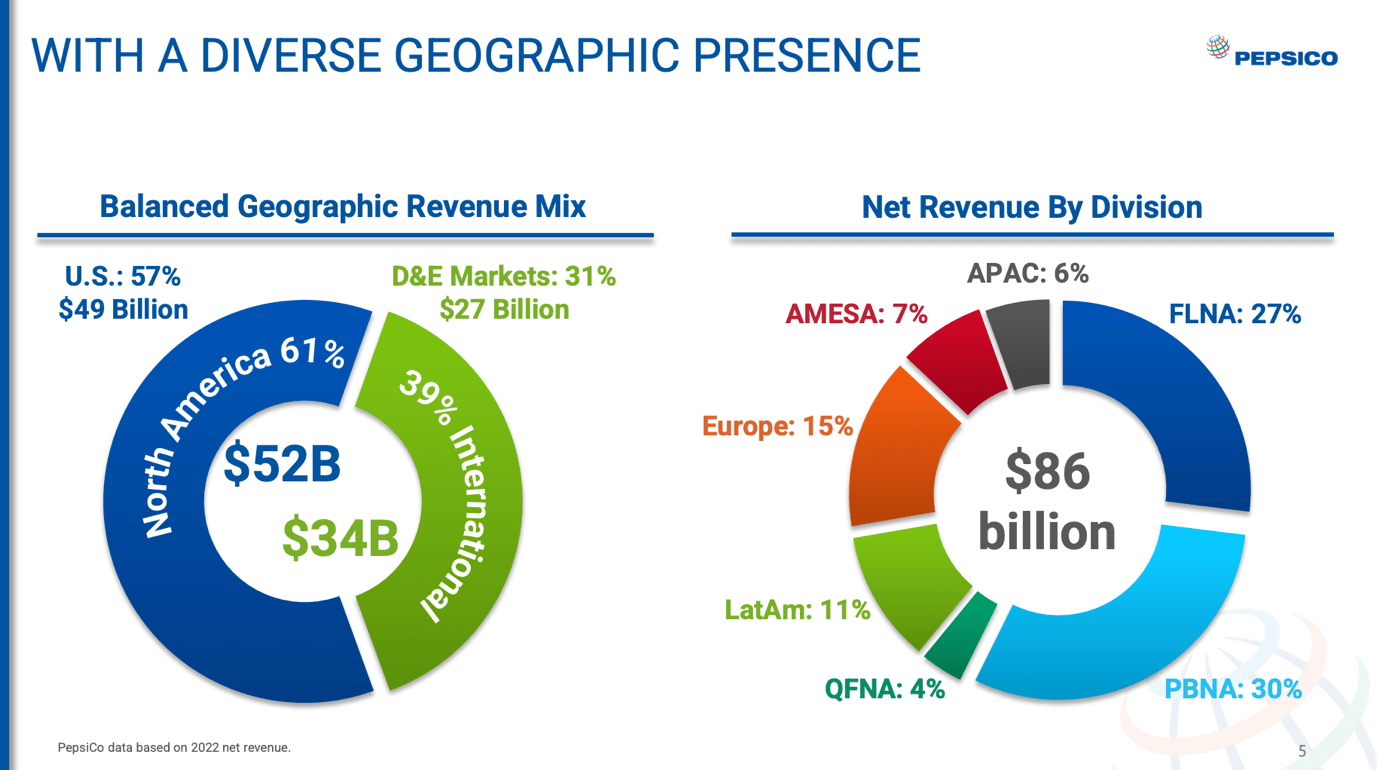

On top of that, the company generates close to 40% of its revenues in international markets.

{kind=link}

Here’s how some of the company’s brands did in the 2020-2022 period. Please note that these are compounding annual revenue growth rates.

- Gatorade: +13%

- Doritos: +11%

- Cheetos: +11%

- Lay’s: +9%

- Mountain Dew: +8%

- Pepsi Cola: +7%

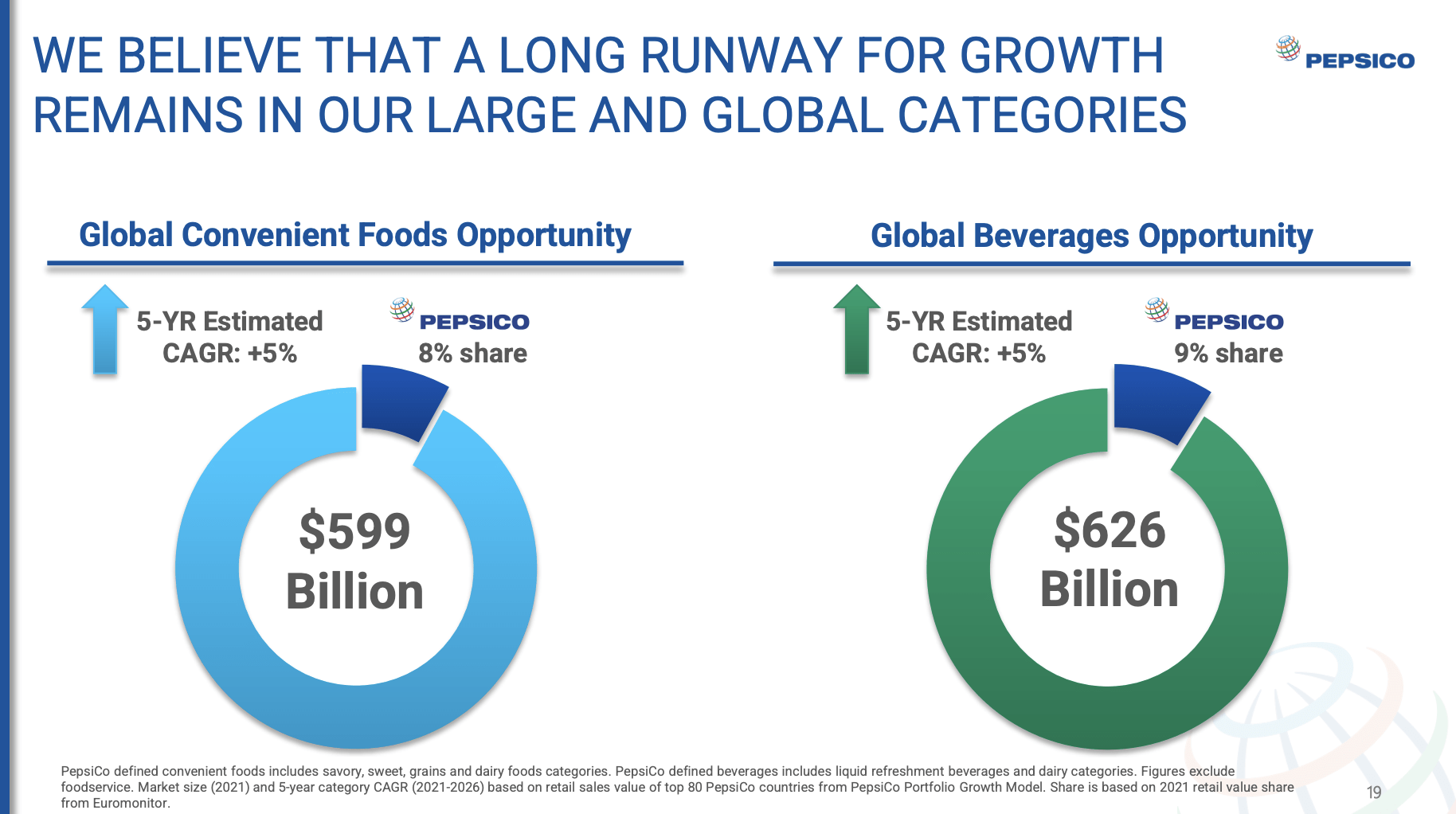

With these brands, the company isn’t just benefitting from population growth but also its small market share in a highly fragmented industry. It owns just 9% of the beverage market and 8% of the global convenience foods industry.

{kind=link}

Even in this environment, the company is firing on all cylinders, showing tremendous pricing power.

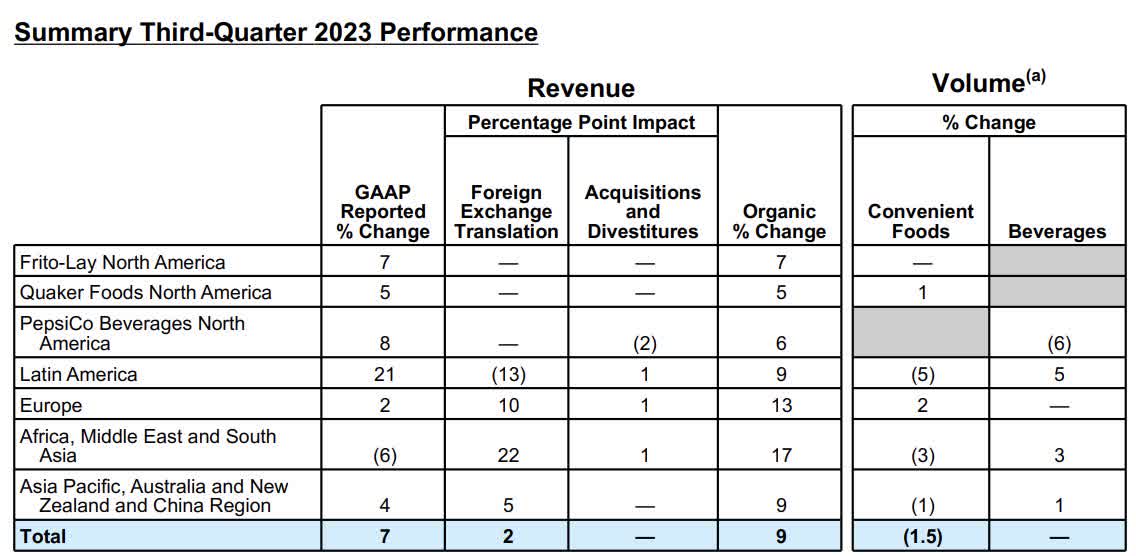

Despite a slight decline in volumes (as consumers are cutting back on spending), the company saw 9% higher revenue, excluding M&A.

{kind=link}

This is a stellar performance that most companies are very jealous of.

Additionally, Pepsi has issued guidance for the full-year fiscal 2024.

According to management, the company expects to achieve results that are on the higher end of the long-term target ranges for both organic revenue and core constant currency earnings per share growth.

The target ranges for organic revenue growth of 4% to 6% and core constant currency EPS growth at a high-single-digit percentage have remained unchanged.

The company currently yields 3.2%. It has a 65% payout and a 5-year dividend CAGR of 6.9%.

PepsiCo is also a member of the exclusive Dividend Kings club, with a track record of 50 consecutive annual dividend hikes!

Seeking Alpha

The company, which enjoys an A+ credit rating, is also trading at a very attractive price.

Thanks to a stellar financial performance, strong expectations, and a 12% year-to-date stock price decline, the company is now trading highly favorably.

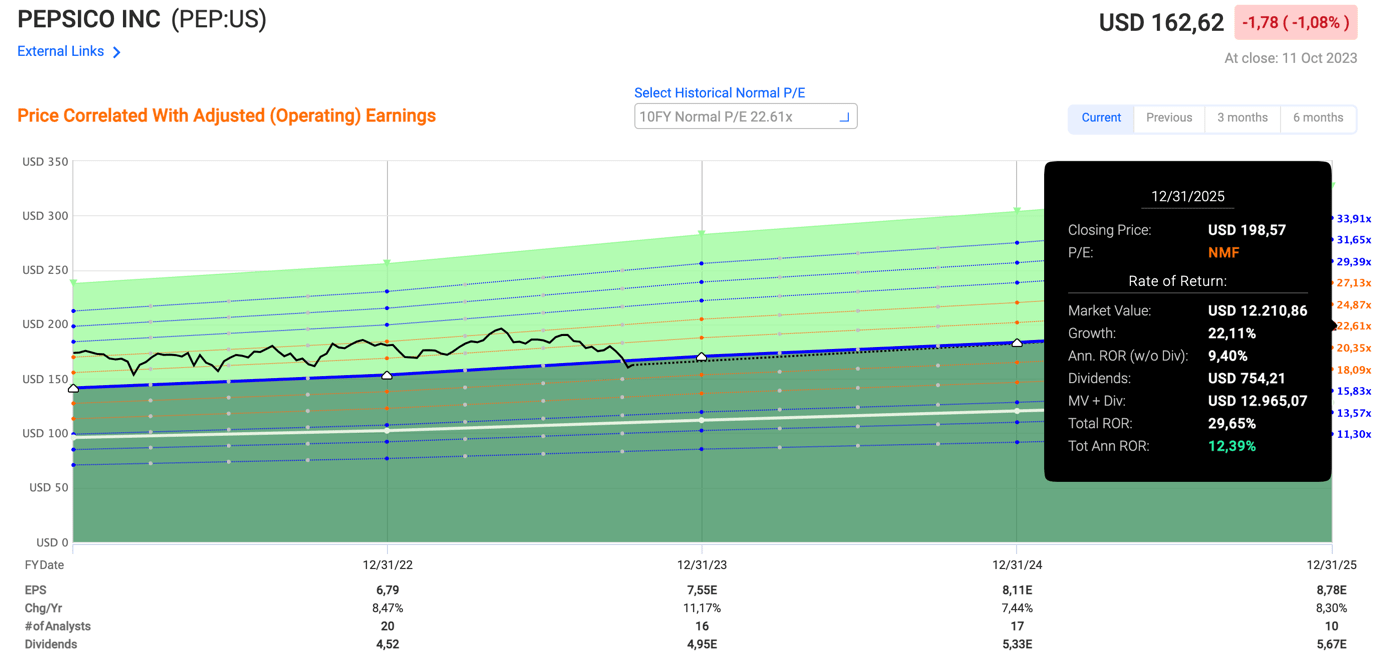

PEP is trading at 22x earnings.

The 10-year normalized P/E ratio is 22.6%.

When adding that the company is expected to maintain strong mid-to-high-double digit annual earnings growth, we get a potential annual return of 12.4% through 2025.

{kind=link}

While it needs to be seen when PEP will bottom, we're buying weakness. This week, we aggressively added to this position, as we have little doubt that PEP will continue to give me outperforming returns and rising income.

Like PSA, PEP has outperformed its peers over the past ten years (and prior to that).

The stock has returned 168% over the past ten years. The XLP ETF has returned just 115%.

Seeking Alpha

Investors looking for defensive, sleep-well-at-night dividend growth should take a closer look at this gem. It has suited us very well, and we have little doubt that it will continue to do so for a very long time.

Takeaway

In the face of challenging economic conditions, including sticky inflation and the looming possibility of a recession, two dividend-yielding stocks stand out for potential investors.

Public Storage, a strong player in the self-storage sector, demonstrates resilience through its business model, growth strategies, and solid balance sheet.

PepsiCo, a titan in the snack and beverage industry, shows strong pricing power and impressive revenue growth, making it an attractive choice even in a competitive market.

Despite the uncertainties in the market, these two stocks with high yields and solid fundamentals present promising opportunities for investors seeking stable returns and reliable income in today's economic climate.

We've been aggressively adding to them and will continue to do so if the market keeps providing opportunities.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Flight To Quality Is A Must