FND - Floor & Decor: Macroeconomic Challenges Are Obstacles

2023-10-16 23:38:17 ET

Summary

- Floor & Decor is a leading specialty retailer in the hard surface flooring market, offering a wide range of products at competitive prices.

- FND is facing challenges due to rising mortgage rates and a decline in existing home sales, impacting its performance.

- In the long term, the Company is strategically positioned to capture a larger market share and remains committed to reinvesting in its stores.

Summary

Floor & Decor Holdings ( FND ) is a leading specialty retailer in the hard surface flooring market, offering a broad range of products including tile, wood, laminate, and natural stone. With a commitment to quality and design, FND has carved a niche for itself by providing homeowners and professional contractors access to a diverse range of flooring products at competitive prices. Their expansive showrooms, knowledgeable staff, and in-house design experts set them apart, ensuring customers receive both a vast selection and personalized guidance. As the home improvement sector continues to evolve, FND remains at the forefront, constantly innovating and expanding its offerings to meet the ever-changing needs of its clientele.

In the ever-evolving economic landscape, FND finds itself at a crossroads. While the company has demonstrated resilience and strategic prowess in capturing market share, it has not been immune to the broader challenges of the industry. Rising mortgage rates, shifts in existing home sales, and other macroeconomic factors have cast a shadow on its performance. When comparing FND's performance metrics against those of its peers, its present valuation appears warranted. However, even when applying a more generous multiple in comparison to its peers, my DCF analysis indicates notable potential downsides. Given all these factors, my recommendation for FND is a sell rating.

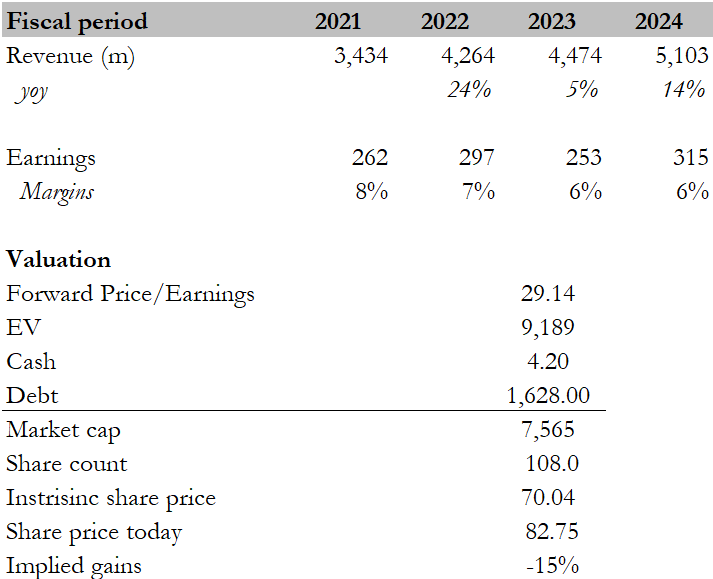

Over the last 5 years, FND has experienced robust growth, with its revenue expanding at a compound annual growth rate of approximately 21%. This impressive surge can be attributed to the ultra-low interest rate climate that emerged in the wake of the COVID-19 pandemic, leading to reduced mortgage rates. However, a consequence of this monetary policy has been rising inflation, which currently hovers at levels deemed concerning. In response, the Federal Reserve has initiated interest rate hikes, creating substantial challenges for the housing sales sector and, by extension, impacting FND's revenue stream. For 2023, projections indicate a sharp deceleration in FND's growth rate, expected to settle in the mid-single digits. The market continues to grapple with uncertainties surrounding the duration and implications of inflation's effects, making it challenging to predict the duration of these headwinds. On a more optimistic note, while inflation remains above the Federal Reserve's 2% target, recent trends suggest it's showing signs of moderation.

Investment thesis

During the second quarter, the company experienced a 6.0% decline in comparable store sales. This was primarily driven by a 7.1% drop in comp transactions. However, this was somewhat offset by a 1.1% rise in the composite average ticket. For the second half of 2023, the company anticipates continued pressure on transaction trends year-over-year. Additionally, the average ticket is expected to face challenges due to the comparison with retail price increases from the previous year and a trend of customers purchasing less square footage.

As a reminder, we are lapping a 10.4% decline in transactions in Q4 of 2022 versus a 6.7% decline in transactions in Q3 of 2022." "The sequential decelerating growth in our average ticket is mainly due to retail increases last year that we are now starting to anniversary in a more meaningful way, as well as customers purchasing less square footage and our strategic decision to selectively lower retail prices on specific SKUs. 2Q23 earnings results call

The company is currently facing economic challenges, including rising mortgage rates and a decline in existing home sales. As of the beginning of September, mortgage rates had surpassed 7% and then peaked at 7.57% in the second week of October. This is the highest rate observed since 2000, as reported by Freddie Mac . Experts in the housing market anticipate that mortgage rates will continue to be high due to prevailing economic uncertainties and the Federal Reserve's efforts to combat inflation by raising interest rates.

According to FRED's chart , existing home sales in the US for August 2023 experienced a slight decline of 0.7% from the previous month. This brought the sales to an annualized rate of 4.04 million units, marking the lowest rate since January. This figure also fell short of market expectations, which were set at 4.1 million units. This decline in August marked the third consecutive month of decreasing sales, a trend influenced by rising mortgage rates and elevated house prices. Specifically, sales of single-family homes decreased by 1.4%, settling at 3.60 million units. As for housing inventory, by the end of August, there were 1.1 million units available, reflecting a 0.9% drop from July. On the pricing front, the median price for all types of existing homes reached $407,100, showing a 3.9% increase compared to August 2022.

Amidst the backdrop of increasing mortgage rates, a decline in existing home sales (which are approaching their lowest levels since January 2023), rising home prices, and a decrease in housing inventory, the company's management has adjusted their FY23 guidance to account for an anticipated softer demand in the second half of 2023. The company now projects FY23 sales to be in the range of $4.46 billion to $4.53 billion, down from the previously estimated $4.61 billion to $4.75 billion. This includes an expected decline in comparable store sales of between negative 7.0% and 5.5%, adjusted from the earlier forecast of negative 3.0% to a flat rate. Additionally, the adjusted EPS is now anticipated to be between $2.30 and $2.50, a decrease from the previous range of $2.55 to $2.85. In essence, at the midpoint, the sales guidance has been reduced by 4%, and the adjusted EPS guidance has been lowered by 11%.

On a more positive note, I'm of the opinion that FND is strategically poised to capture a larger market share amidst the prevailing inflationary conditions. The company's emphasis on value is likely to resonate well with consumers. Moreover, I anticipate that smaller independent players might continue to lose market share to larger, more financially robust entities like FND, especially as they grapple with ongoing challenges and a dip in demand. It's also worth noting that FND remains committed to reinvesting in its stores. This proactive approach positions them favorably for long-term market share gains, especially when some competitors might be holding back on certain projects given the current market dynamics.

Valuation

I believe that the fair value for FND, based on my DCF model, stands at $70.04. The assumptions in my model reflect the economic challenges the company currently faces. These challenges include rising mortgage rates and a decline in existing home sales, which have reached their lowest point since January 2023. Additionally, with increasing home prices and dwindling home supplies, existing home sales are anticipated to pose challenges for the company in the second half of the year. In light of these factors, the management has adjusted its revenue and EPS guidance downward. Consequently, my projections for 2023 and 2024 are 5% and 14%, respectively. These figures align with both the market consensus and the guidance provided by the company's management.

{kind=link}

Peers include Tile Shop Holdings ( TTSH ). The forward P/E multiple for TTSH stands at 21.25x, with an expected growth rate over the next twelve months of 3% and a net margin of 4.06%. In comparison, FND's forward P/E multiple is 29.14x, its expected growth rate for the next twelve months is 14%, and it boasts a net margin of 7.06%. Given FND's superior metrics, its forward P/E multiple is warranted. However, based on FND's current multiple, the price target is projected at $70.04, representing a potential downside of 15%. Considering this, I recommend a sell rating for FND.

Risk

Several potential upside risks warrant attention. First and foremost, there's the possibility that housing turnover could recover at a faster pace than currently predicted. Additionally, should inflationary conditions stabilize, the Federal Reserve might opt to decrease the federal funds rate, which would, in turn, likely result in reduced mortgage rates. Given that existing home sales are currently at a low point, any rebound could be substantial. Such a development could challenge the validity of my sell rating on the stock.

Conclusion

FND has encountered challenges in the current economic environment, including a decline in comparable store sales and broader impacts from rising mortgage rates and a decrease in existing home sales. The highest mortgage rates in recent memory and a consistent decline in existing home sales, as shown in FRED's data, emphasize these difficulties even more. In response, the company has adjusted its guidance, anticipating softer demand in the upcoming months. Despite these headwinds, FND's strategic positioning and emphasis on value present an opportunity for market share growth, especially when compared to smaller competitors. My valuation, based on a DCF model, suggests a fair value for FND that reflects these economic challenges. When compared to peers, FND's metrics appear superior, justifying its forward P/E multiple. However, considering the potential downside from the current price target, I recommend a sell rating for FND.

For further details see:

Floor & Decor: Macroeconomic Challenges Are Obstacles