K - Flowers Foods: A Healthy Dividend With Shares Near A Strong Entry Point

2023-10-24 00:24:35 ET

Summary

- This packaged bakery food company has a significant 17.4% share of the US bread market.

- It is wisely updating its brand portfolio by rotating into organic bread, gluten-free bread and keto products, which tend to sell at a premium and appeal to modern consumers.

- The company has grown by “smart acquisitions,” including Canyon Bakehouse, Dave’s Killer Bread and Papa Pita. Legacy brands like Tastykake are becoming a smaller part of the portfolio.

- Shares are slightly undervalued at their current $20.86, but I believe a drop below $20.00 would make the shares a buy.

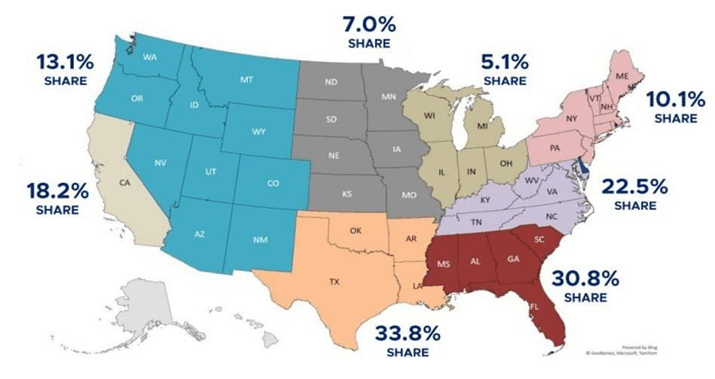

Flowers Foods ( FLO ) is the “second-largest producer of packaged bakery foods in the U.S.” after Bimbo Bakeries USA ( OTCPK:BMBOY ). The company was founded in 1919 and is headquartered in Thomasville, Georgia. Many of Flowers’ brands are well-known to American consumers, including Wonder Bread, Sunbeam Bread, Mrs. Freshley’s, Nature’s Own, Dave’s Killer Bread, Canyon Bakehouse, and Tastykake. Flowers distributes its products through a network of independent partners and its customers include supermarkets, fast food chains, discount chains, restaurants, dollar stores and vending companies. The largest customer is Walmart/Sam’s Club. The company has a 17.4% market share of breads (see chart below) and a 6.3% share of cakes in the US, but a significant 74.7% share of the organic bread market and 34.5% of the gluten free bread market. Flowers’ strategy has increasingly moved toward organic brands in the last decade, as these have higher price points and margins.

Flowers is a consumer staples company and it is part of the S&P Mid Cap 400 , with a total market cap of $4.4 billion. It has a Beta of 0.45 , so it is less volatile than the overall market. Today, shares are trading at $20.86, down significantly from the November 2022 high of $29.98. Consumer staples are currently the second worst performing sector of the S&P 500 with shares down 9.1% year to date. Only utilities, down 9.3%, have fared worse.

{kind=link}

Flowers US Market Share (2023 Investor Presentation)

Recent Performance

Flowers Food’s long term goals are to grow sales by 1.0%-2.0% per year and earnings per share by 7.0%-9.0% per year, as set forth in the 2023 Investor Presentation . Double digit growth is expected from the new brands, while legacy brands like Tastykake are expected to grow in the single digits, through increased prices or improved margins. In its Second Quarter Report , the company reaffirmed the 2023 guidance of earnings per share between $1.18 to $1.25, and annual sales of $5.1-$5.14 billion.

Over the last few years, however, FLO has fallen a little short of its goals. Earnings per share in the First Quarter 2023 were $0.38 per share, down $0.06 from the fourth quarter 2022. However, sales for this quarter were $1.53 billion, up 6.9% over the same period the prior year. The CEO said the company had a “slow start to the year (with) lower-than-expected branded retail sales due to softer category demand.” I take this to mean customers bought less expensive items with lower margins. Earnings per share in the second quarter 2023 were $0.33, up $0.02 per share over the same period in 2022. Sales for the quarter were $1.23 billion, down 19.6% from the first quarter. This was attributed, again, to consumers being more price conscious.

For the year 2022, sales were $4.81 billion, up 11.1% from $4.33 billion in 2021. 2021 sales were 1.1% lower than 2020’s sales of $4.39 million. Net income was $228.39 million in 2022, up 10.8% from $206.18 in 2021. Net income in 2020 was only $152.32 million largely due to a one-time payment of $108.8 million to end a pension plan; otherwise income for that year would have been $261.12 million. Per the 2022 Annual Report , the largest customer for the year was Walmart/Sam’s Club, which is 21.7% of sales, and this percentage has been consistent since 2020. By implication the end customer for Flower’s products is likely price sensitive. The company states that it continues to benefit from work from home policies, which have increased demand for baked goods in general.

Flowers has had a consistent EBITDA margin over the years, between 10-12.0%. This calculation is defined as EBITDA/Total Sales. In 2022 it was 10.4%; in 2021 it was 11.3%; and in 2020 it was 11.9%.

{kind=link}

EBITDA Margin Over Time (2023 Investor Presentation)

New Products and Acquisitions – The Future is Organic

Between 1968 and 2020, Flowers reports that it acquired more than 100 brands. Its frequently quoted strategy is that “growth will occur through smart acquisitions.”

Over the last 10 years the company has made four major acquisitions. In 2015, Flowers Foods bought Dave's Killer Bread , which was founded in 2005. Total consideration was $275 million in an all cash deal. Dave’s specializes in breads made with whole grains and sprouted wheat and at the time of acquisition had an existing customer base in the Pacific Northwest. As a FLO subsidiary, it is currently the largest organic bread company in the US.

Also acquired in 2015 was Alpine Valley Bread Company for $120 million in cash and stock . This Mesa, Arizona company produces certified organic and all natural breads. Alpine currently operates as an independent subsidiary of Flowers. Its products include Super Grain Bread, 21 Grain Bread, and Sprouted Wheat with Flaxseed, and all are certified organic and kosher.

In 2018, FLO acquired gluten-free bakery Canyon Bakehouse LLC for $205 million. This company is based in Johnstown, Colorado.

In February 2023, the company acquired Papa Pita , a private Salt Lake City company, for $270 million paid for with cash from FLO’s existing credit lines. This was reported to have boosted sales by 1.6% in the second quarter of 2023 and increased earnings per share by $0.30. The company makes pita bread, tortillas and bagels and all its products are organically certified. Papa Pita had a direct-to-store distribution system in place that increased its attractiveness.

These acquisitions have augmented Flower’s position in the packaged foods industry. It currently has the number one bread loaf in the US (Nature’s Own), the number one organic loaf (Dave’s Killer Bread) and the number one gluten free brand (Canyon Bakehouse). In 2023, there were two important new products released from the existing brands. These were Dave’s Killer Organic Snack Bars and Nature’s Own Keto loaf, which appeals to households on keto diet plans. The Nature’s Own loaf has one carbohydrate per slice. Three flavors of Dave's Killer Bread Snack Bars were manufactured this year.

Long-Term Debt

FLO currently has a Standard & Poor's credit rating of BBB, or lower investment grade. The company has two major issues of long-term debt outstanding, both used to finance acquisitions. In September of 2016 FLO issued $400 million in senior notes maturing in 2026. These bear an interest rate of 3.5%, but can be redeemed before the due date. This issue was used to pay down short-term debt and fund acquisitions. The company later took advantage of the low interest rate environment in 2020-2021 and issued $500 million in senior notes due March 2031 with a rate of 2.4%. These are redeemable any time before 2031, though I can’t imagine the company would do this. Below is FLO’s Long-Term Debt Ratio over time. The levels appear very reasonable and manageable; generally an acceptable long-term debt to total assets ratio is below 0.50.

Long-Term Debt Ratio (Author Calculated)

{kind=link}

Flowers Long-Term Debt (2022 Annual Report)

FLO’s Dividend History

The current yield is 4.41% . If it were in the S&P 500, Flowers would be another Dividend Aristocrat in the making. If the current trend continues, in 2027 it will have increased its dividend consistently for 25 years. The company has paid a dividend since January 1987. However, it has only raised its dividend consistently since 2003, a streak of 21 years, from $.019 to $0.23 per quarter, a compound annual growth rate of 12.6%. During the last five years, dividend growth has been lower. The most recent increase was in August 2023 from $0.22 to $0.23 per quarter, a change of 4.5%. FLO was added to S&P High Yield Dividend Aristocrats list in January of 2023. This is a group of companies that have raised dividends for each of the last 20 years, but there is not a requirement to be part of the S&P 500.

When analyzing the company’s payout ratio, it is better to look at cash flow per share . This is because earnings per share in several years have been impacted by one-time events. In 2020, there was a $108.8 million charge related to the termination of a retirement plan. There was also another $26.6 million in restructuring impairment charges per the 2020 Annual Report . Together I calculate that these equaled about $0.64 per share. In 2019 net income was impacted by $28.0 million in legal costs and restructuring costs of $23.5 million. The adjusted earnings per share would have been $0.96, not $0.78. Based on cash flow, the payout ratio is consistently between 35.0% and 51.0%, a very manageable range.

{kind=link}

Payout Ratio, Cash Flow vs. EPS (Value Line and Author Calculated)

{kind=link}

Annual Dividend History (2023 Investor Presentation)

Flowers Food’s current 4.41% yield is generally comparable to its competitors. At present General Mills ( GIS ) is paying 3.75%, Kellanova ( K ) is paying 4.79%, and Conagra ( CAG ) is at 5.16%. Outlier J&J Snack Foods ( JJSF ) is paying 1.93%, while Grupo Bimbo ( OTCPK:BMBOY ) is paying 2.59%.

Stock Repurchases

FLO has bought back a considerable number of its shares. During 2022, the company bought 1.32 million shares at an average price of $26.52 per share, for a total of $35.0 million. This is less than 1.0% of the 211.8 million shares outstanding. In 2021, 0.41 million shares were repurchased at an average price of $24.39, another $10 million. Of course these purchases are more than 15.0% above the current price of $20.86 per share. There is still authorizations outstanding for the company to purchase another 24.4 million shares, about 12.0% of the outstanding shares.

Current Share Valuation

I have done a five-year discounted cash flow to estimate the fair value of Flowers Foods. To do this I’ve used the upper end of the recently affirmed EPS guidance for 2003: $1.25 per share. I think the new products and acquisition of Papa Pita this year will move the number to the upper end of the range.

For the discount rate, I looked to the average annual return of the S&P 500 and FLO’s sector, consumer staples. The long-term average for the 500 is about 9.8% , while over the last 10 years it has been higher at 12.4% . The Consumer Staples sector rate of return over the last 10 years was 9.55% and for the Consumer Staples Select Index ( XLP ) it was 7.8%. I have chosen a discount rate of 9.5%. For reversion I have used a rate of 6.5%.

FLO’s goal is to grow EPS from 7.0-9.0% per year, although it hasn’t really been able to achieve this. I’m using a number for annual growth of 6.0%, just below this range, and even this is perhaps optimistic. I estimate that the value of shares today is $22.21, so at the current share price of $20.86, shares are about 6.0% undervalued.

{kind=link}

Discounted Cash Flow Valuation (Author Calculated)

I’ve also used a P/E Ratio calculation to cross check the above number. According to Morningstar , “U.S. stocks in the consumer staples sector have been getting hammered this year as investors fled dividend-paying shares in favor of higher yields and less risk in the U.S. Treasuries.” The current P/E multiple they report for the sector is 17.7x, with a possible retreat to 16.0x. Packaged foods companies currently have a higher overall have a P/E Ratio of 19.78. Using the more conservative multiple of 17.7 x $1.25 EPS, the value of the shares would be $22.13, which just about equals the DCF number. At a multiple of 16.0, the value of the shares would be 16.0 X $1.25 = $20.00.

Risks to Outlook

The first thing that comes to mind is that a large portion Flowers Foods end users are price sensitive. A recession, or further inflation pressure, could cause them to cut back on purchases. Another risk is that EPS does not grow as rapidly as 6.0% per year as estimated in the DCF model. Additionally, baked goods are a competitive market, and somewhat subject to trends of late, and Flowers has had to rely on acquisitions for growth. There are low barriers for another competitor to enter the organic or gluten-free markets.

Conclusion

I believe that shares of FLO are currently about 6.0% undervalued. The yield is attractive at 4.41%, but not as attractive as current money market yields over 5.0%. To get there, the share price would have to drop another 12.0% to $18.40, which last happened in December of 2018. If there is any further downturn in the share price, I believe FLO can be an attractive buy, and I believe a strong entry point would be below $20.00. At this price the yield would be 4.6% or higher, and the P/E ratio would be 16.0 or less, a very defensible position.

Flowers continues to grow by strategic acquisitions, and while there is a lot of variety in earnings per share from year to year, FLO has achieved a 21-year streak of rising dividends, a nice track record if you are an income investor. I expect another increase announcement in mid-2024 with the quarterly amount going to $0.24 per share, based on the pattern of recent years. I have rated this company a “hold,” but think it is on the edge of being a “buy.” I think the key is to buy below $20.00.

For further details see:

Flowers Foods: A Healthy Dividend, With Shares Near A Strong Entry Point