FLO - Flowers Foods: Margins Under Pressure

2023-06-06 05:24:35 ET

Summary

- Flowers Foods has experienced good revenue growth but faces economic headwinds and lower operating margins in recent years.

- The company's high selling, general, and administration expenses may indicate a lack of a competitive moat.

- Despite these concerns, Flowers Foods trades at a forward GAAP PE of 22x, which is higher than some of its competitors, suggesting it may be overvalued.

Flowers Foods ( FLO ) registered good revenue growth during the past few years, driven by pandemic-induced work-from-home and stimulus spending. But, consumers are quickly depleting their savings and are looking to cut their spending on food at home and outside. The company has seen lower price elasticities but has warned of a slower start to 2023. Although the company has great gross margins, spending on selling expenses lowers its operating margins and cash flows. Given its lower operating margins and the potential for further economic headwinds to its sales, the company may deserve a lower valuation.

Price increases drive revenue growth, but declining volumes are a worry

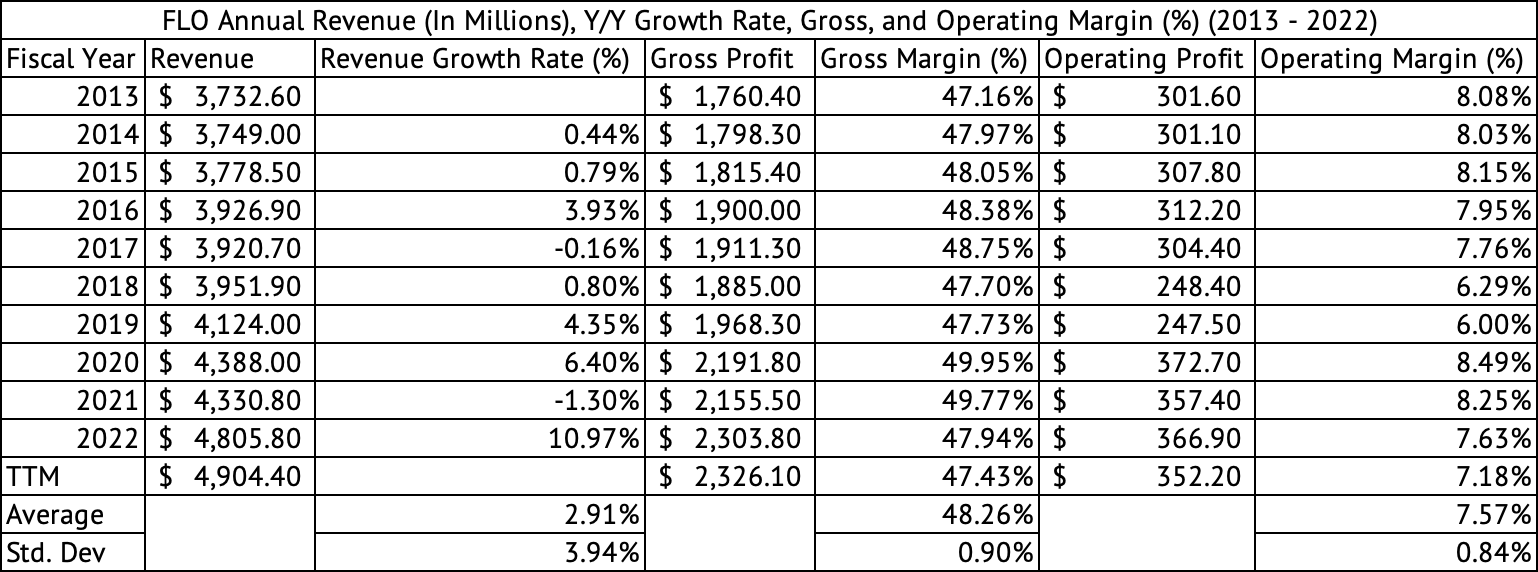

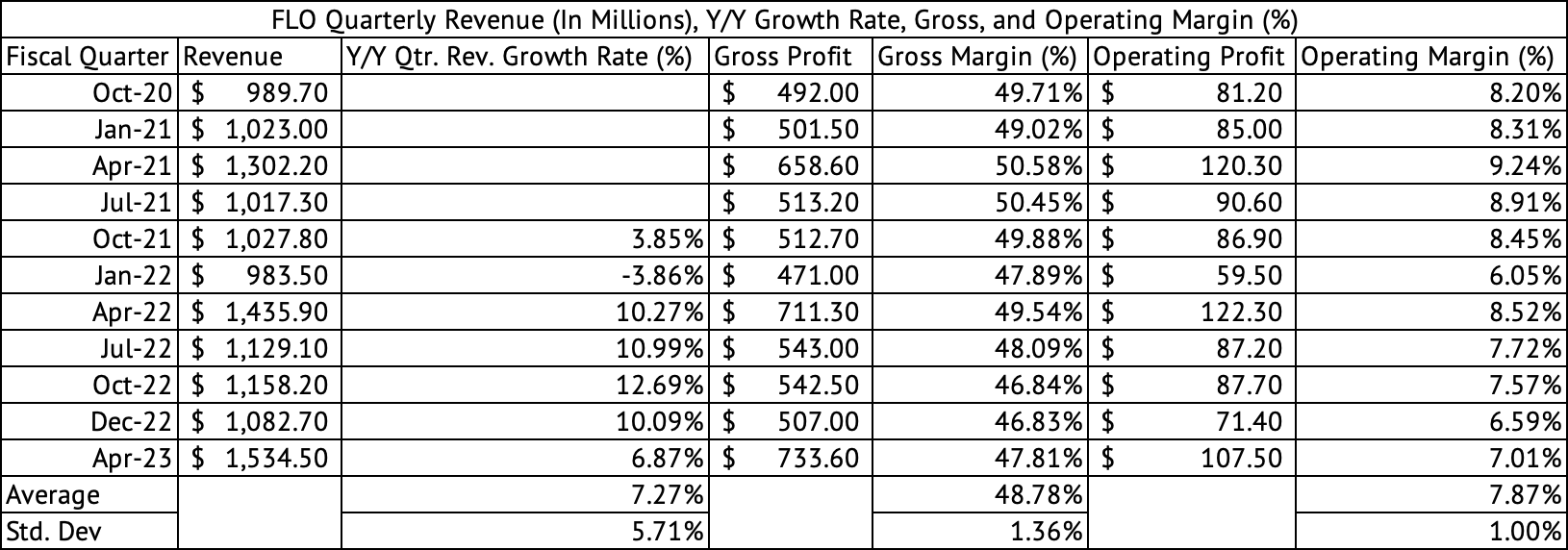

In Q1 2023, the company registered a y/y revenue growth of 6.9% . The company increased prices by 13.6%, but sales volumes dropped by 7.3%. In Q4 2022, the company increased sales by 11% by increasing prices by 16.7%, but volume declined by 6.6%. Although volumes continue to decline, the company's price elasticity is low. But the company's stellar gross margins dropped to 47.9% in 2022 compared to its annual average of 48.2% (Exhibit 1) ; it still has some of the best gross margins in the consumer staples sector (Exhibit 3) . The quarterly gross margins have been lower than its quarterly average of 48.78% since the July 2022 quarter (Exhibit 2) .

Exhibit 1:

Flowers Foods Annual Revenue, Gross, Operating Profits, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

Exhibit 2:

Flowers Foods Quarterly Revenue, Gross, Operating Profits, and Margins (%) (Seeking Alpha, Author Compilation)

{kind=link}

Exhibit 3:

Consumer Staples Quarterly Gross Margin (Seeking Alpha, Author Compilation)

Flowers Foods enjoys gross margins on par with the Procter & Gamble Company ( PG ), but that margin strength does not translate into higher operating margins (Exhibit 1) . Flowers Foods has one of the lowest operating margins across consumer staples companies (Exhibit 4) . In fact, it is the only company on the list to register an operating margin below 10%. Every other company registered a double-digit operating margin.

Exhibit 4:

Consumer Staples Quarterly Operating Margin (Seeking Alpha, Author Compilation)

Flowers Foods had an average annual operating margin of 7.5% over the past decade and an average quarterly operating margin of 7.8% since October 2020. J.M. Smucker ( SJM ) has an operating margin of over 13%, and Conagra ( CAG ) over 16%. The company's Selling, General & Administration expense [SG&A] is high, leading to a lower operating margin. For example, in the April 2023 quarter, the company spent 38.9% of its sales on SG&A expenses. J.M. Smucker spent 17.2%, and Conagra spent 11% of its revenue on SG&A. Flowers Foods may heavily depend on advertising and marketing to bolster its sales, much more so than other consumer staples brands. This high SG&A expense does not bode well for the company and may prove that it does not have a competitive moat.

Conagra Brands trades at a forward GAAP PE of 18x, and J.M. Smucker trades at a forward GAAP PE of 21x. With lower operating and cash flow margins, Flowers Foods trades at a PE on par with J.M. Smucker and higher than Conagra's.

The cash flows and dividends come under pressure due to margin pressure

Seeking Alpha gives a grade of "D+" for dividend safety for Flowers Foods (Exhibit 5) . I agree that the company deserves a low grade for its dividend safety. The company's operating cash flow has to improve quickly to cover its dividend payments easily. The company is also running low on its cash and short-term investment. The company generated very little cash flow after paying dividends and CapEx in 2021 and 2022. Over the past twelve months, the company used $46.7 million in its operations after paying dividends and CapEx. The company's cash and short-term investments have dropped from $165 million in its December quarter to $27 million in March. Inflationary pressure is the primary cause behind the reduced margins and cash flows.

Exhibit 5:

Flowers Foods Dividend Grades (Seeking Alpha)

Fortunately, for Flowers Foods, overall inflation is fading, and although the y/y food inflation is much higher than the overall rate, it should fall in the coming months. As measured by the CPI , the overall inflation index rose by 4.9% y/y in April, while inflation rose by 7.7% y/y in the food category. Most food companies have passed along price increases to the consumer, which is reflected in the CPI. But, some companies have done better than others in recovering their costs.

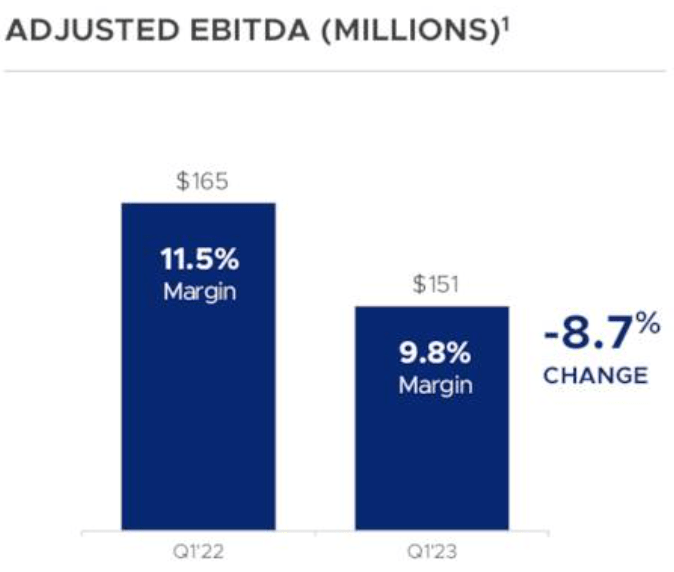

Clearly, Flowers Foods has not entirely passed along its cost increases-the company's adjusted EBITDA margin dropped from 11.5% to 9.8% y/y in the March 2023 quarter (Exhibit 6) . The company would count on food inflation to fade quickly and demand to stay strong to recover its margins. But, the company is highly confident that it can continue paying its dividend. It recently increased its dividend by 4.5%, with the stock now yielding an attractive 3.5%.

Exhibit 6:

Flowers Foods Adjusted EBITDA Margin (Flowers Foods Investor Presentation)

{kind=link}

Flowers Foods' stock has lost its momentum

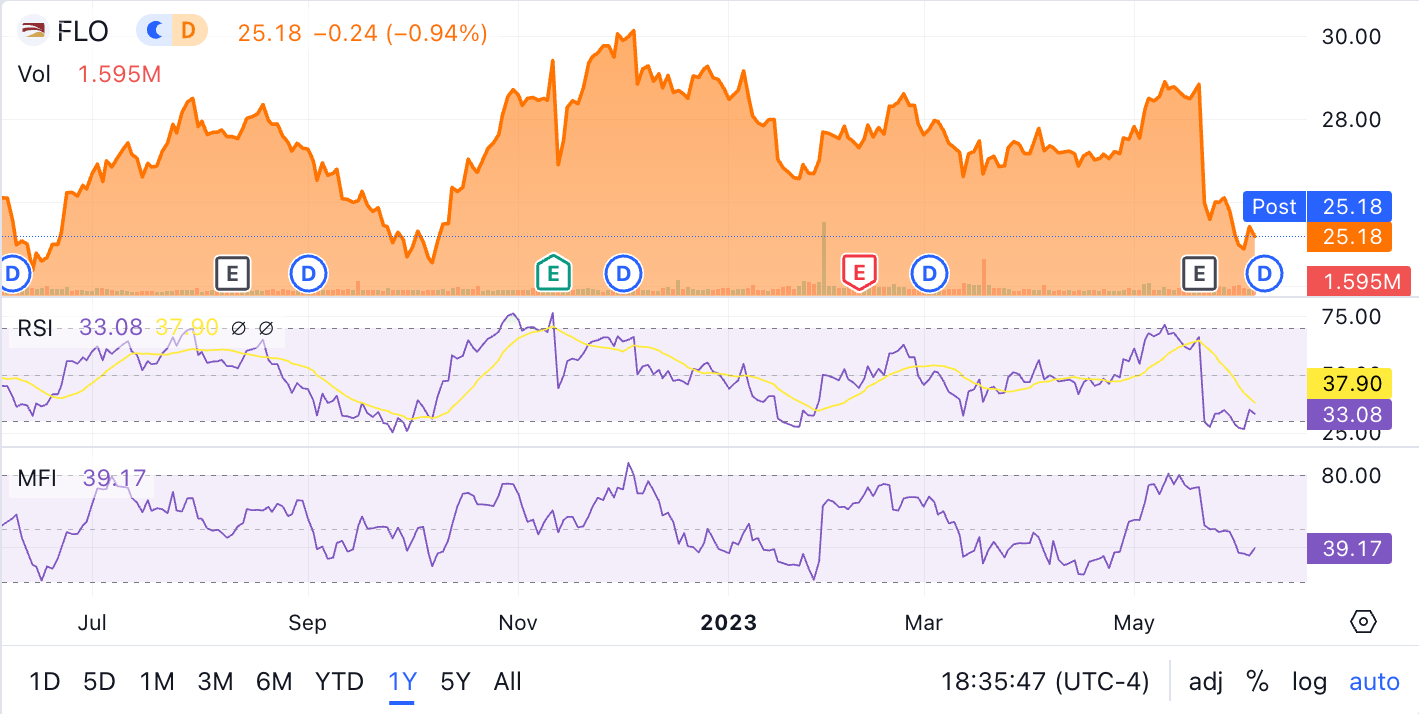

The company has underperformed its sector and the S&P 500 Index over the past three and six months. The stock has dropped 8.4% and 15.2% over the past three and six months, compared to 1.4% and 3.2% for the consumer staples sector. Meanwhile, the Vanguard S&P 500 Index ETF ( VOO ) has gained 6% over the past six months. The stock was hit after it reported a slow start to the year and lower-than-expected branded retail sales in its Q1 2023 earnings call. After the sell-off in May, the stock's RSI and MFI technical indicators are near oversold levels (Exhibit 7) .

Exhibit 7

Flowers Foods RSI and MFI Technical Indicators (Seeking Alpha)

{kind=link}

Flowers Foods is overvalued

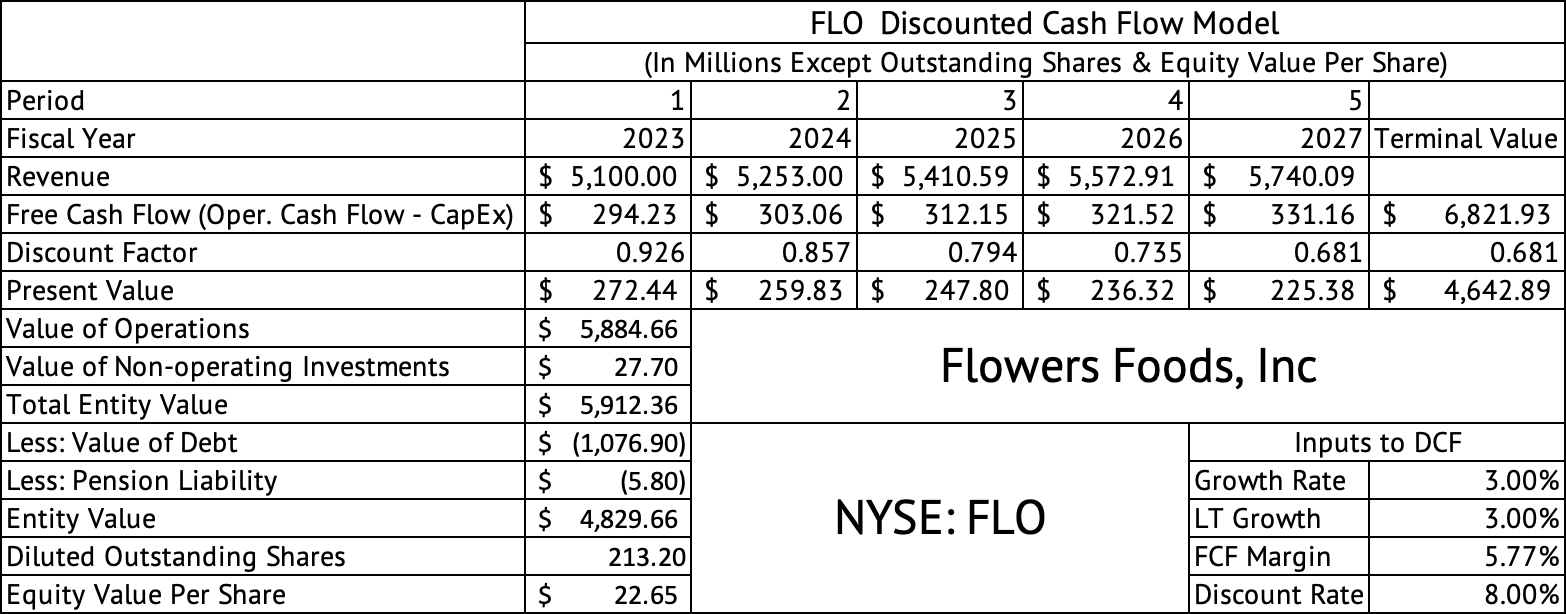

The stock trades at a forward GAAP PE of 22x compared to the sector median of 20x. The Vanguard Consumer Staples ETF ( VDC ) stocks trade at a weighted average PE of 25x , more expensive than Flowers Foods. A discounted cash flow model estimates the per-share equity value at $22, about 10% below its current price of $25.18 (Exhibit 8) . This model assumes a modest revenue growth rate of 3%, a free cash flow margin of 5.7%, the company's long-term average, and a discount rate of 8%. The model estimates the value using before-tax cash flows; the after-tax value will be lower than $22.

Exhibit 8:

Flowers Foods Discounted Cash Flow Model (Seeking Alpha, Author Calculations)

{kind=link}

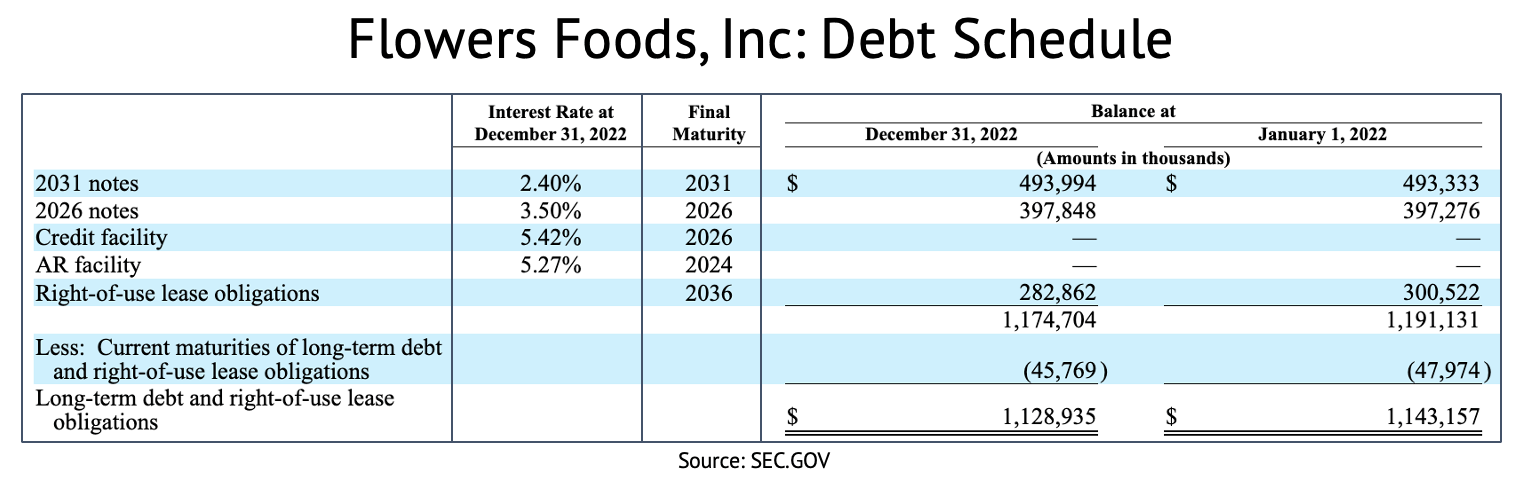

The company has a manageable debt load with a debt-to-EBITDA ratio 1.9x (Source: Seeking Alph/YCharts) . So, an 8% discount rate may be appropriate for the company in the current rate environment. In reality, most companies across various sectors took on debt when the Federal Funds rate was zero percent, so companies are not paying close to 8% on their debt. But, in the future, if interest rates stay high, the cost of their debt will increase. For example, Flowers Foods carried two fixed rate notes, one expiring in 2031 with an interest of 2.4% and another expiring in 2026 with an interest rate of 3.5% (Exhibit 9) .

Exhibit 9:

{kind=link}

Flowers Foods has benefitted from lower price elasticities over the past year. But, the company may have run out of runway to increase prices further, and a slowing economy may pressure consumers to switch to cheaper brands. The company has to spend a lot on marketing its products, which points to its lack of a strong competitive moat. This stock could go lower if its sales weaken in 2023.

For further details see:

Flowers Foods: Margins Under Pressure