FLO - Flowers Foods: Stable Prospects Stretched Valuation

2023-12-26 16:02:32 ET

Summary

- 9M 2023 revenues up single digits but operating profits and margins impacted by California settlement.

- Long-term organic growth projected in the low single digits. Margins should recover assuming no further major lawsuit settlements.

- Competitive risks from larger rival Grupo Bimbo may impact performance.

America's second biggest packaged bakery products company Flowers Foods' ( FLO ) prospects are stable with organic growth expected in the low single digits long term. Valuation appears stretched based on a DCF analysis as well as on a relative basis.

Company Overview

Flowers Foods is America’s second-largest packaged bakery foods producer. The company’s products include breads, buns, rolls, packaged cakes, and tortillas sold to retail, private label, and foodservice customers under a portfolio of brands including Nature’s Own, Dave’s Killer Bread (“DKB”), Wonder, Canyon Bakehouse, Tastykake, and Mrs. Freshley’s. Nature’s Own is the best-selling loaf bread in the U.S., DKB is the #1 selling organic brand in the U.S., and Canyon Bakehouse is the #1 selling gluten-free bread brand in the U.S. according to their information published in Flowers Foods’ FY2022 10-K (Source: Circana (Total US MultiOutlet+C-Store 12 Weeks Ended 10/8/23).

9M 2023 performance

9M 2023 revenues were up 6.4% YoY to $3.96 billion largely driven by pricing which more than offset volume declines due to consumers continuing to trade down to cheaper private-label brands as well as the company’s exit from lower-margin categories.

| Price/Mix |

| Acquisition |

| Volume |

| 13.6% |

| 0.6% |

| (7.3%) |

| 13.3% |

| 1.6% |

| (6.1%) |

| 6.3% |

| 1.3% |

| (4.1%) |

9M 2023 gross margins held steady at 48%, flat from the same period last year as price hikes helped offset cost inflation pressures. Operating margins however dropped to 3% in 9M 2023 from 6% partly due to an increase in selling, distribution, and administrative expenses which increased to 42% of revenues from 38.7% the same period last year largely due to litigation expenses stemming from a $135 million settlement concerning a distributor-related lawsuit in California.

Flowers Foods 10-Q, Q3 2023

9M 2023 free cash flows amounted to $160 million, down 1.7% YoY from $163 million the same period last year.

Looking ahead, volume pressures from consumers trading down to private label are likely to recede medium term. Longer term, America’s bakery market is a mature and saturated one, leaving relatively few growth opportunities particularly in mainstream bakery categories in which players like Flowers Foods compete in. Management is aiming for a 1%-2% organic growth long term.

Flowers Foods is also leaning on acquisitions to support growth however near term M&A is likely to focus on smaller targets as their acquisition of Papa Pita early this year (which was funded with a combination of cash and credit facilities) has left them with a relatively high debt to equity of nearly 0.8 at the end of September.

Y Charts

Margins and profitability should benefit after 2023 assuming the company has no further litigation settlements. Margins may however be impacted slightly by the shift to a company-owned distributor model (required as part of the lawsuit settlement in California) which according to management is generally more costly however this may be offset by cost savings from the company’s ERP upgrade, digital initiatives, and exit from lower margin SKUs.

Management anticipates capital expenditures of $135.0 million to $145.0 million for FY 2023 (inclusive of expenditures for the ERP upgrade of $25.0 million to $35.0 million). CAPEX needs are likely to moderate after 2023 with no major investment projects for the foreseeable future.

Risks

America’s mainstream packaged bakery category is competitive with just a handful of players dominating the market; Grupo Bimbo ( GRBMF ), Flowers Foods, Campbell Soup ( CPB ) and retailer-owned private label brands collectively command a market share of over 50%. Flowers Foods with 46 bakeries across 19 states in the U.S. reaching 85% of the U.S. population is a formidable player however larger rival Grupo Bimbo, with a market share that is nearly double that of Flowers Foods (31% market share for Grupo Bimbo versus 17% for Flowers Foods), and stronger financials (Grupo’s revenues are roughly four times higher than Flowers Foods) may have scale and financial advantages over Flowers Foods particularly in terms of acquisitions which is a key growth tactic in the saturated U.S. market. Pepperidge Farms with a 6% market share could be an enticing acquisition target for the top two players, of which Grupo appears to be a stronger potential acquirer than Flowers Foods. Competitive pressures may hinder Flowers Foods’ growth and margins longer term.

Conclusion

Flowers Foods has a hold analyst consensus rating.

Seeking Alpha

Taking the following assumptions suggests Flowers Foods is worth less than $3.5 billion based on projected organic growth rates, considerably lower than their current market capitalization of $4.7 billion.

| Revenue FY2023 |

| $5.3 billion including Papa Pita acquisition (based on their current run rate over three quarters) |

| Revenue growth YoY % |

| 2% (based on management's 1%-2% organic growth target) |

| Net margin % |

| 3% in FY2023 recovering to 3.5% assuming no further litigation settlements as well as cost savings from ERP upgrade, exit from unprofitable SKUs, receding inflationary pressures, and easing volume pressures from consumer trade-downs, offset by costs due to their shift from an independent distributor to a company-owned model. |

| Depn |

| 2.5% of revenues |

| CAPEX |

| $140 million (or around 2.7% of revenues) in FY2023 based on management projections, moderating to 2.5% of revenues thereafter |

| Discount rate % |

| 7% |

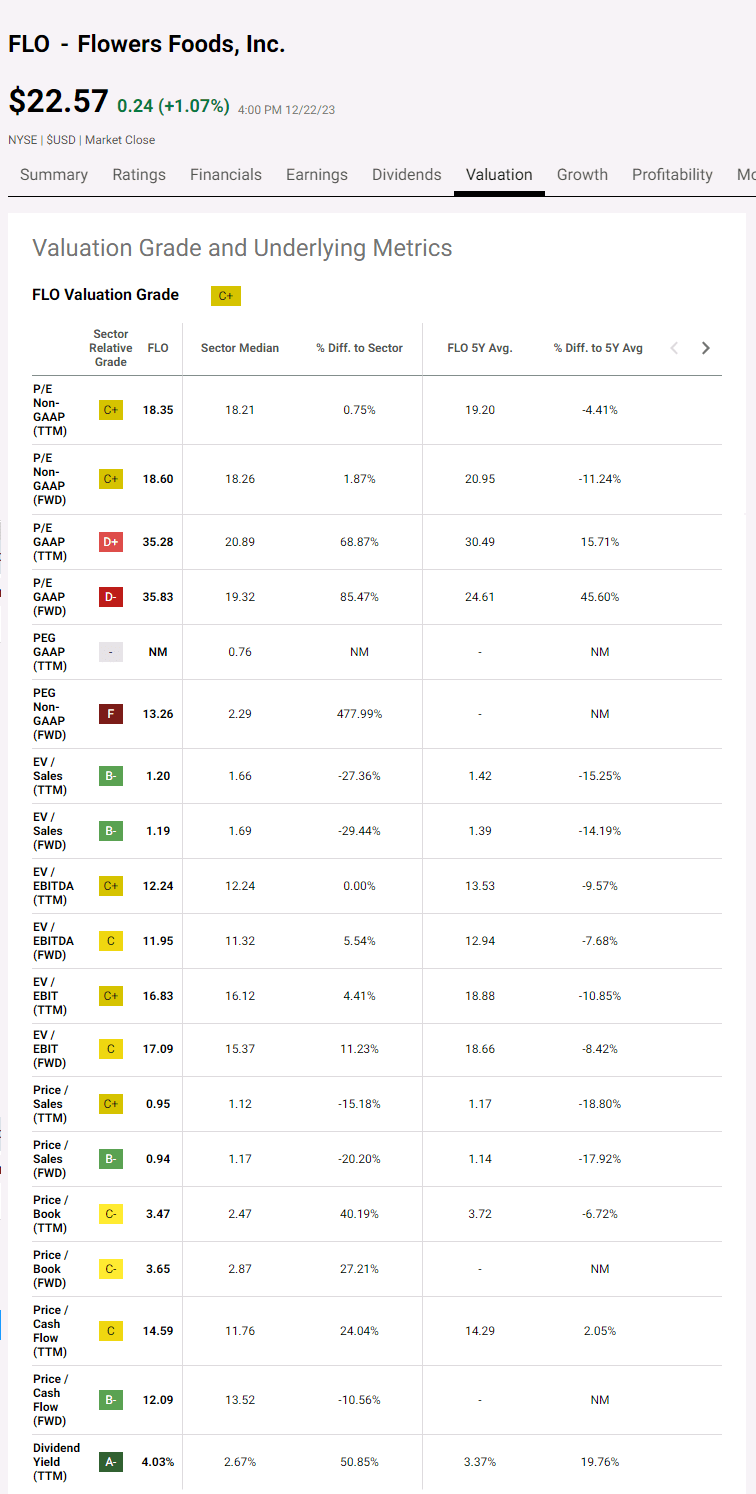

Flowers Foods appears pricey on a relative valuation basis as well with the company’s GAAP forward P/E of 35 being considerably higher than the sector median, and higher than their five-year average. Furthermore, it appears quite rich for a company with a projected low single digit organic long term growth rate. The company however is a strong player in defensive market with relatively high barriers to entry. Some may view the stock as a hold while others with better opportunities to invest elsewhere may view it as a sell.

{kind=link}

For further details see:

Flowers Foods: Stable Prospects, Stretched Valuation