FLO - Flowers Foods: The Valuation Remains Unattractive Despite The Sell-Off

2023-08-30 21:42:11 ET

Summary

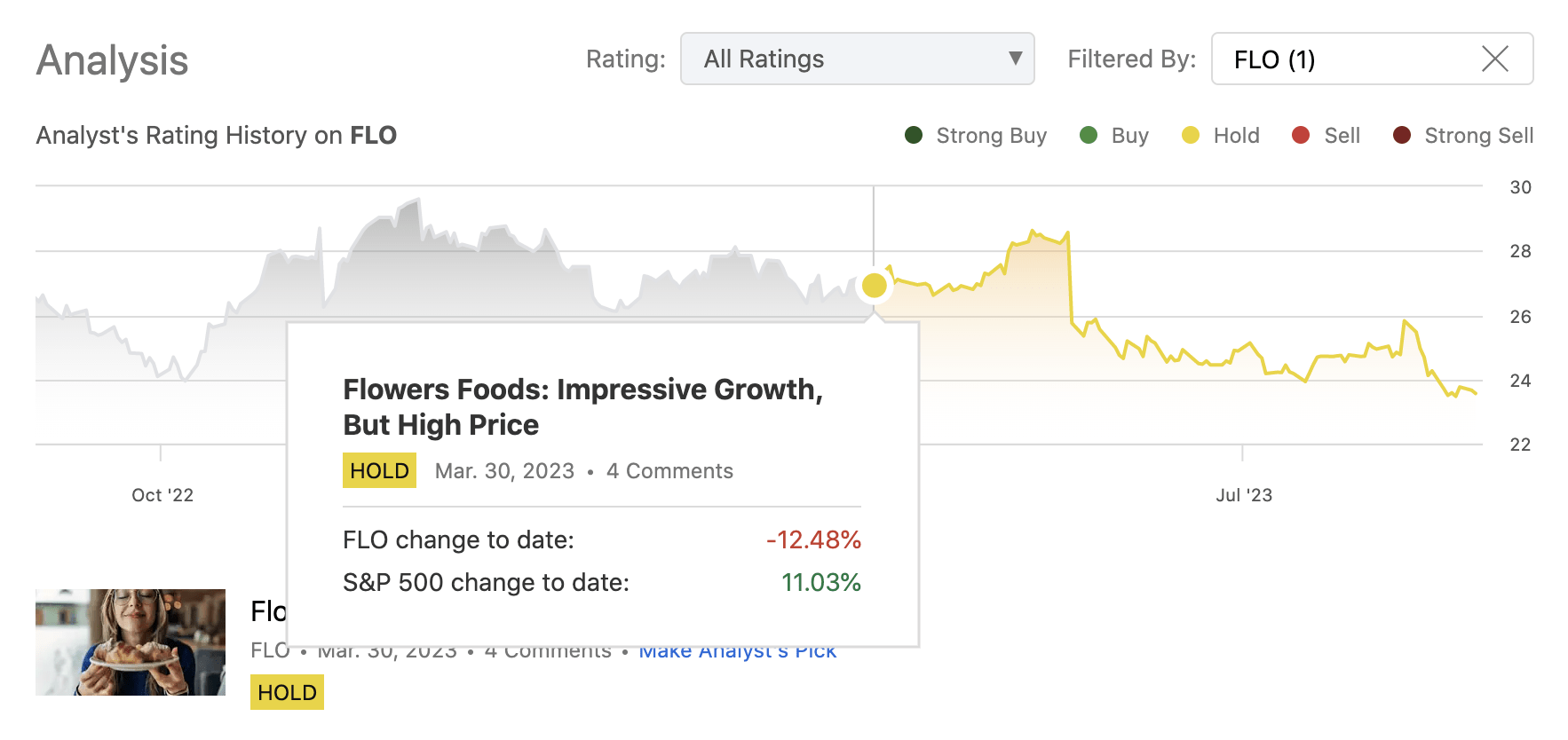

- Flowers Foods has experienced a decline in stock price by 12%, while the broader market has gained 11% since our last writing in March 2023.

- The decline in stock price can be attributed to lower-than-expected Q1 results along with lowered guidance. Despite the strong Q2 results, the price has kept on declining after the announcement.

- Dividend sustainability and safety are questionable as FLO's free cash flow has not been enough to cover dividends and share repurchases in the past quarter.

Flowers Foods, Inc. ( FLO ) produces and markets packaged bakery food products in the United States. Its principal products include fresh breads, buns, rolls, snack cakes, and tortillas, as well as frozen breads and rolls under the Nature's Own, Dave's Killer Bread, Wonder, Canyon Bakehouse, Mrs. Freshley's, and Tastykake brand names.

We have started coverage on the firm in March 2023 with a neutral outlook. The primary reasons for our neutral view have been, on one side, the impressive growth in the prior year and its relative independence from the consumer confidence readings, while, on the other side, the relative overvaluation as indicated by our dividend discount models.

Since our first writing the stock price of FLO has actually declined by as much as 12%, while the broader market has gained more than 11% in the same time period.

{kind=link}

The aim of our article today is to see what has changed over the past months that could explain the decline in the stock price and to see what implications it may have on our valuation model and eventually on our rating.

Past developments

Impacts of the Q1 results

The first large decline in the stock price has happened in May after the company has announced a " slow start of the year ". Although the company has achieved record sales in the first quarter of 2023 , the results came in below analyst estimates, which has been fuelling the sell off. At that point, full year sale guidance has been also reduced to $5.086B to $5.141B vs. $5.2B consensus account for the slow start. Important to note that EPS estimates actually came in in-line with estimates as the firm has managed to largely offset inflationary pressures by price increases.

Impacts of the Q2 results

The second large decline has happened in early August, after the latest earnings announcement. Despite the initial jump in the share price after the earnings announcement FLO has lost roughly 10% of its market value since the release of the results. We believe that this decline is somewhat unjustified as results came in above analyst estimates and have also shown strong increase compared to the same period in the prior year. At the same time, the lower levels of the guidances have also been lifted.

- Sales increased 8.8% to a second quarter-record $1.228 billion.

- Net income increased 18.8% to $63.8 million. Adjusted net income(1) increased 8.8% to $70.9 million.

- Adjusted EBITDA(1) increased 10.9% to $133.1 million, representing 10.8% of sales, a 20-basis point increase.

- Diluted EPS increased $0.05 to $0.30. Adjusted diluted EPS(1) increased $0.02 to $0.33.

Impacts on the dividends

Now, as we have previously based our valuation on dividend discount models, (just like we will do it now as well) we need to understand, how these developments may impact the firm's dividend and dividend growth in the coming quarters and how these may impact our previous input parameter assumptions.

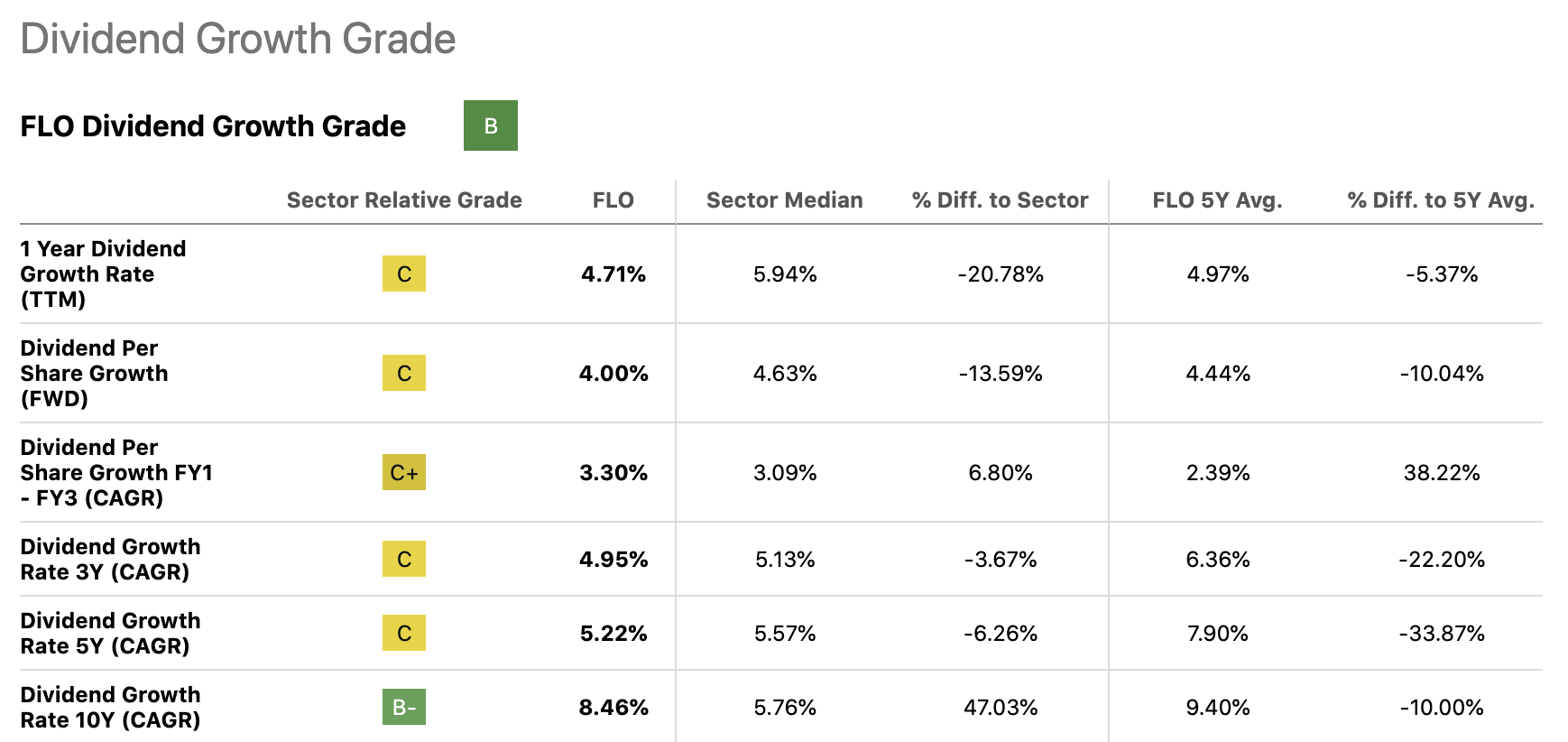

FLO has increased its quarterly dividend early this year by roughly 5% to $0.23 per share. This gross is about in line with the firm's Dividend Growth Rate 3Y ((CAGR)). The dividend has remained constant since then. The ex-dividend date for the following dividend payment is the 31st of August, and the dividend is payable on 15th of September. Assuming the $0.23 dividend for the rest of the year, the current annual dividend yield is roughly 3.9%, which may look intriguing for many dividend investors.

The main question, however, is: are these payments sustainable?

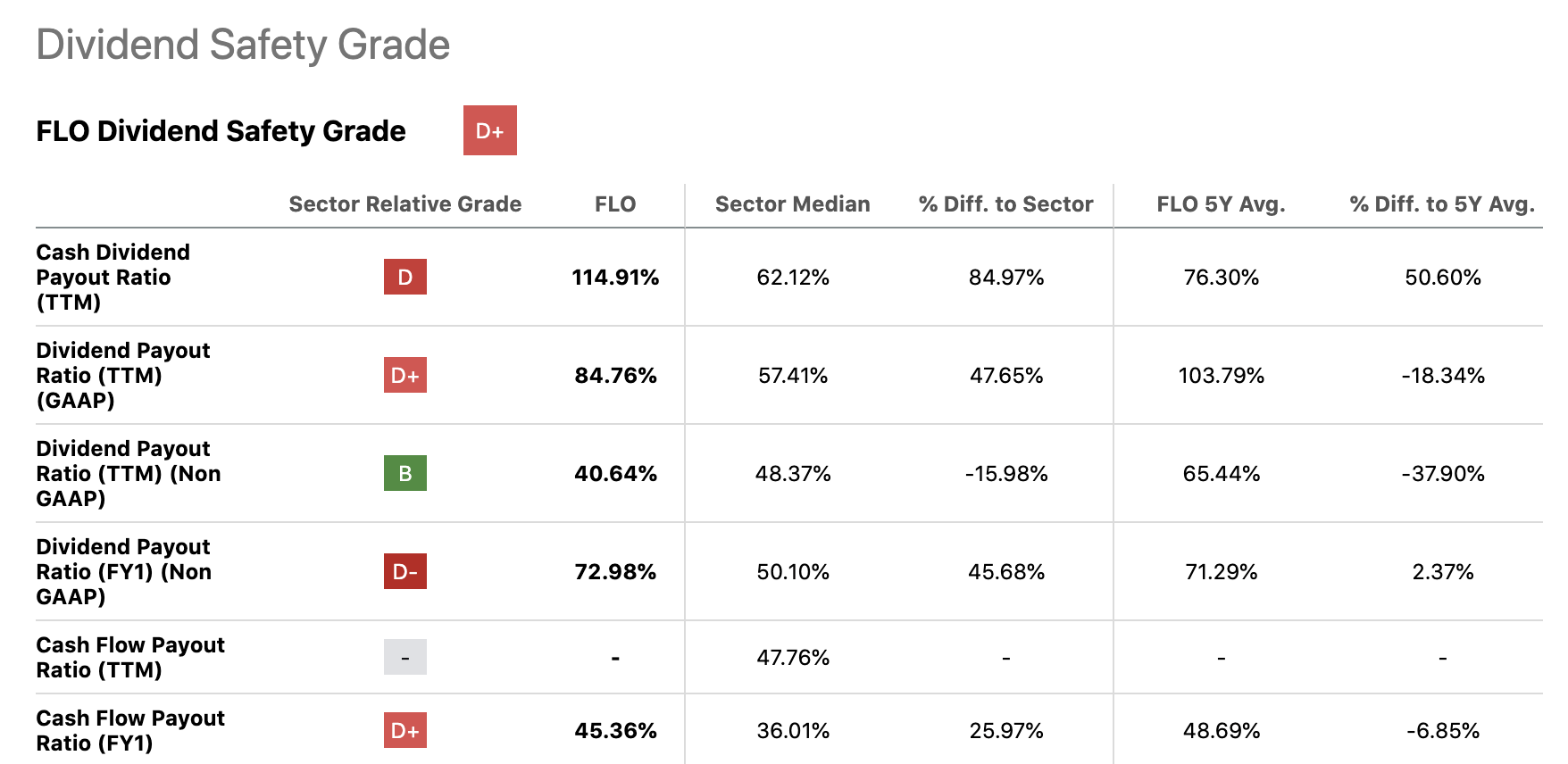

The following table shows the firm's dividend payout ratios. While the values appear to be relatively high compared to the sector medians, they do not appear to be concerning when comparing them to the company's own 5Y averages.

{kind=link}

Important to note that in the previous quarter the firm's cash flow from operation has been $71 million, while its capital expenditures came in at $34.4 million, leaving the company with a free cash flow of $36.6 million. At the same time, the firm has spent more than $15 million on share repurchases and roughly $49 million on dividends. This means that the free cash flow has not been enough to cover the returns to shareholders. At the same time the firm has issued $270 million worth of debt, which may be concerning, considering the current interest rate environment, especially if it is used for dividends and not for growth initiatives.

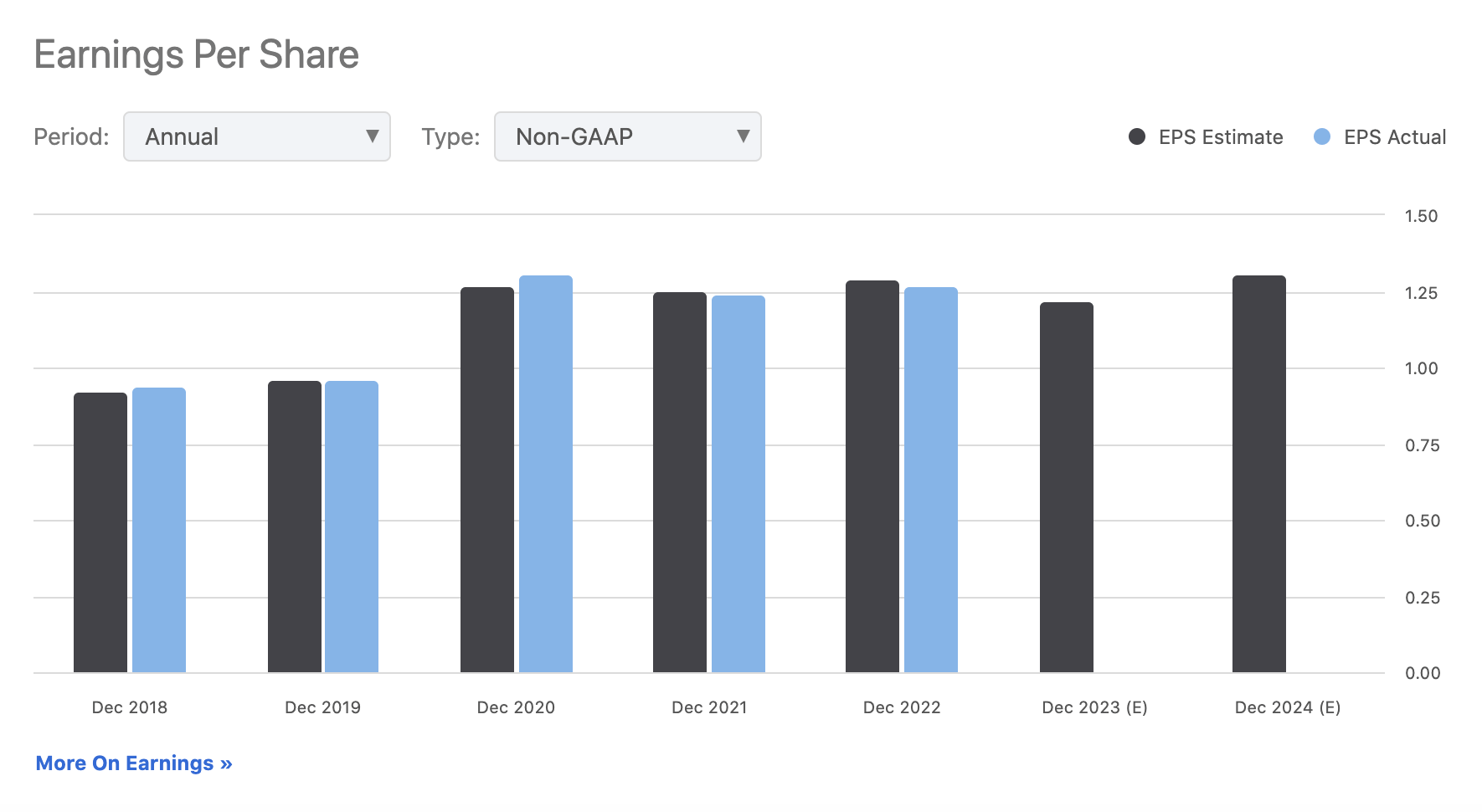

The following chart shows the earnings forecast for FLO for 2023 and 2024.

{kind=link}

We can see that earnings are forecasted to remain stable at the current level, meaning that probably there is little room left for dividend growth. Now it is time to update our valuation model in light of these developments and check how the calculated fair value compares to our prior estimates.

Valuation

In our previous article, we have come up with a fair value range for FLO's stock between $20-27 per share depending on the growth rate assumptions, using scenario analysis and dividend discount models. To get these figures, in all cases we have assumed a required rate of return of 8.75%, in line with the firm's weighted average cost of capital.

Update - Required rate of return

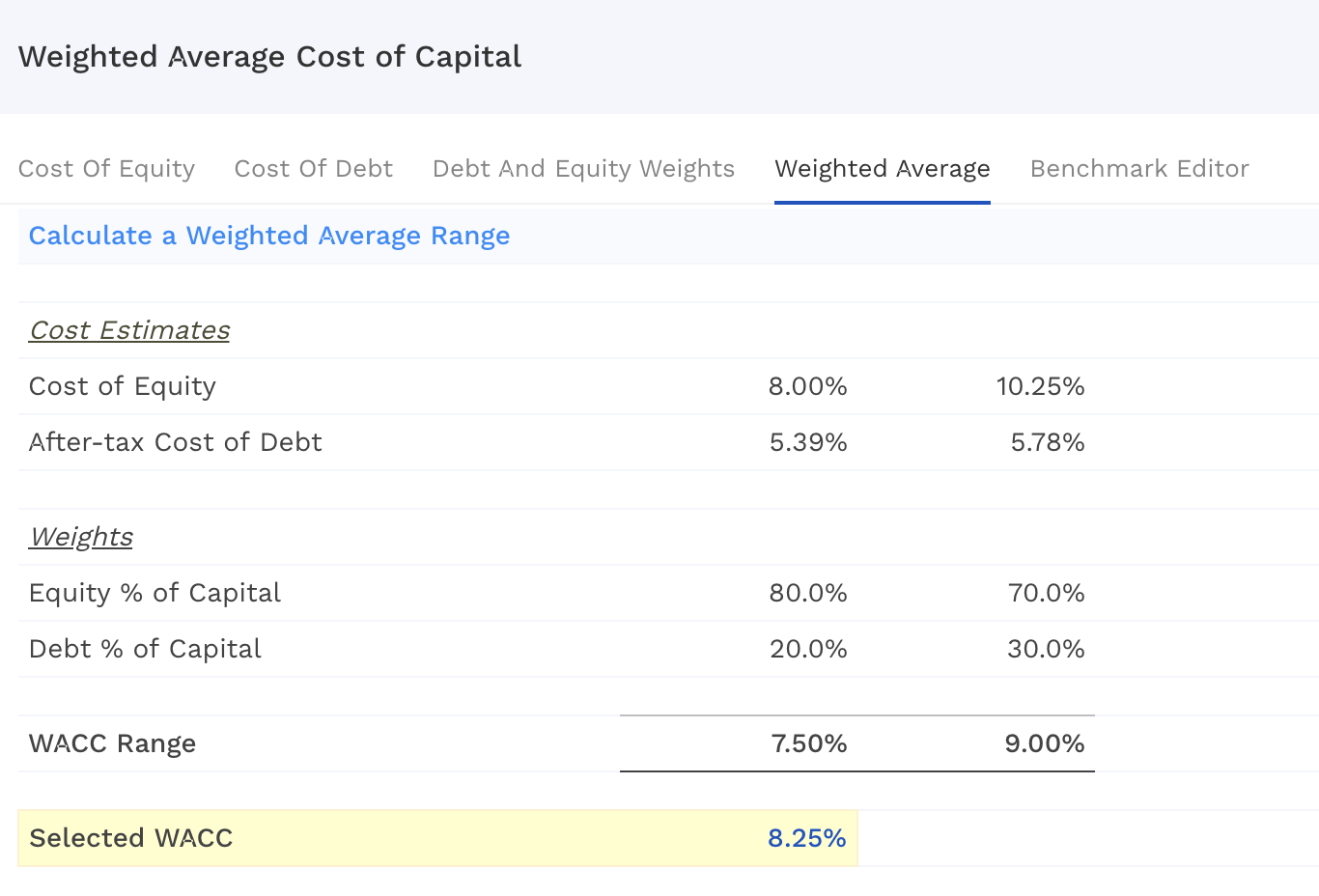

As the macroeconomic environment has evolved, we have to reflect the developments in our calculations too. First of all, we need to adjust the required rate of return.

According to the latest estimates, the company's WACC is thought to be around 8.25%.

{kind=link}

Update - Growth assumptions

In our previous article, we have been using near term growth assumptions between 5% - 7% and perpetual growth rates in the range of 3% to 4.8%. Today we will approach the situation slightly more conservatively.

We assume that the dividend will remain the same in 2023, but will need to be cut by 50% in 2024 and from the date onwards we will use 3% - 5% dividend growth rates in-line with the firm's past growth figures.

{kind=link}

Results

Using the above outlined assumptions, our calculation yields a fair value range of $10 to $15 per share.

{kind=link}

{kind=link}

While it may seem like a large drop, when Foot Locker ( FL ) has just recently announced its results and paused its dividend, a similar price movement has occurred.

Now, one might argue that the 50% dividend cut is extreme. So let us see how much the firm would need to cut its dividend so that it is covered by the free cash flow. As mentioned above the free cash flow came in at $36.6 million, while share repurchases and dividends totalled in $15 million and $49 million respectively. If we eliminate the share repurchases completely, then the dividend would be reduced by roughly 25%. This scenario would result in a fair value of $22 per share on the high end, which is still below the current market price.

{kind=link}

Conclusions

Since our last writing, FLO's market value has dropped by more 12%, mainly fuelled by the price declines following the quarterly earnings announcements.

Despite the decline, we believe that the stock is still not attractively priced based on our dividend discount models. Plus, in the latest quarter, the firm's free cash flow has not been enough to cover the share repurchases and dividends, which might raise further questions about dividend safety and sustainability.

On the other hand, the firm has managed to increase its sales year over year and has managed to deal with inflationary pressures by price increases.

For these reasons, we maintain our "hold" rating.

For further details see:

Flowers Foods: The Valuation Remains Unattractive Despite The Sell-Off