FLNC - Fluence Energy: Armed With Disruptive A.I.

2023-08-04 17:19:55 ET

Summary

- Fluence Energy offers grid scale storage hardware installation, maintenance, and A.I. energy management services.

- They are a joint venture by AES Energy and Siemans to produce a company capable of meeting the growing demand for grid storage.

- Over the last two years, they have experienced a 611.7% revenue increase at an average quarterly rate of 76.47%.

- Margins have been improving; guidance places the company Adjusted EBITDA neutral by the end of the year, and positive at some point in 2024.

- After looking over their tailwinds, financials, and valuation, I currently consider FLNC a Buy.

Thesis

Dramatic changes in the levelized cost of solar power are currently forcing a sea change in how our electric grid functions. In order to mitigate the problems caused by the widespread adoption of solar, we are incorporating storage into the system and transitioning from a continuously oversupplied grid into an instantaneously managed one.

The passage of the Inflation Reduction Act dramatically increased our pace of adoption. Instantaneously managing something as dynamic and complicated as our grid has always been beyond human capability, so up until fairly recently we wouldn't have considered it. Developments in Artificial Intelligence have changed everything.

Fluence Energy, Inc. ( FLNC ) is one of several companies currently positioning themselves to be able to compete for dominance in this highly disruptive emerging industry. With the company already vertically integrated for the production of grid scale batteries, and already in control of their own fully functioning A.I. energy manager, they are very well positioned to benefit from the widespread adoption of grid scale energy storage. After looking over their financials and valuation, I presently rate Fluence Energy as a Buy.

Company Background

Fluence Energy provides energy storage equipment and services. The company was formed in early 2018 as the result of a joint venture between AES Corporation ( AES ) and Siemens ( OTCPK:SIEGY ). The two companies hoped to pair AES's extensive research with Siemens' expansive global presence. Fluence currently has 6.6GW of storage deployed, contracted, or managed in 47 different markets.

Fluence Energy offers both hardware installation and maintenance services, as well as operational capability through A.I. controlled energy management software. They provide turnkey energy storage products with fully integrated hardware, software, and digital intelligence.

{kind=link}

FLNC Delivery Services (Fluenceenergy.com/energy-storage-services/)

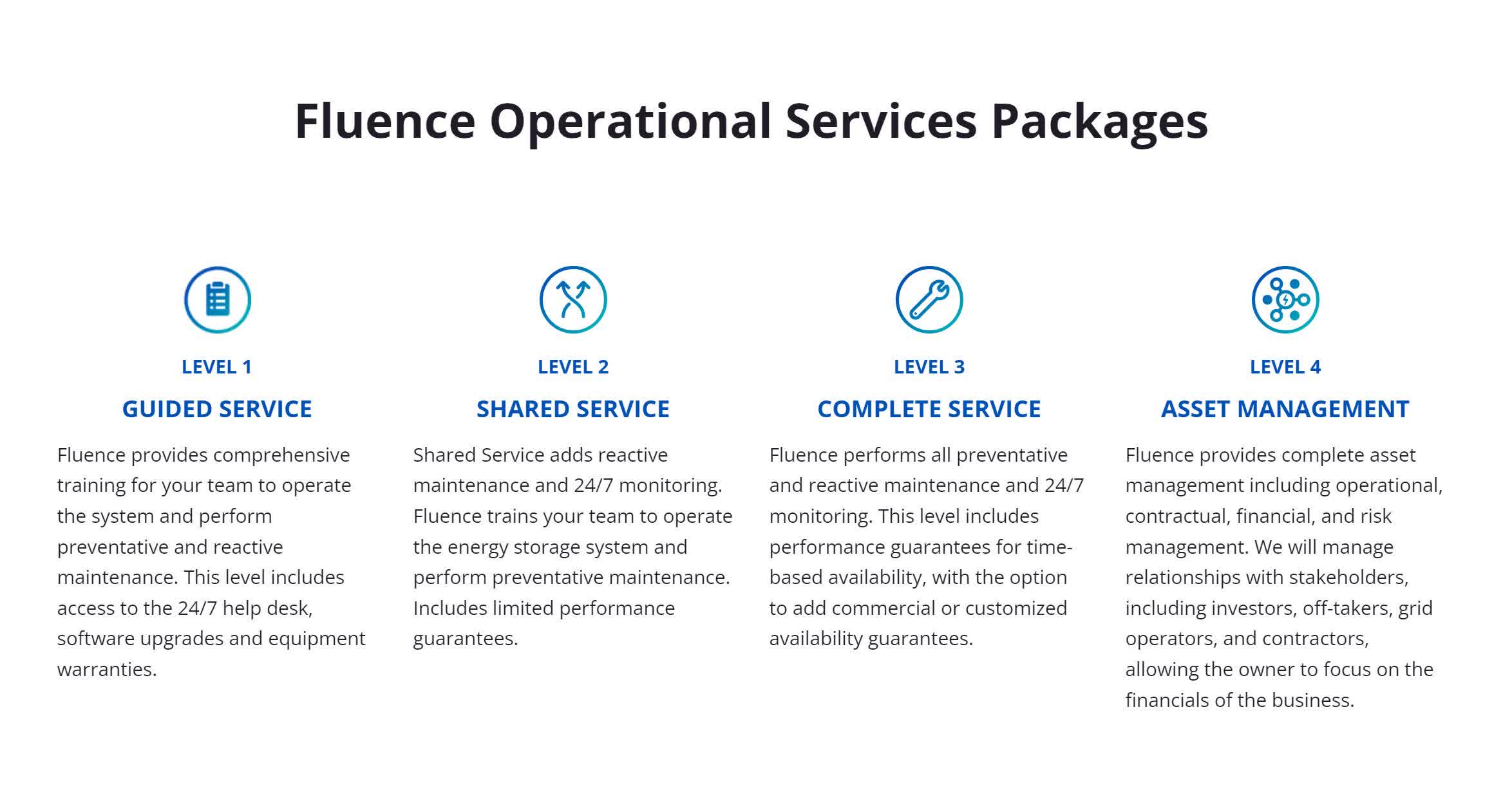

Fluence also offers a variety of service and management packages. Customers who want a more hands off approach can sign up to one of their more full-service options.

{kind=link}

FLNC Operational Services (Fluenceenergy.com/energy-storage-services/)

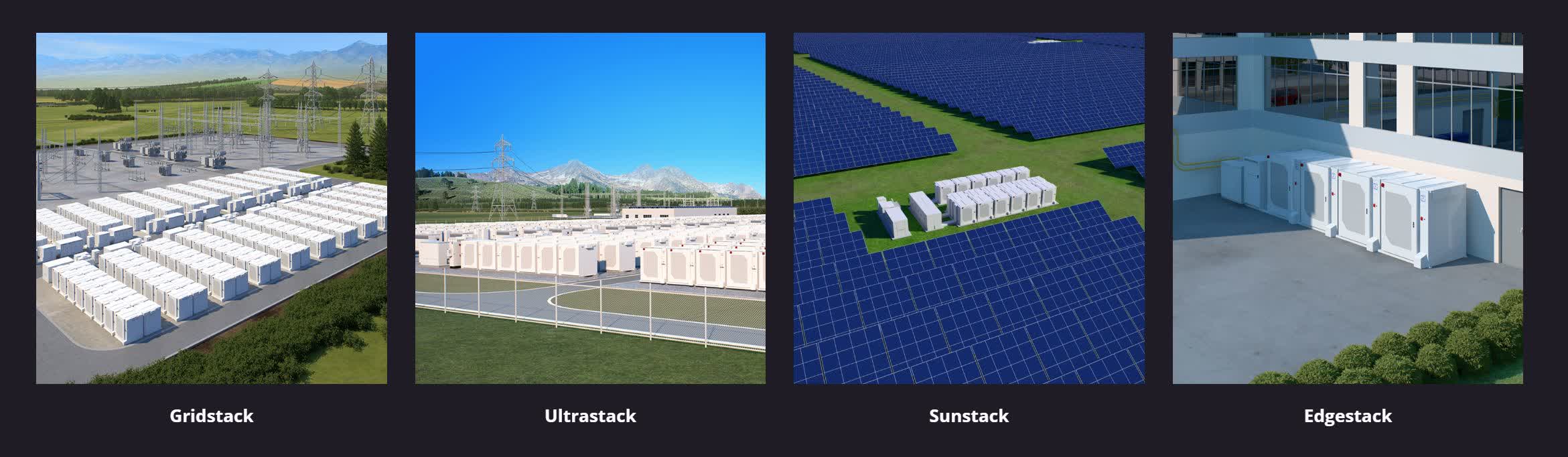

Fluence is a vertically integrated grid scale battery manufacturer. They are several generations into their development, they currently produce a highly modular cube shaped battery. When used in their separate applications, Fluence gives each of their technologies its own unique brand. Their grid-scale energy storage product is known as Gridstack; their control and operation system is known as Ultrastack; their solar capture optimization system is known as Sunstack; and their commercial energy storage and load flattening system is known as Edgestack.

{kind=link}

FLNC Storage Services (Fluenceenergy.com/energy-storage-technology/)

Long-Term Trends

The grid-scale battery market is projected to experience a CAGR of 26.1% until 2031. The global smart grid market is projected to have a CAGR of 18.2% until 2030. The United States renewable energy market is estimated to have a CAGR of 10.1% through 2028, and the global market is projected to have a CAGR of 16.9% until 2030.

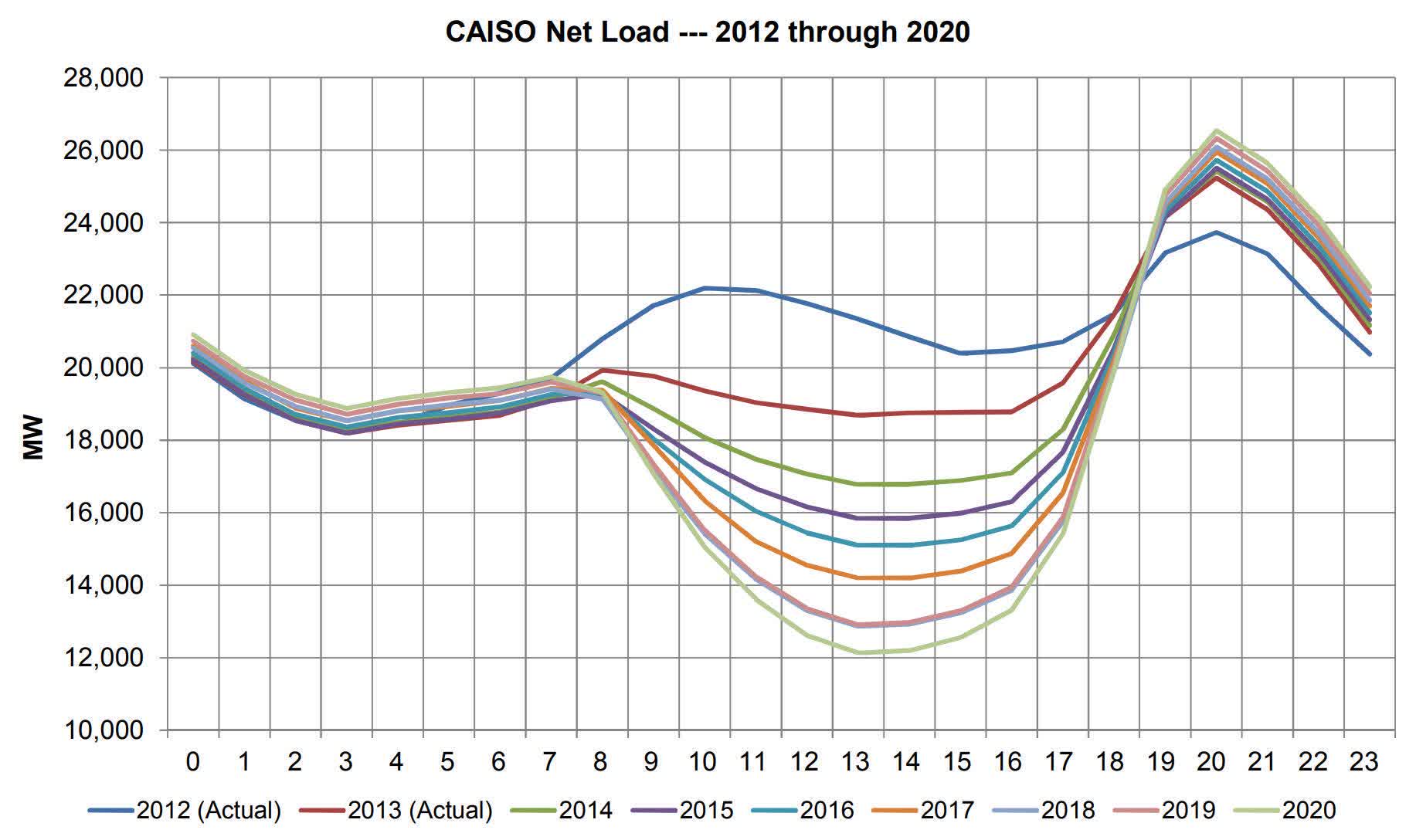

The Levelized Cost of Electricity is one of the primary factors at play when examining long-term energy infrastructure trends. With photovoltaics achieving the title of our cheapest source of electricity several years ago, additional inclusion of renewable sources seems inevitable. However, the adoption of intermittent sources has been warping the daily supply and demand curve for grid supplied electricity. This supply and demand imbalance produced by solar is known as the Duck Curve. Uncontrolled overproduction from solar has the potential to damage portions of the grid. This problem has grown severe enough that we are already disconnecting portions of commercial scale solar operations during the middle of the day.

{kind=link}

The Duck Curve (Brad Bouillon; Standford University)

Since the initial adoption of our electric grid, it has operated on a continuous supply basis. Traditionally, because of the significant startup time for most power plants, changes in future demand must be forecast. Because of the need to avoid shortages, not only must demand be forecast, managers must intentionally overshoot that expected demand. Our continuously oversupplied grid operates with significant waste and is in dire need of storage capacity.

Because they are viewed as the single most vital part of our current grid, the base load providers have enjoyed superior pricing power at the negotiating table. With our inverter technology already above the threshold where they can achieve a strong stable signal, and the rise of storage providers undermining the need for continuous oversupply, as even more decentralized sources are incorporated into the system the individual negotiating power of electricity producers should diminish.

As the total storage capacity within the system grows, and we incorporate more medium and long-term storage into the system, I expect that negotiating power will shift toward the storage providers. Eventually, they may be able to adopt a we don't need you stance while negotiating against any single source provider. For this reason, I believe only the most cost-effective base load providers will thrive in the coming decades.

Also, I believe the need for peaker plants will also slowly go away . Peaker plants are usually powered by natural gas. They are designed to be able to synchronize with the grid and achieve operational power from a cold start within a few minutes. We ask them to come online breifly to mitigate the spikes in demand that occur every evening. We also ask them to help us maintain stable oversupply during events which cause changes to usage habits on a truly massive scale, like the Super Bowl, the Olympics, or the World Cup.

{kind=link}

Wholesale California Electricity Prices Over 24 Hrs. On A Spring Day (Charles W. Forsberg; ResearchGate, May 2020)

As the grid storage industry is incredibly disruptive, I also expect a price war to break out. Storage providers can collect free or almost-free electricity during periods of overproduction. In places where a significant portion of electricity comes from solar, this happens in the middle of the day, every day. They can later sell that electricity when it's trading at its highest every evening. In addition to experiencing an erosion of their negotiating power, I do not expect the source providers will be able to compete with actively managed storage providers if a price war breaks out.

The thing to note here is that storage providers are financially incentivized to get their hands on as much overproduction as possible. Companies wanting to increase the volume of electricity they can arbitrage each day are going to attempt to install grid scale storage sites into as many markets as possible. This is one of the greatest shake-ups the industry has seen since its inception; we may even see already established utility companies begin installing storage into the service areas of rival utility providers. Over the next several decades, I believe the arbitrage business has the potential to scale into a truly massive industry.

Fluence Energy's A.I.

The machine learning software packages that we have been developing to actively manage multiple dynamic sources are what is making this possible. I think the companies which are able to develop the most capable A.I. are the ones which stand to benefit the most from actively managing our future smart grid.

Fluence Energy was formed as an attempt by AES and Siemens to pool their knowledge and experience to produce a company capable of meeting the growing demand for grid scale storage. Fluence Energy expanded their capability with the aquisisiton of Nispera in April 2022. Nispera collects and analyzes data from multiple sources to monitor production in real time. It uses this data to forecast production, identify underperformance, screen for anomalies, and give automated feedback.

The acquisition of Nispera increased their capabilities and in February of 2023, they began offering Fluence Mosaic . Mosaic is intelligent bidding software designed to help asset owners maximize revenue. This cloud-based digital intelligence is already performing feats beyond human capability; handling bidding cycles as short as 5 minutes in California , Texas , and Australia .

Guidance

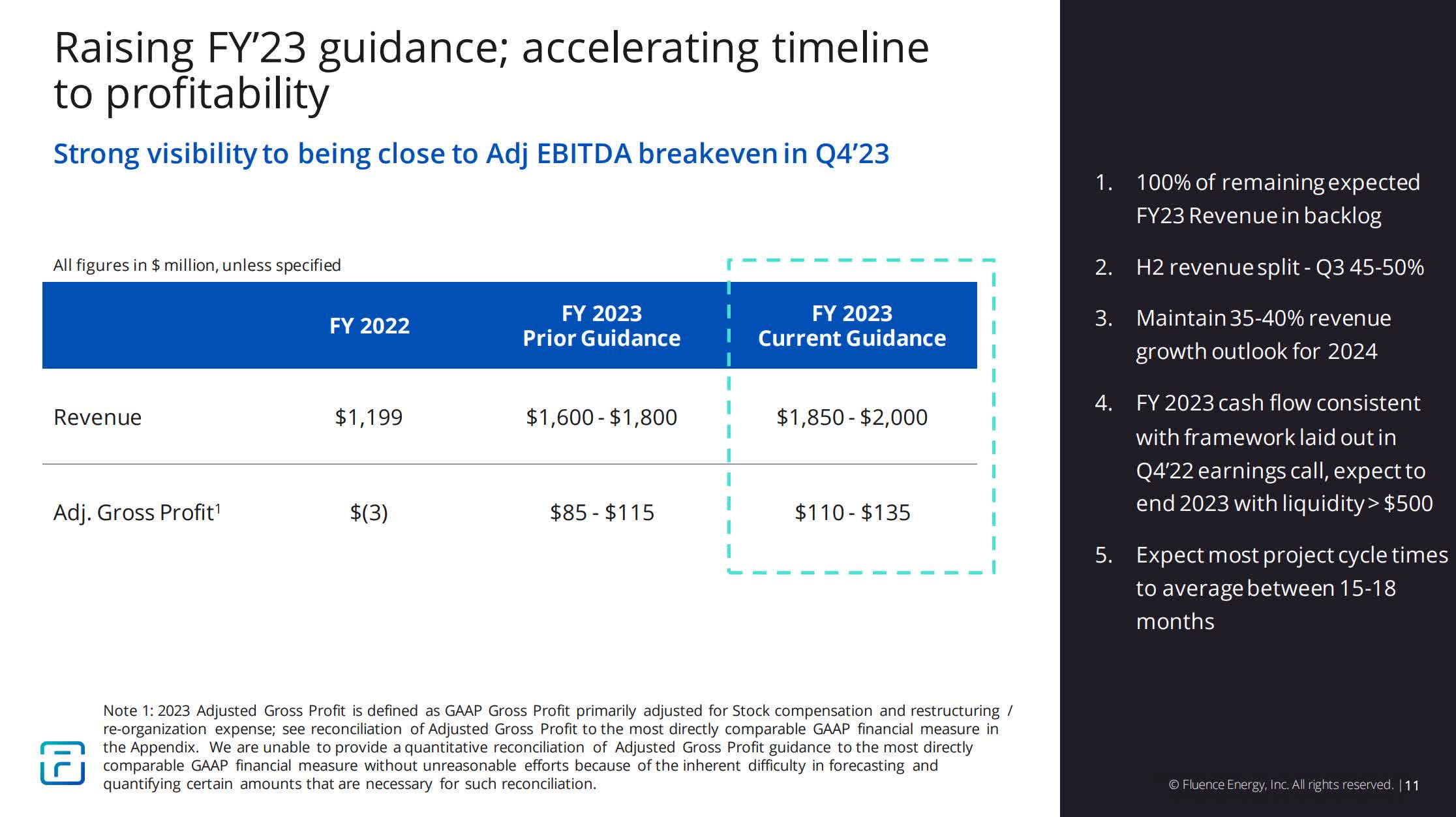

Their most recent earnings call revealed that their backlog of signed contracts had reached $2.8B as of March 31st, coming in approximately $100M above the previous quarter. While their parent companies have accounted for a significant portion of their business so far, approximately 81% of their backlog is with not-related parties. Their total backlog of contracts is up to $11.2B.

They also increased the amount of assets they had under A.I. management by 800 MW and were able to place an additional 2.7 GW under contract for digital management. They stated this represented a 200% increase from the previous quarter.

They previously expected to be adjusted EBITDA positive in fiscal year 2024. They are now revising their expectations to be close to adjusted EBITDA break even in the fourth quarter of fiscal year 2023. They stated they believe they will not need to raise any additional capital and have ample liquidity to meet their cash needs for the next 12 months.

{kind=link}

FLNC Guidance (2Q FY2023 Earnings Presentation, Page 11)

Financials

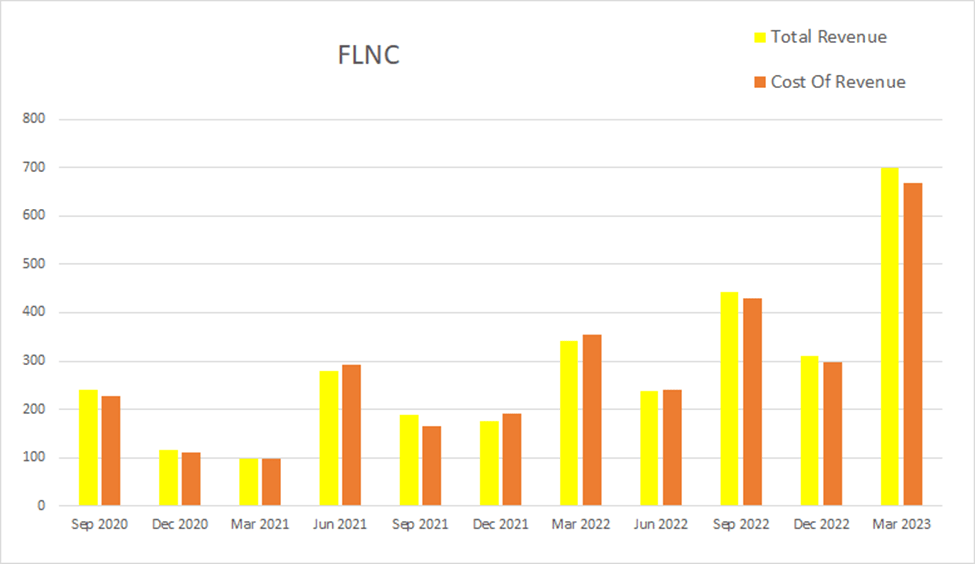

Fluence has been experiencing significant revenue increases. Eight quarters ago Fluence Energy had a quarterly revenue of $98.1M. Four quarters ago that had risen to $342.7M; by this most recent quarter that had further grown to $698.2M. This represents a total two-year rise of 611.7% at an average quarterly rate of 76.47%.

{kind=link}

FLNC Quarterly Revenue (By Author)

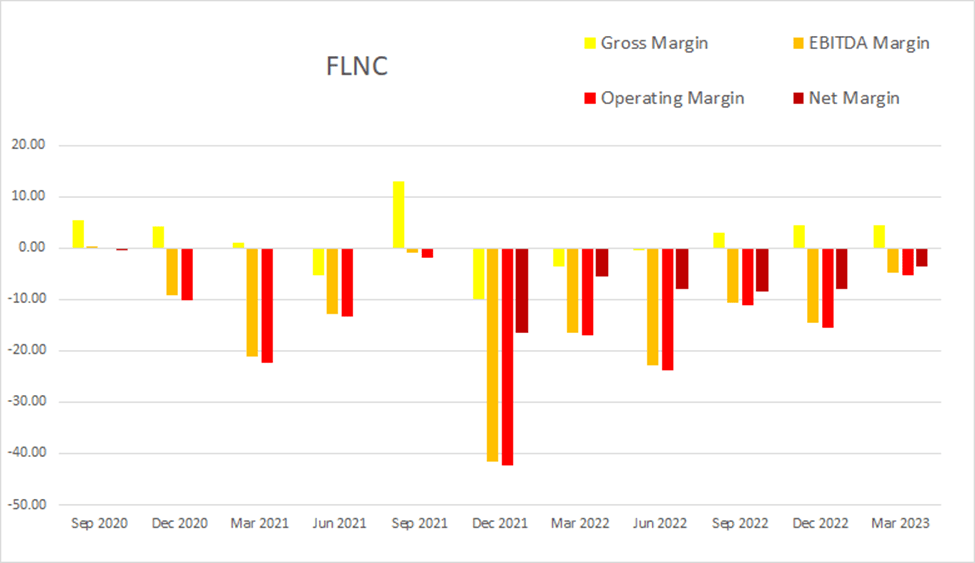

Their margins have been improving for the last several quarters. As of the most recent quarter gross margins were 4.38%, EBITDA margins were -4.88%, operating margins were -5.27%, and net margins were -3.57%.

{kind=link}

FLNC Quarterly Margins (By Author)

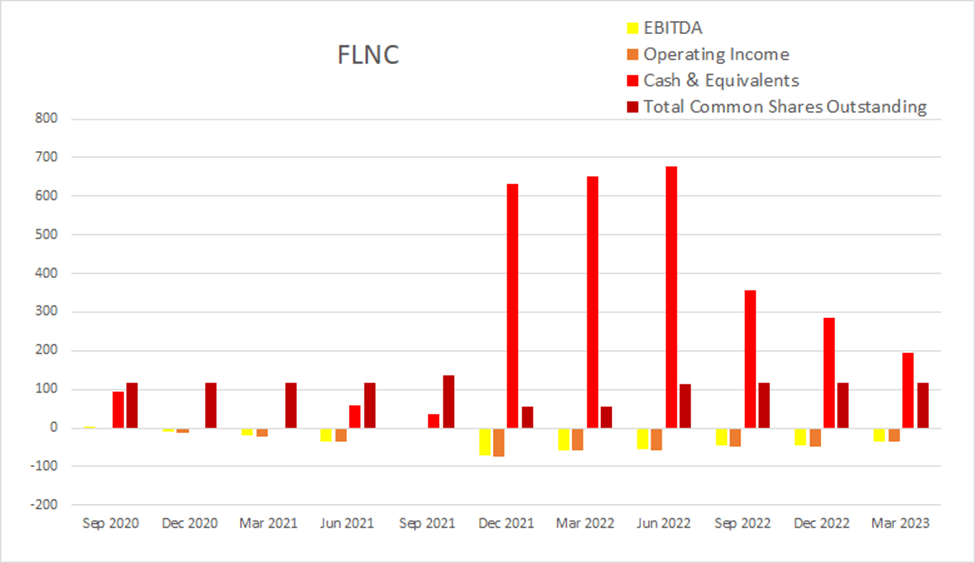

As of the most recent quarter cash and equivalents was $194M, short-term investments was $70M, and quarterly operating income was -$37M. Their share count has been growing at a fairly stable rate for the last four quarters. In June of 2021, total common shares outstanding was at 114.3M; by this most recent quarter that had risen to 116.9M, a 2.27% increase.

{kind=link}

FLNC Quarterly Share Count vs. Cash vs. Income (By Author)

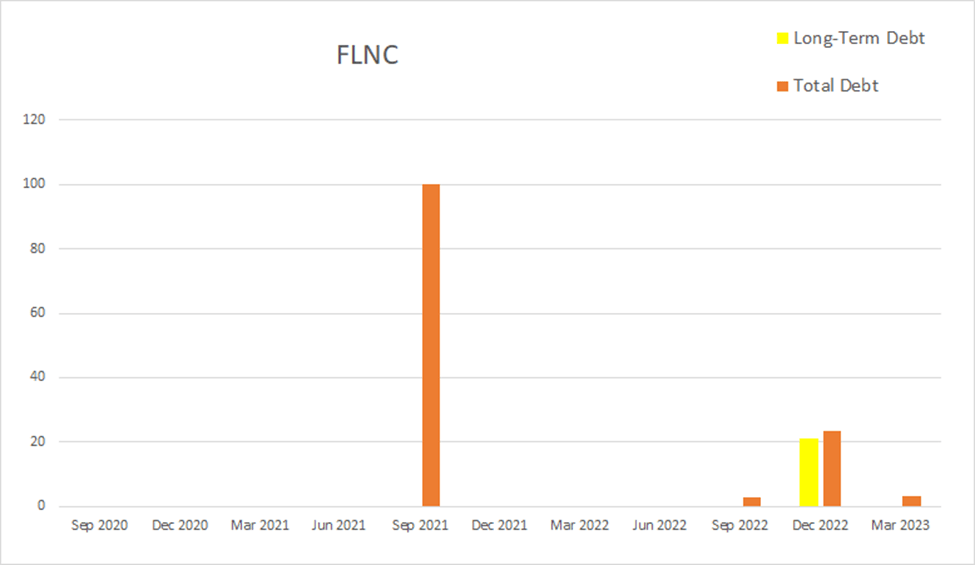

As with many spin-offs and joint ventures, and unlike many start-ups, Fluence has not had to take on large amounts of debt on its path to operational viability. This most recent quarter, Fluence Energy had -$0.1M in net interest expense, total debt was at $3.4M, and long-term debt was at $0M.

{kind=link}

FLNC Quarterly Debt (By Author)

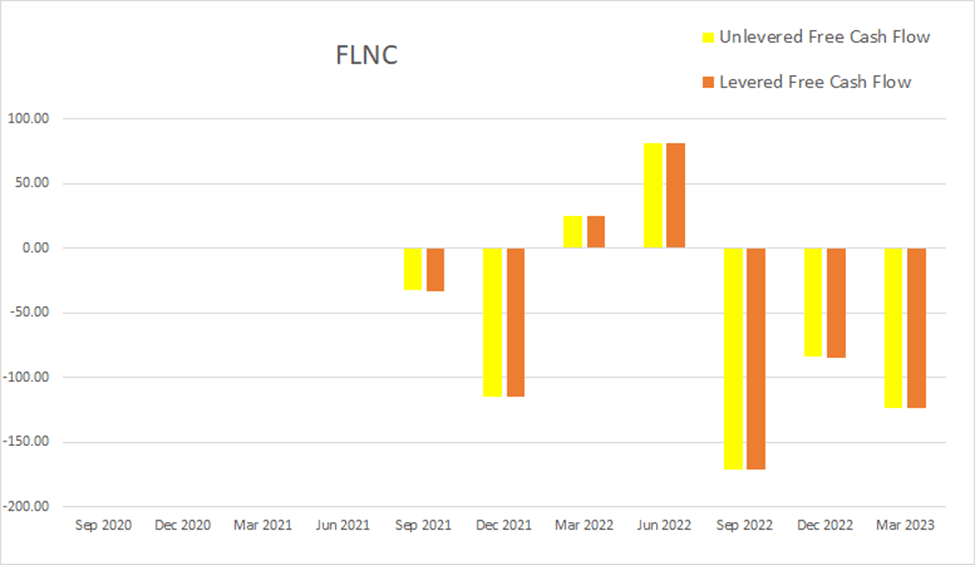

As the company approaches adjusted EBITDA profitability, I expect that these cash flow values will improve. As of this most recent earnings report, unlevered free cash flow was at -$123.4M, while levered free cash flow was at -$123.9M.

{kind=link}

FLNC Quarterly Cash Flow (By Author)

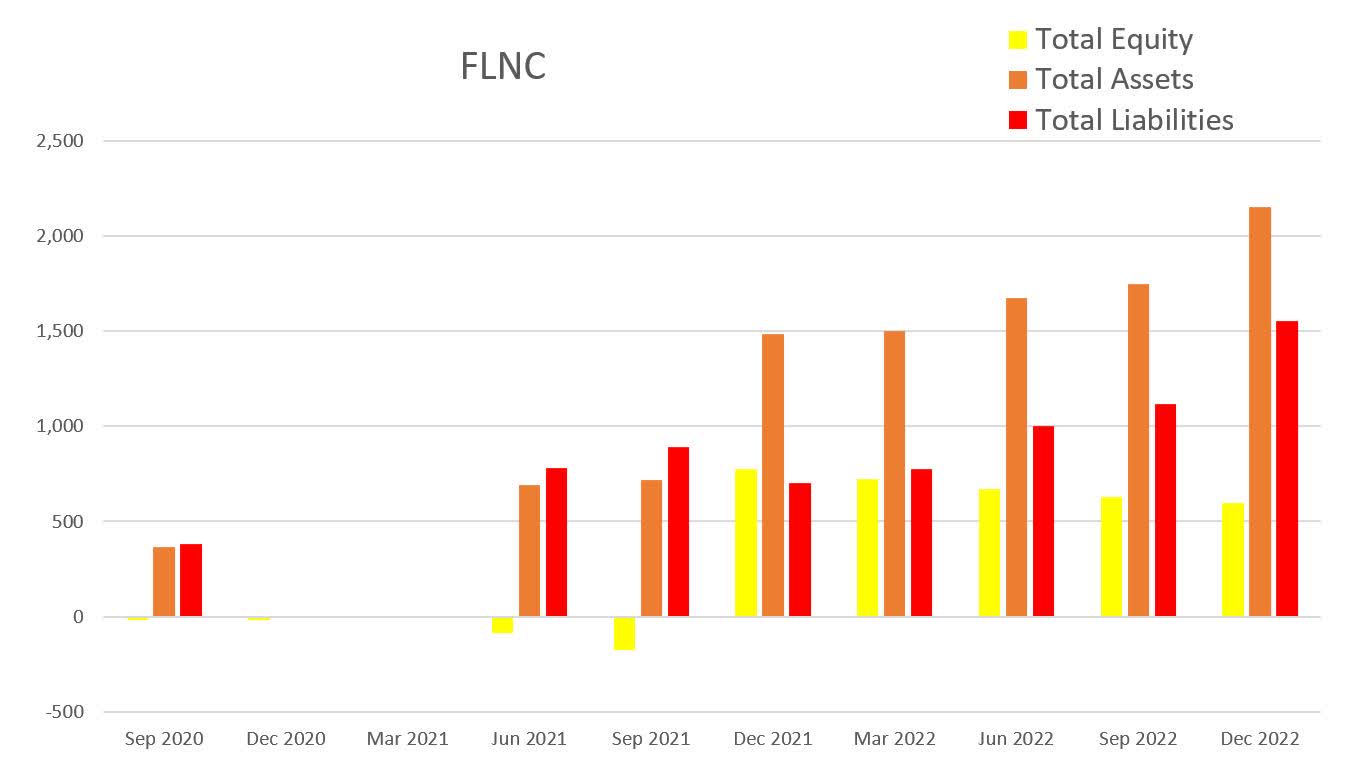

Their total equity rose dramatically in late 2021 but has been slowly declining since then.

{kind=link}

FLNC Total Equity (By Author)

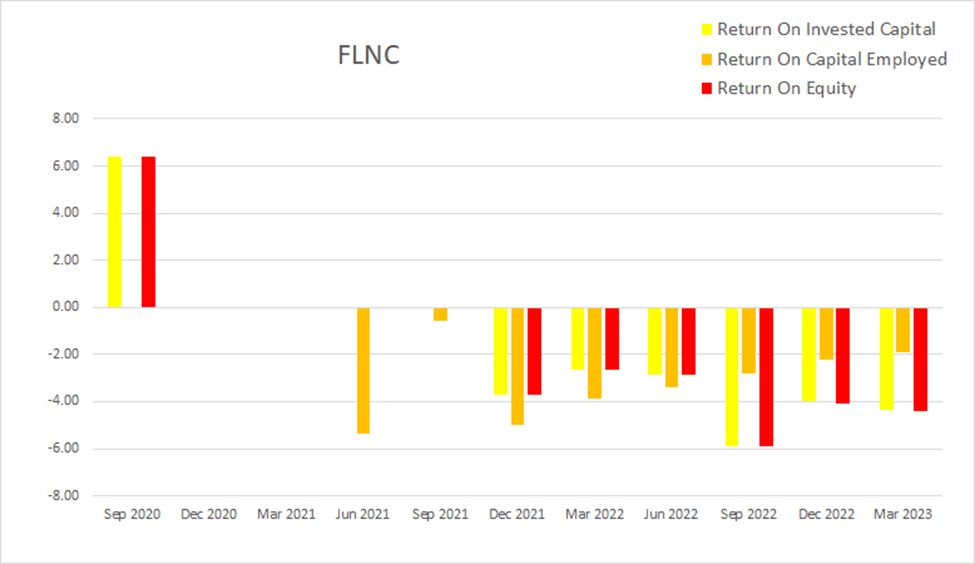

Similar to my thoughts about their cash flow, I expect their returns will shift into positive territory as they continue to improve their margins. As of the most recent earnings report ROIC was -4.36%, ROCE was -1.89%, and ROE was at -4.38%.

{kind=link}

FLNC Quarterly Returns (By Author)

Valuation

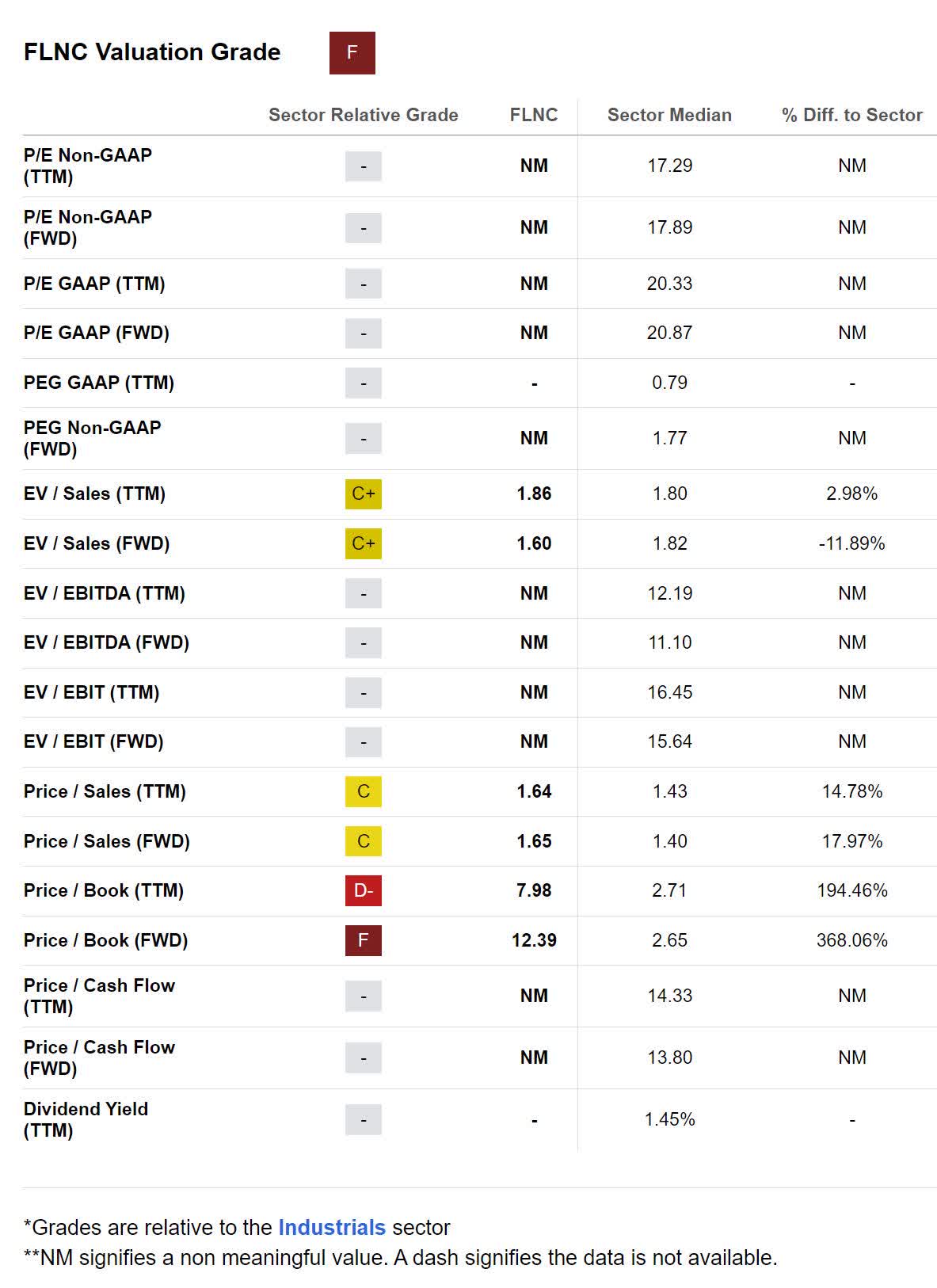

As of August 3rd, 2023, Fluence Energy had a market capitalization of $4.92B and traded for $28.36 per share. The company is not profitable so I cannot produce a PEGY estimate, but they do have an EPS Long-Term CAGR of 35%. Considering their guidance for profitability, I view their forward EV/Sales of 1.6x, Price/Sales of 1.65x, and Price/Book of 12.39x as showing the company as presently undervalued.

{kind=link}

FLNC Valuation (Seeking Alpha)

Risks

Despite their positive guidance, the margin expansion and cash flow improvements might not materialize. With their cash and short-term investments, the company currently has $264.4M in unrestricted funds. Their most recent quarterly levered cash flow was -$123.9M, while cash from operations was -$74.5M, EBITDA was at -$34.1M, and operating income was -$36.8M

I believe that arbitragers will eventually gain significant control over the price of electricity as supply and demand both vary throughout the day. However, this may not occur. If the general public views what the storage providers do as price manipulation, they may one day face regulations.

Fluence Energy has multiple competitors including Stem ( STEM ), and C3.ai ( AI ). While they certainly do appear to be capable, their eventual dominance in this emerging industry is far from a guarantee.

Catalysts

The company currently has $11.2B under contract waiting to be converted into revenue. This most recent quarter, they were only able to fill $700M worth of orders and yet signed $2.8B in new contracts. This $2.8B came in above their previous quarter's new contract value of $2.7B. The picture that is being painted by this trend is that demand for their product is currently outstripping the pace they can install new storage. It's fairly clear why the company believes they will be able to grow revenue; their waiting list is growing.

The grid scale storage industry currently uses mostly lithium-ion based batteries, but I believe this will change. As the upcoming production ramp up of Iron-Air batteries comes to market, the total cost of grid scale storage should decline significantly. This should further increase demand for Fluence's products and services.

Currently, most of the conversation within the industry is about short-term storage. As we further develop batteries more capable of handling medium and long-term applications, the storage market will find new demand.

Conclusions

Fluence Energy is still transitioning from the introduction/startup phase of the business life cycle into the growth phase. They are currently blessed with no long-term debt, and the low cost of solar should provide them with sustained tailwinds for years to come. I think their machine learning digital management packages have already proven themselves effective, and are probably one of the reasons the company is experiencing increasing demand. This company already has $11.2B in revenue waiting on them, and they are signing up more every quarter. Their margins have been improving and guidance is positive, so most of my remaining questions revolve around how quickly they can reach positive cash flow.

Because of the disruptive nature of their technology, and their attractive long-term projected growth rate, I believe waiting to buy until after the company achieves positive cash flow may be a mistake.

Editor’s Note : This article was submitted as part of Seeking Alpha’s Best AI Ideas investment competition , which runs through August 15. With cash prizes, this competition -- open to all contributors -- is one you don’t want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Fluence Energy: Armed With Disruptive A.I.