AES - Fluence Energy: Differentiating Itself As A Leader In Battery Energy Storage

Summary

- The new Fluence Energy, Inc. management team has shown strong execution capabilities as they addressed each of their objectives set for the company.

- In the Q1 FY2023, Fluence Energy achieved a record order intake of $856 million, bringing the contracted backlog to $2.7 billion.

- The company is the preferred supplier of energy storage solutions as a result of strong safety, performance, bankability, and reliability profile.

- Fluence Energy had $460 million in cash as of the first quarter of FY2023, and management expects that they do have more than sufficient capital for its current business plans.

- My 1-year target price for Fluence Energy is $26, implying 34% upside from current levels.

Investment thesis

I think that Fluence Energy, Inc. ( FLNC ) is looking more attractive to me, as the company's new management team looks to be executing well and working towards the company's new focus of profitable growth. The management team showed investors that they are serious about meeting their strategic objectives set in the prior quarter. Furthermore, Fluence Energy has a solid backlog of $2.7 billion and $10.3 billion in its pipeline, highlighting strong visibility on revenue and commercial opportunities. Lastly, the company remains well-funded for its near-term business plans with the cash on its balance sheet , while the backing from its two sponsors provides a great support for the business.

Meeting strategic objectives

Management set strategic objectives it wanted to achieve in the prior quarter. They managed to deliver strongly on these objectives. One of the strategic objectives is to deliver profitable growth. In FY2023, the revenue and gross margin improvement was admirable, and Fluence Energy, Inc. even raised its guidance as a result of improvements in the supply chain and increased demand.

Another objective was to develop products and solutions that its customers need, which was satisfied in the quarter as Fluence Energy announced that they will start giving customers the option of using Northvolt batteries in its Gen 6 Cubes . The addition of Northvolt batteries will also help Fluence Energy to further diversify its supply of batteries by introducing a European battery producer.

In addition, another of Fluence Energy's objectives is to use Fluence Digital as a competitive differentiator and margin driver. In the quarter, management entered the ERCOT market with its Mosaic Bidding application and was awarded the first contract with a non-related party. Mosaic is now available in ERCOT, California ISO, and Australia's National Electricity Market. Management expects to bring Mosaic to four more markets in the next three years. On top of that, Fluence Energy launched Nispera's Battery Energy Storage Systems ("BESS") performance management capabilities, which will allow customers to use one asset performance management platform for all of their assets. This is one of the first asset performance management system in the world to be deployed across all four renewable asset classes of battery energy storage, solar, wind and hydro.

Lastly, Fluence Energy, Inc. management improved the company's supply chain, as the battery requirements for FY2023 are either in-transit or in-country. This enables Fluence Energy with better supply chain management, and it should be able to execute well operationally to deliver products to customers when they require them. This is a great improvement, in my view, for the Fluence Energy team as the company faced challenges in getting batteries from suppliers in 2022, and now the company is in better control of its supply chain. Management also states that they do not "foresee supply chain issues that could derail its FY2023 expectations."

Commercial traction

In the first quarter of FY2023, Fluence Energy achieved an order intake of $856 million. This is a record order intake for the company, up from its order intake of $560 million in the fourth quarter of FY2022. Furthermore, it highlighted the strong demand for Fluence Energy across its three business segments, with 624 megawatts for Solutions, 139 megawatts for Services, and 783 megawatts for Digital.

One other significant point to note is that management highlighted its 1,200 megawatts contract with Orsted.

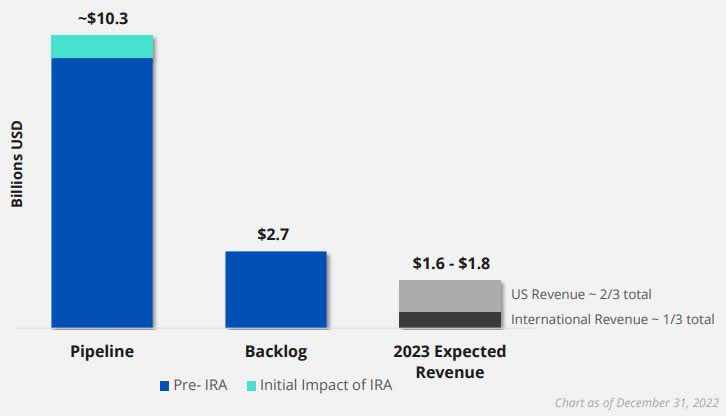

Fluence Energy currently has a signed backlog contract value of $2.7 billion. Its current backlog is about 1.6 times the current guidance for 2023 revenue at the midpoint. Furthermore, this quarter's signed backlog contract value was 20% higher sequentially when compared to the prior quarter.

Finally, and most importantly, management highlighted that more than 70% of the company's backlog are with non-related parties. This is significant, because many investors did not believe in Fluence Energy's ability to grow the backlog without using its partners The AES Corporation ( AES ) and Siemens AG ( SIEGY ). As a result of the disclosure that the backlog made up of at least 70% non-related parties, along with the $500 million project with Orsted and the $225 million project in Germany that has been announced, this will help provide strong evidence in demand for Fluence Energy's products and services from outside its partners.

Also, the company has a pipeline of more than $10.3 billion . This is almost four times that of its backlog. This strong pipeline was a result of some projects that have come in early that are a result of the Inflation Reduction Act.

Fluence Energy pipeline and backlog (Fluence Energy IR)

{kind=link}

Management highlighted in the fiscal Q1 earnings call that its project leads are currently at an all-time high, which indicates strong potential opportunities ahead. With the Inflation Reduction Act, Fluence Energy's United States revenue growth is expected to be 40% to 50%, resulting in expectations for the overall business revenue growth to come in at 35% to 40%.

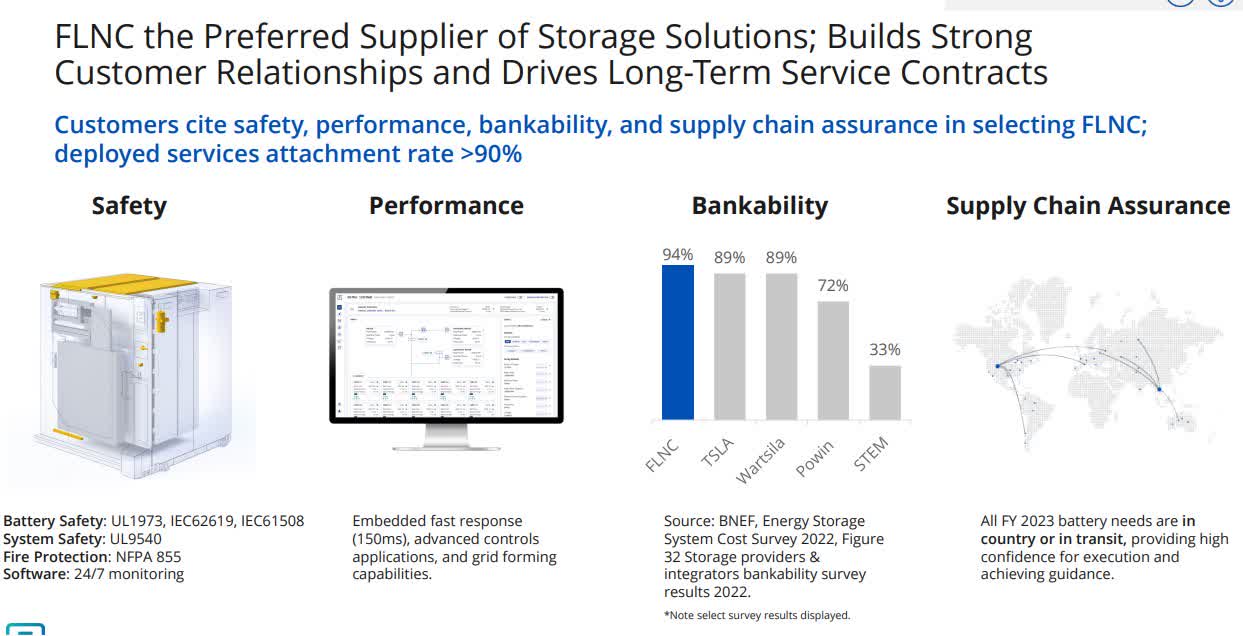

Fluence Energy as the preferred supplier of energy storage solutions

The first way Fluence Energy prioritizes itself is on safety. The company continues to be a leader in safety in the industry and meets all industry standards. This forms the foundation for the demand for Fluence Energy products.

In addition, Fluence Energy is able to deliver products that perform at a high level, as the company deployed the world's fastest-responding battery and storage facility, and its team has achieved demand response times of less than 150 milliseconds on assets deployment.

On top of that, Fluence Energy has high bankability, as customers look for additional finance for larger projects and have found the company to be reliable. Customers are thus confident when they underwrite projects with Fluence BESS. Based on BNEF's BESS cost survey, customers ranked Fluence Energy at the top for bankability.

Lastly, Fluence Energy has been able to provide customers with battery solutions when they require it. Also, as mentioned earlier, most of Fluence Energy's battery requirements for the year have been secured.

I think that customers are increasingly choosing Fluence Energy as their top choice for battery energy storage solutions as a result of its strong track record of performance, safety, bankability, and a resilient supply chain. This is evident from the large players that Fluence Energy is attracting as customers.

FLNC as a preferred supplier of energy storage solutions (Fluence Energy IR)

{kind=link}

Q1 2023 results

Revenue for the first quarter of FY2023 came in at $310 million , up 78% year-on-year. More than 95% of the Fluence Energy, Inc. revenue generated from the first quarter was a result of working on its backlog.

Gross margin for the quarter also improved in the first quarter of 2023, and the company generated positive gross margin for the quarter.

Fluence Energy's Services and Digital business segments continued to grow in the quarter, boosting the recurring revenue business segments further. Its deployed service attachment rate is currently rated at 90%. Most of its customers only sign service agreements when the storage solutions have been deployed, and a 90% deployed service attachment rate is healthy.

EBITDA was in-line with expectations as management continued to execute on its plan to optimize its operating expenses. Management has been able to improve operating leverage and optimize its cost structure. In the quarter, Fluence Energy moved more resources to India, utilizing its India Technology Center to enhance the support function of the business. As a result, management continued to reiterate that they are able to limit operating expense growth to less than 50% of revenue growth. Furthermore, they expect that the operating expense as a percentage of revenue for 2022 will be the high watermark for the business, implying further operating leverage improvement and improvement in adjusted EBITDA going forward.

Inventory for the quarter increased by about $400 million as a result of building its battery supply chain resilience. This is a risk mitigation strategy to de-risk the company's guidance for 2023.

Fluence Energy had $460 million in cash as of the first quarter of FY2023. As a result of the inventory build expected to the first quarter of FY2023, the second quarter's cash usage is expected to be incrementally higher than the first quarter, but management expects that they do have more than sufficient capital for its current business plans.

As a result of the higher demand for its products and services and better supply chain visibility as a result of recent measures, management increased revenue guidance for FY2023 to the range between $1.6 billion and $1.8 billion, an increase of almost 10% at the midpoint. Adjusted gross profit was also brought higher to the range of $85 million and $115 million, an increase in 25% from the prior guidance for FY2023. In addition, 99% of the 2023 revenue guided is currently in its backlog, which provides very strong visibility into the forward guidance. The benefits from the Inflation Reduction Act are expected to only become more apparent in the second half of 2023 and beyond. Lastly, management reiterated that they are working towards targeting positive adjusted EBITDA in 2024 and are currently on track.

Valuation

My 1-year price target for Fluence Energy is based on a discounted cash flow ("DCF") model used for each segment using a sum-of-the-parts of the business. Based on my DCF-based sum-of-the-parts, I assume a WACC of 12%, with values pf $2.7 billion for the product segment, $1.1 billion for the services segment and $0.6 billion for the software segment.

Thus, my 1-year target price for Fluence Energy is $26, implying 34% upside from current levels.

Risks

Execution risk

As a result of a new Fluence Energy, Inc. management team, this brings about execution risks. Fluence Energy brought in a new CEO after a few weak quarters, while they also brought in Head of Siemens Smart Infrastructure Global Competitiveness Program to assume the SVP, Chief of Business Operations & Transformation Officer. While Fluence Energy is able to leverage on the strategic partners for talent, there remains risks whether the new management team is able to execute well, scale up and deliver on their objectives and targets.

Competitive pressures

The market in which Fluence Energy is operating in is rather competitive. In addition, the technology is changing quite rapidly. As a result, Fluence Energy could face intensified competitive pressures in the future if other players in the market like Tesla, Inc. ( TSLA ) or Stem, Inc. ( STEM ) decide to take more share in the market.

Supply chain risks

The company was adversely affected by disruption to the supply chain. As Fluence Energy relies heavily on shipping and only recognizes revenue when products are delivered, if there are any supply chain disruptions, this will bring downside to the company.

Conclusion

All in all, Fluence Energy, Inc. continues to show fundamental strength, as it saw record order intake in the quarter, strong visibility for FY2023 revenue guidance as a result of its huge backlog, and continued commercial momentum with its $10.3 billion pipeline. I think that Fluence Energy, Inc. management is executing well in managing supply chain risks through measures taken in the quarter and securing its battery needs for 2023. The company is working towards its strategic objectives highlighted in the prior quarter, including focusing on profitable growth, introducing new products and services, improving its supply chain and differentiating its business with Fluence Digital.

Thus, my 1-year target price for Fluence Energy, Inc. is $26, implying 34% upside from current levels.

For further details see:

Fluence Energy: Differentiating Itself As A Leader In Battery Energy Storage