FLNC - Fluence Energy: Risk Factors In The Evolving BESS Landscape

2023-11-27 22:45:18 ET

Summary

- Fluence Energy is a leading global provider of energy storage products and services with strong revenue growth and backlog.

- The company is anticipated to face challenges in a crowded and competitive BESS market, particularly from Chinese integrators.

- Fluence's non-diversified business model, supply chain risks, and competitive pressures are limiting its growth potential.

We Are Not Bullish on Fluence, Despite Its Strong Growth and Backlog

Fluence Energy ( FLNC ) is a global system integrator of energy storage products, services, and digital applications for renewables and storage. The company was formed in 2018 as a joint venture between AES Corporation and Siemens AG, two major players in the energy sector. Fluence is currently the world second-biggest Battery Energy Storage Systems (BESS) integrator company after Sungrow with a 14% market share .

Fluence has a presence in over 40 markets globally and has more than 7 GW of energy storage deployed or contracted as of July 31, 2023. The company has achieved strong revenue growth and margin improvement in 2023. It reported Q3 revenue of $536 million , which is an increase of 124% year-over-year. The Q3 gross profit margins also increased to 4.1%, compared to -2% a year ago. Company has not been profitable since it started its business, but it expects to reach positive adjusted EBITDA in FY24.

Fluence has a large and growing backlog, which provides visibility into its future revenue potential. The company reported a total backlog of $2.9 billion as of September 30, 2023, and a consolidated pipeline of $12.4 billion which is an increase of $1.2 billion from last quarter. Additionally, the company is benefiting from the US government clean energy investment tax credit ((ITC)), which is to incentivize deployment of energy storage systems to achieve clean energy goals.

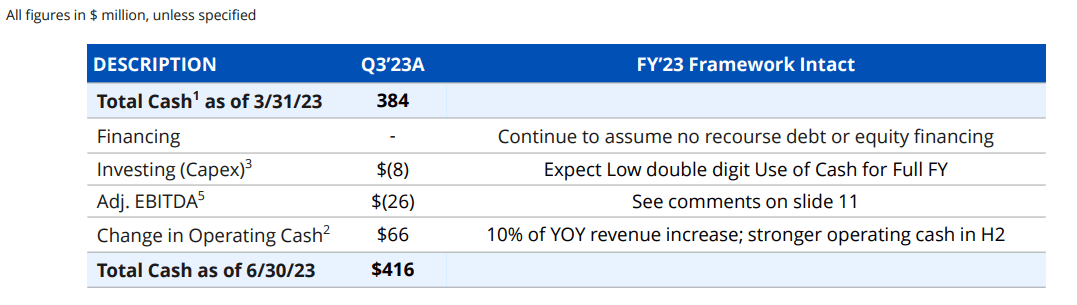

The company has a solid balance sheet, with sufficient liquidity and financial flexibility to support its growth strategy. The company has $54M debt and $416 million total cash as of June 30, 2023 (see below)

FLNC Q3 Earnings Presentation (Fluence)

{kind=link}

However, despite its strong market position and growth potential, Fluence faces several challenges and risks that may limit its upside and attractiveness for investors. In this article, we will examine some of the factors that make us skeptical about Fluence, and provide a valuation based on our assumptions and projections.

BESS Market Becoming Overcrowded

The global battery energy storage market is expected to grow at a CAGR of 20% , reaching $52 billion by 2031. The main drivers of this growth are the increasing demand for clean and reliable energy, the declining cost of batteries, the supportive government policies and incentives, and the technological advancements in battery technologies.

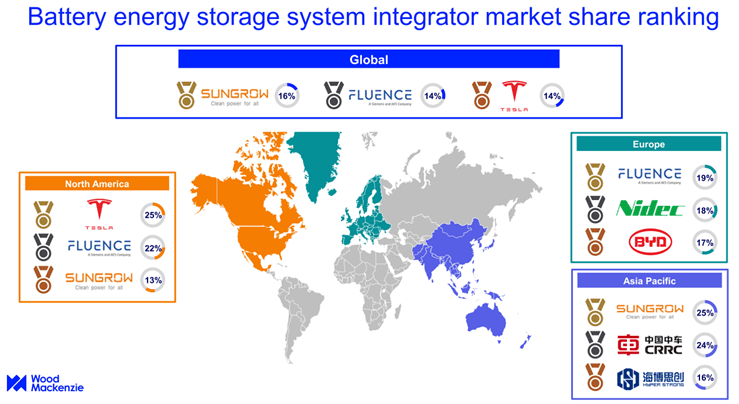

According to a Wood Mackenzie research , Sungrow dominated the market with 16% of global market share rankings by shipment (MWh), jointly followed by Fluence (14%) and Tesla (14%), Huawei (9%), and BYD (9%). However, these rankings may change rapidly, as new entrants, challenge the incumbents with their cost-effective solutions. The concern that we have for Fluence is that BESS market is becoming increasingly crowded and competitive, as more players enter the field and offer similar products at lower prices.

BESS Integrator Market Share (Wood Mackenzie)

{kind=link}

The research states that a price war has erupted among system integrators in China, where companies are trading profits for market share, lowering the industry profitability. The report further states that the fierce market competition will challenge the survival of low-profit companies in the coming years.

In alignment with the research insights, we anticipate that Fluence is going to face tough competition from the Chinese BESS integrators, who have advantages in terms of production capacity and cost efficiency. In the face of the ongoing price war, Fluence will likely need to lower its prices to remain competitive or risk losing potential contracts. This situation suggests that Fluence could face difficulties in improving its unprofitable operating margins as it competes with cheaper rivals in the market.

Non-Diversified Business Model

Fluence is a pure system integrator and its product portfolio consists mainly of two solutions: energy storage products and services, and digital software for renewables and storage assets. However, Fluence’s business model is heavily reliant on energy storage revenues, which account for 99% of its total revenue. This is a non-diversified business model which exposes Fluence to several risks, such as:

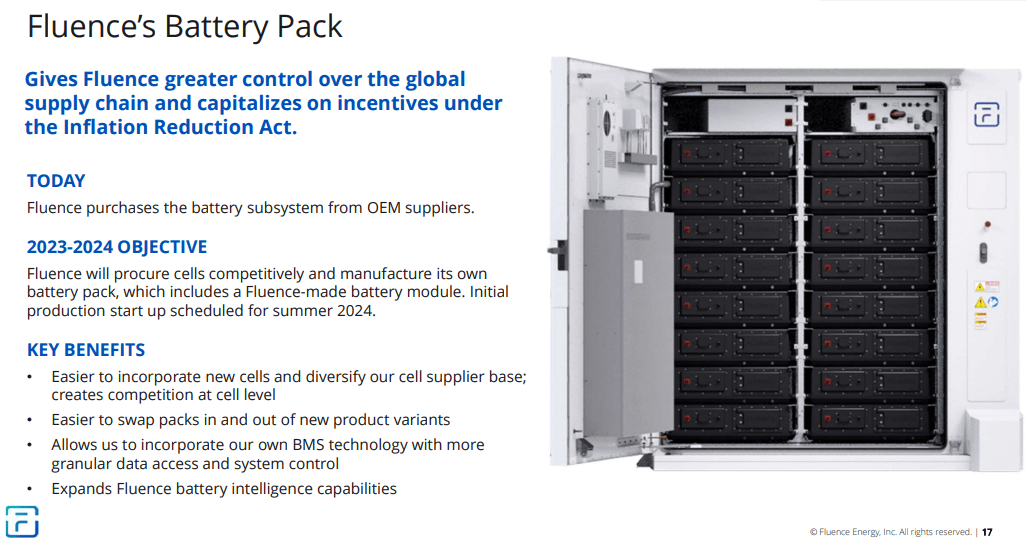

- The lack of differentiation and innovation in its energy storage products, which may become commoditized, as the market becomes more crowded and competitive. The company is working on manufacturing its own battery pack and release in mid-2024, but we are not convinced that this will give it a significant edge over its rivals.

Fluence Battery Pack (Fluence Investor Presentation)

{kind=link}

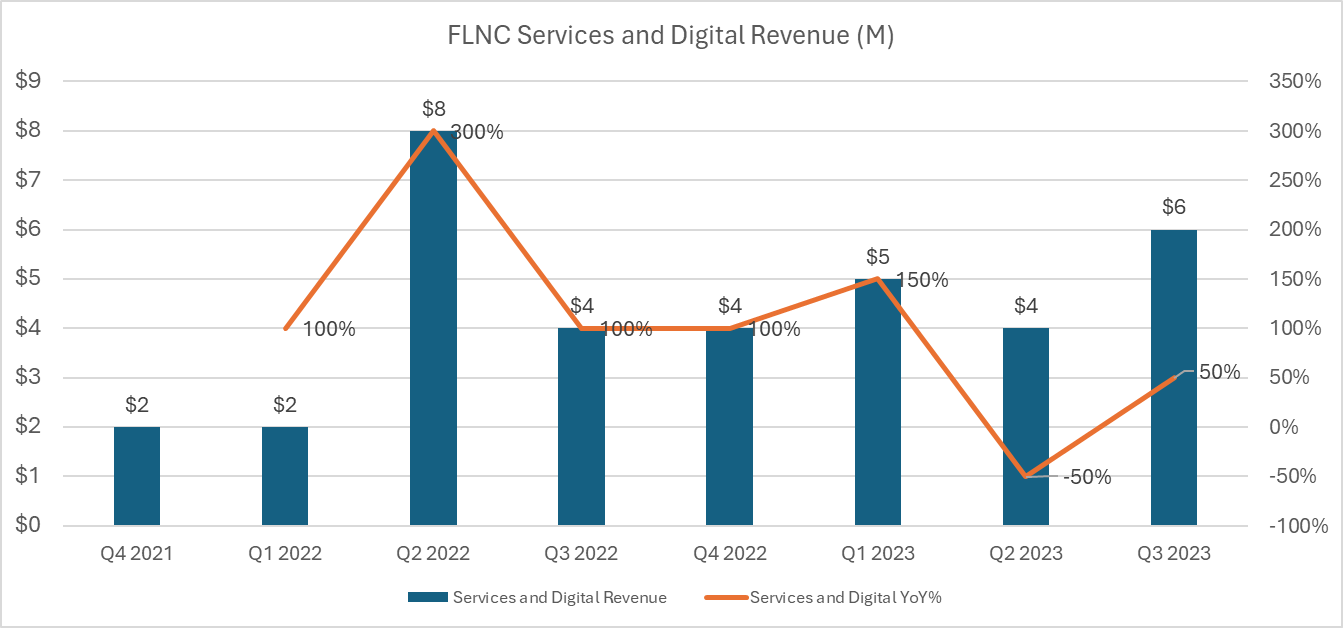

- Fluence’s software segment seems to be a weak spot in its product portfolio. It accounts for only 1% of its total revenue and has a slow growth rate (see below). We suspect that its software business is struggling to compete with other players in the market, who might offer more advanced and integrated software solutions.

Fluence Services and Digital Revenue (Author)

{kind=link}

- The cyclicality and seasonality of the energy storage market will affect the demand and pricing of the company’s energy storage products and services which is 99% of the business.

- Fluence is selling projects and has a dependence on long-term and non-recurring contracts, which may have variable or delayed revenue recognition. They are also subject to project delivery issues, which involve complex engineering, procurement, construction, and commissioning processes that could cause delays and cost overruns.

In conclusion, we think that Fluence’s non-diversified business model may limit its ability to respond to changing market conditions, supply chain challenges, and competitive dynamics, and may also increase its vulnerability to macro shocks and disruptions.

Fluence Lacks Vertical Integration and Faces Supply Chain Risks

Unlike some of its competitors, Fluence is not vertically integrated and depends on external suppliers for its battery cells, modules, and other components. This exposes the company to supply chain risks, such as shortages, delays, quality issues, and price fluctuations. The company currently depends on a few suppliers, mostly in Asia, to source the key parts for its energy storage products (Fluence has signed a deal with a US battery supplier, AESC but we are doubtful if AESC can compete with Chinese suppliers).

For instance, in the US, the energy storage supply chain is facing a new constraint due to shortage of transformers , which have a lead time of at least a year. This has a direct impact on system integrators, as transformers are integral for grid connection. Fluence may experience delays or cancellations of its projects, as it may not be able to secure enough transformers or other components in time or at a reasonable cost. For example, during the Q3 earnings call , Fluence CEO attributed the gross profit margin decrease to a supply chain delay issue.

Julian Nebreda - President and CEO:

Turning to adjusted gross profit, we delivered $24 million or a margin of approximately 4.4% for the quarter. This is slightly lower than the Q2 level of 4.6%, primarily because of one project that experienced delay from a noncore supplier. This was an isolated incident which will not hinder us from our expectation of achieving double digit gross profit margins in Q4.

Furthermore, the rising cost of raw materials may also affect the profitability and competitiveness of Fluence, as it may have to absorb the cost increase or pass it on to its customers, which may reduce its margins or market share.

Fluence also faces the risk from some of its suppliers who are or might become BESS integrators as we are witnessing in China. For instance, BYD, one of the top battery cell suppliers, is also a major integrator in the energy storage market and has a partnership with Tesla, Fluence’s biggest competitor in the United States. These are all high-risk scenarios that could threaten Fluence’s market position and growth prospects.

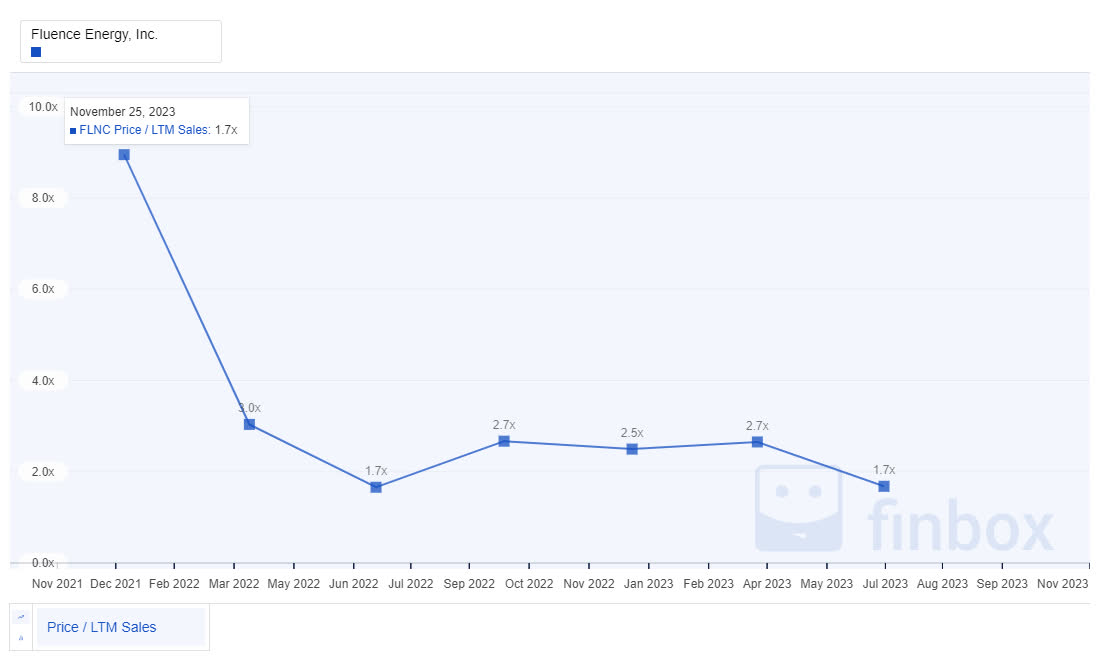

Valuation is Fair and Risks are Priced In

Fluence’s market value as of November 24, 2023 was $3.36 billion, and its P/S ratio was 1.7x (as per 177.1 million shares outstanding). This is higher than renewable energy industry's PS ratio of 1.3 which suggests that Fluence is trading at a premium value to its industry peers. We think this is due to its market-leading position.

{kind=link}

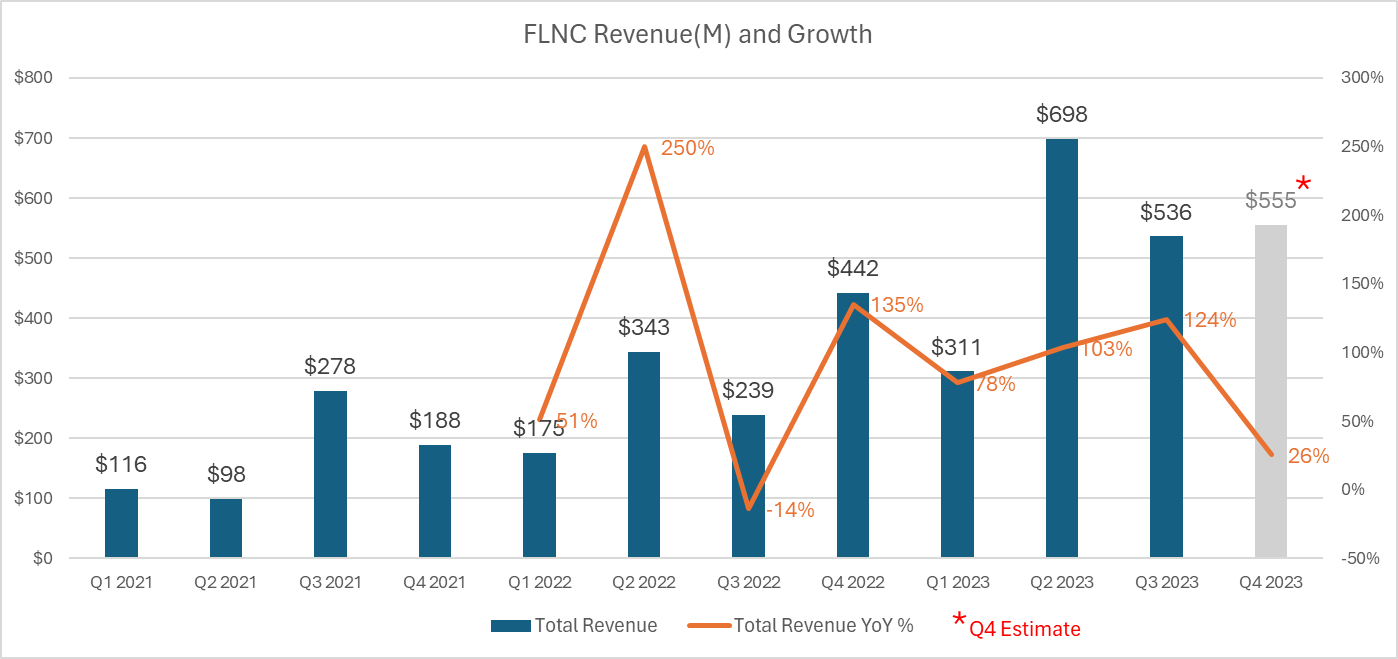

Also, we see a risk in the revenue growth trajectory. Fluence expects its Q4 revenue to range from $455 million to $555 million. Assuming they report on the higher end which is $555 million, this translates to a 26% YoY growth (see below). This is a significant deceleration on a YoY basis which is concerning.

Fluence Revenue Growth (Author)

{kind=link}

Fluence also projects a 35-40% increase in revenue for FY24. This means that the slowdown in its revenue growth will continue through FY24. Moreover, we expect that this trend will persist in FY25 and beyond, as Fluence will face increasing competition from other players in the market. These competitors, such as Tesla, Sungrow, and BYD, have clear advantages over Fluence in terms of cost efficiency, production capacity, vertical integration, and product diversity. All these factors will put pressure on Fluence’s revenue growth and margins.

In summary, we think that Fluence is fairly valued considering its market-leading position and growth trajectory. However, we do not see any positive catalysts that could improve its financial performance or market share in the near future. Therefore, we recommend Fluence as a Hold.

Upcoming Earnings

Fluence is scheduled to announce Q4 earnings on Tuesday, November 28th, 2023. Analysts expect the firm to report an EPS of -$0.07 and revenue of $518M (+17% Y/Y).

We expect the company to beat its earnings expectations, and provide FY24 outlook in line with its previous guidance (revenue growth of 35-40%, positive adj. EBITDA).

Conclusion

Fluence Energy has a strong market position in the BESS market, as it benefits from the increasing demand for clean and reliable energy, the declining cost of batteries, and the supportive government policies. It has a solid revenue trajectory, improving gross margins, and a healthy balance sheet.

However, we think Fluence’s shares have no room for growth at the current price levels, because of the following reasons: its business model is too dependent on energy storage revenues and lacks diversification, its supply chain is vulnerable to disruptions from 3rd party suppliers, and it's under pressure from both existing and new competitors.

We recommend a Hold rating for Fluence.

For further details see:

Fluence Energy: Risk Factors In The Evolving BESS Landscape