FLR - Fluor - Remaining Conservative Despite The Trend

Summary

- Fluor has been a market outperformer for the time that I have been covering it with "Hold". The company is up around 8.5% above market since November.

- This is a good RoR, and clearly, given my first article, I underestimated how the market could push the company here.

- I go through my thesis for 2023 to see if I see any reason for changes in the short term here.

Dear readers/followers,

Fluor ( FLR ) deserves an update for 2023E. This company has been on my list for about a year, unfortunately, my track record with the business has been so-so. Initially, the company fell in accordance with my targets in my first article, only to then come back with a vengeance. I view this reaction as unjustified and exaggerated, but it goes to show you that sometimes the market works against you on the negative as well.

I often find companies that are undervalued and that result in over 50-80% short-term RoR, but at times, I do the wrong stance on a company at a specific time, and the result is "missing out". I'll also be the first to admit when this is the case. There is no "maybe" in such a stance. If Stock X outperforms the market by Y%, then you as an analyst have missed the mark by Y%, and it's up to you to see how to change your approach and valuation process, if applicable , to make sure that the same doesn't happen again. Success in investing is more of a binary result, yes or no - that's what's so great about it.

Now, at times there's really no good explanation beyond irrational. And in those cases, I can't do much. However, let's see if that's the case here.

Revisiting Fluor for 2023E

Fluor isn't a strange or hard-to-read business. It might be more difficult to value than some more clear-cut companies, but at its heart, it is a holding company for a number of subs and JVs in the professional service field. Some of the respective fields are a bit difficult to get any real grip or understanding of - you might need real sector expertise to develop understanding, such as modularization services found especially in fuels, LNG, Chemicals, and nuclear, but the company also does EPC, Fabrication, infrastructure, mining and high-level project management.

Now, as before, Fluor does not have a dividend. It's a pure growth sort of business. Also, it's not as though I'm the only one with the current take on the company. In fact, the latest article as of this publishing is a bearish article, and the latest bullish one was around a year back.

The key thing that I look at here, is that Fluor's overall thesis or its negatives haven't really massively changed. Its collapse in EPS during COVID-19 was absolutely spectacular, going to around negative 785%, from a single-digit positive EPS range to a negative double-digit near-$11/share. The recovery hasn't been as explosive, even if expectations are for the company to grow back up again. Also, despite carving its dividend, the company is still at BBB-, which is always a red flag for me.

While I'm unhappy about missing out on positive RoR - I always am - doing so is part of any investor's life, and in this case, I stay true and say that in retrospect, there was no other conclusion that I would have drawn based on the data, the trends, the estimates and the fundamentals available to me at the time.

The company hasn't in any way specifically outperformed to very long-term trends. It remains a Fortune-500 business that's been listed for well over 60 year, with over 41,000 employees around the globe, and my argument has never been against the fundamental potential to capture growth from megatrends, but how this will develop over the shorter term. There are, after all, plenty of large and small infrastructure and services companies that haven't seen close to the same overall volatility seen here in Fluor in terms of earnings.

What's more, the company remains somewhat exposures to the energy sector, which I even with current trends view as a bit of a wild card. With that in mind, here are the company's segments...

{kind=link}

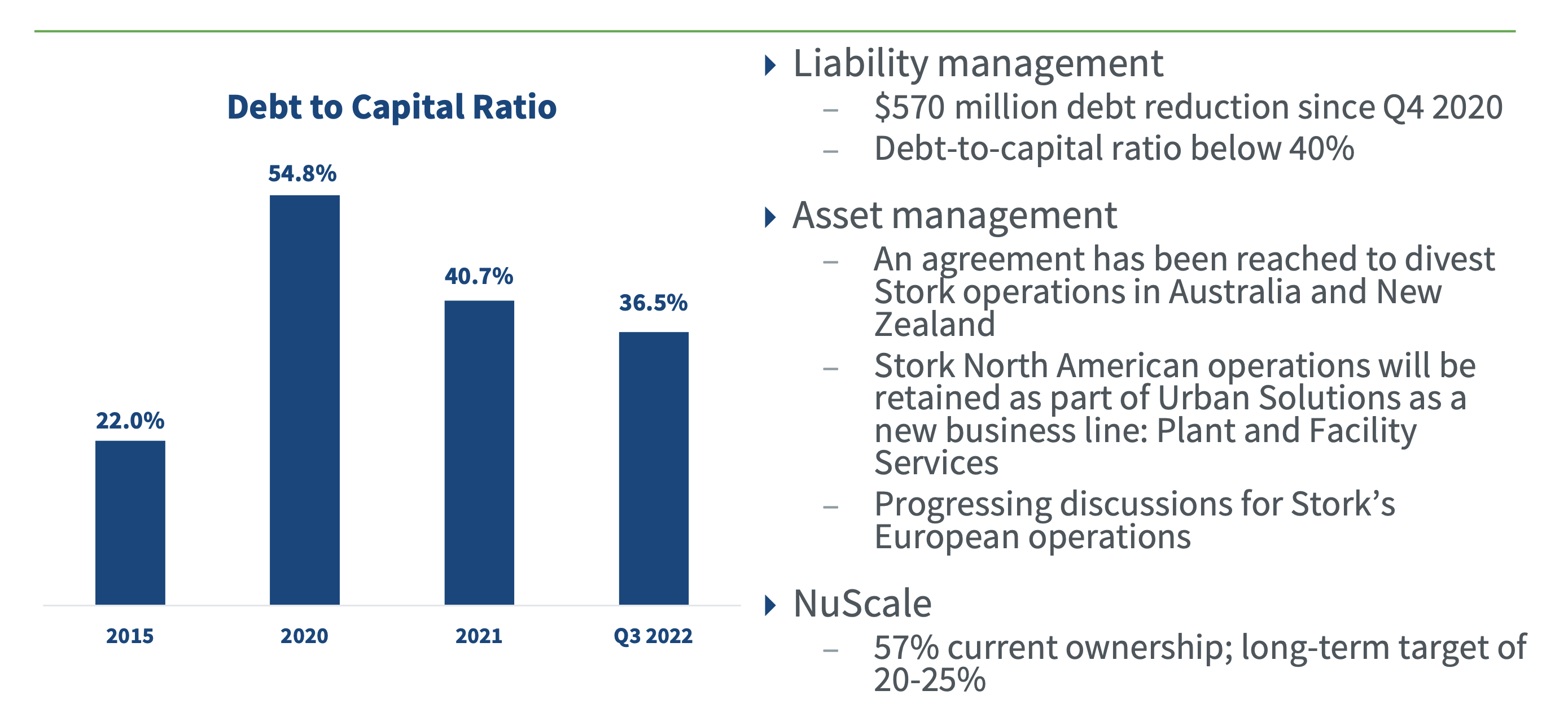

And much of the current company progress in its plans, they're relatively "soft". We do have some hard results, such as a reduction in debt reflecting a debt/cap of 36%, down from 55% during COVID-19, and an adjusted RoIC up to 9% for the 2022E. However, a lot of it is about "reinforcing company values", and enabling behaviors, together with ESG metrics, fairness and diversity metrics and gender equality pushes. Mind you, I'm not saying that these things are unimportant to today's organizations - but I'm interested in the bottom line - I only care about the person getting that bottom line insofar as he/she does it without skirting relevant laws.

The company's offerings remain fundamentally attractive, all things considered.

{kind=link}

The company is a non-trivial player in the energy transition, with offerings in renewables, H2, Clean power and storage, batteries, and carbon reduction. The latest report, however, still reports segment losses YTD (9M22), in the double-digit (millions). These results continue to reflect significant cost growth in legacy infrastructure projects, that the company can't index or ratchet up pricing for due to contracts. In many ways, this reflects what companies in Scandinavian like Skanska ( OTCPK:SKBSY ) were facing prior to changing their approach. Fluor is focusing on new business and backlog here - similar to what these infrastructure businesses did in 2012-2017, but the net result unless the contracts are actually profitable is a loss.

Fluor is doing the same thing that Skanska has already finished doing - focusing on quality above quantity in terms of contracts, but unlike many of the infrastructure businesses I follow, Fluor still has significant legacy contracts going that likely won't see much profit at all, reflected in the relatively poor RoiC. Meanwhile, the mission solutions and Energy solutions are working well, reflecting a good market and good energy prices. No issues there, so to speak - except if energy prices dip back down.

The company is also pushing LNG.

{kind=link}

Overall, the company has been able to deliver profitability - but just barely. EBITDA margins are less than 1% here and delivering an adjusted eps of less than $0.1/share. The company still has plenty of cash on hand, it has good demand (provided that contract quality is solid), and overall, it's a fairly decent outlook.

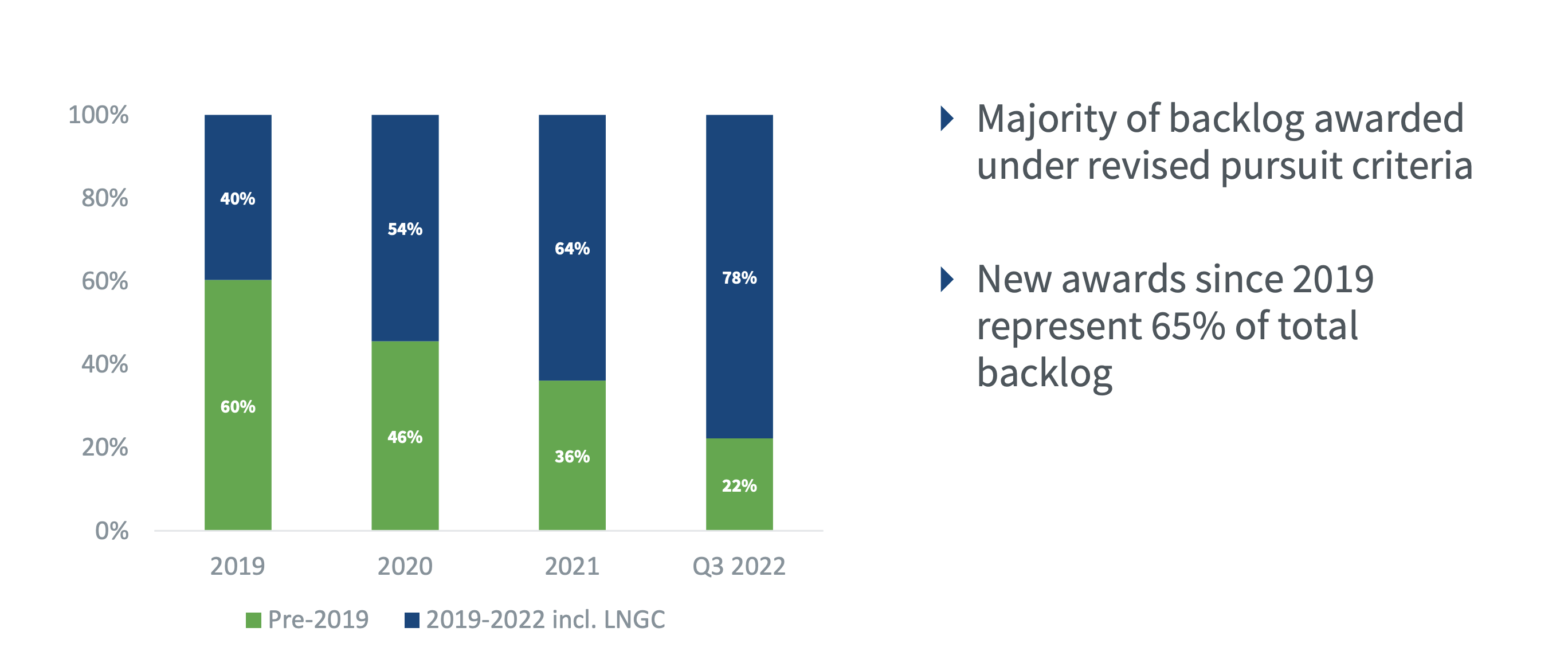

However, the company is still focusing on top-line revenues, with only a slightly increasing profit. The backlog is up - but it's still only "majority reimbursable", which calls into question how much is being pushed in terms of contract quality, which we'll see clearer going forward.

Also, let's not oversell the company's debt improvements.

{kind=link}

Still, it's no doubt that the legacy backlog is slowly disappearing, and this should result in a natural quality evolution, trickling down to the bottom line.

{kind=link}

Let's look at how this works in terms of current valuation and forecast for the company.

Fluor Forecasts & Valuation - almost 40x P/E, and close to 30x normalized

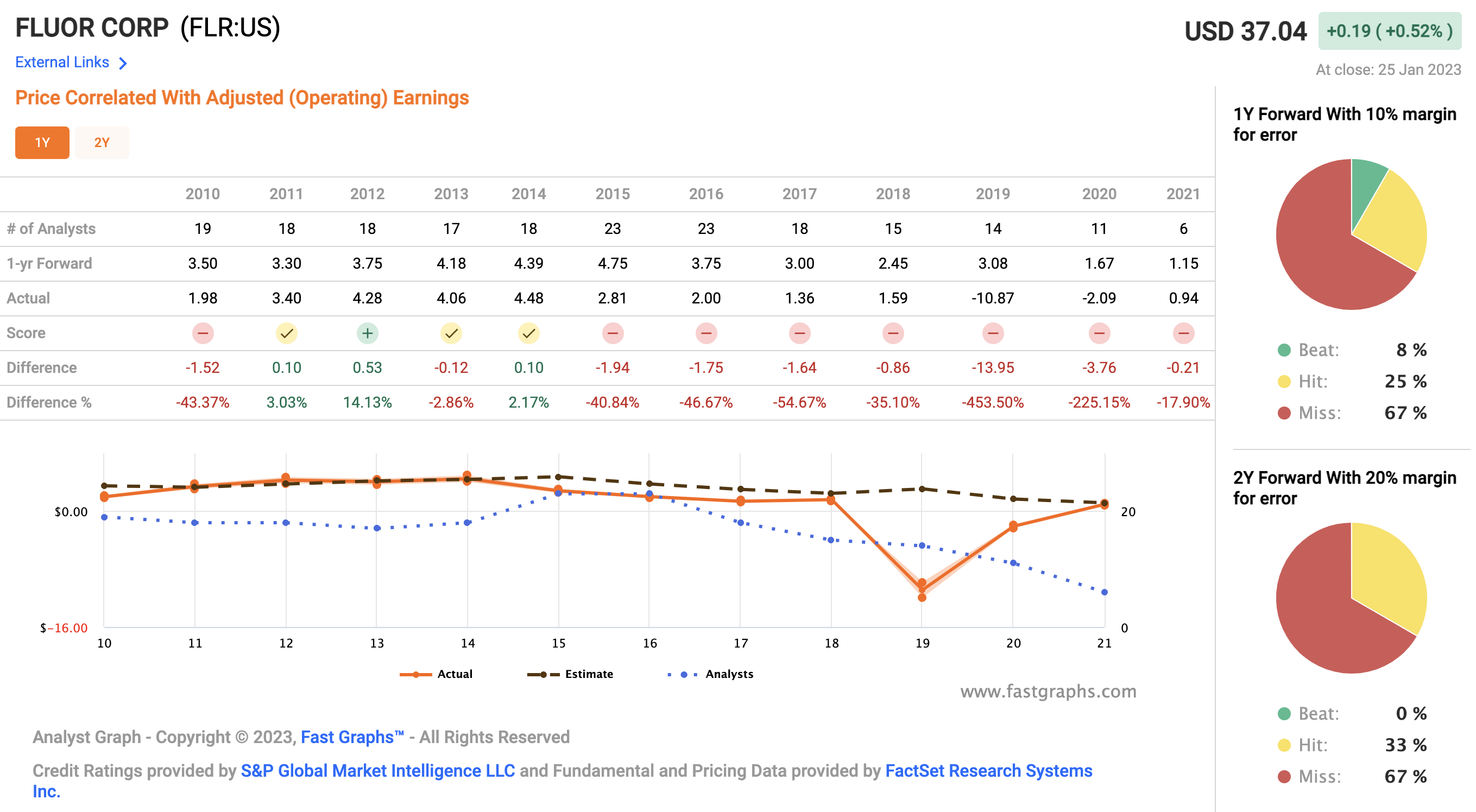

The company remains expensive. Even if we normalize the current earnings at forecasted levels, we're still looking at almost 30-33x P/E, depending on how you normalize. However, when we normalize any type of earnings with forecasted data, we need to take into consideration the forecast accuracy.

{kind=link}

Accuracy is below average here. Below-average forecast accuracy coupled with a premium valuation, in a volatile business segment/s, with recent-history instability, and a cut dividend.

That's quite a cocktail, and not one I'm really a fan of.

Even though the company has an upside at this point of double digits to a 2025E here, that's not one I consider to be all that likely or worth taking seriously here.

Fluor remains a bit of a high-risk investment. Not because the company is in a threatened position in terms of survival, but because of the relative historical volatility this business sees.

Even forecasts we can look at aren't exactly certain no matter what forecast sources or data sources we use, and it wouldn't be unfair or wrong to say that this company has already recovered to a level where, on a 2021-2022E EPS level, it has reached the valuation that it should be, based on historical multiples.

We also have zero clarity with regards to the reintroduction of the company dividend, and frankly, given where the company is today, I can't say that I blame or consider the company wrong to take this approach here. There's too much uncertainty in the company's results here, with one out of three segments not even EBITDA-profitable at this time.

An upside exists only on a premium-adjusted forecasted multiple. You need to put Fluor at above 25x P/E, and that's not something I'm willing to do here. On a 15x P/E, the forecast here is negative - even with the company's estimates growing over 80% for the coming years.

What makes me "bearish" on Fluor is forecasting the company at a far lower multiple than the market considers to be accurate or relevant, given a premium of above 25x. I believe that my justification for targeting the 15x P/E still remains strong. Keep in mind, we really have no reason in terms of results or fundamentals as to why the company has grown almost double digits in terms of share price. No new results are in.

Also, S&P global analysts, which usually are the pictures of exuberance, are entirely in agreement with me on this. The company is being followed by 8 analysts - 7 of them are at a "HOLD". They work with a range of $26.5 to $40, and average at $34.4, meaning the company is considered to be 7% overvalued at this juncture. Not exactly the most appealing valuation for a company like this, and not one I'm really willing to work with.

So, for that reason, I see no reason to make a change in terms of how I value Fluor.

If the company drops below $25.90/share , then I would consider this company a "BUY" - but even then, it would only be a buy-in of what I would consider a "vacuum". And that's not really how the market works.

Thesis

Here is my thesis on Fluor:

- Fluor has a similar problem to most construction and engineering companies. They're great companies - and I do mean great companies to invest in during an upswing.

- However, when and if these companies go into the doldrums, they can stay there for several years, and once earnings crash, they can do so to negative levels and be there for several years as well. This is more or less what happened to some of those construction companies I invested in.

- For now, I remain tepid on this company - my PT is $25.9 and I'm at a "HOLD" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

If you're interested in significantly higher returns, then I'm probably not for you. If you're interested in 10% yields, I'm not for you either.

If you, however, want to grow your money conservatively, and safely, and harvest well-covered dividends while doing so, and your timeframe is 5-30 years, then I might be for you.

Fluor is a "HOLD" here due to poor valuation and some lacking qualities

Here are my criteria and how the company fulfills them ( italicized ):

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I will call the company qualitative and fundamentally safe, but without a dividend, not cheap, and without a real solid upside. It's a "HOLD" here.

For further details see:

Fluor - Remaining Conservative Despite The Trend